Annual Report 1999/2000 Joint Runner-Up, 27Th Annual

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Singapore River Walk Traces the CITY PARK E 06169

C L D E BUS Embark On A M 06039 A O Journey That Built E R Robertson PEARL’S HILL N BUS A Nation Quay C 06161 BUS K The Singapore River Walk traces the CITY PARK E 06169 A C development of the Singapore River R U O E and its surroundings through the L V A I quays, bridges and other conserved E Alkaff Bridge R V landmarks that remind us of the V E E A communities who once lived and N R U H worked by the river. E O P Since 1819, when modern Singapore A was founded, the Singapore River has G N served as an artery of international I S commerce that drew people from all over the region to work, trade and seek their fortunes on this island. Today, MAGAZIN CLEMENCEAU AVENUE after a major clean-up that ended in 1983, the river continues to bustle with life. This clean and pleasant waterway E ROAD now flows past modern skyscrapers and historic buildings before ending at BUS Marina Bay, a freshwater reservoir 06171 since 2008. T Clemenceau E E Bridge R BUS T S 05013 S S O Tan Si Chong R Su Temple E C Legend U TONG SEN STRER BUS E P P 06189 U Collyer Quay Whampoa’s Ice House OINT Y CHINATOWN R Masjid Omar MINIST Ord Bridge BUS OCK ROADOF MANPOWERKampong Melaka Customs House ET 05022 L MERCHANTRIVERSIDE ROAD P The Cannery E R BUS ET Walk That Built A Nation A Built That 05049 LIA Embark On A Journey A On Embark BUS COURT NG Clifford Pier OSS ST 05023 HAVE Singapore River River Singapore River House River House CHINATOWN i The The Read Bridge BUS Change Alley UPPER05131 CR Former Thong Chai Read Bridge Medical Institution R E MERCHA V REET SW I Cavenagh -

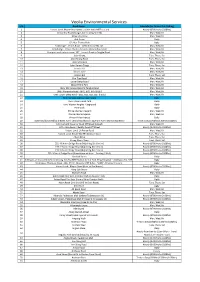

Veolia Environmental Services

Veolia Environmental Services S/N Road Name Schedule (Inc Drain Litter Picking) 1 Vacant Land: Mayne Road (next to Little India MRT station) Hourly (0700hrs to 0100hrs) 2 Alexandra Road (Ganges Ave to Leng Kee Rd) Mon, Wed, Fri 3 Alexandra View Mon, Wed, Fri 4 Ash Grove Daily 5 CP: Mar Thoma Park Daily 6 Footbridge - Jervois Road behind house No. 40 Mon, Wed, Fri 7 Footbridge - Prince Charles Crescent (Alexandra canal) Mon, Wed, Fri 8 Footpath and staircase near 107 Jervois Road to Tanglin Road Mon, Wed, Fri 9 Jalan Kilang Tues, Thurs, Sat 10 Jalan Kilang Barat Tues, Thurs, Sat 11 Jalan Membina Mon, Wed, Fri 12 Jalan Rumah Tinggi Tues, Thurs, Sat 13 Jervois Hill Mon, Wed, Fri 14 Jervois Lane Mon, Wed, Fri 15 Keppel Hill Tues, Thurs, Sat 16 Kim Tian Road Mon, Wed, Fri 17 Lower Delta Road Mon, Wed, Fri 18 Mount Echo Park Mon, Wed, Fri 19 Near 107 Jervois Road to Tanglin Road Mon, Wed, Fri 20 OHB: Alexandra Road - (B01, B03, B05 & B07) Mon, Wed, Fri 21 OHB: Lower Delta Road - (B01, B03, B05, B07 & B10) Mon, Wed, Fri 22 Park: Ganges Avenue Open Space Daily 23 Park: Kheam Hock Park Daily 24 Park: Watten Heights Playground Daily 25 Pine Walk Daily 26 Prince Charles Crescent Mon, Wed, Fri 27 Prince Charles Square Mon, Wed, Fri 28 Prince Philip Avenue Daily 29 State land bounded by sheares Ave / Central Boulevard / Bayfront Ave / Marina Boulevard Thrice a day (0700hrs/1100hrs/1500hrs) 30 URA Carpark: Spooner Road Off Street Carpark Mon, Wed, Fri 31 URA: Jalan Besar / Beatty Road Off Street Hourly (0700hrs to 0100hrs) 32 Vacant Land: 1A Peirce -

Singapore River Walk

The Singapore River Walk takes you on a journey from Collyer Quay to » DISCOVER OUR SHARED HERITAGE Robertson Quay, focusing on the contributions of the river towards Singapore’s mercantile development through the various communities who lived and worked by the river, as well as the spectacular architecture SINGAPORE RIVER and social history of the bridges that criss-cross the river, facilitating the movement of people and goods across the river at various junctures. The Singapore River Walk is adopted by American Express. WALK For more information, visit Roots.sg Supported by Roadside hawkers along the Singapore River, 1970 Collyer Quay waterfront, 1960s STAMFORD ROAD Bus River HILL STREET CONTENTS LO MRT KE YEW STREE BUS Stop Taxi BUS 04143 STAMFORD ROAD T THE SINGAPORE RIVER WALK: AN INTRODUCTION p. 1 Roads Prominent Sites BUS A HARBOUR OF HISTORY: THE SINGAPORE RIVER THROUGH TIME p. 3 Parks Heritage Sites 04111 A 14th century port and kingdom Marked Sites BUS An artery of commerce: The rise of a global port of trade River 04142 A harbour and home: Communities by the river Walkways Of landings and landmarks: The river’s quays, piers and bridges BUS A river transformed: Creating a clean and fresh waterway 04149 BUS 04167 RIV FORT AD POINTS OF ARRIVAL: THE QUAYS OF THE SINGAPORE RIVER p. 7 ER VALLEY R EET O Boat Quay CANNING Clarke Quay PARK E R BUS River House 04168 North Boat Quay and Hong Lim Quay LIANG COURT OA HILL STR Read Street and Tan Tye Place D Robertson Quay H B R I DG Ord Bridge RT Alkaff Quay and Earle Quay US Robertson B BUS NO , 04219 Y Quay 04223 R Whampoa’s OLD HILL COMMERCE ON THE WATERFRONT p. -

Nhb SGRW-Flyermap FA-CLEAN HI

Updated 14.10.15 C L D E BUS A Embark On A M 06039 Robertson O Journey That Built E Quay N R A Nation PEARL’S HILL BUS C 06161 BUS K The Singapore River Walk traces the CITY PARK E 06169 C A R development of the Singapore River U O E and its surroundings through the V L Alkaff I A quays, bridges and other conserved E Bridge R V V landmarks that remind us of the E E A communities who once lived and N R H worked by the river. U O E P Since 1819, when modern Singapore A G was founded, the Singapore River has N I served as an artery of international S commerce that drew people from all over the region to work, trade and seek their fortunes on this island. Today, MAGAZINE CLEMENCEAU AVENUE after a major clean-up that ended in 1983, the river continues to bustle with life. T his clean and pleasant waterway ROAD now flows past modern skyscrapers and historic buildings before ending at BUS 06171 Marina Bay, a freshwater reservoir Tan Si TEERTS SSORC REPPU SSORC TEERTS Clemenceau since 2008. Chong Su Bridge Temple BUS 05013 E U T O N Legend BUS 06189 Masjid G S E N S T R E E T Omar Collyer Quay Whampoa ROAD Ice House Kampong Ord CHINA Melaka TOWN Bridge CK ROAD MINISTRY RCHANT Custom House BUS OF MANPOWER 05022 ME RIVERSIDE POINT The Cannery BUS That Built A Nation A Built That Walk 05049 Embark On A Journey A On Embark River LIANG BUS COURT Clifford Pier SS STREET House 05023 HAVELO Read Singapore River River Singapore Bridge River House CHINA Former R CRO TOWN Thong Chai The The BUS Medical Change Alley UPPE 05131 Institution Read Bridge MERCHANT -

Member's Handbook

Waterways Watch Society Member’s Handbook Personal Details: Name Contact No Email Event Contact/Remarks CONTENTS History of WWS 4 WWS Fundamental Core Values 8 Boat Familiarization 9 Boat Patrol Duty & Responsibilities 10 Bicycle Patrol Duty & Responsibilities 14 Kayak Patrol Duty and Responsibilities 16 Incident Reporting 18 Guidelines for All Members 20 Boat Patrol Route 24 Bicycle Patrol Routes 25 Notes 26 Emergency Contact List 28 History of WWS Historical background The clean-up of six main rivers and canals, namely: the Singapore River, Kallang River, Geylang River, Whampoa River, Pelton Canal and Rochor Canal took place almost twenty years ago (1977-1987). It removed the major sources of pollution which included farm waste, sewage, and illegal disposal of waste water from street hawkers, vegetable wholesalers and industries. Current Situation Although these rivers and canals are now relatively clean but problems such as littering and illegal disposal of waste still exist. The current measures by PUB to protect the aesthetics of the rivers are the installation of vertical gratings at selected drain outlets placing float booms at strategic locations along the waterways and deployment of cleaning contractors on motorized boat vessels. Despite these measures, pollution along the river still persists. The best way of stopping pollution is at its source. In this case, the sources of pollution are land-based and widespread, including areas within HDB estates, food establishments, entertainment outlets, wet markets, bin centres, trade premises and commercial buildings. It would require extensive operations to comb the island and identify these sources. Obviously, our government cannot do this alone. -

Media Release for Immediate Release REVITALISED SINGAPORE RIVER WALK FOCUSES on ITS HISTORY AS the LIFELINE of SINGAPORE Singa

Media Release For immediate release REVITALISED SINGAPORE RIVER WALK FOCUSES ON ITS HISTORY AS THE LIFELINE OF SINGAPORE Singapore River Walk gets a new lease of life from American Express grant of US$160,000 “I will always recall the city, know every street and shore. Sail down the river which brings us life, winding through my Singapore.” -- Home by Dick Lee SINGAPORE, 7 October 2015 – So loved is the Singapore River by Singaporeans it was “immortalised” in Singapore’s 1998 National Day song, “Home”. Indeed, the Singapore River holds a special place in the hearts of many Singaporeans, with many fond memories forged along its banks. More than that, it has played a vital role in the growth and development of Singapore over the years, going as far back as the 19th century. From a bustling port-of-call for early merchants, the lifeline to the different communities who lived and worked along the river, to the popular hang-out spot it is today, the importance and relevance of the Singapore River has not diminished through the years. The Trail of Choice 2 And these are the reasons why the American Express Foundation has specifically chosen to adopt the Singapore River Walk, contributing US$160,000 to its first refurbishment in 10 years. Mr Cheng Heng Chew, Country Manager of American Express Singapore, said: “The Singapore River is an important part of the country’s history as this is where early commercial activities started for Singapore. At American Express, we feel that you can’t know where you are going unless you know where you have come from and that’s why we wanted to be part of this project of identifying and locating historic sites and buildings in Singapore. -

Integrated Public Cleaning Central South

Integrated Public Cleaning Central South Subject: Central South Cleaning Schedule Dear residents, The public areas within Central South region will be cleaned as per the schedule below: Schedule S/N Road Name (Inc Drain Litter Picking) 1 Ganges Avenue Daily 2 Backlane Drain: Ganges Ave Daily 3 OHB: Ganges Avenue Daily 4 Park: Ganges Avenue Open Space Daily 5 Indus Road Daily 6 ESS: 78A Indus Road (Within Multi Storey Car Park) Daily 7 Vacant Land: 1 Delta Road Daily 8 Footpath Beside Blk 79 Indus Road leading to Bus Daily Stop 9 Havelock Road (Ganges Ave to Kim Seng Rd) Daily 10 ESS: 50 Havelock Road (Standalone without fencing Daily / Wall) 11 ESS: 22A Havelock Road (Standalone with Fencing / Daily Wall) 12 ESS: 96 Havelock Road (Adjoining Bin Centre) Daily 13 ESS: 51 Havelock Road (Facing Blk 52) (Within Multi Daily Storey Car Park) 14 ESS: 51 Havelock Road (Facing Ganges Ave) (Within Daily Multi Storey Car Park) 15 Vacant Land: Along Havelock Road Daily 16 Vacant Land: Havelock Road Daily 17 ESS: 44A Beo Crescent (Within Multi Storey Car Daily Park) 18 ESS: 28A Beo Crescent (Within Multi Storey Car Daily Park) 19 Havelock Link Daily 20 Kim Seng Walk Daily 21 Zion Road (Zion Riverside FC to Kellock Rd) Daily 22 URA: Zion Road off street Daily 23 Zion Road (Ganges Ave to River Valley Rd) Daily Page 1 of 72 24 Zion Close Daily 25 Backlane Drain: Zion Close Daily 26 Vacant Land: State land at Zion Road Daily 27 Vacant Land: Zion Road (Near Blk 87) Daily 28 Kellock Road Daily 29 General Footpath - MRT Linkway Near Outram Daily Road 30 Outram