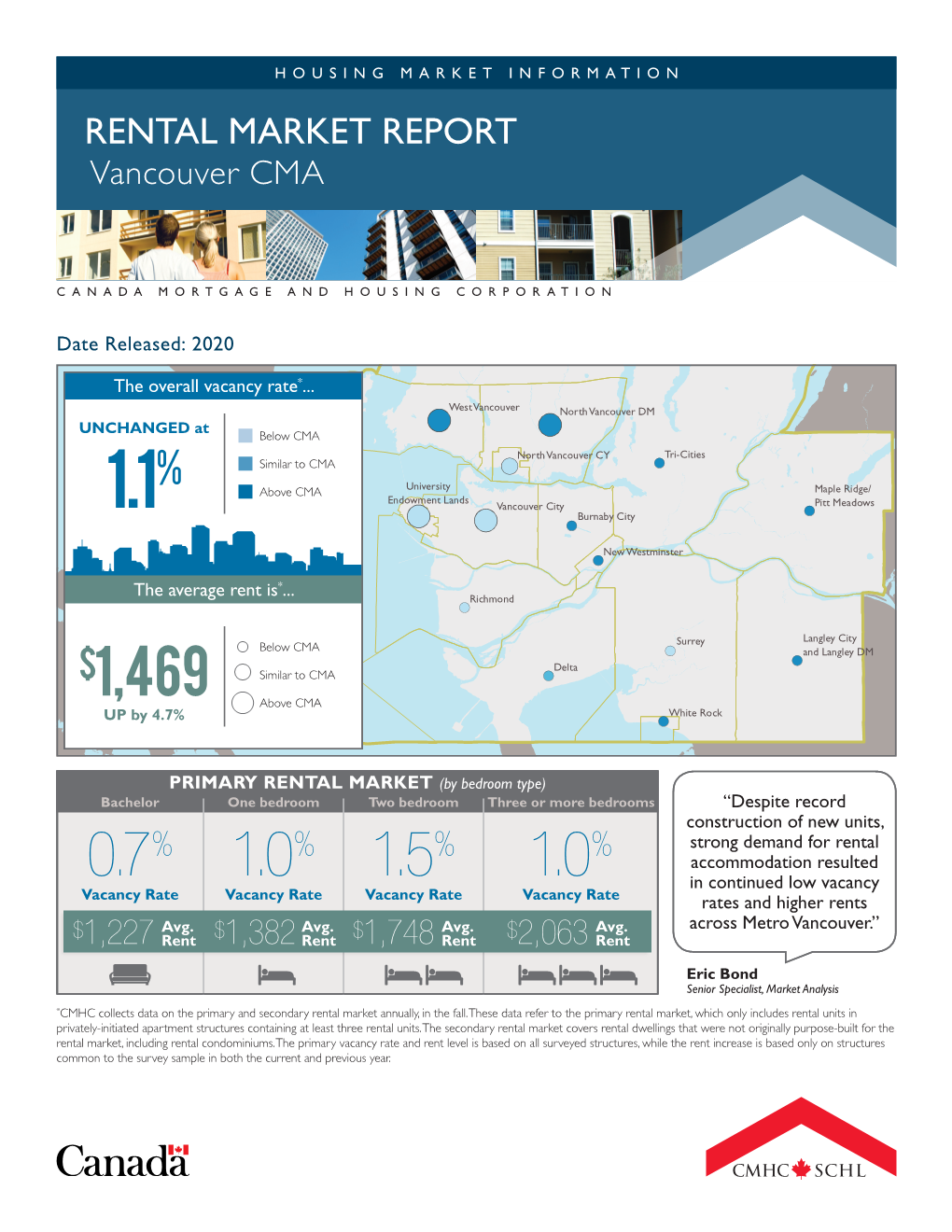

RENTAL MARKET REPORT Vancouver CMA

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vancouver Early Years Program

Early Years Programs The following is a list of Early Years Programs (EYP) in the City of Vancouver. These programs offer drop-in sessions or registered programs for families to attend with young children. These programs include: A. Community Centres: A variety of programs available for registration for families and children of all ages. B. Family Places: Programs offered include drop-ins for parents, caregivers and children, peer counseling, prenatal programs, clothing exchanges, community kitchens and nutrition education. C. Neighourhood Houses: Various programs offered for all children and families, including newcomers, such as literacy, family resource programs, childcare and much more. D. Strong Start Programs: StrongStart is a free drop-in program in some Vancouver schools that is offered to parents and caregivers with children ages zero to five years old. You must register to attend. Visit Vancouver School Board website for registration information www.vsb.bc.ca/Student_Learning/Early-Learners/StrongStart. E. Vancouver Public Libraries: Public libraries are located around the City. Many programs, such as story times are offered for children, families and caregivers. Visit www.vpl.ca for hours, programs and locations. October 2018 Westcoast Child Care Resource Centre www.wccrc.ca| www.wstcoast.org A. Community Centres Centre Name Address Phone Neighourhood Website Number Britannia 1661 Napier 604-718-5800 Grandview- www.brittnniacentre.org Woodland Champlain Heights 3350 Maquinna 604-718-6575 Killarney www.champlainheightscc.ca -

For Sale Single Tenant Investment Opportunity For5650 Dunbar Sale Street | Vancouver, Bc Single Tenant Investment Opportunity 5650 Dunbar Street | Vancouver, Bc

FOR SALE SINGLE TENANT INVESTMENT OPPORTUNITY FOR5650 DUNBAR SALE STREET | VANCOUVER, BC SINGLE TENANT INVESTMENT OPPORTUNITY 5650 DUNBAR STREET | VANCOUVER, BC DOWNTOWN VANCOUVER ENGLISH BAY KITSILANO KERRISDALE ARBUTUS RIDGE Kerrisdale Dunbar Community Elementary Centre School West 41st Avenue Dunbar Street Crofton House PROPERTY School DUNBAR- SOUTHLANDS JACK ALLPRESS* DANNY BEN-YOSEF DAVID MORRIS* Dunbar Street 604 638 1975 604 398 5221 604 638 2123 [email protected] [email protected] [email protected] *Personal Real Estate Corporation FORM RETAIL ADVISORS INC. FOR SALE SINGLE TENANT INVESTMENT OPPORTUNITY 5650 DUNBAR STREET | VANCOUVER, BC PROPERTY HIGHLIGHTS LOCATION A rare opportunity to purchase a prime C-2 zoned investment site with future • 10 minute drive to the University of British Columbia • Within close proximity to Dunbar Village, Kerrisdale, development upside in one of Vancouver’s most prestigious neighborhoods numerous schools, parks and golf courses • Situated in an affluent part of Vancouver with the primary trade area averaging a household income of $192,554 The Ivy by TBT Venture • Close proximity to various high profile developments Limited Partnership West Boulevard - 48 units of rental suites 4560 Dunbar by the Prince of Wales including 5555 Dunbar, The Dunbar/Kerrisdale, The - Completion Winter 2017 Harwood Group Secondary School - 59 units condo Stanton, The Kirkland, McKinnon and Sterling projects • Major retailers in the area include: Save-on-Foods, Shoppers Drug Mart and Stong’s Market Point Grey INVESTMENT HIGHLIGHTS Secondary Dunbar/Kerrisdale The Two Dorthies by Trasolini PROPERTY by Magellen 2020 Construction Corporation - 8 units townhouse • Single tenant property occupied by a neighbourhood 5505 Dunbar by Wesgroup liquor store, with lease running until February 2022. -

Statements and Schedules of Financial Information

Insurance Corporation of British Columbia Statements and Schedules of Financial Information Year Ended March 31, 2020 Table of Contents Statement of Financial Information Approval 1 Management’s Responsibility for the Consolidated Financial Statements 2 Independent Auditor’s Report 4 Actuary’s Report 7 Consolidated Statement of Financial Position 8 Consolidated Statement of Comprehensive Loss 9 Consolidated Statement of Changes In Equity 10 Consolidated Statement of Cash Flows 11 Notes to Consolidated Financial Statements 12 Corporate Governance 77 Schedule of Guarantees and Indemnities 78 Schedule of Debts 79 Financial Information Reconciliation 80 Remuneration and Expenses Paid to Employees 81 Remuneration and Expenses Paid to Members of the Board of Directors 101 Amounts Paid to Suppliers for Goods and Services 103 Plaintiff Firm Payments 141 Statements and Schedules of Financial Information 2019/20 Statement of Financial Information Approval The undersigned represents the Board of Directors of the Insurance Corporation of British Columbia and approves the information contained in the Statements and Schedules of Financial Information prepared in accordance with the Financial Information Act and including voluntary disclosure of other financial information. Joy MacPhail Chair of the Board of Directors September 23, 2020 1 Insurance Corporation of British Columbia Management’s Responsibility for the Consolidated Financial Statements Scope of Responsibility Management prepares the accompanying consolidated financial statements and related -

Marpole Oakridge Community Centre

Marpole-Oakridge Community Centre 990 West 59th Avenue, Vancouver, B.C., V6P 1X9 Phone 604-257-8180 Fax 604-257-8179 This attachment to the legal waiver obtains approval from the parent/guardian for their child to participate in the weekly listed activities. Youth Summer Leadership Camp 2016 Activity Consent Form Child’s First and Last Name: Male Female Parent/Guardian: Please sign your initials for each week your child is registered in. Youth Summer Leadership Camp Scheduled Out Trips: Parent/Guardian Initial Required (PT) – Public Transportation (W) – Walking (CB) – Chartered Bus Week 1 – Queen Elizabeth Park (PT), Playland (PT) Week 2 – Swimming @ Hillcrest Pool (PT), Exit The Room (PT), Workshop at Killarney CC (PT) Week 3 – Kitsilano Pool (PT), Kayaking at Jericho Beach (PT), Workshop at CHCC (PT), Community Clean Up – Marpole Neighborhood (W) Week 4 – Deliver Care Packages in the Downtown Eastside (PT/W), VPL Downtown Library (PT), Rogers Arena Tour (PT), Lonsdale Quay Summerfest (PT), VPD Workshop Mt Pleasant CC (PT) Week 5 – Splashdown Waterslides (PT/CB), Volunteering - Paint Out @ Mt Pleasant (PT) Week 6 – Town N’ Country Bowling (PT), Workshop at CHCC (PT), Photography Project – Marpole Neighborhood (W) Week 7 –Stanley Park Bike Ride (PT), Art Start Tour (PT), Ice Skating @ Sunset CC (W), Workshop at Strathcona CC (PT) Week 8 – The Fair at the PNE (PT), Seymour Creek Golf Centre (PT) Swimming Ability: Good_________ None:_________ Level:__________________________ I understand the following alternate activities may occur due to rainy days or other necessary scheduling changes: Cineplex Marine Gateway , Country Town Bowling, Hillcrest Pool, Dodgeball , Maple Grove Pool, Winona Park. -

Investment Property for Sale 245 East Hastings Street Vancouver, British Columbia

Investment Property For Sale 245 East Hastings Street Vancouver, British Columbia For further information contact JORDAN J. ENG CHRIS TSOROMOCOS Success Realty & insurance Ltd. T.R.G. Commercial Realty Ltd. 604-728-0883 604-725-4519 [email protected] [email protected] Investment Property For Sale 245 East Hastings Street Vancouver, British Columbia Location Zoning 245 East Hastings is strategically located on the north DEOD (Downtown-Eastside/Oppenheimer District) The side mid-block between Main Street and Gore Avenue zoning allows a broad variety of uses including residential, in the Downtown Eastside (DTES), the City’s oldest commercial, and light industrial. neighbourhood. East Hastings Street is the main The property lies within “Sub-Area 1 Main/Hastings” an East-West commercial corridor into Downtown important gateway to Downtown. This area is intended to Vancouver. be a high-density, mixed commercial and residential area. In close proximity is Chinatown, Gastown and The maximum density for any development is a 1.0 F.S.R. Railtown. These neighbourhoods have seen except that the Development Permit Board may permit an substantial commercial office and residential increase in the maximum floor space ratio of 5.0. development in recent years resulting from growth pressures of the Downtown Core. Subject to certain provisions, an increase in the floor space ratio is allowable for retail, service, manufacturing, or The development of the 18.4 acre Station Street site of wholesale uses. the new St. Paul’s Hospital on the False Creek will have a significant impact on economic development in the area. Property Taxes (2019): $9,104.21 Similarly, the current planning of the North East False Legal Description: Lot 14, Block 10 District Creek Area Plan (NEFC) which includes the removal Lot 196 Plan 184 of the Georgia Viaduct will bring an unprecedented population growth to the area. -

Beds & Medication Carts Roll Into Yaletown House

SUMMER 2019 FRIEND-MAKING COMMUNITY CONNECTIONS PROGRAM HIGHLIGHTS & FUNDRAISING IN OUR COMMUNITY N°63 Roof Top Garden Update Another year of sweet sounds thanks to Music Heals $6,000 grant We are pleased to announce that the Rooftop Garden will be opening in June. Thank you to everyone for their patience and understanding during BEDS & MEDICATION the renovation and roof replacement work. Special thank you to our donors Thanks to Music Heals, we have received a A lifelong pianist, Paul often jokes about whose contributions made our garden grow! fourth year consecutive grant to fund additional learning piano for over 80 years. He fondly music therapy services. recalls meeting Glenn Gould after the CARTS ROLL INTO competition, touring Europe and playing In Loving Memory of George Waterman In Loving Memory of Agnes Jones With each grant, we target a specific group around the Vancouver area. In Loving Memory of Connie KM Lau In Loving Memory of Marilyn of individuals that will benefit from these In Loving Memory of Lily and H.K. Lai and John Filewood additional services: such as our ever-increasing One day, after returning from a hospital stay YALETOWN HOUSE In Loving Memory of Bruce Yorke Interex Forest Products Ltd multicultural non-English speaking population after a surgery late last year, Paul approached In Loving Memory of Joan Marie Opsal Roger McKie & Joyce Wilson, or those socially isolated due to cognition. music therapist Mayumi Holbrook and asked if Thanks to family contributions, corporate gifts and government grants— In Loving Memory of Heather Kelleher Dressew Supply he can practice duet pieces. -

Orientation Booklet

Orientation Booklet 1. The City of Vancouver - Information ................................................................................ 3 2. Discovering Vancouver .................................................................................................... 5 3. Guide to public transit .....................................................................................................10 4. Vancouver City Facilities .................................................................................................13 Service Canada ........................................................................................................ 13 Money and Banking ................................................................................................. 15 Transferring Funds to Canada ...................................................................................... 15 Cell Phone ................................................................................................................ 16 Public Libraries ........................................................................................................ 17 Recreational Activities ............................................................................................ 17 Swimming .................................................................................................................. 17 Skating ....................................................................................................................... 17 Golf courses and lessons .......................................................................................... -

Building of the Coquitlam River and Port Moody Trails Researched and Written by Ralph Drew, Belcarra, BC, June 2010; Updated Dec 2012 and Dec 2013

Early Trail Building in the New Colony of British Columbia — John Hall’s Building of the Coquitlam River and Port Moody Trails Researched and written by Ralph Drew, Belcarra, BC, June 2010; updated Dec 2012 and Dec 2013. A recent “find” of colonial correspondence in the British Columbia Archives tells a story about the construction of the Coquitlam River and Port Moody Trails between 1862 and 1864 by pioneer settler John Hall. (In 1870 Hall pre-empted 160 acres of Crown Land on Indian Arm and became Belcarra’s first European settler.) The correspondence involves a veritable “who’s who” of people in the administration in the young ‘Colony of British Columbia’. This historic account serves to highlight one of the many challenges faced by our pioneers during the period of colonial settlement in British Columbia. Sir James Douglas When the Fraser River Gold Rush began in the spring of 1858, there were only about 250 to 300 Europeans living in the Fraser Valley. The gold rush brought on the order of 30,000 miners flocking to the area in the quest for riches, many of whom came north from the California gold fields. As a result, the British Colonial office declared a new Crown colony on the mainland called ‘British Columbia’ and appointed Sir James Douglas as the first Governor. (1) The colony was first proclaimed at Fort Langley on 19th November, 1858, but in early 1859 the capital was moved to the planned settlement called ‘New Westminster’, Sir James Douglas strategically located on the northern banks of the Fraser River. -

Communicative Regionalism and Metropolitan Growth Management Outcomes a Case Study of Three Employment Nodes in Burnaby – an Inner Suburb of Greater Vancouver

COMMUNICATIVE REGIONALISM AND METROPOLITAN GROWTH MANAGEMENT OUTCOMES A CASE STUDY OF THREE EMPLOYMENT NODES IN BURNABY – AN INNER SUBURB OF GREATER VANCOUVER by LAURA ELLEN TATE B.A., McGill University, 1988 M.A. (Planning), The University of British Columbia, 1991 A THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY in THE FACULTY OF GRADUATE STUDIES (Planning) THE UNIVERSITY OF BRITISH COLUMBIA (Vancouver) September 2009 © Laura Ellen Tate, 2009 Abstract In North America, metropolitan growth management (MGM) has been significantly influenced by what I term communicative regionalism. The latter concept is rooted in communicative planning theory, and thus stresses dialogue and consensus in problem- solving. To explore the impact of communicative regionalism on actual growth management outcomes, this dissertation investigates a case study on the implementation of communicatively-informed regional plans in metropolitan or GreaterVancouver, Canada, as they have impacted three employment nodes in suburban Burnaby. The dissertation applied a three-part methodology, involving the collection of empirical data on outcomes, analysis of plan development against communicative planning criteria, and the critical application of an Actor Network Theory (ANT) lens to better examine the relationships and interactions of key government agencies during MGM plan development and implementation. The analysis suggested mixed results in terms of goal outcomes. Notably, it found that longstanding goals for attracting office employment to a designated Regional Town Centre had not been achieved to the desired degree. In explaining how this occurred, the analysis supplied empirical evidence of recent critiques made against communicative planning theory. Such results appear to support calls made by other theorists for the development of a post- communicative approach to theory and practice. -

Top 500 Valued Residential Properties- Province

BC - TOP VALUED RESIDENTIAL PROPERTIES (2021) Value Rank Property Address Total Taxable Value ($) Jurisdiction Neighbourhood Property Type 1 3085 Point Grey Rd, Vancouver 66,828,000 200 - City of Vancouver 200002 - Kitsilano Single Family Residence 2 4707 Belmont Ave, Vancouver 60,362,000 200 - City of Vancouver 200001 - Point Grey Single Family Residence 3 James Island, James Island 57,980,000 763 - Gulf Islands Rural 763965 - Inner Islands Acreage 4 4719 Belmont Ave, Vancouver 37,340,000 200 - City of Vancouver 200001 - Point Grey Single Family Residence 5 2815 Point Grey Rd, Vancouver 34,269,000 200 - City of Vancouver 200002 - Kitsilano Single Family Residence 6 4743 Belmont Ave, Vancouver 33,839,000 200 - City of Vancouver 200001 - Point Grey Single Family Residence 7 4773 Belmont Ave, Vancouver 32,787,000 200 - City of Vancouver 200001 - Point Grey Single Family Residence 8 4857 Belmont Ave, Vancouver 31,576,000 200 - City of Vancouver 200001 - Point Grey Acreage 9 35220 Cassiar Ave, Abbotsford 31,423,000 313 - City of Abbotsford 313103 - East Abbotsford Acreage 10 2999 Point Grey Rd, Vancouver 30,649,000 200 - City of Vancouver 200002 - Kitsilano Single Family Residence 11 3489 Osler St, Vancouver 29,434,000 200 - City of Vancouver 200008 - Shaughnessy Single Family Residence 12 5695 Newton Wynd, Vancouver 28,020,000 631 - University Endowment Lands 631804 - Uel North Single Family Residence 13 Unit 3101 277 Thurlow St, Vancouver 28,005,000 200 - City of Vancouver 200028 - Coal Harbour Strata Residential 14 1388 The Crescent, Vancouver -

GVFB Community Agency Partners – 84

GVFB Community Agency Partners – 84 Date: November 13th 2020 AGENCY ADDRESS Aboriginal Front Door Society 384 Main Street, Vancouver, BC V6A 2T1 Aboriginal Mother Centre 2019 Dundas Street, Vancouver, BC V5L 1J5 AIDS Vancouver 1101 Seymour Street, Vancouver, BC V6B 5S8 Al Mitchell Place 346 Alexander Street, Vancouver, BC V6A 1C3 Antoinette Lodge 509 Hastings Street, Vancouver, BC V6A 1P9 Arco Hotel 81 West Pender Street, Vancouver, BC V6B 1R3 Bridge Housing for Women 1906 Haro St, Vancouver, BC V6G 1H7 Boundless Vancouver, Salvation Army 3213 Fraser Street, Vancouver, BC V5V 4B8 Britannia Secondary 1001 Cotton Drive, Vancouver, BC V5L 3T4 Broadway Youth Resource Centre 2455 Fraser Street, Vancouver, BC V5T 1T1 Burnaby Association for Community Inclusion 2702 Norland Avenue, Burnaby, BC V5B 3A6 Canadian Mental Health Association 300-1835 Lonsdale Avenue, North Vancouver, BC V7M 2J8 City of New Westminster 514 Carnarvon St, New Westminster, BC V3L 1C4, Canada Coast Mental Health Resource Centre 1225 Seymour Street, Vancouver, BC V6B 7B6 Collingwood Neighbourhood House 5288 Joyce Street, Vancouver, BC V5R 6C9 Community Builders Foundation 1060 Howe Street, Vancouver, BC V6Z 2T1 Directions Youth Services 1138 Burrard Street, Vancouver, BC V6Z 1Y7 Dixon Transition House 2101 Holdom Avenue, Burnaby, BC V5B 0A4 Providing healthy food to those in need Date: November 13, 2020 AGENCY ADDRESS Downtown Eastside Neighbourhood House 573 East Hastings Street, Vancouver, BC V6A 1P9 Downtown Eastside Women’s Centre 302 Columbia Street, Vancouver, BC -

Downloadasset.Aspx?Id=2126, Accessed 24 November 2013

Escape into Nature: the Ideology of Pacific Spirit Regional Park by Marina J. La Salle M.A., The University of British Columbia, 2008 B.A., Simon Fraser University, 2006 A THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY in THE FACULTY OF GRADUATE AND POSTDOCTORAL STUDIES (Anthropology) THE UNIVERSITY OF BRITISH COLUMBIA (Vancouver) July 2014 © Marina La Salle, 2014 ABSTRACT This dissertation investigates the ideology of Pacific Spirit Regional Park, an urban forest adjacent to the University of British Columbia in Vancouver, Canada. Using the tools of archaeology and anthropology, I analyse the history, landscape, performance, and discourse of the park to understand Pacific Spirit as a culturally-constructed place that embodies an ideology of imperialism. Central in this dynamic is the carefully crafted illusion of Pacific Spirit as a site of “nature,” placed in opposition to “culture,” which naturalizes the values that created and are communicated through the park and thereby neutralizes their politics. They remain, however, very political. The park as nature erases the history and heritage of the Indigenous peoples of this region, transforming Pacific Spirit into a new terra nullius—a site to be discovered and explored, militaristic themes that consistently underlie park programs and propaganda. These cultural tropes connect to produce a nationalistic settler narrative wherein class ideals of nature and community are evoked in the celebration of Canada’s history of colonialism and capitalist expansion—paradoxically, the very processes that have caused the fragmentation of communities and ecosystems. The park as nature also feeds into the portrayal of this space as having been saved from development and, as such, an environmental triumph.