Shimao Property Holdings Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

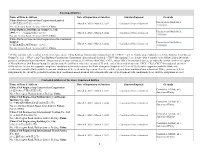

Sanctioned Entities Name of Firm & Address Date

Sanctioned Entities Name of Firm & Address Date of Imposition of Sanction Sanction Imposed Grounds China Railway Construction Corporation Limited Procurement Guidelines, (中国铁建股份有限公司)*38 March 4, 2020 - March 3, 2022 Conditional Non-debarment 1.16(a)(ii) No. 40, Fuxing Road, Beijing 100855, China China Railway 23rd Bureau Group Co., Ltd. Procurement Guidelines, (中铁二十三局集团有限公司)*38 March 4, 2020 - March 3, 2022 Conditional Non-debarment 1.16(a)(ii) No. 40, Fuxing Road, Beijing 100855, China China Railway Construction Corporation (International) Limited Procurement Guidelines, March 4, 2020 - March 3, 2022 Conditional Non-debarment (中国铁建国际集团有限公司)*38 1.16(a)(ii) No. 40, Fuxing Road, Beijing 100855, China *38 This sanction is the result of a Settlement Agreement. China Railway Construction Corporation Ltd. (“CRCC”) and its wholly-owned subsidiaries, China Railway 23rd Bureau Group Co., Ltd. (“CR23”) and China Railway Construction Corporation (International) Limited (“CRCC International”), are debarred for 9 months, to be followed by a 24- month period of conditional non-debarment. This period of sanction extends to all affiliates that CRCC, CR23, and/or CRCC International directly or indirectly control, with the exception of China Railway 20th Bureau Group Co. and its controlled affiliates, which are exempted. If, at the end of the period of sanction, CRCC, CR23, CRCC International, and their affiliates have (a) met the corporate compliance conditions to the satisfaction of the Bank’s Integrity Compliance Officer (ICO); (b) fully cooperated with the Bank; and (c) otherwise complied fully with the terms and conditions of the Settlement Agreement, then they will be released from conditional non-debarment. If they do not meet these obligations by the end of the period of sanction, their conditional non-debarment will automatically convert to debarment with conditional release until the obligations are met. -

The Annual Report on the Most Valuable and Strongest Real Estate Brands June 2020 Contents

Real Estate 25 2020The annual report on the most valuable and strongest real estate brands June 2020 Contents. About Brand Finance 4 Get in Touch 4 Brandirectory.com 6 Brand Finance Group 6 Foreword 8 Executive Summary 10 Brand Finance Real Estate 25 (USD m) 13 Sector Reputation Analysis 14 COVID-19 Global Impact Analysis 16 Definitions 20 Brand Valuation Methodology 22 Market Research Methodology 23 Stakeholder Equity Measures 23 Consulting Services 24 Brand Evaluation Services 25 Communications Services 26 Brand Finance Network 28 © 2020 All rights reserved. Brand Finance Plc, UK. Brand Finance Real Estate 25 June 2020 3 About Brand Finance. Brand Finance is the world's leading independent brand valuation consultancy. Request your own We bridge the gap between marketing and finance Brand Value Report Brand Finance was set up in 1996 with the aim of 'bridging the gap between marketing and finance'. For more than 20 A Brand Value Report provides a years, we have helped companies and organisations of all types to connect their brands to the bottom line. complete breakdown of the assumptions, data sources, and calculations used We quantify the financial value of brands We put 5,000 of the world’s biggest brands to the test to arrive at your brand’s value. every year. Ranking brands across all sectors and countries, we publish nearly 100 reports annually. Each report includes expert recommendations for growing brand We offer a unique combination of expertise Insight Our teams have experience across a wide range of value to drive business performance disciplines from marketing and market research, to and offers a cost-effective way to brand strategy and visual identity, to tax and accounting. -

Oktober 2019 Warengruppe Name Adresse Land Mitarbeiter

Produktionsstätten nach Warengruppe Letzte Aktualisierung: Oktober 2019 Warengruppe Name Adresse Land Mitarbeiteranzahl Bekleidungstextilien 8. Mart d.o.o. Sencanski Put 85, 24000 Subotica, Vojvodina Serbien 501-1000 ABM Fashions Ltd. Kashimpur Road, Holding No. 1143-1145, Konabari, 1751 Gazipur Bangladesch 3001-4000 AKH Stitch Art Ltd. Chandanpur, Rajfulbaria,Hemayetpur, Savar, 1340 Dhaka Bangladesch 2001-3000 Amity (Myanmar) Lingerie Co., Ltd. Plot No.53, Kwin No.1190(Kha), East of Gonminn Inn, Inndagaw, Bago Myanmar (früher Birma) 0-500 Ananta Jeanswear Ltd. Kabi Jashim Uddin Road No. 134/123, Pagar, Tongi, 1710 Gazipur Bangladesch 3001-4000 Anhui Runtex Fashion Co., Ltd. Jincheng (West) Road, Langxi Economic and Industry District, Xuancheng, Langxi Volksrepublik China 0-500 County, Anhui Anyang Yiyang Clothing Manufact. Co., Ltd. Anyang Textiles Industry District, Children Garment City, Tower 2 West, Anyang, Henan Volksrepublik China 0-500 Asdet (Myanmar) Garment Co., Ltd Shwe Lin Pan Industrial Zone, Plot No. 458, Hlaing Thar Yar Township,Yangon Myanmar (früher Birma) 501-1000 Aspire Garments Ltd. 491, Dhalla Bazar, Singair,1820 Manikganj Bangladesch 2001-3000 Best Hubo Co., Ltd. U Myuu Street, Plot No. 7,8, Myay Taing Block No. 65 (Settmu), Yangon, Shwe Pyithar Myanmar (früher Birma) 1001-2000 Township BHIS Apparels Ltd. Dattapara No. 671, 0-5 Floor, Tongi, Hossain Market, 1712 Gazipur/Dhaka Bangladesch 2001-3000 Blue Planet Knitwear Ltd. P.O: Tengra, Sreepur, Sreepur, Gazipur District 1740, Dhaka Bangladesch 1001-2000 Burcu Tekstil San. ve Tic A.S. (Duzce Subesi) D-100 Karayolu Uzeri Altinpinar Koyu no. 8, 81100 Duezce Türkei 0-500 Caelygirl (Anhui) Co., Ltd. Ruquan Blvd. -

出口鳗鱼产品加工企业及其配套备案养殖场最新名单 配套养鳗场 鳗鱼产品加工厂 序号 中英文名称 备案号 备注 中英文名称 中英文地址 注册号 宁波徐龙水产有限公司 1 3900/M0002 Ningbo Xulong Aquatic Co.,Ltd

別表30 中国産養殖鰻加工品検査命令免除業者 出口鳗鱼产品加工企业及其配套备案养殖场最新名单 配套养鳗场 鳗鱼产品加工厂 序号 中英文名称 备案号 备注 中英文名称 中英文地址 注册号 宁波徐龙水产有限公司 1 3900/M0002 Ningbo Xulong Aquatic Co.,Ltd.. 宁波旦晨食品有限公司 慈溪市经济开发区担山北路418号 No.418, 东台市东升鳗鱼养殖场 2 3200/M0014 (Ningbo Danchen Food Industry Danshan North Rd.,Cixi Economic 3302/02051 DONGTAI DONGSHENG EEL BREEDING CO.,LTD. Co.LTD ) Development Zone 东台市徐龙鳗鱼养殖场 3 3200/M0015 DONGTAI XULONG EEL BREEDING CO.,LTD. 台山市胜记鳗鱼养殖场 4 4400/M586 SHENGJI EEL FARMS OF TAISHAN CITY 台山市徐南水产养殖有限公司 5 4400/M602 XUNAN AQUATIC PRODUCTS COMPANY LIMITED OF TAISHAN CITY 台山市端芬镇朋诚水产养殖场 6 4400/M626 TAISHAN PENGCHENG AQUAFARM 台山市海宴兴中鳗鱼养殖场 7 4400/M628 XINGZHONG EEL FARM OF HAIYAN TAISHAN CITY 佛山市顺德区东龙烤鳗有限公司 广东省佛山市顺德区杏坛镇新冲工业区 台山市斗山镇永利园水产养殖场 8 4400/M814 FOSHAN SHUNDE DONGLONG ROASTED XINCHONG INDUSTRIAL ZONE XINTAN TOWN 4400/02152 YOULIYUAN AQUAFARM OF DOUSHAN TAISHAN CITY EEL CO.,LTD SHUNDE GUANGDONG 顺德徐顺水产养殖贸易有限公司有记鳗鱼养殖场 9 YOUJI EEL FARM OF SHUNDE XUSHUN AQUATIC BREEDING &TRADE 4400/M815 CO., LTD. 台山市海宴镇沙湾鳗鱼场 10 4400/M844 TAISHAN CITY HAIYAN TOWN SHAWAN EEL BREEDING FARM 台山市威信鳗鱼养殖场 11 4400/M852 TAISHAN CITY WEIXIN EEL BREEDING FARM 饶平县黄岗镇隆生鳗鱼养殖场 12 4400/M527 RAOPING COUNTY HUANGGANG TOWN LONGSHENG EEL BREEDING FARM 广东省饶平县黄冈镇龙眼城村 饶平县健力食品有限公司 LONGYANCHEN VILLAGE,HUANGGANG 4400/02243 RAOPING JIANLI FOOD CO.,LTD 饶平县烤鳗厂有限公司鳗鱼养殖基地 TOWN,RAOPING COUNTY,GUANGDONG,CHINA 13 4400/M892 RAOPING COUNTY EEL ROASTING FACTORY CO.,LTD. BREEDING BASE 配套养鳗场 鳗鱼产品加工厂 序号 中英文名称 备案号 备注 中英文名称 中英文地址 注册号 潮安县古巷华光养鳗场 14 4400/M024 CHAOAN GUXIANG HUAGUANG EEL BREEDING FARM 潮安县古巷岭后养鳗场 15 4400/M151 CHAOAN GUXIANG LINGHOU EEL BREEDING FARM 潮安县古巷华江水产养殖场 16 4400/M518 潮州市华海水产有限公司 广东潮安古巷镇 CHAOAN GUXIANG HUAJIANG AQUAFARM CHAOZHOU HUAHAI AQUATIC PRODUCTS GUXIANG TOWN,CHAOAN COUNTY GUANGDONG, 4400/02188 潮安县登塘华湖水产养殖场 CO., LTD. -

2018年第四季度在越南注册的中国水产企业名单the List of Chinese Registered Fishery Processing Export Establish

2018年第四季度在越南注册的中国水产企业名单 The List of Chinese Registered Fishery Processing Export Establishments to Vietnam (Total 744,the Fourth quarter of 2018,updated on October 10th, 2018 ) 产品 No. Est.No. 企业名称(中文) Est.Name 企业地址(中文) Est.Address (Products) 北海市嘉盈冷冻食品 BEIHAI JIAYING FROZEN NO.156 IN THE THIRD LANE THREE WAISHA Fishery 1 4500/02059 广西北海市外沙三巷156号 有限公司 FOOD CO.,LTD. ISLAND BEIHAI,GUANGXI,CHINA. Products Funing county boyuan Yegezhuang village taiying town 抚宁县渤远水产品有 秦皇岛市抚宁县台营镇埜各庄 Fishery 2 1300/02229 aquatic products co.,ltd funing county qinhuangdao city hebei 限公司 村 Products province Wugezhuang Village Jingan Town 昌黎县永军冷冻食品 Changli County Yongjun 河北省秦皇岛市昌黎县靖安镇 Fishery 3 1300/02239 Changli County Qinhuangdao City,Hebei 有限公司 Freezing Food Co.,Ltd. 吴各庄 Products Province,China Zhazili Village, Dapuhe Town, Changli 昌黎县嘉辉水产食品 ChangLi Jiahui Aquatic Fishery 4 1300/02244 大蒲河镇栅子里村 County, Qinhuangdao City, Hebei 有限责任公司 Products Co., Ltd. Products Province, China Nandaihe Village, Funing County, 秦皇岛市成财食品有 Qinhuangdao Chengcai Fishery 5 1300/02245 秦皇岛市抚宁县南戴河村 Qinhuangdao City, Hebei Province, 限公司 Foodstuff Co., Ltd. Products China Tuanlinzhong Village,Tuanlin 秦皇岛鑫海食品有限 Qinhuangdao Xinhai 秦皇岛市昌黎县团林乡团林中 Fishery 6 1300/02247 Town,Changli County,Qinhuangdao 公司 Foodstuffs Co., Ltd. 村 Products City,Hebei Province, China Qinhuangdao Gangwan Industrial Park, Changli County, 秦皇岛港湾水产有限 Fishery 7 1300/02259 Aquatic Products Co., 秦皇岛昌黎县工业园区 Qinhuangdao City, Hebei Province, 公司 Products Ltd. China 秦皇岛靖坤食品有限 Qinhuangdao Jingkun Foods North Of Dapuhekou,Dapuhe Town, Fishery 8 1300/02261 昌黎县大蒲河镇大蒲河口北 责任公司 Co.,Ltd. Changli County, Hebei Province Products Changli Haidong Aquatic South Chiyangkou Village, Changli 昌黎县海东水产食品 Fishery 9 1300/02262 Product And Food Stuff 昌黎县赤洋口村南 County, Qinhuangdao City, Hebei 有限责任公司 Products Co., Ltd. Province, China Industrial Park, Changli County, 昌黎县禄权水产有限 Changli Luquan Aquatic Fishery 10 1300/02263 秦皇岛昌黎县工业园区 Qinhuangdao City, Hebei Province, 责任公司 Products Co., Ltd. -

Download Article

Advances in Social Science, Education and Humanities Research, volume 324 International Conference on Architecture: Heritage, Traditions and Innovations (AHTI 2019) Exploration on the Protection Scheme of the Great Ruins of Southern Lifang District in the Luoyang City Site in Sui and Tang Dynasties Haixia Liang Luoyang Institute of Science and Technology Luoyang, China Peiyuan Li Zhenkun Wang Xi’an University of Architecture and Technology China Petroleum First Construction Company (Luoyang) Xi'an, China Luoyang, China Abstract—The great ruins are a kind of non-renewable district in a comprehensive and detailed way. Through the precious resources. The southern Lifang district in the analysis of the current situation of southern Lifang district, a Luoyang City Site in Sui and Tang Dynasties is the product of relatively reasonable planning proposal is obtained. This the development of ancient Chinese capital to a certain study can provide theoretical or practical reference and help historical stage. As many important relics and rich cultural on the protection and development of Luoyang City Site in history have been excavated here, the district has a rich Sui and Tang Dynasties, as well as the reconstruction of humanity history. In the context of the ever-changing urban southern Lifang district. construction, the protection of the great ruins in the district has become more urgent. From the point of view of the protection of the great ruins, this paper introduces the II. GREAT RUINS, SUI AND TANG DYNASTIES, LUOYANG important sites and cultural relics of southern Lifang district CITY AND LIFANG DISTRICT in Luoyang city of the Sui and Tang Dynasties through field Great ruins refer to large sites or groups of sites with a investigation and literature review. -

Deciphering the Spatial Structures of City Networks in the Economic Zone of the West Side of the Taiwan Strait Through the Lens of Functional and Innovation Networks

sustainability Article Deciphering the Spatial Structures of City Networks in the Economic Zone of the West Side of the Taiwan Strait through the Lens of Functional and Innovation Networks Yan Ma * and Feng Xue School of Architecture and Urban-Rural Planning, Fuzhou University, Fuzhou 350108, Fujian, China; [email protected] * Correspondence: [email protected] Received: 17 April 2019; Accepted: 21 May 2019; Published: 24 May 2019 Abstract: Globalization and the spread of information have made city networks more complex. The existing research on city network structures has usually focused on discussions of regional integration. With the development of interconnections among cities, however, the characterization of city network structures on a regional scale is limited in the ability to capture a network’s complexity. To improve this characterization, this study focused on network structures at both regional and local scales. Through the lens of function and innovation, we characterized the city network structure of the Economic Zone of the West Side of the Taiwan Strait through a social network analysis and a Fast Unfolding Community Detection algorithm. We found a significant imbalance in the innovation cooperation among cities in the region. When considering people flow, a multilevel spatial network structure had taken shape. Among cities with strong centrality, Xiamen, Fuzhou, and Whenzhou had a significant spillover effect, which meant the region was depolarizing. Quanzhou and Ganzhou had a significant siphon effect, which was unsustainable. Generally, urbanization in small and midsize cities was common. These findings provide support for government policy making. Keywords: city network; spatial organization; people flows; innovation network 1. -

China Equity Strategy

June 5, 2019 09:40 AM GMT MORGAN STANLEY ASIA LIMITED+ China Equity Strategy | Asia Pacific Jonathan F Garner EQUITY STRATEGIST [email protected] +852 2848-7288 The Rubio "Equitable Act" - Our Laura Wang EQUITY STRATEGIST [email protected] +852 2848-6853 First Thoughts Corey Ng, CFA EQUITY STRATEGIST [email protected] +852 2848-5523 Fran Chen, CFA A new bill sponsored by US Senator Marco Rubio has the EQUITY STRATEGIST potential to cause significant change in the listing domains of [email protected] +852 2848-7135 Chinese firms. After the market close in the US yesterday 4th June the Wall Street Journal published an Op-Ed by US Senator Marco Rubio in which he announced that he intends to sponsor the “Equitable Act” – an acronym for Ensuring Quality Information and Transparency for Abroad-Based Listings on our Exchanges. At this time the text of the bill has not been published and we are seeking additional information about its contents and likelihood of passing. However, our early reaction is that this has the potential to cause significant changes in the domain for listings of Chinese firms going forward with the potential for de- listing of Chinese firms on US exchanges and re-listing elsewhere (most likely Hong Kong). More generally we see this development as part of an increased escalation of tensions between China and the US on multiple fronts which should cap the valuation multiple for China equities, in particular in the offshore index constituents and US-listed parts of the universe. We provide a list of the potentially impacted China / HK names with either primary or secondary listings on Amex, NYSE or Nasdaq. -

High People's Court of Fujian Province Civil Judgement

High People's Court of Fujian Province Civil Judgement (2015) Min Min Zhong Zi No.2060 Appellant (defendant of the first instance): Xie Zhijin, Male, DOB: 10/27/1963, Han Chinese, Self-employed, residing in Cangshan District, Fuzhou, Fujian Appellant (defendant of the first instance): Ni Mingxiang, Male, DOB: 03/28/1965, Han Chinese, Farmer, residing in Fuqing, Fujian Appellant (defendant of the first instance): Zheng Shijiang, Male, DOB: 04/04/1966, Han Chinese, Farmer, residing in Fuqing, Fujian Attorney of the three appellants above: Xie Changling, Zhong Yin (Fuzhou) Law Firm. Appellee (plaintiff of the first instance): Friends of Nature Domicile: Room A201, Building 2, No. 12 Yumin Road, Chaoyang District, Beijing Legal Representative: Zhang Hehe, Deputy Director-General Entrusted Agent: Ge Feng, Female, Director of Legal and Policy Affairs, residing in Wuchang District, Wuhan Attorney: Liu Xiang, Golden Diamond Law Firm Appellee (plaintiff of the first instance): Fujian Green Home Environment-friendly Center Domicile: 3H, Buidling B, Hot Spring Park, Yingji Road No. 38, Gulou District, Fuzhou, Fujian Legal Representative: Lin Meiying, Director Attorney: Wu Anxin, Hubei Longzhong Law Firm Defendant of the First Instance: Li Mingshuo, Male, DOB: 12/16/1968, Han Chinese, Farmer, residing in Taishun County, Zhejiang Attorney: Qiu Shuhua, Fujian Quanxin Law Firm Third Party of the First Instance: Yanping District Land Resources Bureau of Nanping Municipal Land Resources Bureau Domicile: Shengli Street No. 182, Yanping District, Nanping, Fujian Legal Representative: Huang Ge, Director-General Attorney: He Jianhua, Fujian Shunning Law Firm Third Party of the First Instance: Yanping District Forestry Bureau of Nanping Municipal Forestry Bureau Domicile: Chaoyang Street No. -

Sustainability Development Work Sustainability Development Work

2019 Shimao Group Holdings Limited Sustainability Report Chairman's Message Chairman's Message Harmonic co-existence and empowered development Invest in philanthropy and conserve cultural legacy In 2019, due to the advantage of diverse business and investment Over the years, Shimao adheres its originality and takes social planning in advance, Shimao shifted from the role of city operator responsibility. At present, Shimao is actively engaged in philanthropic to the role of city empowerment, the core of which is framework of sectors, such as cultural inheritance, medical assistance for poverty Big Plane Strategy: body is the property development; wings are the alleviation, community care, life illumination, etc. commercial office, property management, hotel operation, culture and Chairman's Message entertainment; stabilizers are high technology, healthcare, education, In 2019, Shimao continued to invest into the conservation of cultural elder care, finance and etc. The rapid-moving Big Plane will power up legacy and integrated Chinese cultural IP into products and service through those components, injecting the power into the sustainable of Shimao, energizing traditional Chinese culture in current popular development and working on high-quality and better life of people. market. From Quanzhou Shimao • The Palace Museum Maritime Silk Road Museum (temporary name) to The Forbidden City Gallery • Wuyi Activating the new engine of Chinese economy and attracting Mountain Branch, Shimao keeps exploring and practicing and shifted worldwide attention -

Set out Below Is a Summary of the Major Property Development Projects of the Group As at 31 December 2019: Major Development

1 Set out below is a summary of the major property development projects of the Group as at 31 December 2019: Major Development Properties Pre-sold Interest Approximate Planned during Total attributable site area total GFA the year GFA sold Expected Projects of Type of to SI (square (square (square (square date of City SI Development property Development meters) meters) meters) meters) completion 1 Kaifu District, Fengsheng Building Residential and 90% 5,468 70,566 6,627 30,870 Completed Changsha commercial 2 Chenghua District, Hi-Shanghai Residential and 100% 61,506 254,885 4,996 190,153 Completed Chengdu commercial 3 Beibei District, Hi-Shanghai Residential and 100% 30,845 74,935 3,301 57,626 Completed Chongqing commercial 4 Yuhang District, Hi-Shanghai (Phase I) Residential and 85% 74,864 230,484 27,758 150,289 Completed Hangzhou commercial 5 Yuhang District, Hi-Shanghai (Phase II) Residential and 85% 59,640 198,203 56,539 – Completed Hangzhou commercial 6 Wuxing District, SIIC Garden Hotel Hotel and 100% 116,458 47,177 – – Completed Huzhou commercial 7 Wuxing District, Hurun Commercial Commercial 100% 13,661 27,322 – – Under Huzhou Plaza planning 8 Wuxing District, SIIC Tianlan Bay Residential and 100% 115,647 193,292 26,042 – Completed Huzhou commercial 9 Wuxing District, SIIC Yungjing Bay Residential 100% 68,471 207,906 28,953 – 2020 Huzhou 10 Shilaoren National International Beer City Composite 100% 227,675 806,339 – 333,798 2014 to 2022, Tourist Resort, Qingdao in phases 11 Fengze District, Sea Palace Residential and 100% 170,133 -

Shop Direct Factory List Dec 18

Factory Factory Address Country Sector FTE No. workers % Male % Female ESSENTIAL CLOTHING LTD Akulichala, Sakashhor, Maddha Para, Kaliakor, Gazipur, Bangladesh BANGLADESH Garments 669 55% 45% NANTONG AIKE GARMENTS COMPANY LTD Group 14, Huanchi Village, Jiangan Town, Rugao City, Jaingsu Province, China CHINA Garments 159 22% 78% DEEKAY KNITWEARS LTD SF No. 229, Karaipudhur, Arulpuram, Palladam Road, Tirupur, 641605, Tamil Nadu, India INDIA Garments 129 57% 43% HD4U No. 8, Yijiang Road, Lianhang Economic Development Zone, Haining CHINA Home Textiles 98 45% 55% AIRSPRUNG BEDS LTD Canal Road, Canal Road Industrial Estate, Trowbridge, Wiltshire, BA14 8RQ, United Kingdom UK Furniture 398 83% 17% ASIAN LEATHERS LIMITED Asian House, E. M. Bypass, Kasba, Kolkata, 700017, India INDIA Accessories 978 77% 23% AMAN KNITTINGS LIMITED Nazimnagar, Hemayetpur, Savar, Dhaka, Bangladesh BANGLADESH Garments 1708 60% 30% V K FASHION LTD formerly STYLEWISE LTD Unit 5, 99 Bridge Road, Leicester, LE5 3LD, United Kingdom UK Garments 51 43% 57% AMAN GRAPHIC & DESIGN LTD. Najim Nagar, Hemayetpur, Savar, Dhaka, Bangladesh BANGLADESH Garments 3260 40% 60% WENZHOU SUNRISE INDUSTRIAL CO., LTD. Floor 2, 1 Building Qiangqiang Group, Shanghui Industrial Zone, Louqiao Street, Ouhai, Wenzhou, Zhejiang Province, China CHINA Accessories 716 58% 42% AMAZING EXPORTS CORPORATION - UNIT I Sf No. 105, Valayankadu, P. Vadugapal Ayam Post, Dharapuram Road, Palladam, 541664, India INDIA Garments 490 53% 47% ANDRA JEWELS LTD 7 Clive Avenue, Hastings, East Sussex, TN35 5LD, United Kingdom UK Accessories 68 CAVENDISH UPHOLSTERY LIMITED Mayfield Mill, Briercliffe Road, Chorley Lancashire PR6 0DA, United Kingdom UK Furniture 33 66% 34% FUZHOU BEST ART & CRAFTS CO., LTD No. 3 Building, Lifu Plastic, Nanshanyang Industrial Zone, Baisha Town, Minhou, Fuzhou, China CHINA Homewares 44 41% 59% HUAHONG HOLDING GROUP No.