Malaysia Real Estate Highlights

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Destination: Malaysia a Great Place to Own a Property Complimentary Copy

Destination: Malaysia A great place to own a property Complimentary copy. Complimentary copy. for sale. Not Destination: Malaysia Contents Chapter 1 Chapter 2 Chapter 4 Why choose Malaysia? 4 A fertile land for 17 What to do before 42 economic growth you buy? More bang for your buck 5 Ease of property purchase 7 Chapter 5 Tropical weather and 8 Malaysia My Second Home 44 disaster-free land Low cost of living, 9 Chapter 6 high quality of life Thrilling treats & tracks 48 Easy to adapt and fit in 10 Must-try foods 51 Safe country 11 Must-visit places 55 Fascinating culture 12 Chapter 3 and delicious food Where to look? 22 Quality education 13 KL city centre: 24 Quality healthcare 14 Where the action is services Damansara Heights: 26 The Beverly Hills of Malaysia Cyberjaya: Model 30 smart city Useful contact numbers 58 Desa ParkCity: KL’s 32 to have in Malaysia most liveable community Mont’Kiara: Expats’ darling 34 Advertorial Johor Bahru: A residential 37 Maker of sustainable 20 hot spot next to Singapore cities — Sunway Property Penang Island: Pearl 40 The epitome of luxury 28 of the East at DC residensi A beach Destination: on one of the many pristine Malaysia islands of Sabah, Malaysia. PUBLISHED IN JUNE 26, 2020 BY The Edge Property Sdn Bhd (1091814-P) Level 3, Menara KLK, No 1 Jalan PJU 7/6, Mutiara Damansara, 47810 Petaling Jaya, Selangor, Malaysia MANAGING DIRECTOR/ EDITOR-IN-CHIEF — Au Foong Yee EDITORIAL — Contributing Editor Sharon Kam Assistant Editor Tan Ai Leng Preface Copy Editors James Chong, Arion Yeow Writers lessed with natural property is located ranging Chin Wai Lun, Rachel Chew, beauty, a multi-cul- from as low as RM350,000 for any Natalie Khoo, Chelsey Poh tural society, hardly residential property in Sarawak Photographers any natural disas- to almost RM2 million for a landed Low Yen Yeing, Suhaimi Yusuf, ters and relatively home on Penang Island. -

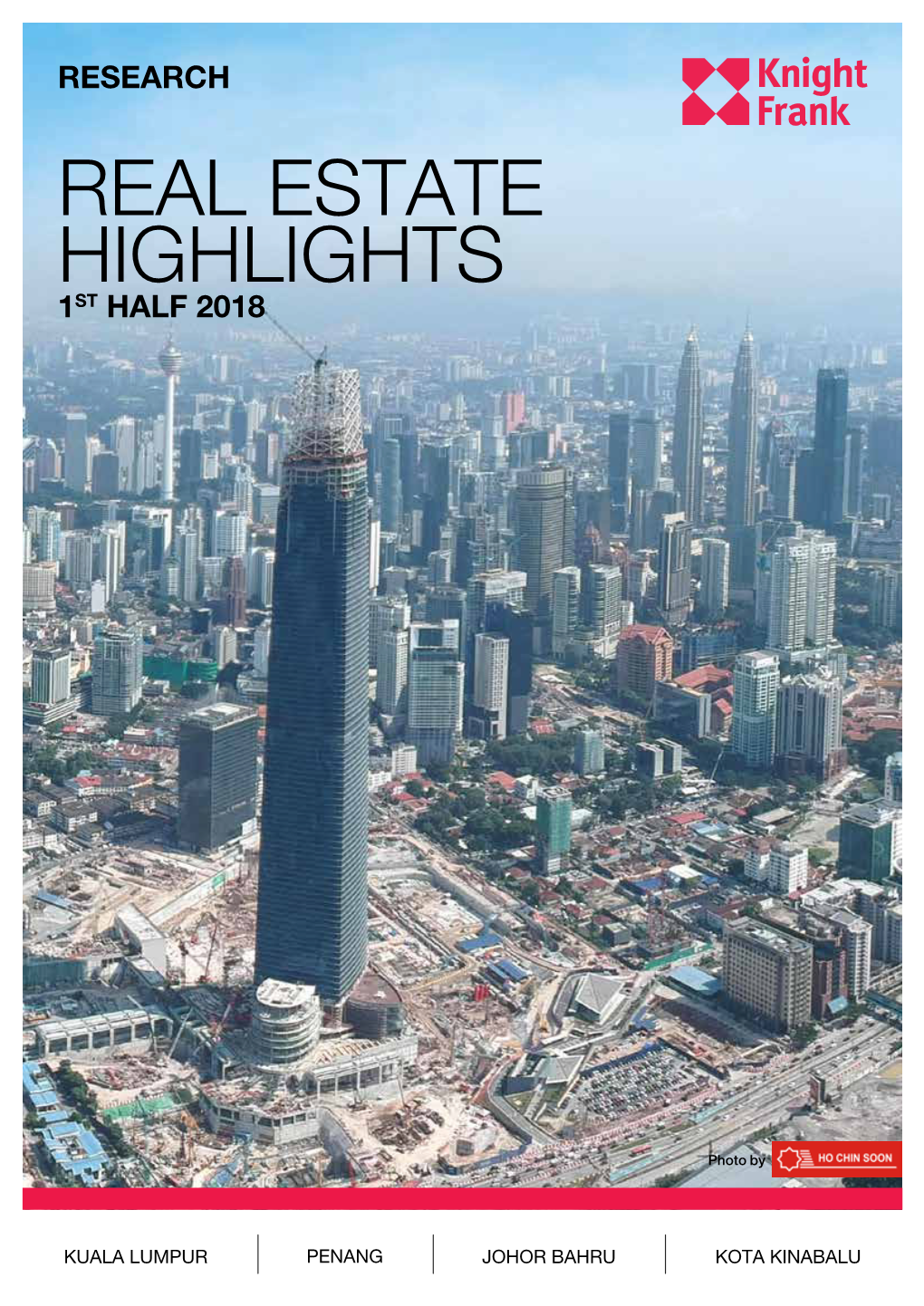

Real Estate Highlights Kuala Lumpur - Penang - Johor Bahru • 1St Half 2008

Research Real Estate Highlights Kuala Lumpur - Penang - Johor Bahru • 1st Half 2008 Contents Kuala Lumpur Hotel • Condominium Market 2 • Office Market 5 • Retail Market 8 • Hotel Market 10 Penang Property Market 12 Retail Johor Bahru Property Market 14 Residential Office Executive Summary Kuala Lumpur • The high end condominium market stabilised in the first half of 2008 in terms of take up, capital values and rentals. • Rentals and occupancies of prime offices continued to rise due to the current tight supply of good quality office buildings. • Several retail centres located at fringes of KL City are undergoing refurbishment works to remain competitive. • The performance of the hotel industry had been resilient attributed to high tourist arrivals and receipts, which led to the increase in average room rates and occupancies. Penang • Most of the high end condominium projects which are nearing completion have been sold, with prices being revised upwards. • The retail industry performed well with higher tourist arrivals in Penang. • The asking rentals of newly completed offices with better IT facilities are ranging from RM2.50 to RM3.50 per sq ft per month. Johor • The high end residential market is gaining momentum with the positive development of Iskandar Malaysia. • Prime retail centres continued to enjoy growth in rentals and occupancies. • Office sector remains healthy at an average occupancy of 70%. 2 Real Estate Highlights - Kuala Lumpur | Penang | Johor Bahru • 1st Half 2008 Knight Frank Figure 1 Projection of Cumulative Supply Kuala Lumpur High End Condominium Market for High End Condominium (2008 - 2010) Market Indications 30,000 The high end condominium market generally stabilised during the first six months of the year with one 25,000 notable new project, The Regent Residences (across Twin Towers), recording prices in excess of RM2,500 per sq ft. -

1Pay E-Wallet and Onecard Member Terms and Conditions of Use (V.4.0 01 June 2021)

1PAY E-WALLET AND ONECARD MEMBER TERMS AND CONDITIONS OF USE (V.4.0 01 JUNE 2021) Definitions 1PAY The electronic payment system which is established and managed by the Operator for 1 Utama Shopping Centre and other Bandar Utama Group entities for use by ONECARD Members by way of a 1PAY E-Wallet or by using the credit card, debit card or online banking linked in the 1Utama Mobile App or other online and offline means that may be introduced by the Operator from time to time. 1PAY E-Wallet The electronic wallet under 1PAY accessed via the 1 Utama Mobile App or a valid physical ONECARD (by swiping or tapping) which contains the ONECARD Member’s available CASH balance denominated in Ringgit Malaysia which can be used to make a 1PAY E-Wallet Transaction or a CPC Top Up. 1PAY E-Wallet Top Up When a ONECARD Member increases the CASH balance in its 1PAY E-Wallet via one or more of the methods and at any of the locations provided in Clause 29. For the avoidance of doubt, the earning of UPoints and CPC Top Ups are not 1PAY E-Wallet Top Ups. 1PAY E-Wallet Transaction A completed and successful payment made by the ONECARD Member to a Merchant for a purchase at the Merchant’s Outlet or to the Operator for a purchase on ONESHOP using the 1PAY E-Wallet which may be a payment using CASH, UPoints (through a Redemption Transaction) or a combination of the two. For the avoidance of doubt, 1PAY E-Wallet Top Ups and Direct Pull Transactions are not 1PAY E-Wallet Transactions and are not subject to the daily CASH transaction limit set out in Clause 33. -

Asian Insights Sparx

Asian Insights SparX KL-SG High Speed Rail Refer to important disclosures at the end of this report DBS Group Research . Equity 27 Jun 2019 KLCI : 1,676.61 Riding the HSR revival Success of Bandar Malaysia hinges on HSR Analyst Tjen San CHONG, CFA +60 3 26043972 [email protected] Holistic project financing is key QUAH He Wei, CFA +603 2604 3966 [email protected] Strong catalyst to revitalise property market STOCKS Top picks – IJM Corp, Gamuda, Matrix Concepts 12-mth HSR revival. Two key events unfolded in 2Q19 which could pave the Price Mkt Cap Target Price Performance (%) way for the recommencement of the Kuala Lumpur (KL)-Singapore(SG) RM US$m RM 3 mth 12 mth Rating high-speed rail (HSR) project in May 2020. First, MyHSR Corp called for a Technical Advisory Consultant (TAC) and a Commercial Advisory Gamuda 3.62 2,165 4.30 27.5 11.0 BUY Consultant (CAC) tender. Second is the revival of the Bandar Malaysia. IJM Corp 2.40 2,108 2.55 8.6 32.6 BUY Muhibbah 2.77 323 3.55 (6.1) (9.5) BUY The revival would be timely for construction as it will ensure a growth WCTEngineering Holdings Bhd 1.05 358 1.37 30.6 33.0 BUY agenda during the mid-term of the PH-led government. From an Kimlun Corp 1.40 113 2.16 15.7 2.9 BUY economic standpoint, the project would appear feasible given that the Sunway 2.02 631 1.91 9.2 8.6 HOLD KL-SG flight route remains the world’s busiest. -

The Datasheetarchive

New Product Guide Low Power Consumption Photo-IC TPS842 Outline The TPS842 is a digital-output Si photo-IC which incorporates a photodiode, an amplifier circuit and a schmitt trigger circuit in a single chip. The TPS842 is a low-voltage drive device which has been designed for 3.3-V systems. The device allows construction of low-voltage systems which thus consume less power. In addition, the sensitivity of the device is superior to that of a phototransistor. Features Compact side-view epoxy resin package (black package impermeable to visible light) Digital-output Si photo-IC which incorporates a photodiode, amplifier circuit and schmitt trigger circuit in a single chip Low-voltage drive: operating power supply voltage: VCC = 2.7 V ~ 7 V High-speed response: tpLH= 15 µs Threshold radiant incidence: EHL= 0.3 mW/cm2 (max) @Ta = 25°C Digital output: low-level output when optical input signal is received (open-collector) Direct connection to TTL and CMOS devices possible Maximum Rating (Ta = 25°C) Characteristic Symbol Rating Unit Supply Voltage VCC 7V Output Voltage VO 15 V Low-Level Output Current(Ta=Topr) IOL 8mA Operating Temperature Topr -25 ~ 85 °C Storage Temperature Tstg -40 ~ 100 °C Soldering Temperature(5s) (Note1) Tsol 260 °C Note 1: Soldering is carried out 1.3 mm from the resin which comprises the underside of the package. Optical and Electrical Characteristics (unless otherwise specified: Ta = 25° ~ 85°C and VCC = 2.7 V ~ 7 V) Characteristic Symbol Test ConditionMin Typ. Max Unit _ _ Supply Voltage VCC 2.7 7V _ High-Level Supply -

EY KL Calling 2020

KL calling: dynamic, digital, diverse Investors guide Foreword The next phase of Kuala Lumpur’s growth is pivoting towards next-gen industries, including Industry 4.0. In recent years, Kuala Lumpur has garnered investments from high-tech multinational corporations in advanced medical technologies, digital e-platforms, Internet of Things, robotics and higher-value Global Business Services. Malaysia’s world-class infrastructure, supportive government policies and agencies Dato’ Abdul Rauf Rashid and future-ready digital talent proficient in EY Asean Assurance Leader English and Asian languages continue to Malaysia Managing Partner attract international businesses to establish Ernst & Young PLT their regional headquarters and centers in Kuala Lumpur. Beyond 2020, I envision that Kuala Lumpur will holistically evolve to become a smart digital city, driven by a balanced community purpose, i.e., to serve its residents’ needs and systemically improve common facilities and amenities for the well-being of Malaysians, business residents, expatriates and international visitors. Malaysia welcomes investors to recognize Kuala Lumpur’s 3 D strengths: dynamic, digital, diverse, and participate in Kuala Lumpur’s next exciting transformation! Selamat datang ke Kuala Lumpur! KL calling: dynamic, digital, diverse | 1 Our strategy is to be as close as “possible to our customers to understand their needs and to Malaysia’s fundamentals remain develop suitable products and “ solutions to fulfil their strong and attractive to investors. requirements. As the region’s most competitive manufacturing Despite the COVID-19 pandemic, powerhouse, Kuala Lumpur we remain in active discussions emerged as a natural favorite. with potential investors. Although some investors are ABB taking a wait-and-see approach, others remain committed to their investments as they hold a long- About 16 months into our term view. -

BANDAR MALAYSIA FAQ IWH-CREC Sdn Bhd (ICSB)

BANDAR MALAYSIA FAQ IWH-CREC Sdn Bhd (ICSB) has signed a deal to acquire 60% of Bandar Malaysia Sdn Bhd (BMSB) equity from TRX City Sdn Bhd (TRXC) on 17th December 2019 for a consideration of RM6.45 billion. 1. Who is IWH-CREC Sdn Bnd (ICSB)? ICSB is a joint venture between Iskandar Waterfront Holdings Sdn Bhd (IWH) and China Railway Engineering Corp (M) Sdn Bhd (CRECM). IWH holds 60% interest in ICSB and the remaining 40% is by CRECM. CRECM is a 100% owned subsidiary of CREC. CREC is a world-leading construction conglomerate with more than 120 years history. As one of the world’s largest construction and engineering contractors, CREC takes a leading position in infrastructure construction, industrial equipment manufacturing and real estate development. Over the decades, the CREC has built more than 2/3 of China’s national railway network and 90% of China’s electrified railway. IWH shareholding is 37% Kumpulan Prasarana Rakyat Johor (KPRJ – Johor State Govt) and 63% Credence Resources (Tan Sri Dato’ Lim Kang Hoo). At the BMSB level, there will be approximately 76% Malaysian/local interest or 53% federal/state’s interest. Credence KPRJ Resources China Railway (Johor (TS Lim Engineering State Govt) Kang Hoo) Corporation 37% 63% (M) Sdn. Bhd. 100% China Railway Iskandar Engineering Waterfront Corporation (M) Holdings Sdn. Bhd Sdn. Bhd. Bhd. 60% 40% IWH CREC Sdn. Bhd. 2. Who is TRX City Sdn Bhd (TRXC)? TRXC is a wholly owned subsidiary of the Ministry of Finance, Malaysia. TRXC was formerly a subsidiary of 1Malaysia Development Bhd before it was transferred to MoF due to mounting 1MDB debts and the inability to fund the TRXC projects, including Bandar Malaysia. -

M.V. Solita's Passage Notes

M.V. SOLITA’S PASSAGE NOTES SABAH BORNEO, MALAYSIA Updated August 2014 1 CONTENTS General comments Visas 4 Access to overseas funds 4 Phone and Internet 4 Weather 5 Navigation 5 Geographical Observations 6 Flags 10 Town information Kota Kinabalu 11 Sandakan 22 Tawau 25 Kudat 27 Labuan 31 Sabah Rivers Kinabatangan 34 Klias 37 Tadian 39 Pura Pura 40 Maraup 41 Anchorages 42 2 Sabah is one of the 13 Malaysian states and with Sarawak, lies on the northern side of the island of Borneo, between the Sulu and South China Seas. Sabah and Sarawak cover the northern coast of the island. The lower two‐thirds of Borneo is Kalimantan, which belongs to Indonesia. The area has a fascinating history, and probably because it is on one of the main trade routes through South East Asia, Borneo has had many masters. Sabah and Sarawak were incorporated into the Federation of Malaysia in 1963 and Malaysia is now regarded a safe and orderly Islamic country. Sabah has a diverse ethnic population of just over 3 million people with 32 recognised ethnic groups. The largest of these is the Malays (these include the many different cultural groups that originally existed in their own homeland within Sabah), Chinese and “non‐official immigrants” (mainly Filipino and Indonesian). In recent centuries piracy was common here, but it is now generally considered relatively safe for cruising. However, the nearby islands of Southern Philippines have had some problems with militant fundamentalist Muslim groups – there have been riots and violence on Mindanao and the Tawi Tawi Islands and isolated episodes of kidnapping of people from Sabah in the past 10 years or so. -

Property Market 2013

Property Market 2013 www.wtw.com.my C H Williams Talhar and Wong 30.01, 30th Floor, Menara Multi-Purpose@CapSquare, 8 Jalan Munshi Abdullah, 51000 Kuala Lumpur Tel: 03-2616 8888 Fax: 03-2616 8899 KDN No. PP013/07/2012 (030726) Property Market 2013 www.wtw.com.my C H Williams Talhar and Wong 30.01, 30th Floor, Menara Multi-Purpose@CapSquare, 8 Jalan Munshi Abdullah, 51000 Kuala Lumpur Tel: 03-2616 8888 Fax: 03-2616 8899 KDN No. PP013/07/2012 (030726) CH Williams Talhar & Wong established in 1960, is a leading real estate services company in Malaysia & Brunei (headquartered in Kuala Lumpur) operating with 25 branches and associated offices. HISTORY Colin Harold Williams established C H Williams & Co, Chartered Surveyor, Valuer and Estate Agent in 1960 in Kuala Lumpur. In 1974, the company merged with Talhar & Co, a Johor-base Chartered Surveying and Valuation company under the sole-proprietorship of Mohd Talhar Abdul Rahman. With the inclusion of Wong Choon Kee, in a 3-way equal partnership arrangement, C H Williams Talhar and Wong was founded. PRESENT MANAGEMENT The Group is headed by Chairman, Mohd Talhar Abdul Rahman who guides the group on policy de- velopments and identifies key marketing strategies which have been instrumental in maintaining the strong competitive edge of WTW. The current Managing Directors of the WTW Group operations are: C H Williams Talhar & Wong Sdn Bhd Foo Gee Jen C H Williams Talhar & Wong (Sabah) Sdn Bhd Robin Chung York Bin C H Williams Talhar Wong & Yeo Sdn Bhd (operating in Sarawak) Robert Ting Kang Sung -

Kuala Lumpur

Powered by Powered by Kuala Lumpur Residential Market Update January 2019 The formation of a new government following Malaysia’s recent general election is already having a positive impact Economic indicators on the economy. Nominal quarterly GDP growth for Malaysia, Malaysia-wide unemployment, inflation and the overnight policy rate Consumer sentiment has been improving following the three month tax holiday, with the introduction of the GDP Quarter-on- Malaysia Overnight zero-rating of the Goods and Services Tax (GST), effective 1.7% Quarter Growth 3.25% Policy Rate from 1st June 2018, and the re-introduction of the Sales and Q2 2018 September 2018 Services Tax (SST) on 1st September 2018. This has been reinforced by strong employment and a low inflation rate; in Unemployment Rate Inflation Rate August 2018, unemployment levels stood at 3.4% and the 3.4% August 2018 0.2% August 2018 inflation rate was low at 0.2%. In the second quarter of 2018, the Business Conditions Index Nominal GDP growth Unemployment Rate Inflation Rate 6% (BCI), published by the Malaysian Institute of Economic Research, hit its highest level for the past 13 quarters at 5% 116.3 points. In addition, the continuing development of Kuala 4% Lumpur’s new financial district, Tun Razak Exchange, looks set 3% to further boost Malaysia’s growing financial services sector. 2% Keeping pace with rapid urbanisation is the development 1% progress of transport infrastructure in Greater Kuala Lumpur 0% (GKL). The completed and on-going Light Rail Transit (LRT) and Mass Rapid Transit (MRT) lines are enhancing mobility and -1% connectivity within the region, and helping to transform GKL -2% into a sustainable and liveable metropolis. -

Highline Residences Understand Your Credit Report Property Markettrends 2015 Designer

(w/GST) S$5.80 PRICE: Apr 2015 Apr - Mar Singapore Property Singapore Property International Property Highline Residences Understand Your Credit Report Credit Understand Your Property Market Trends 2015 MarketTrends Property Designer A Property ThatGoesAboveAndBeyond A Property Homes Crowdfunders Magazine Con t e n t s SINGAPORE PROPERTY ANALYSIS 4 Property Market Trends for 2015 6 SRX Residential Property Flash Report (Feb 2015) 9 SRX Residential Property Flash Report (Jan 2015) 11 SRX Residential Property Flash Report (Rental Market) PROPERTY SPOTLIGHT 12 SEA’s First Real Estate Crowdfunding Site CoAssets’ seals S$1 million investment – CoAssets FINANCE 13 Understanding Your Credit Report by Credit Bureau PROPERTY SHOWCASE 20 14 A property that goesAbove and Beyond – Highline Residences 16 A New Level of Inclusiveness – Sims Urban Oasis 18 The New Treasure in Jurong Lake District – Lakeville 20 The Gem of the East – Meridian 38 22 Crown At Robinson INTERNATIONAL PROPERTY ANALYSIS 52 Penang Real Estate Market – Henry Butcher Malaysia Sdn Bhd PROPERTY SHOWCASE 50 Bridging Possibilities In Phnom Penh – The Bridge 22 EVENT 62 Piscine SPLASH! Asia DESIGNER HOMES returns to Singapore and announces new show features 64 Adventure Home - Rezt & Relax Interior 70 Art Party - I-Bridge Design Pte Ltd 74 to Back Cover CROWDFUNDERS Magazine HOMEBUYERS: MCI(P)131/11/2014. ISSN 0129 - 8703 is published Bi-monthly available at bookstores & newstands at S$5.80 (w/GST). Publisher: PROPERTY MEDIA, 808 French Road #07-163 Kitchener Complex Singapore 200808. Tel: (65) 6294 4588 Fax: (65) 6294 5812. Email: [email protected]. (This issue of Homebuyers come with Crowdfunders magazine). -

Malaysia Real Estate Highlights

RESEARCH REAL ESTATE HIGHLIGHTS 1ST HALF 2016 KUALA LUMPUR PENANG JOHOR BAHRU KOTA KINABALU HIGHLIGHTS KUALA LUMPUR HIGH END CONDOMINIUM MARKET The residential market continues to remain lacklustre with lower volume and value of transactions recorded. ECONOMIC AND MARKET INDICATORS Limited project completions and new Malaysia’s economy expanded at a launches of high end condominiums / slower pace in 2015 with Gross Domestic residences during the review period. Product (GDP) growing at an annual rate of 5.0% (2014: 6.0%). For 2016, the Government has trimmed the country’s Growing pressure on rentals amid GDP growth forecast to 4 - 4.5% due to strong supply pipeline (existing and the volatility in crude oil prices and other new completions) and a challenging economic challenges. GDP continued rental market while prices in to moderate in the first quarter of 2016, the secondary market generally posting 4.2% growth, its slowest since continue to remain resilient. 3Q2009 (4Q2015: 4.5%), driven by domestic demand. Private consumption expanded by 5.3% while private Developers adopt innovative ‘push investment moderated to 2.2%. marketing’ strategies to boost Headline inflation for April 2016 registered at sales of selected projects and 2.1%. It is expected to be lower at 2% to 3% improve revenue. this year, compared to an earlier projection Aria of 2.5% to 3.5% and will continue to remain stable in 2017. (432 units) and The Residences at The Meanwhile, labour market conditions St. Regis Kuala Lumpur (160 units). continued to weaken with more retrenchment of workers, particularly in By the second half of 2016, the scheduled the manufacturing, mining and services completions of another five projects will sectors.