THE LOCATION PATTERN of MALLS in TEXAS a Thesis by DONGJIN

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Galleria Dallas

GALLERIA DALLAS DALLAS, TEXAS Visionary, inspiring—Galleria Dallas 4 is unquestionably the most dynamic shopping environment in North Texas. 6 The 1.4 million-square-foot shopping APARTMENT center is part of the largest mixed-use COMPLEXES complex in the Dallas/Ft. Worth metroplex and one of the largest in the country. In Broadstone On The Parkway: Stylish, addition to 200 world-class shops and sophisticated urban living, 160 units boutiques, Galleria Dallas offers an impressive lineup of dining options, Verona Rental Residences: Luxury high-rise, 142 residences a legendary ice-skating center, and The Westin Hotel. Villa Piana: New luxury resort living, 200 units 3 1 5 GALLERIA DALLAS MAJOR OFFICE Major Retailers: Macy’s, Nordstrom, Belk, 3 COMPLEXES ® American Girl, and the world’s only combined I-635 260,000 ADT Galleria North: 680,000 square feet, Banana Republic/Gap/Old Navy concept store two Class A office buildings GLA: 1,451,000 Sq. Ft. Galleria Plaza: Twelve-story tower, 2 189,000+ square feet Westin Galleria Dallas: 448 guest rooms and 2 suites plus more than 50,000 square feet of 4 5 Lincoln Centre: Three Class A office meeting space attached to Galleria Dallas 3 4 5 buildings on 33 acres, 1.7 million square feet Galleria Office Towers I, II, and III: 1.5 million Oxy Tower: 23 floors, 540,000+ square feet square feet of Class A office space attached of Class A office space to Galleria Dallas 3 5 1 ALPHA RD. 6 2 SINGLE-FAMILY HOTELS DALLAS NORTH TOLLWAY 200,000 ADT 5 RESIDENTIAL Hilton Dallas Lincoln Centre: Four-diamond luxury -

Prom 2018 Event Store List 1.17.18

State City Mall/Shopping Center Name Address AK Anchorage 5th Avenue Mall-Sur 406 W 5th Ave AL Birmingham Tutwiler Farm 5060 Pinnacle Sq AL Dothan Wiregrass Commons 900 Commons Dr Ste 900 AL Hoover Riverchase Galleria 2300 Riverchase Galleria AL Mobile Bel Air Mall 3400 Bell Air Mall AL Montgomery Eastdale Mall 1236 Eastdale Mall AL Prattville High Point Town Ctr 550 Pinnacle Pl AL Spanish Fort Spanish Fort Twn Ctr 22500 Town Center Ave AL Tuscaloosa University Mall 1701 Macfarland Blvd E AR Fayetteville Nw Arkansas Mall 4201 N Shiloh Dr AR Fort Smith Central Mall 5111 Rogers Ave AR Jonesboro Mall @ Turtle Creek 3000 E Highland Dr Ste 516 AR North Little Rock Mc Cain Shopg Cntr 3929 Mccain Blvd Ste 500 AR Rogers Pinnacle Hlls Promde 2202 Bellview Rd AR Russellville Valley Park Center 3057 E Main AZ Casa Grande Promnde@ Casa Grande 1041 N Promenade Pkwy AZ Flagstaff Flagstaff Mall 4600 N Us Hwy 89 AZ Glendale Arrowhead Towne Center 7750 W Arrowhead Towne Center AZ Goodyear Palm Valley Cornerst 13333 W Mcdowell Rd AZ Lake Havasu City Shops @ Lake Havasu 5651 Hwy 95 N AZ Mesa Superst'N Springs Ml 6525 E Southern Ave AZ Phoenix Paradise Valley Mall 4510 E Cactus Rd AZ Tucson Tucson Mall 4530 N Oracle Rd AZ Tucson El Con Shpg Cntr 3501 E Broadway AZ Tucson Tucson Spectrum 5265 S Calle Santa Cruz AZ Yuma Yuma Palms S/C 1375 S Yuma Palms Pkwy CA Antioch Orchard @Slatten Rch 4951 Slatten Ranch Rd CA Arcadia Westfld Santa Anita 400 S Baldwin Ave CA Bakersfield Valley Plaza 2501 Ming Ave CA Brea Brea Mall 400 Brea Mall CA Carlsbad Shoppes At Carlsbad -

Best Western Innsuites Hotel & Suites

Coast to Coast, Nation to Nation, BridgeStreet Worldwide No matter where business takes you, finding quality extended stay housing should never be an issue. That’s because there’s BridgeStreet. With thousands of fully furnished corporate apartments spanning the globe, BrideStreet provides you with everything you need, where you need it – from New York, Washington D.C., and Toronto to London, Paris, and everywhere else. Call BridgeStreet today and let us get to know what’s essential to your extended stay 1.800.B.SSTEET We’re also on the Global Distribution System (GDS) and adding cities all the time. Our GDS code is BK. Chek us out. WWW.BRIDGESTREET.COM WORLDWIDE 1.800.B.STREET (1.800.278.7338) ® UK 44.207.792.2222 FRANCE 33.142.94.1313 CANADA 1.800.667.8483 TTY/TTD (USA & CANADA) 1.888.428.0600 CORPORATE HOUSING MADE EASY ™ More than just car insurance. GEICO can insure your motorcycle, ATV, and RV. And the GEICO Insurance Agency can help you fi nd homeowners, renters, boat insurance, and more! ® Motorcycle and ATV coverages are underwritten by GEICO Indemnity Company. Homeowners, renters, boat and PWC coverages are written through non-affi liated insurance companies and are secured through the GEICO Insurance Agency, Inc. Some discounts, coverages, payment plans and features are not available in all states or all GEICO companies. Government Employees Insurance Co. • GEICO General Insurance Co. • GEICO Indemnity Co. • GEICO Casualty Co. These companies are subsidiaries of Berkshire Hathaway Inc. GEICO: Washington, DC 20076. GEICO Gecko image © 1999-2010. © 2010 GEICO NEWMARKET SERVICES ublisher of 95 U.S. -

General Growth Properties, Inc. Case Number: 09-11977

General Growth Properties, Inc. Attachment 4a Case Number: 09-11977 4a. Suits and Administrative Proceedings - Debtor as Plaintiff Case Name Case Number Court Name and Location GENERAL GROWTH PROPERTIES, INC. V. CHICAGO DEPARTMENT OF REVENUECASE NO. 08 TX 0182 DEPARTMENT OF ADMINISTRATIVE HEARINGS, TAX SECTION OF THE CITY OF CHICAGO If a Debtor entity does not appear as a named party in a particular line item on this Statement of Financial Affairs it is because that Debtor is named under the full case name rather than the abbreviated case caption set forth on this Schedule. If multiple Debtors are parties in a given proceeding, that proceeding will be listed on Attachment 4(a) of the Statement for each Debtor named. Attachment 4(a)(i) lists those suits where the Debtor is a Plaintiff; Attachment 4(a)(ii) lists those suits where the Debtor is a Defendant. LID: 1 1 General Growth Properties, Inc. Attachment 4a(ii) Case Number: 09-11977 4a(ii). Suits and Administrative Proceedings - Debtor as Defendant Case Name Case Number Court Name and Location ACCESS FOR THE DISABLED, INC., A FLORIDA NOT FOR PROFIT CORPORATION, AND DENISE 6:08-CV-1645-ORL-31- UNITED STATES DISTRICT COURT MIDDLE DISTRICT OF PAYNE, INDIVIDUALLY, V. GENERAL GROWTH PROPERTIES, A FOREIGN TRUST DAB FLORIDA; FLORIDA ACCESS FOR THE DISABLED, INC., A FLORIDA NOT-FOR-PROFIT CORPORATION, AND DENISE CASE NO. 1:09-CV-43 U.S. DISTRICT COURT FOR THE WESTERN DISTRICT OF PAYNE, INDIVIDUALLY V. GENERAL GROWTH PROPERTIES, INC., A DELAWARE CORPORATION MICHIGAN, SOUTHERN DIVISION; MICHIGAN AILEEN BETANCOURT-ESPADA V. -

Official Rules

OFFICIAL RULES NO PURCHASE OR PAYMENT NECESSARY TO ENTER OR WIN. A PURCHASE OR PAYMENT WILL NOT INCREASE AN ENTRANT’S CHANCES OF WINNING. OPEN TO LEGAL RESIDENTS OF THE UNITED STATES AND THE DISTRICT OF COLUMBIA (EXCLUDING FLORIDA, NEW YORK AND RHODE ISLAND) WHO ARE AT LEAST 18 YEARS OF AGE AT THE TIME OF ENTRY. VOID IN FLORIDA, NEW YORK, RHODE ISLAND AND WHERE PROHIBITED OR RESTRICTED BY LAW. To Enter: NO PURCHASE NECESSARY. PURCHASE WILL NOT INCREASE YOUR CHANCES OF WINNING. To be eligible, entrant (“Entrant”) must provide the Administrator (as defined herein) of this promotion (the “Promotion”), Pro Silver Star, Ltd. (the “Administrator”) and J.C. Penney Corporation Inc. (the “Sponsor”), with its full name, email address, phone number, zip code and date of birth. Limit one (1) entry per person. Administrator will not be responsible for entries lost, delayed, incomplete or misdirected. Entries will become the sole property of Administrator and by entering, Entrant expressly consents to adding his/her name to receive future promotional offers, and using Entrant’s name for advertising, publicity or any other purposes whatsoever, as determined by Administrator in its sole discretion, without compensation and with or without attribution to Entrant, as Sponsor and/or Administrator in their sole discretion, without compensation and with Method of Entry: A. Purchase and Online Entry: Entry codes are available with the purchase of one (1) limited edition fleece bearing The Salvation Army and Dallas Cowboys trademarks (the “Fleece”) at select JCPenney stores in Texas as listed in the Appendix of these Official Rules (each a “Participating Store” and collectively the “Participating Stores”), while supplies last. -

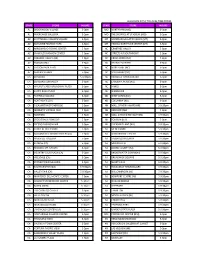

State Storeno Mall Name Store Type 2015 Sales 2014 Sales Variance

Variance State StoreNo Mall Name Store Type 2015 Sales 2014 Sales Inc/(Dec) % Inc/(Dec) TX 83 NorthPark Center In-Line 1,472,766.00 1,363,984.00 108,782.00 7.98% SC 135 Coastal Grand Mall In-Line 1,151,631.67 1,113,877.31 37,754.36 3.39% TX 20 Barton Creek Square Shopping Center In-Line 1,096,658.41 1,083,499.33 13,159.08 1.21% CA 8 Westfield Valencia Town Center In-Line 1,071,022.26 1,087,795.83 (16,773.57) -1.54% TX 19 Baybrook Mall In-Line 1,025,120.43 1,055,953.79 (30,833.36) -2.92% AZ 125 Park Place Mall In-Line 950,664.23 946,527.12 4,137.11 0.44% TN 48 Wolfchase Galleria In-Line 923,588.32 867,012.22 56,576.10 6.53% TX 55 Stonebriar Centre In-Line 876,800.55 815,558.37 61,242.18 7.51% CA 126 Westfield Galleria at Roseville In-Line 869,168.30 754,757.11 114,411.19 15.16% CO 167 Cherry Creek Shopping Center In-Line 868,959.85 835,887.13 33,072.72 3.96% CO 61 Park Meadows Center In-Line 831,157.07 800,397.91 30,759.16 3.84% AZ 28 Arrowhead Towne Center In-Line 771,406.64 656,746.72 114,659.92 17.46% CA 39 Westfield University Towne Center In-Line 738,949.33 573,464.00 165,485.33 28.86% CA 35 The Promenade at Temecula In-Line 733,268.27 666,557.65 66,710.62 10.01% KY 78 Mall St. -

2019 Dallas Cowboys Training Camp Promo

Training Camp Store Allocations Store Number Name Address 2685 The Parks Mall 3851 S Cooper St 2795 Stonebriar Mall 2607 Preston Rd 2434 Coronado Center 6600 Menaul Blvd NE Ste 3000 2939 North Star Mall 7400 San Pedro Ave 226 La Plaza 2200 S 10th St 2904 Southpark Meadows S/C 9500 S IH-35 Ste H 631 Ingram Park Mall 6301 NW Loop 410 702 Cielo Vista Mall 8401 Gateway Blvd W 1330 La Palmera Mall 5488 S Padre Island Dr Ste 4000 179 Timber Creek Crossing 6051 Skillman St 2946 Plaza at Rockwall 1015 E I 30 2877 The Rim Shopping Center 17710 La Cantera Pkwy 2338 Town East Mall 6000 Town East Mall 2055 Collin Creek Mall 821 N Central Expwy 1046 Golden Triangle Mall 2201 S Interstate 35 E Ste D 2410 Vista Ridge Mall 2401 S Stemmons Fwy Ste 4000 2884 Tech Ridge Center 12351 N IH-35 2826 Cedar Hill Village 333 N Hwy 67 2960 El Mercado Plaza 1950 Joe Battle Blvd 2969 Sherman Town Center 610 Graham Dr 2934 University Oaks Shopping Center 151 University Oaks 993 South Park Mall 2418 SW Military Dr 2982 Village at Fairview 301 Stacy Rd 2921 Robertsons Creek 5751 Long Prairie Rd 2105 Crossroads Mall 6834 Wesley St Ste C 1943 North East Mall 1101 Melbourne Dr Ste 5000 1419 Ridgmar Mall 1900 Green Oaks Rd 2093 Mesilla Valley Mall 700 Telshor Blvd Ste 2000 2021 Richland Mall 6001 W Waco Dr 579 Music City Mall 4101 E 42nd St 485 Mall of Abilene 4310 Buffalo Gap Rd 2682 Penn Square Mall 1901 NW Expwy Ste 1200 2833 Rolling Oaks Mall 6909 N Loop 1604 E 2806 Sunrise Mall 2370 N Expwy Ste 2000 712 Sikes Senter Mall 3111 Midwestern Pkwy 996 Broadway Square Mall 4401 S Broadway 450 Rio West Mall 1300 W Maloney Ave Ste A 1749 Central Mall 2400 Richmond Rd Ste 61 2905 Alliance Town Center 3001 Texas Sage Trl 658 Mall De Norte S/C 5300 San Dario 1989 Sunset Mall 6000 Sunset Mall 259 Colonial/Temple Mall 3111 S 31st St Ste 3301 1101 Valley Crossing Shopping Center 715 E Expressway 83 2036 Midland Park Mall 4511 N Midkiff Rd 304 Longview Mall 3550 McCann Rd 2110 Killeen Mall 2100 S W.S. -

Retail Big Deals 2015

RETAIL BIG DEALS 2015 FREE Buckle with a $10 Purchase FREE MATCHING BELT WITH EACH CUSTOM MADE TO MEASURE BOOT. BELT VALUE UP TO $300 .LIMIT ONE OFFER PER CUSTOMER. NOT VALID WITH ANY OTHER OFFERS Wild Bill’s Western Store RETAIL 311 N. Market Street ENDS 12/31/15 Dallas has BIG DEALS for our meeting attendees. Dallas, TX 75202 SHOW YOUR BADGE to take advantage of the 214-954-1050 WildBillsWestern.com special opportunities offered through our partners. DOWNTOWN FREE Gift $2 OFF in Retail Store VISIT PINTO RANCH FOR A SPECIAL TEXAS MEMENTO. PRESENT THIS VOUCHER WITH YOUR CONFERENCE BADGE FOR A COMPLIMENTARY GIFT. NO PURCHASE NECESSARY. Pinto Ranch Fine Western Wear LIMIT ONE PER PERSON NorthPark Center 8687 North Central Expressway, ENDS 12/31/15 House of Blues ENDS 12/31/15 Suite 2184 2200 N Lamar Street Dallas, TX 75225 Dallas, TX 75202 214-217-6200 214-978-BLUE PintoRanch.com HOB.com/dallas NORTH DALLAS DOWNTOWN COMPLIMENTARY Discounts and Coupon Book Special Offers REDEEM THIS VOUCHER FOR A COMPLIMENTARY PRESENT THIS AT THE GUEST RECEPTION GRAPEVINE MILLS VIP COUPON BOOK AT SIMON CENTER, LEVEL 1, CENTER COURT, TO RECEIVE GUEST SERVICES LOCATED NEAR ENTRANCE 3. COUPON CODE - DCVB YOUR VIP PRIVILEDGE CARD FILLED WITH SPECIAL OFFERS TO PARTICIPATING SHOPS AND RESTAURANTS. Galleria Dallas Grapevine Mills I-635 at Dallas North Tollway ENDS 12/31/15 3000 Grapevine Mills Parkway ENDS 12/31/15 13350 Dallas Parkway Grapevine, TX 76051 Dallas, TX 75240 972-724-4900 972-702-7171 GrapevineMills.com GalleriaDallas.com WEST OF DALLAS NORTH DALLAS COMPLIMENTARY COMPLIMENTARY Coupon Book Coupon Book REDEEM THIS VOUCHER AT GUEST SERVICES FOR A REDEEM THIS VOUCHER AT GUEST SERVICES FOR A COMPLIMENTARY VIP COUPON BOOK FILLED WITH COMPLIMENTARY VIP COUPON BOOK FILLED WITH HUNDREDS OF DOLLARS OF ADDITIONAL SAVINGS HUNDREDS OF DOLLARS OF ADDITIONAL SAVINGS FROM PARTICIPATING MERCHANTS. -

Michael Kors® Make Your Move at Sunglass Hut®

Michael Kors® Make Your Move at Sunglass Hut® Official Rules NO PURCHASE OR PAYMENT OF ANY KIND IS NECESSARY TO ENTER OR WIN. A PURCHASE OR PAYMENT WILL NOT INCREASE YOUR CHANCES OF WINNING. VOID WHERE PROHIBITED BY LAW OR REGULATION and outside the fifty United States (and the District of ColuMbia). Subject to all federal, state, and local laws, regulations, and ordinances. This Gift ProMotion (“Gift Promotion”) is open only to residents of the fifty (50) United States and the District of ColuMbia ("U.S.") who are at least eighteen (18) years old at the tiMe of entry (each who enters, an “Entrant”). 1. GIFT PROMOTION TIMING: Michael Kors® Make Your Move at Sunglass Hut® Gift Promotion (the “Gift ProMotion”) begins on Friday, March 22, 2019 at 12:01 a.m. Eastern Time (“ET”) and ends at 11:59:59 p.m. ET on Wednesday, April 3, 2019 (the “Gift Period”). Participation in the Gift Promotion does not constitute entry into any other promotion, contest or game. By participating in the Gift Promotion, each Entrant unconditionally accepts and agrees to comply with and abide by these Official Rules and the decisions of Luxottica of America Inc., 4000 Luxottica Place, Mason, OH 45040 d/b/a Sunglass Hut (the “Sponsor”) and WYNG, 360 Park Avenue S., 20th Floor, NY, NY 10010 (the “AdMinistrator”), whose decisions shall be final and legally binding in all respects. 2. ELIGIBILITY: Employees, officers, and directors of Sponsor, Administrator, and each of their respective directors, officers, shareholders, and employees, affiliates, subsidiaries, distributors, -

Brookfield Properties' Retail Group Overview

Retail Overview Brookfield Properties’ Retail Group Overview We are Great Gathering Places. We embrace our cultural core values of Humility, Attitude, Do The Right Thing, H Together and Own It. HUMILITY Brookfield Properties’ retail group is a company focused A ATTITUDE exclusively on managing, leasing, and redeveloping high- quality retail properties throughout the United States. D DO THE RIGHT THING T TOGETHER O HEADQUARTERS CHICAGO OWN IT RETAIL PROPERTIES 160+ STATES 42 INLINE & FREESTANDING GLA 68 MILLION SQ FT TOTAL RETAIL GLA 145 MILLION SQ FT PROFORMA EQUITY MARKET CAP $20 BILLION PROFORMA ENTERPRISE VALUE $40 BILLION Portfolio Map 2 7 1 4 3 5 3 6 2 1 2 1 1 2 1 3 3 3 1 1 2 4 1 2 1 3 2 1 1 10 4 2 5 1 4 10 2 3 3 1 48 91 6 5 6 2 7 6 4 5 11 7 4 1 1 1 2 2 2 5 7 1 2 1 2 1 1 1 1 6 1 3 5 3 4 15 19 2 14 11 1 1 3 2 1 2 1 1 3 6 2 1 3 4 18 2 17 3 1 2 1 3 2 2 5 3 6 8 2 1 12 9 7 5 1 4 3 1 2 1 2 16 3 4 13 3 1 2 6 1 7 9 1 10 5 4 2 1 4 6 11 5 3 6 2 Portfolio Properties 1 2 3 3 3 1 7 4 Offices 13 12 2 Atlanta, GA 7 3 1 1 Chicago, IL Baltimore, MD 8 5 2 Dallas, TX 4 Los Angeles, CA 6 New York, NY 8 2 9 5 Property Listings by State ALABAMA 7 The Oaks Mall • Gainesville 3 The Mall in Columbia • Columbia (Baltimore) 9 Brookfield Place • Manhattan WASHINGTON 8 Pembroke Lakes Mall • Pembroke Pines 4 Mondawmin Mall • Baltimore 10 Manhattan West • Manhattan 1 Riverchase Galleria • Hoover (Birmingham) 1 Alderwood • Lynnwood (Seattle) 5 Towson Town Center • Towson (Baltimore) 11 Staten Island Mall • Staten Island 2 The Shoppes at Bel Air • Mobile (Fort Lauderdale) -

2019 Property Portfolio Simon Malls®

The Shops at Clearfork Denver Premium Outlets® The Colonnade Outlets at Sawgrass Mills® 2019 PROPERTY PORTFOLIO SIMON MALLS® LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME 2 THE SIMON EXPERIENCE WHERE BRANDS & COMMUNITIES COME TOGETHER SIMON MALLS® LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME 2 ABOUT SIMON Simon® is a global leader in retail real estate ownership, management, and development and an S&P 100 company (Simon Property Group, NYSE:SPG). Our industry-leading retail properties and investments across North America, Europe, and Asia provide shopping experiences for millions of consumers every day and generate billions in annual sales. For more information, visit simon.com. · Information as of 12/16/2019 3 SIMON MALLS® LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME More than real estate, we are a company of experiences. For our guests, we provide distinctive shopping, dining, and entertainment. For our retailers, we offer the unique opportunity to thrive in the best retail real estate in the best markets. From new projects and redevelopments to acquisitions and mergers, we are continuously evaluating our portfolio to enhance the Simon experience—places where people choose to shop and retailers want to be. 4 LOCATION GLA IN SQ. FT. MAJOR RETAILERS CONTACTS PROPERTY NAME WE DELIVER: SCALE A global leader in the ownership of premier shopping, dining, entertainment, and mixed-use destinations, including Simon Malls®, Simon Premium Outlets®, and The Mills® QUALITY Iconic, irreplaceable properties in great locations INVESTMENT Active portfolio management increases productivity and returns GROWTH Core business and strategic acquisitions drive performance EXPERIENCE Decades of expertise in development, ownership, and management That’s the advantage of leasing with Simon. -

State Store Hours State Store Hours Al Brookwood

ALL HOURS APPLY TO LOCAL TIME ZONES STATE STORE HOURS STATE STORE HOURS AL BROOKWOOD VILLAGE 5-9pm MO NORTHPARK (MO) 5-9pm AL RIVERCHASE GALLERIA 5-9pm MO THE SHOPPES AT STADIUM (MO) 5-9pm AZ SCOTTSDALE FASHION SQUARE 5-9pm MT BOZEMAN GALLATIN VALLEY (MT) 5-9pm AZ BILTMORE FASHION PARK 5-9pm MT HELENA NORTHSIDE CENTER (MT) 5-9pm AZ ARROWHEAD TOWNE CENTER 5-9pm NC CRABTREE VALLEY 5-9pm AZ CHANDLER FASHION CENTER 5-9pm NC STREETS AT SOUTHPOINT 5-9pm AZ PARADISE VALLEY (AZ) 5-9pm NC CROSS CREEK (NC) 5-9pm AZ TUCSON MALL 5-9pm NC FRIENDLY CENTER 5-9pm AZ TUCSON PARK PLACE 5-9pm NC NORTHLAKE (NC) 5-9pm AZ SANTAN VILLAGE 5-9pm NC SOUTHPARK (NC) 5-9pm CA CONCORD 5-9:30pm NC TRIANGLE TOWN CENTER 5-9pm CA CONCORD SUNVALLEY 5-9pm NC CAROLINA PLACE (NC) 5-9pm CA WALNUT CREEK BROADWAY PLAZA 5-9pm NC HANES 5-9pm CA SANTA ROSA PLAZA 5-9pm NC WENDOVER 5-9pm CA FAIRFIELD SOLANO 5-9pm ND WEST ACRES (ND) 5-9pm CA NORTHGATE (CA) 5-9pm ND COLUMBIA (ND) 5-9pm CA PLEASANTON STONERIDGE 5-9pm NH MALL OF NEW HAMPSHIRE 5-9:30pm CA MODESTO VINTAGE FAIR 5-9pm NH BEDFORD (NH) 5-9pm CA NEWPARK 5-9pm NH MALL AT ROCKINGHAM PARK 5-9:30pm CA STOCKTON SHERWOOD 5-9pm NH FOX RUN (NH) 5-9pm CA FRESNO FASHION FAIR 5-9pm NH PHEASANT LANE (NH) 5-9:30pm CA SHOPS AT RIVER PARK 5-9pm NJ MENLO PARK 5-9:30pm CA SACRAMENTO DOWNTOWN PLAZA 5-9pm NJ WOODBRIDGE CENTER 5-9:30pm CA ROSEVILLE GALLERIA 5-9pm NJ FREEHOLD RACEWAY 5-9:30pm CA SUNRISE (CA) 5-9pm NJ MONMOUTH 5-9:30pm CA REDDING MT.