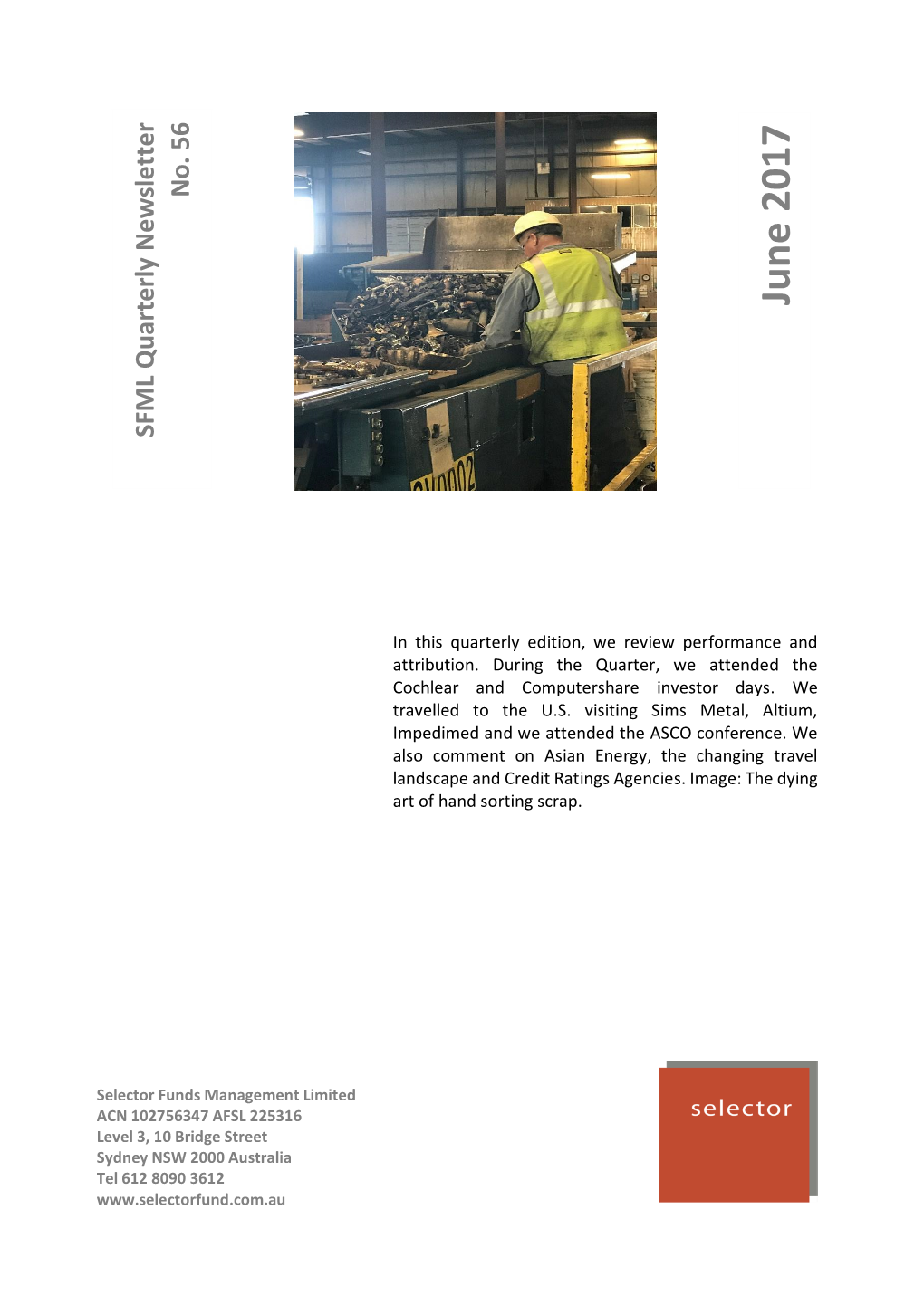

June 2017 Selector High Conviction Equity Fund Quarterly Newsletter #56

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2017 Annual Report 1 I Sirtex 2017 Highlights

2017 ANNUAL REPORT 1 I SIRTEX 2017 HIGHLIGHTS DOSES SOLD 2017 12,578 14,000 12,000 10,000 8,000 6,000 4,000 2,000 0 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 CONTENTS ABOUT SIRTEX 03 2017 FINANCIAL SUMMARY Sirtex Medical Limited is an Australian- 05 CHAIRMAN’S REPORT based global healthcare business working to 09 CHIEF EXECUTIVE OFFICER’S REPORT improve outcomes for people with cancer. 18 ENVIRONMENTAL, SOCIAL AND Our lead product is a targeted radiation GOVERNANCE therapy known as SIR-Spheres® Y-90 resin 22 BOARD OF DIRECTORS microspheres. It is available in more than 23 KEY MANAGEMENT PERSONNEL 40 countries, within over 1,090 certified hospitals to treat patients with 24 FINANCIAL REPORT inoperable liver cancer. Our business revolves around helping medical professionals understand and use our product to improve clinical outcomes and the quality of life for people with liver cancer. While at the same time, we work closely with government and private payers to ensure our patients receive the appropriate reimbursement for our product. We are challenging established practices and developing innovative new therapies that promise to improve the health and lives of many people suffering from cancer or other diseases. Our ongoing success is based on a commitment to serving our customers, professionalism, continuous improvement and innovation. ANNUAL REPORT 2017 I 2 DOSE SALES 12,578 +5.4% REVENUE $234.3m +0.8% NET LOSS AFTER TAX $26.3m -149.0% THE AMERICAS EUROPE, MIDDLE ASIA PACIFIC EAST, AFRICA Boston, United States Frankfurt, -

Sigma Emerging Companies Strategy

Sigma Emerging Companies Strategy Quarterly update as at 30 June 2017 Since Quarter FYTD 1 year 3 years 5 years Inception^ % % % % p.a. % p.a. % p.a. Sigma Emerging Companies Strategy* (1.3) 20.9 20.9 5.7 8.5 6.5 S&P/ASX Small Ord. Acc. Index (0.3) 7.0 7.0 7.1 5.7 1.7 Value added (detracted) (1.0) 13.9 13.9 (1.4) 2.8 4.8 *Gross Performance. Past performance is not a reliable indicator of future performance. ^Since Inception: 1 January 2010 Key points • Small Cap “value opportunity” clearly evident as traditional metrics remain compelling • Cyclical sectors expected to benefit as earnings bottom and risk appetite increases • Fund positioned for cyclical re-rating and away from lower return defensives Individual stock performance of note • The absence of Mayne Pharmaceuticals (-24%), Sigma The Sigma Emerging Companies Strategy (Strategy) Pharmaceuticals (32%) and Myer (-31%) contributed to underperformed a falling small cap market in the June quarter. performance in a relative sense. Stock selection was important, and generally speaking over Strategy performance was driven negatively by: the last 6 months we have seen the performance tilt away from the value recovery we saw during the first half of the financial • Infigen (-25%), lower following an earnings downgrade due year. A recovery in high PE stocks and the move towards to poor wind conditions in the final quarter which impacted more defensive positioning has proven to be a drag on the power generation. We view this as a one-off event and portfolio. -

Australian Listed Equities: Weekly Share Market Wrap

Australian Listed Equities: Weekly Share Market Wrap Total Shareholder Returns as at 15 April 2016 Price 1 week 1 month 6 months 1 year 2 years 3 years 5 years 10 years 10 years Ticker Stock Name $ % % % % % p.a. % p.a. % p.a. % p.a. ranking A2M The A2 Milk Company 1.665 -4.31 2.78 134.51 208.33 - - - - - ABC Adelaide Brighton 5.10 -1.16 6.03 26.15 17.04 19.09 19.37 12.82 10.84 34 ABP Abacus Property Group 3.10 2.99 5.08 -0.47 12.76 20.70 17.15 11.90 -1.96 105 AFI Australian Foundat. 5.53 0.18 -1.60 -4.25 -7.23 0.42 5.09 6.71 5.22 58 AGL AGL Energy Limited. 18.24 -0.65 0.55 15.71 25.25 14.52 10.63 9.90 6.32 53 AHG Automotive Holdings. 3.85 -0.52 -3.78 -1.13 -2.98 4.35 4.94 12.70 14.45 22 AIA Auckland Internation 5.75 -1.88 0.45 25.03 28.95 28.14 37.37 30.93 14.31 23 AIO Asciano Limited 8.84 1.14 -1.67 13.83 38.00 31.68 21.04 13.79 - - AIZ Air New Zealand 2.70 -0.37 9.76 4.19 3.16 27.56 39.16 31.16 13.06 24 ALL Aristocrat Leisure 10.12 4.01 1.50 14.85 23.98 45.00 42.39 29.35 -1.72 102 ALQ ALS Limited 4.38 15.57 1.15 -16.29 -1.83 -16.66 -16.64 -6.48 10.25 37 AMC Amcor Limited 14.76 1.17 4.53 15.59 5.97 25.73 23.23 20.98 11.71 29 AMP AMP Limited 5.79 5.46 2.84 3.13 -8.72 11.19 8.68 4.71 1.17 88 ANN Ansell Limited 19.68 13.30 14.42 3.31 -32.90 7.34 12.16 9.27 7.39 47 ANZ ANZ Banking Grp Ltd 23.85 7.05 -6.07 -13.17 -28.60 -9.52 0.33 6.22 3.50 72 AOG Aveo Group 3.30 0.30 4.10 16.20 24.07 30.19 38.74 -1.59 -9.34 119 APA APA Group 8.71 0.46 5.83 1.14 -1.03 22.97 17.57 21.10 11.78 28 APE AP Eagers Limited 10.00 4.06 -0.58 0.99 24.34 45.68 30.49 -

Fidelity Future Leaders Fund: Themes, Lessons and Thank You the Strong Bounce in the Australian Equity Market in Headwinds for the Economy

From the desk of James Abela March 2019 Fidelity Future Leaders Fund: Themes, lessons and thank you The strong bounce in the Australian equity market in headwinds for the economy. The Reserve Bank is becoming February was broadly interpreted as unsustainable more cautious as global growth slows and a rate cut due to lower earnings expectations and weaker looks imminent. outlooks. However, a number of companies reported For investors this will mean a greater focus on balance a more confident outlook and as a result energy, sheets as sustainability moves to front of mind. High risk/ metals, financials, technology, healthcare and low quality businesses which have experienced phenomenal industrials all performed better than expected. support in the search for yield over the last few years will Results season delivered some big positive price moves see this wane as liquidity slows and risk tolerance declines. from those quality growth stocks or cyclicals that delivered Some critical lessons from history form the foundations strong results. Altium, Appen, A2 Milk, Bluescope Steel, of my portfolio construction process: Cleanaway and Breville were notable winners. On the flipside there were some big negative price moves from 1. The Fund’s Quality, Momentum, Transition and Value those that disappointed such as Blackmores, Bingo, Pact (QMTV) framework is a balanced approach that can and Eclipx, proving that markets are still challenging deliver alpha throughout the cycle and is key from a companies that are exposed to cyclical softness or portfolio risk management perspective. competitive market structures. 2. Remember 2007 – high leverage is not an everlasting Some fundamental themes that emerged from the provider of growth. -

Realindex Australian Share Fund

Realindex Australian Share Fund Fact sheet - 31 Aug 2015 Fund strategy Fund facts The Realindex Australian Share Fund uses the RAFI® methodology in the Benchmark S&P / ASX 200 Accumulation Index construction of its portfolios which selects and weights companies Funds under management $2800.1 million according to their economic footprint defined by fundamental measures of Inception Date 17 November 2008 company size (sales, cash flow, book value and dividends). The portfolio is further enhanced by applying additional factors such as quality of earnings and debt coverage. Commentary The Realindex Australian Shares Fund returned -7.39% (gross of fees) during August 2015 outperforming the S&P/ASX 200 Accumulation Index which returned -7.79% (its worst monthly performance since October 2008). Value (-7.3%) slightly outperformed Growth (-8.0%) during the month, extending the longer-term outperformance trend (-2.4% vs. -6.1%, 12 months to 31 August 2015). This outcome is typically favourable for portfolio performance, given the Value tilt inherent in the Fundamental Indexation methodology. The Materials sector (-5.2%) was the top contributor to relative performance during the month, driven by overweight holdings in steel companies Sims Metal Management (+21.4%) and BlueScope Steel (+18.7%). Sims reported a better-than-expected FY15 result, while BlueScope committed to $200m cost out by FY17, which was well received by investors. An overweight holding in Spark New Zealand (+13.0%) led the portfolio’s outperformance in the Telecommunications sector (-8.3%). Spark rallied after announcing positive earnings growth and an annual dividend increase at its FY15 results. Spark was the top contributor to relative performance across the portfolio at a company level. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021 ASX listed securities ASX Code Security Name LVR ASX Code Security Name LVR A2M The a2 Milk Company Limited 50% CIN Carlton Investments Limited 60% ABC Adelaide Brighton Limited 60% CIP Centuria Industrial REIT 50% ABP Abacus Property Group 60% CKF Collins Foods Limited 50% ADI APN Industria REIT 40% CL1 Class Limited 45% AEF Australian Ethical Investment Limited 40% CLW Charter Hall Long Wale Reit 60% AFG Australian Finance Group Limited 40% CMW Cromwell Group 60% AFI Australian Foundation Investment Co. Ltd 75% CNI Centuria Capital Group 50% AGG AngloGold Ashanti Limited 50% CNU Chorus Limited 60% AGL AGL Energy Limited 75% COF Centuria Office REIT 50% AIA Auckland International Airport Limited 60% COH Cochlear Limited 65% ALD Ampol Limited 70% COL Coles Group Limited 75% ALI Argo Global Listed Infrastructure Limited 60% CPU Computershare Limited 70% ALL Aristocrat Leisure Limited 60% CQE Charter Hall Education Trust 50% ALQ Als Limited 65% CQR Charter Hall Retail Reit 60% ALU Altium Limited 50% CSL CSL Limited 75% ALX Atlas Arteria 60% CSR CSR Limited 60% AMC Amcor Limited 75% CTD Corporate Travel Management Limited ** 40% AMH Amcil Limited 50% CUV Clinuvel Pharmaceuticals Limited 40% AMI Aurelia Metals Limited 35% CWN Crown Limited 60% AMP AMP Limited 60% CWNHB Crown Resorts Ltd Subordinated Notes II 60% AMPPA AMP Limited Cap Note Deferred Settlement 60% CWP Cedar Woods Properties Limited 45% AMPPB AMP Limited Capital Notes 2 60% CWY Cleanaway Waste -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

FTSE World Asia Pacific

2 FTSE Russell Publications 19 August 2021 FTSE World Asia Pacific Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) a2 Milk 0.04 NEW Asustek Computer Inc 0.1 TAIWAN Cheil Worldwide 0.02 KOREA ZEALAND ASX 0.12 AUSTRALIA Cheng Shin Rubber Industry 0.03 TAIWAN AAC Technologies Holdings 0.05 HONG KONG Atlas Arteria 0.05 AUSTRALIA Chiba Bank 0.04 JAPAN ABC-Mart 0.02 JAPAN AU Optronics 0.08 TAIWAN Chicony Electronics 0.02 TAIWAN Accton Technology 0.07 TAIWAN Auckland International Airport 0.06 NEW China Airlines 0.02 TAIWAN Acer 0.03 TAIWAN ZEALAND China Development Financial Holdings 0.07 TAIWAN Acom 0.02 JAPAN Aurizon Holdings 0.05 AUSTRALIA China Life Insurance 0.02 TAIWAN Activia Properties 0.03 JAPAN Ausnet Services 0.03 AUSTRALIA China Motor 0.01 TAIWAN ADBRI 0.01 AUSTRALIA Australia & New Zealand Banking Group 0.64 AUSTRALIA China Steel 0.19 TAIWAN Advance Residence Investment 0.05 JAPAN Axiata Group Bhd 0.04 MALAYSIA China Travel International Investment <0.005 HONG KONG ADVANCED INFO SERVICE 0.06 THAILAND Azbil Corp. 0.06 JAPAN Hong Kong Advantech 0.05 TAIWAN B.Grimm Power 0.01 THAILAND Chow Tai Fook Jewellery Group 0.04 HONG KONG Advantest Corp 0.19 JAPAN Bandai Namco Holdings 0.14 JAPAN Chubu Elec Power 0.09 JAPAN Aeon 0.2 JAPAN Bangkok Bank (F) 0.02 THAILAND Chugai Seiyaku 0.27 JAPAN AEON Financial Service 0.01 JAPAN Bangkok Bank PCL (NVDR) 0.01 THAILAND Chugoku Bank 0.01 JAPAN Aeon Mall 0.02 JAPAN Bangkok Dusit Medical Services PCL 0.07 THAILAND Chugoku Electric Power 0.03 JAPAN Afterpay Touch Group 0.21 AUSTRALIA Bangkok Expressway and Metro 0.02 THAILAND Chunghwa Telecom 0.17 TAIWAN AGC 0.08 JAPAN Bangkok Life Assurance PCL 0.01 THAILAND CIMB Group Holdings 0.08 MALAYSIA AGL Energy 0.04 AUSTRALIA Bank of East Asia 0.03 HONG KONG CIMIC Group 0.01 AUSTRALIA AIA Group Ltd. -

Sep Tem B Er

4 201 Quarterly Newsletter September FML S In this quarterly edition we review performance and attribution. We profile GBST Holdings and IProperty Group. Offshore we take a look at QE and US Energy. We also consider how Technology for the Ages changes with each generation. Photo: School holidays - no worries, surfing for a 9 year old maybe as good as it gets and no technology needed. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 3, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612 www.selectorfund.com.au selector About Selector We are a boutique fund manager and we have a combined experience of over 150 years. We believe in long term wealth creation and building lasting relationships with our investors. Our focus is stock selection. Our funds are high conviction, concentrated and index unaware. As a result we have low turnover and produce tax effective returns. First we identify the best business franchises with the best management teams. Then we focus on valuations. Please forward to us contact details if you would like future newsletters to be emailed to family, friends or business colleagues. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 3, 10 Bridge Street Sydney NSW 2000, Australia Telephone 612 8090 3612 Web www.selectorfund.com.au selector September 2014 Selector High Conviction Equity Fund Quarterly Newsletter #45 Dear Investor, With the company reporting season over for another year, investor attention has quickly shifted to the road ahead. Here the simple message, proceed with caution, has been top of mind and for good reason. -

ASD NTA & Allotment Notice

Friday, 8 March 2019 ASD NTA & Allotment Notice Smartshares Limited would like to report details of the Units on Issue for the Australian Dividend Fund (ASD) as at 7 March 2019. Units on Issue: 15,304,541 Units Allotted/(Redeemed): - Net Tangible Assets (NTA): $1.61250 Tracking Difference: 1.04% The objective of the Australian Dividend Fund (ASD) is to provide a return that closely matches the return on the S&P/ASX Dividend Opportunities Index. The S&P/ASX Dividend Opportunities Index comprises the 50 highest yielding common stocks from the Australian equity market. The following companies are currently held in the Fund: Code Security description ABC Adelaide Brighton Ltd. APA APA Group API Australian Pharmaceutical Industries Ltd. ASL Ausdrill Ltd. AST AusNet Services Ltd. ASX ASX Ltd. AWC Alumina Ltd. BEN Bendigo and Adelaide Bank Ltd. CBA Commonwealth Bank of Australia CCL Coca-Cola Amatil Ltd. CTX Caltex Australia Ltd. CWN Crown Resorts Ltd. DLX DuluxGroup Ltd. DOW Downer EDI Ltd. ECX Eclipx Group Ltd. FMG Fortescue Metals Group Ltd. GUD G.U.D. Holdings Ltd. GWA GWA Group Ltd. HVN Harvey Norman Holdings Ltd. IAG Insurance Australia Group Ltd. ILU Iluka Resources Ltd. ING Inghams Group Ltd. IPH IPH Ltd. JBH JB Hi-Fi Ltd. LLC Lendlease Group MFG Magellan Financial Group Ltd. MIN Mineral Resources Ltd. MMS McMillan Shakespeare Ltd. MQG Macquarie Group Ltd. MTS Metcash Ltd. NEC Nine Entertainment Co. Holdings Ltd. NHC New Hope Corporation Ltd. PDL Pendal Group Ltd. PMV Premier Investments Ltd. RIO Rio Tinto Ltd. www.smartshares.com RRL Regis Resources Ltd. -

Annual Report Year Ended 30 June 2019

Annual Report Year Ended 30 June 2019 This annual report is dated 14 August 2019 and is signed on behalf of the Board of directors of SkyCity Entertainment Group Limited (SkyCity or the company and, together with its subsidiaries, the Group) by: Rob Campbell Bruce Carter Chair Deputy Chair An electronic copy of this annual report is available in the Investor Centre section of the company’s website at www.skycityentertainmentgroup.com ABOUT THIS ANNUAL REPORT Unless otherwise stated, all dollar amounts in this annual report are expressed in New Zealand dollars. Where appropriate, information is also provided in relation to activities that have occurred after 30 June 2019, but prior to publication of this annual report. The non-financial information in this annual report has been informed by the principles and disclosures of the Global Reporting Initiative’s (GRI) Sustainability Reporting Standards. Ernst & Young has undertaken limited assurance (in accordance with the International Standard on Assurance Engagements (New Zealand)) over disclosures associated with selected performance data included in the Sustainability section included in this annual report. A GRI reference index based on the GRI Sustainability Reporting Standards is included on pages 178–181 of this annual report. Normalised numbers are a non-GAAP financial measure. A reconciliation of reported and normalised earnings and description of the differences are provided on pages 174–177. GENERAL Year in Review 4 Creating Value 6 Performance 8 Diversity Snapshot 12 Chair’s Review