Full Page Photo

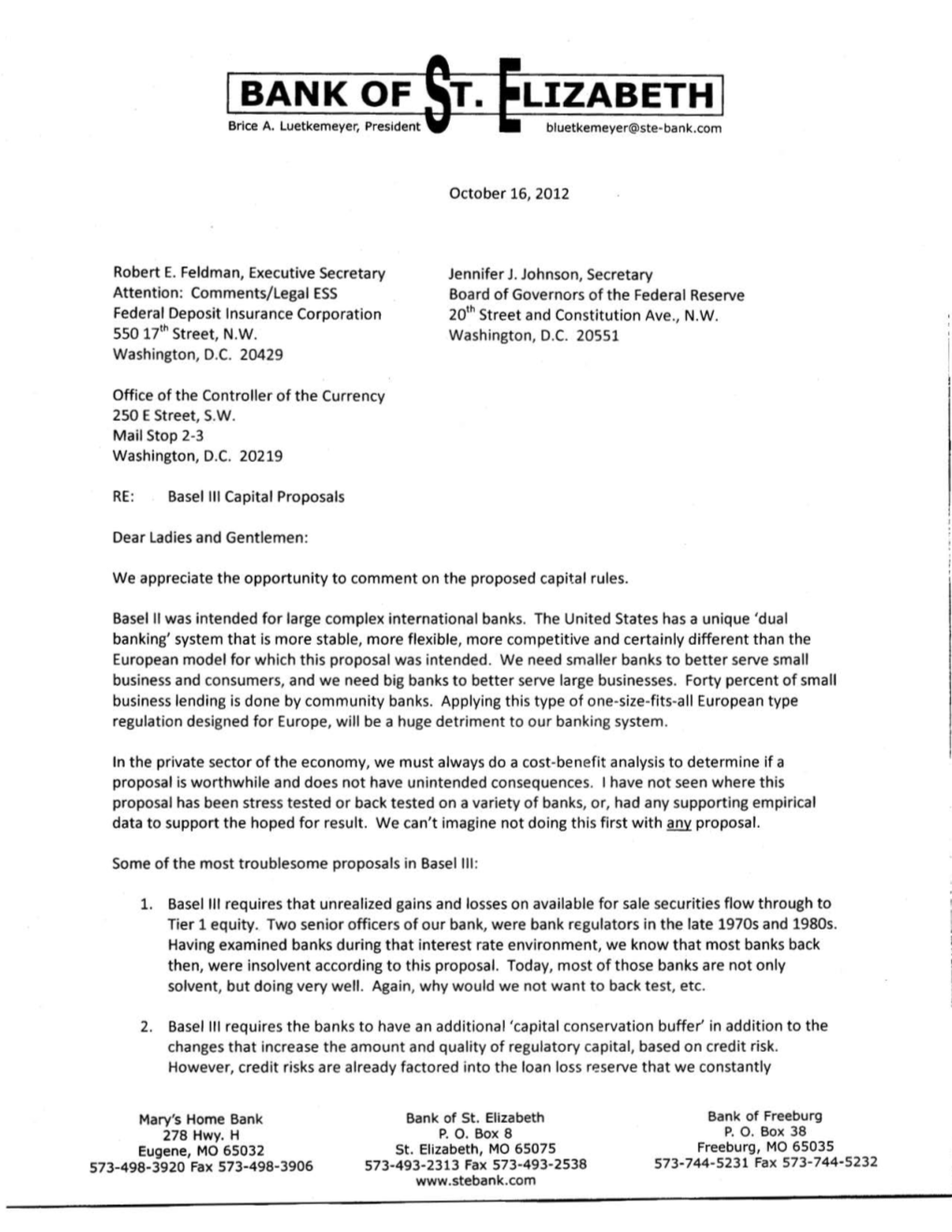

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Primary Election August 2, 2016 Miller County, Missouri

SAMPLE BALLOT PRIMARY ELECTION AUGUST 2, 2016 MILLER COUNTY, MISSOURI NOTICE OF ELECTION Notice is hereby given that the Primary Election will be held in the County of Miller on Tuesday, August 2, 2016 as certified to this office by the participating entities of Miller County. The ballot for the Election shall be in substantially the following form. DEMOCRATIC PARTY REPUBLICAN PARTY REPUBLICAN PARTY FOR UNITED STATES SENATOR FOR UNITED STATES SENATOR FOR STATE REPRESENTATIVE Vote For ONE Vote For ONE DISTRICT 59 CHIEF WANA DUBIE ROY BLUNT Vote For ONE CORI BUSH KRISTI NICHOLS MIKE BERNSKOETTER JASON KANDER BERNIE MOWINSKI RANDY DINWIDDIE ROBERT MACK RYAN D LUETHY FOR STATE REPRESENTATIVE DISTRICT 62 FOR GOVERNOR FOR GOVERNOR Vote For ONE Vote For ONE Vote For ONE LEONARD JOSEPH STEINMAN II CATHERINE HANAWAY TOM HURST CHRIS KOSTER ERIC GREITENS FOR STATE REPRESENTATIVE ERIC MORRISON JOHN BRUNNER DISTRICT 124 CHARLES B. WHEELER PETER D. KINDER Vote For ONE ROCKY MILLER FOR LIEUTENANT GOVERNOR FOR LIEUTENANT GOVERNOR Vote For ONE Vote For ONE FOR CIRCUIT JUDGE WINSTON APPLE ARNIE C. - AC DIENOFF CIRCUIT 26, DIVISION 2 RUSS CARNAHAN BEV RANDLES Vote For ONE TOMMIE PIERSON, SR. MIKE PARSON KENNY HAYDEN FOR SECRETARY OF STATE FOR SECRETARY OF STATE FOR 1ST DISTRICT Vote For ONE Vote For ONE COMMISSIONER BILL CLINTON YOUNG WILL KRAUS Vote For ONE ROBIN SMITH JOHN (JAY) ASHCROFT DANIEL L. BERENDZEN MD RABBI ALAM ROI CHINN RODNEY FAIR RONNIE VERNON FOR STATE TREASURER FOR STATE TREASURER Vote For ONE Vote For ONE DARRELL L. BUNCH PAT CONTRERAS ERIC SCHMITT FOR 2ND DISTRICT COMMISSIONER JUDY BAKER FOR ATTORNEY GENERAL Vote For ONE FOR ATTORNEY GENERAL Vote For ONE Vote For ONE JOSH HAWLEY TRAVIS LAWSON JAKE ZIMMERMAN KURT SCHAEFER RANDY LUTTRELL TERESA HENSLEY FOR UNITED STATES ROBERT WAYNE JONES REPRESENTATIVE RANDY RUSSELL FOR UNITED STATES DISTRICT 3 REPRESENTATIVE Vote For ONE STEVE EIDSON DISTRICT 3 Vote For ONE BLAINE LUETKEMEYER Q. -

Election Summary Report

Page: 1 of 7 11/8/2016 9:34:28 PM Election Summary Report General Election CALLAWAY COUNTY November 08, 2016 Summary for: All Contests, All Districts, McCREDIE , All Counting Groups Precincts Reported: 1 of 1 (100.00%) Registered Voters: 321 of 489 (65.64%) Ballots Cast: 321 PRESIDENT AND VICE-PRESIDENT for UNITED STATES (Vote for 1) Precincts Reported: 1 of 1 (100.00%) Total Times Cast 321 / 489 65.64% Candidate Party Total HILLARY RODHAM CLINTON/TIMOTHY DEM 48 MICHAEL KAINE DONALD J. TRUMP/MICHAEL REP 248 R. PENCE GARY JOHNSON/BILL WELD LIB 13 DARRELL L. CASTLE/SCOTT CST 3 N. BRADLEY JILL STEIN/AJAMU BARAKA GRN 0 Total Votes 319 UNITED STATES SENATOR (Vote for 1) Precincts Reported: 1 of 1 (100.00%) Total Times Cast 321 / 489 65.64% Candidate Party Total JASON KANDER DEM 85 ROY BLUNT REP 216 JONATHAN DINE LIB 13 FRED RYMAN CST 3 JOHNATHAN McFARLAND GRN 2 Total Votes 319 Page: 2 of 7 11/8/2016 9:34:28 PM GOVERNOR for MISSOURI (Vote for 1) Precincts Reported: 1 of 1 (100.00%) Total Times Cast 321 / 489 65.64% Candidate Party Total CHRIS KOSTER DEM 97 ERIC GREITENS REP 211 CISSE W SPRAGINS LIB 6 DON FITZ GRN 0 LESTER BENTON (LES) IND 4 TURILLI, JR. Total Votes 318 LIEUTENANT GOVERNOR for MISSOURI (Vote for 1) Precincts Reported: 1 of 1 (100.00%) Total Times Cast 321 / 489 65.64% Candidate Party Total RUSS CARNAHAN DEM 86 MIKE PARSON REP 212 STEVEN R. HEDRICK LIB 16 JENNIFER LEACH GRN 1 Total Votes 315 SECRETARY OF STATE for MISSOURI (Vote for 1) Precincts Reported: 1 of 1 (100.00%) Total Times Cast 321 / 489 65.64% Candidate Party Total -

MISSOURI AFL-CIO COPE ENDORSEMENTS GENERAL ELECTION November 2, 2010

MISSOURI AFL-CIO COPE ENDORSEMENTS GENERAL ELECTION November 2, 2010 U.S SENATE : 17 Kenny Biermann (D)* Robin Carnahan (D) 18 Anne Zerr (R)* STATE AUDITOR : 19 Matt Simmons (D) Susan Montee (D)* 20 No Endorsement U.S. REPRESENTATIVE : 21 Kelly Schultz (D) 1 Lacy Clay (D)* 22 Doug Galaske (D) 2 No Endorsement 23 Stephen Webber (D)* 3 Russ Carnahan (D)* 24 Chris Kelly (D)* 4 Ike Skelton (D)* 25 Mary Wynne Still (D)* 5 Emanuel Cleaver II (D)* 26 Joe Aull (D)* 6 OPEN 27 Pat Conway (D)* 7 Scott Eckersley (D) 28 Mark Sheehan (D) 8 Jo Ann Emerson (R)* 29 Bill Caldwell (D) 9 No Endorsement 30 Lexi Norris (D) MISSOURI SENATE : 31 Jay Swearingen (D) 2 OPEN 32 Jason Grill (D)* 4 Joe Keaveny (D)* 33 Jim Stoufer (D) 6 Mike Kehoe (R) 34 Mark Ellebracht (D) 8 Will Kraus (R) 35 OPEN 10 Jolie Justus (D)* 36 Barbara Lanning (D) 12 No Endorsement 37 Mike Talboy (D)* 14 Maria Chapelle-Nadal (D) 38 Ryan Silvey (R)* 16 Frank Barnitz (D)* 39 Jean Peters-Baker (D) 18 Wes Shoemyer (D)* 40 John Joseph Rizzo (D) 20 Terry Traw (D) 41 Shalonn (Kiki) Curls (D)* 22 Ryan McKenna (D)* 42 Leonard (Jonas) Hughes (D)* 24 Barbara Fraser (D) 43 Gail McCann Beatty (D) 26 OPEN 44 Jason Kander (D)* 28 No Endorsement 45 Jason R. Holsman (D)* 30 Michael Hoeman (D) 46 Kevin McManus (D) 32 No Endorsement 47 OPEN 34 Martin Rucker (D) 48 Gavin Fletchall (D) MISSOURI HOUSE : 49 Tom McDonald (D)* 1 Keri Cottrell (D) 50 Michael R. -

Congressional Directory MISSOURI

152 Congressional Directory MISSOURI REPRESENTATIVES FIRST DISTRICT WM. LACY CLAY, Democrat, of St. Louis, MO; born in St. Louis, July 27, 1956; edu- cation: Springbrook High School, Silver Spring, MD, 1974; B.S., University of Maryland, 1983, with a degree in government and politics, and a certificate in paralegal studies; public service: Missouri House of Representatives, 1983–91; Missouri State Senate, 1991–2000; nonprofit organizations: St. Louis Gateway Classic Sports Foundation; Mary Ryder Homes; William L. Clay Scholarship and Research Fund; married: Ivie Lewellen Clay; children: Carol, and William III; committees: Financial Services; Oversight and Government Reform; elected to the 107th Congress on November 7, 2000; reelected to each succeeding Congress. Office Listings http://www.lacyclay.house.gov 2418 Rayburn House Office Building, Washington, DC 20515 ................................. (202) 225–2406 Legislative Director / Administrative Assistant.—Michele Bogdanovich. Scheduler.—Karyn Long. Senior Policy Advisor.—Frank Davis. Legislative Assistants.—Richard Pecantee, Marvin Steele. 625 North Euclid Avenue, Suite 326, St. Louis, MO 63108 ...................................... (314) 367–1970 8021 West Florissant, St. Louis, MO 63136 ............................................................... (314) 890–0349 Press Secretary.—Steven Engelhardt. Counties: ST. LOUIS (part). Population (2000), 621,690. ZIP Codes: 63031–34, 63042–44, 63074, 63101–08, 63110, 63112–15, 63117, 63119–22, 63124, 63130–38, 63141, 63145–47, 63150, 63155–56, 63160, 63164, 63166–67, 63169, 63171, 63177–80, 63182, 63188, 63190, 63195–99 *** SECOND DISTRICT W. TODD AKIN, Republican, of St. Louis, MO; born in New York, NY, July 5, 1947; edu- cation: B.S., Worcester Polytechnic Institute, 1971; military service: Officer, U.S. Army Engi- neers; professional: engineer and businessman; IBM; Laclede Steel; taught International Mar- keting, undergraduate level; public service: appointed to the Bicentennial Commission of the U.S. -

Federal Government

CHAPTER 3 FEDERAL GOVERNMENT President Truman and Winston Churchill in Fulton, MO, 1946. Gerald R. Massie 100 OFFICIAL MANUAL Members, President Obama’s Cabinet Joseph R. Biden, Vice President www.whitehouse.gov/vicepresident John Kerry, Secretary of State United States www.state.gov Jack Lew, Secretary, Department of the Treasury Government www.treasury.gov Chuck Hagel, Secretary, Department of Defense www.defense.gov Executive Branch Eric H. Holder Jr., Attorney General, Department Barack H. Obama, President of the United States of Justice The White House www.usdoj.gov 1600 Pennsylvania Ave. N.W., Washington, D.C. 20500 Sally Jewell, Secretary, Department of the Interior Telephone: (202) 456-1414 www.doi.gov www.whitehouse.gov Thomas J. Vilsack, Secretary, Department of Agriculture The president and the vice president of the www.usda.gov United States are elected every four years by a ma- Penny Pritzker, Secretary, Department of jority of votes cast in the Electoral College. These Commerce votes are cast by delegates from each state who www.commerce.gov traditionally vote in accordance with the majority Thomas E. Perez, Secretary, Department of Labor www.dol.gov of the state’s voters. States have as many electoral Kathleen Sebelius, Secretary, Department of college votes as they have congressional del- Health and Human Services egates. Missouri has 10 electoral college votes— www.hhs.gov one for each of the eight U.S. Congress districts Shaun L.S. Donovan, Secretary, Department of and two for the state’s two seats in the U.S. Senate. Housing and Urban Development The president is the chief executive of the Unit- www.hud.gov ed States, with powers to command the armed Anthony Foxx, Secretary, Department of Transportation forces, control foreign policy, grant reprieves and www.dot.gov pardons, make certain appointments, execute all Ernest Moniz, Secretary, Department of Energy laws passed by Congress and present the admin- www.energy.gov istration’s budget. -

Missouri House of Representatives

STATE REPRESENTATIVES 147 Missouri House of Representatives CATHERINE HANAWAY ROD JETTON House of Representatives Officers Speaker, Missouri House of Speaker Pro Tem, Missouri Representatives House of Representatives Catherine Hanaway, Speaker Rod Jetton, Speaker Pro Tem Jason Crowell, Majority Floor Leader Mark Wright, Assistant Majority Floor Leader Chuck Portwood, Majority Caucus Chair Annie Reinhart, Majority Caucus Secretary Chuck Purgason, Majority Whip Mark Abel, Minority Floor Leader Bill Ransdall, Assistant Minority Floor Leader Russ Carnahan, Minority Caucus Chair Terry Young, Minority Caucus Secretary Rick Johnson, Minority Whip Stephen S. Davis, Chief Clerk JASON CROWELL MARK ABEL Ralph Robinett, Sergeant-at-Arms Majority Floor Leader Minority Floor Leader Missouri House of Missouri House of Father David Buescher, Chaplain Representatives Representatives Rev. James Earl Jackson, Chaplain Goodman; Liese; Lipke; Luetkemeyer; Muckler; Committees of the House 2003 Salva; Smith (118); Spreng; Sutherland; Villa; Administration and Accounts: Miller, chair; Yates; Young Morris, vice chair; Behnen; Cooper (120); Appropriations–Health, Mental Health and Cunningham (145); Davis (122); Hampton; Social Services: Purgason, chair; Holand, vice Haywood; McKenna; Reinhart; Richard; Salva; chair; Bean; Brooks; Campbell; Cooper (155); Sander; Wagner Curls; Donnelly; El-Amin; Johnson (61); May; Agriculture: Myers, chair; Sander, vice chair; Page; Phillips; Portwood; Reinhart; Schaaf; Barnitz; Bean; Black; Bringer; Davis (122); Skaggs; Stefanick; -

UTU News, July-August 2004

Volume 36 July/August 2004 Number 7/8 www.utuia.org www.utu.org The Official Publication of the United Transportation Union THE VOICE OF TRANSPORTATION LABOR “Not in my administration will we ever become a member of the Teamsters organization.” – UTU International President Paul C. Thompson NewsNews && NotesNotes UTU fires back in response Little, Boyd sentenced to unprovoked BLE&T raid HOUSTON, Texas – Past UTU presidents Charles L. Little and Byron A. Boyd Jr. were In nationwide mailing, Hahs, Hoffa urge BLE&T members to raid UTU each sentenced July 9 in federal court to 24 months imprisonment and a $10,000 fine by The UTU “will do everything necessary” to nal merger documents and try to address what Judge Sim Lake. protect itself and its members from “aggression concerns you had with those documents. You Both will face three years of supervised by the Brotherhood of Locomotive Engineers have responded that peace is impossible unless release following completion of their sentences. and Trainmen,” UTU International President the UTU joins you in an affiliation with the Both also were ordered to forfeit $100,000. Paul Thompson told BLE&T President Don Teamsters Union. Little and Boyd previously pled guilty to vio- Hahs in a letter dated July 14. “Now you have dropped a bomb on the lating the Racketeer Influenced and Corrupt Organizations Act by soliciting and accepting The letter followed a plea by Hahs and UTU with a new raid on our members,” payments from certain former UTU designated Teamsters President James Hoffa to BLE&T Thompson said, adding: legal counsel. -

Missouri Elections, Pgs. 627-790

CHAPTER 7 Missouri Elections “Working Man” (Missouri State Archives, Putman Collection) 628 OFFICIAL MANUAL When do Missourians register? An unregistered citizen may register to vote whenever local election officials’ places of busi- Missouri ness are open, by requesting an application by mail from the election authority, when renewing a Missouri driver’s license or when receiving services from a participating state agency. Spe- Voting and cial registration sites and dates may be utilized prior to major elections. The deadline for registration is the fourth Elections Wednesday prior to an election. New Missouri residents may register immediately. Who registers to vote in Missouri? When do Missourians vote? Citizens living in Missouri must register in In addition to certain special and emergency order to vote. Any U.S. citizen 17 years and 6 dates, there are six official election dates in Mis- months of age or older, if a Missouri resident, souri: may register and vote except: The statutes require that all public elections • A person who is adjudged incapacitated be held on the general election day, the primary • A person who is confined under sentence election day, the general municipal election day, of imprisonment the first Tuesday after the first Monday in Febru- ary or November, or on another day expressly • A person who is on probation or provided by city or county charter, the first Tues- parole after conviction of a felony until day after the first Monday in June and in nonpri- finally discharged mary years on the first Tuesday after the first • A person who has been convicted of a Monday in August. -

110Th Congress 149

MISSOURI 110th Congress 149 MISSOURI (Population 2000, 5,595,211) SENATORS CHRISTOPHER S. ‘‘KIT’’ BOND, Republican, of Mexico, MO; born in St. Louis, MO, March 6, 1939; education: B.A., cum laude, Woodrow Wilson School of Public and Inter- national Affairs of Princeton University, 1960; J.D., valedictorian, University of Virginia, 1963; held a clerkship with the U.S. Court of Appeals for the Fifth Circuit, 1964; practiced law in Washington, DC, and returned to Missouri, 1967; assistant attorney general of Missouri, 1969; state auditor, 1970; Governor of Missouri, 1973–77, 1981–85; married: the former Linda Holwick; children: Samuel Reid Bond; committees: Appropriations; Environment and Public Works; Small Business and Entrepreneurship; Select Committee on Intelligence; elected to the U.S. Senate on November 4, 1986; reelected to each succeeding Senate term. Office Listings http://bond.senate.gov 274 Russell Senate Office Building, Washington, DC 20510 .................................... (202) 224–5721 Chief of Staff.—Brian Klippenstein. FAX: 224–8149 Legislative Director.—Kara Smith. Legal Counsel.—John Stoody. Scheduling Secretary.—Annie O’Toole. 1001 Cherry Street, Suite 204, Columbia, MO 65201 ................................................ (573) 442–8151 911 Main Street, Suite 2224, Kansas City, MO 64105 ............................................... (816) 471–7141 7700 Bonhomme, Suite 615, Clayton, MO 63105 ...................................................... (314) 725–4484 300 South Jefferson, Suite 401, Springfield, MO 65806 -

Blue Book, Official Manual, Secretary of State, Federal Government, Missouri

CHAPTER 3 Federal Government Edward Gill with his bicycle, 1932 Gill Photograph Collection Missouri State Archives 104 OFFICIAL MANUAL ND DIV TA ID S E D E E PLU UM RI BU N S U W W E D F E A T I L N L U www.doc.gov; SALUS X ESTO LE P O P A U L I S UP R E M M D C C C X X Robert M. Gates, Secretary of Defense; www.defencelink.mil; Margaret Spellings, Secretary of Education; United States www. ed.gov; Samuel W. Bodman, Secretary of Energy; www.energy.gov; Government Michael O. Leavitt, Secretary of Health and Hu man Services; www.hhs.gov; Michael Chertoff, Secretary of Homeland Secu- Executive Branch rity; www.dhs.gov; George W. Bush, President of the United States Alphonso Jackson, Secretary of Housing and The White House Urban Development; www.hud.gov; 1600 Pennsylvania Ave., N.W. Dirk Kempthorne, Secretary of the Interior; Washington, D.C. 20500 www.doi.gov; Telephone: (202) 456-1414 Alberto Gonzales, Attorney General; www.usdoj.gov; www.whitehouse.gov Elaine Chao, Secretary of Labor; www.dol.gov; Condoleezza Rice, Secretary of State; Note: Salary information in this section is taken from www.state.gov; “Legislative, Executive and Judicial Officials: Process for Mary E. Peters, Secretary of Transportation; Adjusting Pay and Current Salaries,” CRS Report for Con- www.dot.gov; gress, 07-13-2007. Henry M. Paulson Jr., Secretary of the Treasury; The president and the vice president of the www.ustreas.gov; United States are elected every four years by a Jim Nicholson, Secretary of Veterans Affairs; majority of votes cast in the electoral college. -

Notice of Election

SAMPLE BALLOT PRIMARY ELECTION AUGUST 2, 2016 COLE COUNTY, MISSOURI NOTICE OF ELECTION Notice is hereby given that the Primary Election will be held in the County of Cole on Tuesday, August 2, 2016 as certified to this office by the participating entities of Cole County. The ballot for the Election shall be in substantially the following form. DEMOCRATIC PARTY REPUBLICAN PARTY REPUBLICAN PARTY FOR UNITED STATES SENATOR FOR UNITED STATES SENATOR FOR STATE REPRESENTATIVE Vote For ONE Vote For ONE DISTRICT 59 CHIEF WANA DUBIE ROY BLUNT Vote For ONE CORI BUSH KRISTI NICHOLS MIKE BERNSKOETTER JASON KANDER BERNIE MOWINSKI RANDY DINWIDDIE ROBERT MACK RYAN D LUETHY FOR STATE REPRESENTATIVE FOR GOVERNOR FOR GOVERNOR DISTRICT 60 Vote For ONE Vote For ONE Vote For ONE LEONARD JOSEPH STEINMAN II CATHERINE HANAWAY JASON (JAY) BARNES CHRIS KOSTER ERIC GREITENS FOR STATE REPRESENTATIVE ERIC MORRISON JOHN BRUNNER DISTRICT 62 CHARLES B. WHEELER PETER D. KINDER Vote For ONE FOR LIEUTENANT GOVERNOR FOR LIEUTENANT GOVERNOR TOM HURST Vote For ONE Vote For ONE FOR EASTERN DISTRICT WINSTON APPLE ARNIE C. - AC DIENOFF COMMISSIONER RUSS CARNAHAN BEV RANDLES Vote For ONE TOMMIE PIERSON, SR. MIKE PARSON JEFF HOELSCHER FOR SECRETARY OF STATE FOR SECRETARY OF STATE FOR WESTERN DISTRICT Vote For ONE Vote For ONE COMMISSIONER BILL CLINTON YOUNG WILL KRAUS Vote For ONE ROBIN SMITH JOHN (JAY) ASHCROFT KRIS SCHEPERLE MD RABBI ALAM ROI CHINN JANET OUSLEY FOR STATE TREASURER FOR STATE TREASURER FOR SHERIFF Vote For ONE Vote For ONE Vote For ONE PAT CONTRERAS ERIC SCHMITT GARY L. HILL JUDY BAKER FOR ATTORNEY GENERAL JOHN WHEELER FOR ATTORNEY GENERAL Vote For ONE RANDY DAMPF Vote For ONE JOSH HAWLEY FOR ASSESSOR JAKE ZIMMERMAN KURT SCHAEFER Vote For ONE TERESA HENSLEY FOR UNITED STATES CHRISTOPHER "CHRIS" D. -

Congressional Directory MISSOURI

152 Congressional Directory MISSOURI REPRESENTATIVES FIRST DISTRICT WM. LACY CLAY, Democrat, of St. Louis, MO; born in St. Louis, July 27, 1956; edu- cation: Springbrook High School, Silver Spring, MD, 1974; B.S., University of Maryland, 1983, with a degree in government and politics, and a certificate in paralegal studies; public service: Missouri House of Representatives, 1983–91; Missouri State Senate, 1991–2000; nonprofit organizations: St. Louis Gateway Classic Sports Foundation; Mary Ryder Homes; William L. Clay Scholarship and Research Fund; married: Ivie Lewellen Clay; children: Carol, and William III; committees: Financial Services; Oversight and Government Reform; elected to the 107th Congress on November 7, 2000; reelected to each succeeding Congress. Office Listings http://www.lacyclay.house.gov 2418 Rayburn House Office Building, Washington, DC 20515 ................................. (202) 225–2406 Legislative Director / Administrative Assistant.—Michele Bogdanovich. Scheduler.—Karyn Long. Senior Policy Advisor.—Frank Davis. Legislative Assistants.—Richard Pecantee, Marvin Steele. 625 North Euclid Avenue, Suite 326, St. Louis, MO 63108 ...................................... (314) 367–1970 8021 West Florissant, St. Louis, MO 63136 ............................................................... (314) 890–0349 Press Secretary.—Steven Engelhardt. Counties: ST. LOUIS (part). Population (2000), 621,690. ZIP Codes: 63031–34, 63042–44, 63074, 63101–08, 63110, 63112–15, 63117, 63119–22, 63124, 63130–38, 63141, 63145–47, 63150, 63155–56, 63160, 63164, 63166–67, 63169, 63171, 63177–80, 63182, 63188, 63190, 63195–99 *** SECOND DISTRICT W. TODD AKIN, Republican, of St. Louis, MO; born in New York, NY, July 5, 1947; edu- cation: B.S., Worcester Polytechnic Institute, 1971; military service: Officer, U.S. Army Engi- neers; professional: engineer and businessman; IBM; Laclede Steel; taught International Mar- keting, undergraduate level; public service: appointed to the Bicentennial Commission of the U.S.