Longleaf Partners Global Fund Commentary 2Q21

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CK HUTCHISON HOLDINGS LIMITED (“CK Hutchison”) And

HUTCHISON WHAMPOA INTERNATIONAL (03/33) LIMITED (the “Issuer”) US$1,500,000,000 7.45% Guaranteed Notes due 2033 (the “Notes”) (ISIN: US44841SAC35/CUSIP: 44841SAC3/Common Code: 018124572 for Rule 144A Notes) (ISIN: USG4672CAC94/CUSIP: G4672CAC9/Common Code: 018124629 for Regulation S Notes) unconditionally and irrevocably guaranteed by CK HUTCHISON HOLDINGS LIMITED (“CK Hutchison”) and HUTCHISON WHAMPOA LIMITED In accordance with Regulation (EU) No. 596/2014 on market abuse and the law of 11 January 2008 on transparency requirements, as amended, the Issuer is filing with the Commission de Surveillance du Secteur Financier, storing with the Officially Appointed Mechanism and publishing the attached unaudited results for the six months ended 30 June 2019 of CK Hutchison, a guarantor of the Notes issued by the Issuer. The attached document was also published by CK Hutchison at 4:31 pm and 4:32 pm (Hong Kong time), 1 August 2019 on the websites of Hong Kong Exchanges and Clearing Limited and CK Hutchison, respectively. Hutchison Whampoa International (03/33) Limited Edith Shih Director and Company Secretary 1 August 2019 Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 30 JUNE 2019 HIGHLIGHTS -

Interviewed Bernard L. Madoffat the Metropolitan Correctional Center, 150 Park Row, New York, NY

This document contains information that has been collected in connection with an investigation conducted by the U.S. Securities and Exchange Commission Office of Inspector General (OIG). It contains confidential, privileged and sensitive information and should not be recopied or distributed without the express consent of the GIG. Interview of Bernard L. Madoff At approximately 3:00pm on June 17, 2009, Inspector General H. David Kotz and DeputyInspector General Noelle Frangipaneinterviewed Bernard L. Madoffat the Metropolitan Correctional Center, 150 Park Row, New York, NY. Madoff was accompanied by his attorney, Ira Lee Sorkin of the firm of Dickstein Shapiro, LLP, as well as an associate from that firm, Nicole DeBello. The interview began with IG Kotz advising Madoff of the general nature of the OIG investigation, and advising that we were investigating interactions the Securities and Exchange Commission (SEC) had with Madoff and his firm, Bernard L. Madoff Investment Securities, LLP (BLM), going back to 1992. At that point, Sorkin advised Madoff that his only obligation was to tell the truth during the interview. The interview began with Madoff stating that the prosecutor and trustee in the criminal case "misunderstood" things he said during the proffer, and as a result, there is a lot of misinformation being circulated about this scandal, however, he added, "I'm not saying I'm not guilty." 2006 Exam: Madoff recalled that with respect to the 2006 OCIE exam, "two young fellows," (Lamore and Ostrow) came in "under the guise of doing a routine exam;" He said that during that time period, sweeps were being done of hedge funds that focused on ~-ont- running, and that was why he believed Ostrow and Lamore were at BLM. -

Stock Code Stock Name Margin Category HK 1 CK HUTCHISON HOLDINGS LTD

UOB KAY HIAN (SINGAPORE) PRIVATE LIMITED MARGIN STOCK LIST - HONG KONG MARKET 1 April 2021 Stock Code Stock Name Margin Category HK 1 CK HUTCHISON HOLDINGS LTD. SA HK 2 CLP HOLDINGS LTD. A HK 3 HONG KONG AND CHINA GAS CO. LTD. A HK 4 WHARF (HOLDINGS) LTD. A HK 5 HSBC HOLDINGS PLC SA HK 6 POWER ASSETS HOLDINGS LTD. SA HK 8 PCCW LTD. C HK 10 HANG LUNG GROUP LTD. A HK 11 HANG SENG BANK LTD. SA HK 12 HENDERSON LAND DEVELOPMENT CO. LTD. A HK 14 HYSAN DEVELOPMENT CO. LTD. B HK 16 SUN HUNG KAI PROPERTIES LTD. SA HK 17 NEW WORLD DEVELOPMENT CO. LTD. A HK 19 SWIRE PACIFIC LTD. 'A' A HK 23 BANK OF EAST ASIA, LTD. A HK 27 GALAXY ENTERTAINMENT GROUP LTD. A HK 38 FIRST TRACTOR CO LTD. - H SHARES D HK 41 GREAT EAGLE HOLDINGS LTD. C (Max Net Loan H$10M) HK 45 HONGKONG AND SHANGHAI HOTELS, LTD. B (Max Net Loan H$10M) HK 53 GUOCO GROUP LTD. B (Max Net Loan H$10M) HK 56 ALLIED PROPERTIES (HK) LTD. D HK 62 TRANSPORT INTERNATIONAL HOLDINGS LTD. D (Max Net Loan H$1M) HK 66 MTR CORPORATION LTD. SA HK 69 SHANGRI-LA ASIA LTD. A HK 81 CHINA OVERSEAS GRAND OCEANS GROUP LTD. C HK 83 SINO LAND CO. LTD. A HK 86 SUN HUNG KAI & CO. LTD. D HK 87 SWIRE PACIFIC LTD. 'B' A (Max Net Loan H$10m) HK 101 HANG LUNG PROPERTIES LTD. A HK 107 SICHUAN EXPRESSWAY CO. -

STOXX Hong Kong All Shares 50 Last Updated: 01.12.2016

STOXX Hong Kong All Shares 50 Last Updated: 01.12.2016 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) KYG875721634 BMMV2K8 0700.HK B01CT3 Tencent Holdings Ltd. CN HKD Y 128.4 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 69.3 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.3 3 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 57.5 4 3 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 37.7 5 5 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 32.6 6 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 32.0 7 6 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.5 8 8 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 26.5 9 9 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.4 10 15 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 19.4 11 10 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. CN HKD Y 18.9 12 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 18.3 13 13 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 17.9 14 11 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.8 15 14 HK0688002218 6192150 0688.HK 619215 China Overseas Land & Investme CN HKD Y 14.8 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 14.6 17 17 CNE1000003W8 6226576 0857.HK CN0065 PetroChina Co Ltd 'H' CN HKD Y 13.5 18 19 HK0003000038 6436557 0003.HK 643655 Hong Kong & China Gas Co. -

CENTURYLINK, INC. (Name of Issuer)

SECURITIES AND EXCHANGE COMMISSION FORM SC 13D Schedule filed to report acquisition of beneficial ownership of 5% or more of a class of equity securities Filing Date: 2017-05-08 SEC Accession No. 0001011438-17-000194 (HTML Version on secdatabase.com) SUBJECT COMPANY CENTURYLINK, INC Mailing Address Business Address 100 CENTURYLINK DR P O BOX 4065 CIK:18926| IRS No.: 720651161 | State of Incorp.:LA | Fiscal Year End: 1231 P O BOX 4065 100 CENTURYLINK DR Type: SC 13D | Act: 34 | File No.: 005-30739 | Film No.: 17823558 MONROE LA 71203 MONROE LA 71203 SIC: 4813 Telephone communications (no radiotelephone) 3183889000 FILED BY Corvex Management LP Mailing Address Business Address 667 MADISON AVENUE 667 MADISON AVENUE CIK:1535472| IRS No.: 274190685 | State of Incorp.:DE | Fiscal Year End: 1231 NEW YORK NY 10065 NEW YORK NY 10065 Type: SC 13D (212) 474 6700 Copyright © 2017 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 13D Under the Securities Exchange Act of 1934 (Amendment No. )* CENTURYLINK, INC. (Name of Issuer) COMMON STOCK, $1.00 PAR VALUE (Title of Class of Securities) 156700106 (CUSIP Number) Keith Meister Patrick J. Dooley, Esq. Corvex Management LP 667 Madison Avenue New York, NY 10065 (212) 474-6700 Jeffrey L. Kochian Akin Gump Strauss Hauer & Feld LLP One Bryant Park New York, NY 10036 (212) 872-8069 (Name, Address and Telephone Number of Person Authorized to Receive Notices and Communications) May 4, 2017 (Date of Event Which Requires Filing of this Statement) If the filing person has previously filed a statement on Schedule 13G to report the acquisition that is the subject of this Schedule 13D, and is filing this schedule because of §§240.13d-1(e), 240.13d-1(f) or 240.13d-1(g), check the following box. -

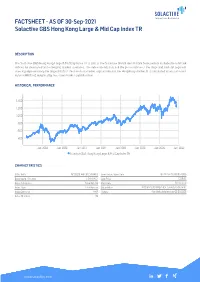

FACTSHEET - AS of 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR

FACTSHEET - AS OF 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR DESCRIPTION The Solactive GBS Hong Kong Large & Mid Cap Index TR is part of the Solactive Global Benchmark Series which includes benchmark indices for developed and emerging market countries. The index intends to track the performance of the large and mid cap segment covering approximately the largest 85% of the free-float market capitalization in the Hong Kong market. It is calculated as a totalreturn index in HKD and weighted by free-float market capitalization. HISTORICAL PERFORMANCE 1,400 1,200 1,000 800 600 400 Jan-2008 Jan-2010 Jan-2012 Jan-2014 Jan-2016 Jan-2018 Jan-2020 Jan-2022 Solactive GBS Hong Kong Large & Mid Cap Index TR CHARACTERISTICS ISIN / WKN DE000SLA4H36 / SLA4H3 Base Value / Base Date 462.12 Points / 08.05.2006 Bloomberg / Reuters / .SHKLMCT Last Price 1256.93 Index Calculator Solactive AG Dividends Reinvested Index Type Total Return Calculation 8:00 am to 10:30 pm (CET), every 15 seconds Index Currency HKD History Available daily back to 08.05.2006 Index Members 52 FACTSHEET - AS OF 30-Sep-2021 Solactive GBS Hong Kong Large & Mid Cap Index TR STATISTICS 30D 90D 180D 360D YTD Since Inception Performance -6.80% -10.27% -11.73% 9.67% -4.51% 171.99% Performance (p.a.) - - - - - 6.71% Volatility (p.a.) 21.54% 18.63% 16.63% 17.91% 18.51% 20.09% High 1364.34 1419.58 1482.24 1493.61 1493.61 1493.61 Low 1228.29 1228.29 1228.29 1115.51 1228.29 287.41 Sharpe Ratio -2.67 -1.91 -1.34 0.55 -0.32 0.33 Max. -

VOICE OVER INTERNET PROTOCOL (Voip)

S. HRG. 108–1027 VOICE OVER INTERNET PROTOCOL (VoIP) HEARING BEFORE THE COMMITTEE ON COMMERCE, SCIENCE, AND TRANSPORTATION UNITED STATES SENATE ONE HUNDRED EIGHTH CONGRESS SECOND SESSION FEBRUARY 24, 2004 Printed for the use of the Committee on Commerce, Science, and Transportation ( U.S. GOVERNMENT PUBLISHING OFFICE 22–462 PDF WASHINGTON : 2016 For sale by the Superintendent of Documents, U.S. Government Publishing Office Internet: bookstore.gpo.gov Phone: toll free (866) 512–1800; DC area (202) 512–1800 Fax: (202) 512–2104 Mail: Stop IDCC, Washington, DC 20402–0001 VerDate Nov 24 2008 14:00 Dec 07, 2016 Jkt 075679 PO 00000 Frm 00001 Fmt 5011 Sfmt 5011 S:\GPO\DOCS\22462.TXT JACKIE SENATE COMMITTEE ON COMMERCE, SCIENCE, AND TRANSPORTATION ONE HUNDRED EIGHTH CONGRESS SECOND SESSION JOHN MCCAIN, Arizona, Chairman TED STEVENS, Alaska ERNEST F. HOLLINGS, South Carolina, CONRAD BURNS, Montana Ranking TRENT LOTT, Mississippi DANIEL K. INOUYE, Hawaii KAY BAILEY HUTCHISON, Texas JOHN D. ROCKEFELLER IV, West Virginia OLYMPIA J. SNOWE, Maine JOHN F. KERRY, Massachusetts SAM BROWNBACK, Kansas JOHN B. BREAUX, Louisiana GORDON H. SMITH, Oregon BYRON L. DORGAN, North Dakota PETER G. FITZGERALD, Illinois RON WYDEN, Oregon JOHN ENSIGN, Nevada BARBARA BOXER, California GEORGE ALLEN, Virginia BILL NELSON, Florida JOHN E. SUNUNU, New Hampshire MARIA CANTWELL, Washington FRANK R. LAUTENBERG, New Jersey JEANNE BUMPUS, Republican Staff Director and General Counsel ROBERT W. CHAMBERLIN, Republican Chief Counsel KEVIN D. KAYES, Democratic Staff Director and Chief Counsel GREGG ELIAS, Democratic General Counsel (II) VerDate Nov 24 2008 14:00 Dec 07, 2016 Jkt 075679 PO 00000 Frm 00002 Fmt 5904 Sfmt 5904 S:\GPO\DOCS\22462.TXT JACKIE C O N T E N T S Page Hearing held on February 24, 2004 ...................................................................... -

United States Court of Appeals for the Ninth Circuit

Case: 11-55577 02/12/2013 ID: 8510031 DktEntry: 43-1 Page: 1 of 46 FOR PUBLICATION UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT DICHTER-MAD FAMILY PARTNERS, No. 11-55577 LLP; PHILIP JAY DICHTER; CLAUDIA GVIRTZMAN DICHTER; RICHARD M. D.C. No. GORDON, 2:09-cv-09061- Plaintiffs-Appellants, SVW-FMO v. ORDER AND UNITED STATES OF AMERICA, OPINION Defendant-Appellee. Appeal from the United States District Court for the Central District of California Stephen V. Wilson, District Judge, Presiding Argued and Submitted January 10, 2013—Pasadena, California Filed February 12, 2013 Before: Stephen Reinhardt, Kim McLane Wardlaw, and Richard A. Paez, Circuit Judges. Order; Per Curiam Opinion Case: 11-55577 02/12/2013 ID: 8510031 DktEntry: 43-1 Page: 2 of 46 2 DICHTER-MAD FAMILY PARTNERS V. UNITED STATES SUMMARY* Federal Tort Claims Act The panel affirmed the district court’s dismissal of an action alleging claims under the Federal Tort Claims Act. The panel held that the district court correctly concluded that it lacked jurisdiction to entertain appellants’ claims because they fell within the “discretionary function” exception to the United States’ waiver of sovereign immunity in the Federal Tort Claims Act. The panel affirmed the district court’s judgment of dismissal for lack of subject matter jurisdiction, and adopted Parts I through V of the district court’s April 20, 2010 opinion, Dichter-Mad Family Partners, LLP v. United States, 707 F. Supp.2d 1016 (C.D. Cal. 2010). The panel also held that the additional allegations made in the Second Amended Complaint were insufficient to overcome the discretionary function exception to the Act’s waiver of sovereign immunity. -

2010 24Th Annual Edition

2010 24th Annual Edition SCHOOL OF ACCOUNTANCY LETTER FROM THE DIRECTOR In June of this year it was announced that the University of Nebraska – Lincoln will join the Big Ten Athletic Conference on July 1, 2011. The first thing most people thought of was the football schedule. Indeed, our sports teams align themselves with an athletic conference but academia also tends to form affiliations through athletic conferences. The decision to accept of our application to join the Big Ten was made by administrators, not football coaches, and we’re pleased to be joining this select group of academic programs. One of the unique academic benefits of joining the Big Ten is becoming a member of the Committee on Institutional Cooperation (CIC). The CIC is a consortium of Big Ten universities plus the University of Chicago that has advanced member academic missions, generated unique opportunities for students and faculty, and served the common good by sharing expertise, leveraging campus resources, and collaborating on innovative programs. Specifically, member schools share resources for academic programs and research. Library materials are shared by CIC members and students are allowed to take specialized courses from member schools and/or to study in residence on member schools’ campuses for credit at their home institution. The Big Ten Conference has a long tradition of prestigious business schools and accounting programs. For example, ten of the current eleven Big Ten undergraduate business programs are ranked in the top 50 in the country according to U.S. News & World Report (the eleventh school does not have an undergraduate business program). -

Centurylink Weighs More Expansion of Prism TV Service•

EXHIBIT 7 Press Coverage and News Articles AUSWRNews Page 1 of 1 AUSWR THE AssociATION oF U S WEsT RETIREES CenturyLink weighs more expansion of Prism TV service• By Andy Vuong The Denver Post May 6, 2011 Centurylink chief executive Glen Post indicated during a first-quarter earnings call Thursday that the next market to receive Centurylink's IPTV service will probably be in Qwest's local-phone service territory. And the rollout could come as early as this year. Post said the company expanded the service, called Prism TV, in the first quarter to three new markets: Tallahassee and Orlando, Fla., and Raleigh, N.C. Prism TV, which offers video content over a dedicated Internet network, is available in eight Legacy Centurylink!Embarq markets. Centurylink purchased Embarq in 2009 and completed its acquisition of Denver-based Qwest on April1. Post said the company will continue to expand Prism TV in 2011, ultimately reaching 1 million homes with the service by year's end. However, in response to a question from an analyst, Post said the company does not expect "any additional rollouts in the Centurylink markets" this year. "We'll be evaluating the Qwest markets in the coming months," Post said. "We do think there could be some opportunity there . .. We'll be making those decisions around midyear as far as any additional rollouts of IPTV in any of those markets." Andy Vuong:·303-954 -1209\.\ls, [email protected] or twitter.comlandwuonq http://www.uswestret iree.org/5 8112.htm 9/4/2013 Printer Friendly Version Page 1 of2 Published Apr I, 20 II Published Friday April I , 20 II CenturyLink aims to win market By Ross Boettcher WORLD-HERALD STAFF WRITER TOTAL ACCESS UNES -!f,,e;;t - {)().>; Ct'l'l ~:l"ni::afi ~ns ~';:::':....~ W~f1dstrenm \St'lm ~~ ~r~fil AJrc;;: ~'1! '001 2CIV.i 2002 2003 t.C•J.i 2005 2COS 2CV1 2c.o·~ 2CV£1 2010 I' \ ' ' 1 .- I H' 1 I ) I ~\c. -

After the Meltdown

Tulsa Law Review Volume 45 Issue 3 Regulation and Recession: Causes, Effects, and Solutions for Financial Crises Spring 2010 After the Meltdown Daniel J. Morrissey Follow this and additional works at: https://digitalcommons.law.utulsa.edu/tlr Part of the Law Commons Recommended Citation Daniel J. Morrissey, After the Meltdown, 45 Tulsa L. Rev. 393 (2013). Available at: https://digitalcommons.law.utulsa.edu/tlr/vol45/iss3/2 This Article is brought to you for free and open access by TU Law Digital Commons. It has been accepted for inclusion in Tulsa Law Review by an authorized editor of TU Law Digital Commons. For more information, please contact [email protected]. Morrissey: After the Meltdown AFTER THE MELTDOWN Daniel J. Morrissey* We will not go back to the days of reckless behavior and unchecked excess that was at the heart of this crisis, where too many were motivated only by the appetite for quick kills and bloated bonuses. -President Barack Obamal The window of opportunityfor reform will not be open for long .... -Princeton Economist Hyun Song Shin 2 I. INTRODUCTION: THE MELTDOWN A. How it Happened One year after the financial markets collapsed, President Obama served notice on Wall Street that society would no longer tolerate the corrupt business practices that had almost destroyed the world's economy. 3 In "an era of rapacious capitalists and heedless self-indulgence," 4 an "ingenious elite" 5 set up a credit regime based on improvident * A.B., J.D., Georgetown University; Professor and Former Dean, Gonzaga University School of Law. This article is dedicated to Professor Tom Holland, a committed legal educator and a great friend to the author. -

AUSWR Mission Centurylink to Continue Retiree 'Cap” for Post

2012 ISSUE 2 CenturyLink To Continue Retiree ‘Cap” for Post-1990 Medicare Management 5-Year Agreement “To Not Reduce Health Benefit” INSIDE In what is called a “partnering proposal,” AUSWR and CenturyLink announced that man- 2 — AUSWR Pres. agement Medicare-eligible retirees (and eligible Appreciation spouses and dependents) who retired after 1990, 3 — CenturyLink now have their health care subsidy payment Annual Shareholder (known as the Cap) protected through March 31, Meeting May 23 2017. Non-Medicare management who retire after 1990 are included in the Agreement. 4— Retirees’ ‘Horror’ Stories Over Health- The post-1990 Medicare-eligible man- care Changes agement retirees were eliminated from the Com- pany health care plan in the 2012 Open Enroll- 5— Help to Access ment period at the end of last year and shifted to the Service Center the Medicare open market to select a plan avail- 6—About to go onto able in their area. Medicare? CenturyLink provides a reimbursed 6— Is your Part B monthly subsidy for the Medicare costs of the Mary Ann Neuman, AUSWR reimbursement the selected plan. NWB leader, and Glen Post, President and CEO of Cen- right amount? The Company and AUSWR worked to turyLink meet at the 2012 An- create this proposal and together stated that they 7 — Understand nual Shareholders’ meeting at HRAs believe the Legacy Qwest Post-1990 Manage- the company’s headquarters in ment Retirees “will be pleased and will appreci- 8— Q&A on “the Monroe, Louisiana, in May. ate the joint efforts to provide some stability in a Agreement” climate of increasing changes to health care.” Thanks to CenturyLink’s Tammy Matthews for the pho- 9— Retiree Advocate For the detailed Questions & Answers for this state listings tos.