World Bank Document

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SDN Changes 2014

OFFICE OF FOREIGN ASSETS CONTROL CHANGES TO THE Specially Designated Nationals and Blocked Persons List SINCE JANUARY 1, 2014 This publication of Treasury's Office of Foreign AL TOKHI, Qari Saifullah (a.k.a. SAHAB, Qari; IN TUNISIA; a.k.a. ANSAR AL-SHARIA IN Assets Control ("OFAC") is designed as a a.k.a. SAIFULLAH, Qari), Quetta, Pakistan; DOB TUNISIA; a.k.a. ANSAR AL-SHARI'AH; a.k.a. reference tool providing actual notice of actions by 1964; alt. DOB 1963 to 1965; POB Daraz ANSAR AL-SHARI'AH IN TUNISIA; a.k.a. OFAC with respect to Specially Designated Jaldak, Qalat District, Zabul Province, "SUPPORTERS OF ISLAMIC LAW"), Tunisia Nationals and other entities whose property is Afghanistan; citizen Afghanistan (individual) [FTO] [SDGT]. blocked, to assist the public in complying with the [SDGT]. AL-RAYA ESTABLISHMENT FOR MEDIA various sanctions programs administered by SAHAB, Qari (a.k.a. AL TOKHI, Qari Saifullah; PRODUCTION (a.k.a. ANSAR AL-SHARIA; OFAC. The latest changes may appear here prior a.k.a. SAIFULLAH, Qari), Quetta, Pakistan; DOB a.k.a. ANSAR AL-SHARI'A BRIGADE; a.k.a. to their publication in the Federal Register, and it 1964; alt. DOB 1963 to 1965; POB Daraz ANSAR AL-SHARI'A IN BENGHAZI; a.k.a. is intended that users rely on changes indicated in Jaldak, Qalat District, Zabul Province, ANSAR AL-SHARIA IN LIBYA; a.k.a. ANSAR this document that post-date the most recent Afghanistan; citizen Afghanistan (individual) AL-SHARIAH; a.k.a. ANSAR AL-SHARIAH Federal Register publication with respect to a [SDGT]. -

Banks in Lebanon

932-933.qxd 14/01/2011 09:13 Õ Page 2 AL BAYAN BUSINESS GUIDE USEFUL NUMBERS Airport International Calls (100) Ports - Information (1) 628000-629065/6 Beirut (1) 580211/2/3/4/5/6 - 581400 - ADMINISTRATION (1) 629125/130 Internal Security Forces (112) Byblos (9) 540054 - Customs (1) 629160 Chika (6) 820101 National Defense (1701) (1702) Jounieh (9) 640038 Civil Defence (125) Saida (7) 752221 Tripoli (6) 600789 Complaints & Review (119) Ogero (1515) Tyr (7) 741596 Consumer Services Protection (1739) Police (160) Water Beirut (1) 386761/2 Red Cross (140) Dbaye (4) 542988- 543471 Electricity (145) (1707) Barouk (5) 554283 Telephone Repairs (113) Jounieh (9) 915055/6 Fire Department (175) Metn (1) 899416 Saida (7) 721271 General Security (1717) VAT (1710) Tripoli (6) 601276 Tyr (7) 740194 Information (120) Weather (1718) Zahle (8) 800235/722 ASSOCIATIONS, SYNDICATES & OTHER ORGANIZATIONS - MARBLE AND CEMENT (1)331220 KESRWAN (9)926135 BEIRUT - PAPER & PACKAGING (1)443106 NORTH METN (4)926072-920414 - PHARMACIES (1)425651-426041 - ACCOUNTANTS (1)616013/131- (3)366161 SOUTH METN (5)436766 - PLASTIC PRODUCERS (1)434126 - ACTORS (1)383407 - LAWYERS - PORT EMPLOYEES (1) 581284 - ADVERTISING (1)894545 - PRESS (1)865519-800351 ALEY (5)554278 - AUDITOR (1)322075 BAABDA (5)920616-924183 - ARTIST (1)383401 - R.D.C.L. (BUSINESSMEN) (1)320450 DAIR AL KAMAR (5)510244 - BANKS (1)970500 - READY WEAR (3)879707-(3)236999 - CARS DRIVERS (1)300448 - RESTAURANTS & CAFE (1)363040 JBEIL (9)541640 - CHEMICAL (1)499851/46 - TELEVISIONS (5)429740 JDEIDET EL METN (1)892548 - CONTRACTORS (5)454769 - TEXTILLES (5)450077-456151 JOUNIEH (9)915051-930750 - TOURISM JOURNALISTS (1)349251 - DENTISTS (1)611222/555 - SOCKS (9)906135 - TRADERS (1)347997-345735 - DOCTORS (1)610710 - TANNERS (9)911600 - ENGINEERS (1)850111 - TRADERS & IND. -

Board of Directors Branch Network General

BOARD OF DIRECTORS BRANCH NETWORK Mr. Walid RAPHAËL Mr. Zafer CHAOUI To reach Banque Libano-Française branches, please dial (01) or (03) 79 13 32 Chairman Mr. Philippe DORÉ or the Short Number 1332 Dr. Samer ISKANDAR Mr. Elie NAHAS Mr. Habib LETAYF • Accaoui • Khaldeh Chairman Mr. Philippe LETTE of Group Banque Libano-Française Mrs. Raya RAPHAËL NAHAS • Achrafieh • Kousba Dr. Marwan NSOULI • Bar Elias • Lebaa • Batroun • Mansourieh • Bechara El-Khoury • Mar Elias GENERAL MANAGEMENT • Bir Hassan • Mar Takla Executive Committee • Chyah • Mazraa Mr. Walid RAPHAËL Chairman and General Manager • Dahr El-Ain - Koura • Mazraat Yachouh Mr. Elie NAHAS Chairman of Group Banque Libano-Française and General Manager • Dbayeh • Miziara Mrs. Raya RAPHAËL NAHAS General Manager • Dekwaneh • Mreijeh Mrs. Hoda ASSI Assistant General Manager • Dora • Nabatieh Mr. Elie AOUN Assistant General Manager Mrs. Josephine CHAHINE Assistant General Manager • Dora - Bourj-Hammoud • Rabieh Mr. Philippe CHARTOUNY Assistant General Manager • Galaxy • Reyfoun Mr. Maurice ISKANDAR Assistant General Manager • Gefinor • Saïda Mr. Georges KHOURY Assistant General Manager Mr. Marwan RAMADAN Assistant General Manager • Geitawi • Saïda - Boulevard Mr. Charles SALEM Assistant General Manager • Hadat • Saïfi Business Development Divisions • Halba • Sami El-Solh Branch Network Mr. Marwan RAMADAN • Hamra (Main Branch) • Sin El-Fil Corporate Banking Mrs. Hoda ASSI • Hamra - Maamari • Sioufi Middle-Market Banking Mr. Elie AOUN Treasury and Capital Markets Mr. Georges KHOURY • Haret-Hreik • Sodeco Private Banking and Wealth Management Mr. Charles SALEM • Hazmieh • Tripoli - El-Mina International Mr. Maurice ISKANDAR Loan Remediation Mr. Moustapha ALWAN • Jal El-Dib • Tripoli - Tebbaneh Retail Banking Products and Marketing Mr. Ronald ZIRKA • Jal El-Dib Centre • Tripoli - Tell Cards Services Mrs. -

Healthcare Network Providers TABLE of CONTENTS

Healthcare Network Providers TABLE OF CONTENTS LIST OF CONTRACTED HOSPITALS - GENERAL NETWORK 02 LIST OF CONTRACTED AMBULATORY PROVIDERS - DIAGNOSTIC CENTERS 05 LIST OF CONTRACTED AMBULATORY PROVIDERS - LABORATORY CENTERS 07 AMBULATORY AND RADIOLOGY SERVICES 10 LIST OF CONTRACTED AMBULATORY PROVIDERS - OPTOMETRY - VISION SERVICE CENTERS 11 LIST OF CONTRACTED AMBULATORY PROVIDERS - FIRST AID CENTER - PRIMARY CARE CENTER 11 LIST OF CONTRACTED AMBULATORY PROVIDERS - HOME CARE 11 LIST OF CONTRACTED AMBULATORY PROVIDERS - DENTAL CENTER 11 LIST OF CONTRACTED PHARMACIES 12 LIST OF CONTRACTED PHYSICIANS 20 HI-AD-02/ED13 1 of 26 Healthcare Network Providers List of Contracted Hospitals - General Network * For members insured under Restricted Network, American University Of Beirut Medical Center (AUBMC) and Clemenceau Medical Center (CMC) are excluded GREATER BEIRUT Address Telephone Beirut Eye & Ent Specialist Hospital Al Mathaf, Hotel Dieu St. 01/423110-111 Hopital Libanais Geitaoui - Centre Hospitalier Universitaire Ashrafieh, Geitawi St. 01/577177 Hotel-Dieu De France Ashrafieh, Hotel Dieu St. 01/615300 - 01/615400 St. George Hospital - University Medical Center Ashrafieh, Rmeil St. After Sagesse University 1287 University Medical Center - Rizk Hospital Ashrafieh, Zahar St. 01/200800 Al Zahraa Hospital Bir Hassan, Jnah, Facing Hotel Galleria 01/853409-10 Beirut General Hospital Bir Hassan, Jnah 01/850236 Rafik Hariri University Hospital Rhuh Bir Hassan, Jnah 01/830000 Trad Hospital & Medical Center Clemenceau, Mexic St. 01/369494-5 Hopital St. Joseph Dora, St. Joseph St. 01/248750 - 01/240111 Hopital Haddad Des Soeurs Du Rosaire Gemmayze, Pasteur St. 01/440800 Rassoul Al Aazam Hospital Ghoubeiry, Airport Road, in Front of Atm Station 01/452700 Sahel General Hospital Ghoubeiry, Airport Road 01/858333-4-5 - 01/840142 Hospital Fouad Khoury & Associate Hamra, Abed El Aziz St. -

Federal Register/Vol. 79, No. 136/Wednesday, July 16, 2014

41628 Federal Register / Vol. 79, No. 136 / Wednesday, July 16, 2014 / Notices Individuals Beirut, Lebanon; Tayyouneh, Haret Registry Number 591610 (United Arab Hreyk, Beirut, Lebanon; Port, Nahr, Emirates) [SDGT] (Linked To: STARS 1. AMHAZ, Issam Mohamad (a.k.a. AMHAZ, Beirut, Lebanon; Ras El Ain, Baalbeck, GROUP HOLDING; Linked To: ’Isam; a.k.a. AMHAZ, Issam Mohamed), Lebanon; Hadeth, Lebanon; Nabatiyeh, IBRAHIM, Ayman). Lebanon; Old Saida Road, Beirut Mall, Ghadir, 5th Floor, Safarat, Bir Hassan, Dated: July 10, 2014. Jenah, Lebanon; Issam Mohamad Amhaz Beirut, Lebanon; Duty-Free Airport, Property, Ambassades (Safarate), Bir Rafik Hariri International Airport, Beirut, Barbara C. Hammerle, Hassan Area, Ghobeiri, Baabda, Lebanon; Lebanon; Sharl Helo Street, Beirut Acting Director, Office of Foreign Assets DOB 04 Mar 1967; POB Baalbek, Seaport, Lebanon; Kamil Shamoun Control. Lebanon; nationality Lebanon; Passport Street, Dekwaneh, Beirut, Lebanon; [FR Doc. 2014–16754 Filed 7–15–14; 8:45 am] Hermel, Lebanon; Commercial Registry RL0000199 (Lebanon); Identification BILLING CODE 4810–AL–P Number 61 Nabha; Chairman, Stars Number 2001929 (Lebanon) [SDGT] Group Holding; General Manager, (Linked To: AMHAZ, Kamel Mohamad; Teleserveplus (individual) [SDGT]. Linked To: STARS GROUP HOLDING). 2. AMHAZ, Kamel Mohamad (a.k.a. AL– 3. STARS COMMUNICATIONS OFFSHORE DEPARTMENT OF VETERANS AMHAZ, Kamel; a.k.a. AMHAZ, Kamel; SAL (a.k.a. STARS COMMUNICATION AFFAIRS a.k.a. AMHAZ, Kamel Mohamed; a.k.a. SAL OFF–SHORE; a.k.a. STARS AMHAZ, Kamil), 5th Floor, Ghadir -

A C Tivity R E P O R T 2010

ACTIVITY REPORT 2010 Contents 4 Message from 14 Spirituality 24 the Grand Master in action Focus 26 Lebanon In every clinic, every day, Christians and Muslims wait, shoulder to shoulder 50 Activities in Europe 68 Africa On the continent of Africa the Order works in 38 countries 72 Middle East Care continues apace Worldwide medical, 46 health and social 78 welfare activities Government Message from the Grand Master ..........4 Africa .....................................................32 Government ........................................78 • Kenya ..............................................32 The government of the Order ...............80 Message from the Grand Chancellor • Congo .............................................34 and the Grand Hospitaller ......................5 • Cameroon .......................................36 Conferences ..........................................82 Momentous events Asia .......................................................38 Official Visits of Grand Master Fra’ for the Order 2008-2009 .......................6 • Burma/Myanmar ............................38 Andrew Bertie .......................................84 The passing of Grand Master Europe ..................................................42 Official Visits of Grand Master Fra’ Fra’ Andrew Bertie .................................8 • Lampedusa ....................................42 Matthew Festing ...................................86 • Belgium ..........................................44 Grand Master Fra’ Matthew Festing ....10 Diplomacy .............................................90 -

MONTHLY-E83-June09 Final.Indd

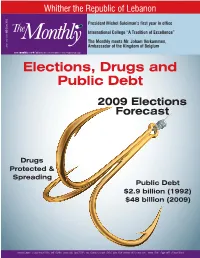

Whither the Republic of Lebanon President Michel Suleiman’s first year in office June 2009 | 83 International College “A Tradition of Excellence” The Monthly meets Mr. Joham Verkammen, Ambassador of the Kingdom of Belgium issue number www.iimonthly.com • Published by Information International sal Elections, Drugs and Public Debt 2009 Elections Forecast Drugs Protected & Spreading Public Debt $2.9 billion (1992) $48 billion (2009) Lebanon 5,000LL | Saudi Arabia 15SR | UAE 15DHR | Jordan 2JD| Syria 75SYP | Iraq 3,500IQD | Kuwait 1.5KD | Qatar 15QR | Bahrain 2BD | Oman 2OR | Yemen 15YRI | Egypt 10EP | Europe 5Euros 2 iNDEX PAGE PAGE 4 Electoral law, results, blocs and elections forecast 35 Between Yesterday and Today LEADER 12 Drugs in Lebanon 36 Lebanon’s MPs Cultivation, traffickingand and Lebanese its spread among youth Parliamentary Elections 1960 - 2009 18 Public debt at USD 48 billion 37 From the series of 20 President Michel Suleiman’s first “Children Entertaining Stories”* year in office 38 Myth #24 21 Whither the Republic of Lebanon: Alexander, worshipper or fighter? Amnesty for drug crimes 39 Jumblatt and Syria 22 Violation of Civil Rights and Duties 40 Release of the four generals: 23 Salt Production End of one phase, beginning of another 24 Syndicate of Petroleum Companies Workers and 42 International Media Employees in Lebanon Iran’s ‘New Proposal’ & The USA 26 International College 44 Karm Al Muhr 28 Lebanese International University 45 Harb families 30 The Monthly meets Mr. 46 Education Enrollment in the Arab Joham Verkammen, World Ambassador of the Kingdom of Belgium 47 Real Estate Index: April 2009 32 High Blood Pressure by Dr. -

UNDP in Lebanon

The Implemented by: Special Edition This is a special supplement issued by the UNDP «Peace Building in Lebanon» project, funded by Germany’s Federal Ministry for Economic Cooperation and Development through the German In Lebanon KfW Development Bank, distributed with the An-Nahar newspaper in its Arabic version, with the The Daily Star in English, and with L'Orient-Le Jour newspaper in French. The supplement brings together writers, journalists, media Joint news supplement professionals, researchers and artists residing in Lebanon, and addresses issues relating to civil war memory and civil peace, Issue nº 15, April 2017 through objective approaches far removed from hate speech. Ammar Saleh A heart-shaped locket, holding photos of Ammar Mohammad Saleh and his father, hang on a chain. Ammar was 21 years old in March of 1982 when he took a taxi from Beirut and headed back home to Baalbek, to his parents’ house. He never reached home that day, nor on any of the days that followed. His fate remains unknown. Dalia Khamissy Dalia © 03 On Memory and Politics 08 - 09 Our Stories in War and 03 The Many Sources of Hatred about It 05 The Lebanon War: The Referents of Memory Constructions 06 «No Justice, No Peace» 07 Mass Graves in Lebanon: Remnants of the Past or Challenges for the Future? 11 The Missing 12 News Bulletin Introductions and the Civil War 13 Problems of Citizenship in Lebanon Carll Hallal Carll © 14 War Is Not an Ammunition Dump The The In Lebanon Issue nº 15, April 2017 Issue nº 15, April 2017 In Lebanon 2 Joint news supplement Joint -

Lebanon Banks.Pdf

942-951.qxd 14/01/2011 09:19 Õ Page 2 AL BAYAN BUSINESS GUIDE BANKS IN LEBANON - Amyoun: Tel: (06)955600 - Fax: (06) 955605 AHLI INTERNATIONAL BANK - Ashrafieh: (Charles Malek Avenue) Tel:(01) 200250-3 -Fax:(01)200724 - General Manager : M. Michel Saroufim - Ashrafieh: (Sassine Square) Tel / Fax: (01)200640 - Assistant General Manager : M. Fadi Zablit - Ashrafieh: (Sassine Street) Tel: (01) 217064 - Fax: (01) 216954 - Assistant General Manager : M. Aed Jalloul - Ashrafieh: (Saydeh) Tel: (01)200753 - Fax: (01)204972 HEAD OFFICE: - Ashrafieh: (Sodeco)Tel: (01) 612790 - Fax: (01) 612793 Bab Idriss - Omar Daouk Str. - Ahli International Bank SAL. Bldg - Beirut - Lebanon: - Baabda: Tel: (05)451452 - Fax: (05)953236 Tel: (1)970920 - Fax: (1)970944 - Bab Idriss: Tel: (01)977588 - Fax: (01) 999410 P.O.B: 11-5556 Riad El Solh - Beirut 1107 2200 Lebanon - Badaro: Tel: (01)387395 - Fax: (01) 387398 E-mail: [email protected] - Basta-Noueiri: Tel / Fax: (01) 661323 BRANCHES: - Bechara El-Khoury: Tel/Fax: (01) 664093 - Bab Idriss: Main Branch: Tel: (1)970920 - Fax: (1)970952 - Bhamdoun: Tel: (05) 261285 - Fax: (05) 261289 - Dora: Tel: (1)899121 - Fax: (1)894721 - Bint Jbeil: Tel: (07)450900 - Fax: (07) 450904 - Hamra: Tel: (1) 340270 - Fax: (1)742843 - Bliss: Tel: (01)361793 - Fax: (01) 361796 - Galerie Semaan: Tel: (5)954630 - Fax: (5)954632 - Bourj-Hammoud: Tel / Fax: (01) 263325 - Jdeideh: Tel: (1)881680 - Fax: (1)883891 - Broummana: Tel: (04)860163 - Fax: (04)860167 - Kaslik: Tel: (9)210769 - Fax: (9)210773 - Chekka: Tel : (06)545379 - Fax: (06)541526 - Saida: Tel: (7)728930 - Fax: (7)728931 - Chiyah: Tel: (01)541120 - Fax: (01)541123 - Tripoli: Tel: (6)430106 - Fax: (6)432720 - Chtaura: Tel: (08) 542960 - Fax: (08)544853 - Verdun: Tel: (1)797079 - Fax: (1)797082 - Dora (Cité Dora): Tel: (01)255686 - Fax: (01)255695 - Dora (City Mall): Tel: (01) 884114 - Fax: (01) 884115 ARAB AFRICAN INTERNATIONAL BANK - Dora (Vartanian Center): Tel / Fax: (01)250404 - Beirut Branch Manager : M. -

2006 4 Section 3.Qxd

INDEX OF ADVERTISERS BY SPECIALIZATION Spare Parts & Garage Garage Spare Parts INDEX OF ADVERTISERS BY SPECIALIZATION Spare Parts & Garage Garage Spare Parts ALL CARS GARAGES & EUROPEAN ALFA ROMEO Sammay Auto Scan . Choueifat MERCEDES OPEL Soufia . Jisr El-basha Apollo 11 . Dora Assiad Sarl . Dekwaneh Abbas Younes . Chyah Geffy Trading Center . Mar Mekhael SPARE PARTS Srour Auto Parts . Bekaa Clinic Cars / Fadi Azar . Nahr El-mott Auto Renault . Bauchrieh Abou Chaaya . Sabtieh Harutune Ishkhanian . Mar Mekhael Am Performance . Nahr El-mott Tony Azar . Hadeth Elie & Milad Ghorayeb . Bauchrieh Joe Chalhoub . Bauchrieh Abou Dahesh . Sour Joseph Yazbeck . Kfarshima Antoine Kallas . Antelias Waleed Motortune . Jal El-dib Georges Jreij & Bros Furn El-chebbak Richie Motorsport . Mansourieh Abou Mrad . Bauchrieh Original . Sour Auto Akkawi . Hadeth Marani Auto Parts . Sabtieh Srour Auto Parts . Bekaa Accessoire Wissam Yaacoub . Sour Raymond Auto Parts . Hadeth Auto Dynamics . Chyah New York . Bauchrieh Ahmad Karake . Sfeir Vasken Auto Parts . Dora Auto Mall . Adlieh Rassi . Batchay Ali Ahmad Motors . Ouzai Auto Tune . Jal El-dib Vahe & Son . Nahr AUDI, VW, SEAT, SKODA FERRARI Auto Benz - Khoueiry Bros . Dora Axe Auto . Bauchrieh A. A. Aoun Spare Parts . Bauchrieh Centrauto . Furn El-chebbak Auto Body - Matar Bros . Dbayeh PEUGEOT, CITROEN Bmr . Dora Abou Chakra . Baabda Nasr Automotive Clinic . Nahr El-mott Auto Dynamics . Chyah Abou Jaoude Spare Parts . Dora Centre Zaher For Mecanic . Sour Auto Benz - Khoueiry Bros . Dora Rectangle . Mtaileb Auto Tune . Jal El-dib El Chayeb . Jounieh Chiha Auto Parts . Bauchrieh Auto Dynamics . Chyah Automotive Club Center . Bir Hassan Elias Azzi . Mkalles Class Car . Choueifat JAPANESE Auto Land . Dora Bechara Ghssoub . -

2008 1 Section 1

CAR LOAN / BANK’S INFORMATION AUTOShop 2008 - 12 INDEX OF CARS 2008 BY BRAND BRAND COMPANY AREA PHONE PAGE ALFA ROMEO Bassoul, Heneine & Co. Sal Bauchrieh 01/684684 18 ASTON MARTIN Unicart (h. Tewtel & Co.) Sal Verdun 01/800001 18 AUDI Ets F.a. Kettaneh Medawar 01/577802 18 BENTLEY Saad & Trad Sal Nahr 01/613670 18 BMW Bassoul, Heneine & Co. Sal Bauchrieh 01/684684 20 CADILLAC Impex Trading Co. (lebanon) Sal Badaro 01/615715 22 CHERY Lebanese Auto Agencies Jal El Dib 04/721188 22 CHEVROLET Impex Trading Co. (lebanon) Sal Badaro 01/615715 22 CHRYSLER T. Gargour & Fils Sal Dora 01/255366 24 CITROEN Centradis Zalka 01/901744 24 DACIA Bassoul, Heneine & Co. Sal Bauchrieh 01/684684 24 DAIHATSU Autostars - Mounir Bazerji Saifi 01/586000 24 DODGE T. Gargour & Fils Sal Dora 01/255366 26 FIAT Saad & Trad Sal Nahr 01/613670 26 FORD Auto Levant Sal Chyah 05/458111 26 GMC Rasamny Younis Motor Co. Sal - Rymco Chyah 01/273333 26 HONDA Unicart (h. Tewtel & Co.) Sal Verdun 01/800001 28 HUMMER Impex Trading Co. (lebanon) Sal Badaro 01/615715 28 HYUNDAI Century Motor Co. Sal Sin El-Fil 01/511751 28 INFINITI Rasamny Younis Motor Co. Sal - Rymco Chyah 01/273333 30 JAGUAR Saad & Trad Sal Nahr 01/613670 30 JEEP T. Gargour & Fils Sal Dora 01/255366 30 KIA Natco - National Automative Trading Co. Sal Hazmieh 05/950812 32 LADA Gimex-general Import Export Co. Wata El Mousaitbeh 01/819805 32 LAMBORGHINI Saad & Trad Sal Nahr 01/613670 34 LANCIA G.a. Bazerji & Sons Co. -

DEPARTMENT of the TREASURY Office of Foreign Assets Control

This document is scheduled to be published in the Federal Register on 07/16/2014 and available online at http://federalregister.gov/a/2014-16754, and on FDsys.gov DEPARTMENT OF THE TREASURY Office of Foreign Assets Control Designation of 5 individuals and 7 entities Pursuant to Executive Order 13224 of September 23, 2001, “Blocking Property and Prohibiting Transactions With Persons Who Commit, Threaten To Commit, or Support Terrorism.” AGENCY: Office of Foreign Assets Control, Treasury. ACTION: Notice. --------------------------- SUMMARY: The Treasury Department’s Office of Foreign Assets Control (“OFAC”) is publishing the names of 5 individuals and 7 entities whose property and interests in property are blocked pursuant to Executive Order 13224 of September 23, 2001, “Blocking Property and Prohibiting Transactions With Persons Who Commit, Threaten To Commit, or Support Terrorism.” DATES: The designations by the Director of OFAC of the 5 individuals and 7 entities in this notice, pursuant to Executive Order 13224, are effective on July 10, 2014. FOR FURTHER INFORMATION CONTACT: Assistant Director, Compliance Outreach & Implementation Office of Foreign Assets Control Department of the Treasury Washington, DC 20220, tel.: 202/622-2490. SUPPLEMENTARY INFORMATION: Electronic and Facsimile Availability This document and additional information concerning OFAC are available from OFAC’s web site (www.treas.gov/ofac) or via facsimile through a 24-hour fax-on-demand service, tel.: 202/622-0077. Background On September 23, 2001, the President issued Executive Order 13224 (the “Order”) pursuant to the International Emergency Economic Powers Act, 50 U.S.C. 1701-1706, and the United Nations Participation Act of 1945, 22 U.S.C.