Central Africa Economic Outlook 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

From Operation Serval to Barkhane

same year, Hollande sent French troops to From Operation Serval the Central African Republic (CAR) to curb ethno-religious warfare. During a visit to to Barkhane three African nations in the summer of 2014, the French president announced Understanding France’s Operation Barkhane, a reorganization of Increased Involvement in troops in the region into a counter-terrorism Africa in the Context of force of 3,000 soldiers. In light of this, what is one to make Françafrique and Post- of Hollande’s promise to break with colonialism tradition concerning France’s African policy? To what extent has he actively Carmen Cuesta Roca pursued the fulfillment of this promise, and does continued French involvement in Africa constitute success or failure in this rançois Hollande did not enter office regard? France has a complex relationship amid expectations that he would with Africa, and these ties cannot be easily become a foreign policy president. F cut. This paper does not seek to provide a His 2012 presidential campaign carefully critique of President Hollande’s policy focused on domestic issues. Much like toward France’s former African colonies. Nicolas Sarkozy and many of his Rather, it uses the current president’s predecessors, Hollande had declared, “I will decisions and behavior to explain why break away from Françafrique by proposing a France will not be able to distance itself relationship based on equality, trust, and 1 from its former colonies anytime soon. solidarity.” After his election on May 6, It is first necessary to outline a brief 2012, Hollande took steps to fulfill this history of France’s involvement in Africa, promise. -

Deconstructing Windhoek: the Urban Morphology of a Post-Apartheid City

No. 111 DECONSTRUCTING WINDHOEK: THE URBAN MORPHOLOGY OF A POST-APARTHEID CITY Fatima Friedman August 2000 Working Paper No. 111 DECONSTRUCTING WINDHOEK: THE URBAN MORPHOLOGY OF A POST-APARTHEID CITY Fatima Friedman August 2000 DECONSTRUCTING WINDHOEK: THE URBAN MORPHOLOGY OF A POST-APARTHEID CITY Contents PREFACE 1. INTRODUCTION ................................................................................................. 1 2. WINDHOEK CONTEXTUALISED ....................................................................... 2 2.1 Colonising the City ......................................................................................... 3 2.2 The Apartheid Legacy in an Independent Windhoek ..................................... 7 2.2.1 "People There Don't Even Know What Poverty Is" .............................. 8 2.2.2 "They Have a Different Culture and Lifestyle" ...................................... 10 3. ON SEGREGATION AND EXCLUSION: A WINDHOEK PROBLEMATIC ........ 11 3.1 Re-Segregating Windhoek ............................................................................. 12 3.2 Race vs. Socio-Economics: Two Sides of the Segragation Coin ................... 13 3.3 Problematising De/Segregation ...................................................................... 16 3.3.1 Segregation and the Excluders ............................................................. 16 3.3.2 Segregation and the Excluded: Beyond Desegregation ....................... 17 4. SUBURBANISING WINDHOEK: TOWARDS GREATER INTEGRATION? ....... 19 4.1 The Municipality's -

East and Central Africa 19

Most countries have based their long-term planning (‘vision’) documents on harnessing science, technology and innovation to development. Kevin Urama, Mammo Muchie and Remy Twingiyimana A schoolboy studies at home using a book illuminated by a single electric LED lightbulb in July 2015. Customers pay for the solar panel that powers their LED lighting through regular instalments to M-Kopa, a Nairobi-based provider of solar-lighting systems. Payment is made using a mobile-phone money-transfer service. Photo: © Waldo Swiegers/Bloomberg via Getty Images 498 East and Central Africa 19 . East and Central Africa Burundi, Cameroon, Central African Republic, Chad, Comoros, Congo (Republic of), Djibouti, Equatorial Guinea, Eritrea, Ethiopia, Gabon, Kenya, Rwanda, Somalia, South Sudan, Uganda Kevin Urama, Mammo Muchie and Remy Twiringiyimana Chapter 19 INTRODUCTION which invest in these technologies to take a growing share of the global oil market. This highlights the need for oil-producing Mixed economic fortunes African countries to invest in science and technology (S&T) to Most of the 16 East and Central African countries covered maintain their own competitiveness in the global market. in the present chapter are classified by the World Bank as being low-income economies. The exceptions are Half the region is ‘fragile and conflict-affected’ Cameroon, the Republic of Congo, Djibouti and the newest Other development challenges for the region include civil strife, member, South Sudan, which joined its three neighbours religious militancy and the persistence of killer diseases such in the lower middle-income category after being promoted as malaria and HIV, which sorely tax national health systems from low-income status in 2014. -

(EIA) Undertaken for the 3-Dimensional (3D) Marine Seismic Survey Programme Proposed by GALP Through Its Namibian Subsidiary Windhoek PEL 23 B.V

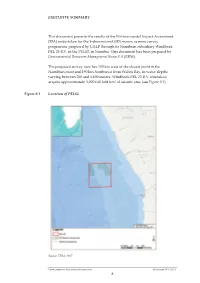

EXECUTIVE SUMMARY This document presents the results of the Environmental Impact Assessment (EIA) undertaken for the 3-dimensional (3D) marine seismic survey programme proposed by GALP through its Namibian subsidiary Windhoek PEL 23 B.V. in the PEL82, in Namibia. This document has been prepared by Environmental Resources Management Iberia S.A (ERM). The proposed survey area lies 100 km west of the closest point in the Namibian coast and 190 km Northwest from Walvis Bay, in water depths varying between 200 and 1,800 meters. Windhoek PEL 23 B.V. intends to acquire approximately 3,000 full fold km 2 of seismic area (see Figure 0.1 ). Figure 0.1 Location of PEL82 Source: ERM, 2017 ENVIRONMENTAL RESOURCES MANAGEMENT WI NDHOEK PEL 23 B.V. 8 Legislation, legal and institutional framework standards In Namibia, the main environmental institution is the Ministry of Environment and Tourism (MET). It is the competent body responsible for aspects related with natural resources management, conservation and environment, including environmental management of in-country resources and approval of all sector EIAs. Key regulations, legislation, as well as international conventions and standards relevant to the Project, are summarized in Table 0.1. Table 0.1 Key Namibian regulations and international conventions relevant to the Project Thematic Reference National Environment Environmental Management Act (Act 7 of 2007 Framework Nature Conservation Ordinance (Ordinance 4 of 1975), Nature Conservation Amendment Act (Act 5 of 1996) Marine Resources Act (Act 27 of 2000) Hydrocarbons Petroleum (Exploration and Production) Act. Act 2 of 1991. Amended by the Petroleum Laws Amendment Act, 1998 Petroleum Act Regulations, 1991. -

CISO Alliances Windhoek 2018 Results

Windhoek Chapter 13th November 2018 Results // 1 Alliance - ‘A union formed for mutual benefit’ 08:30 – 09:00 Registration 09:00 – 09:20 Housekeeping, purpose driver and format reminder Russell Nel – Director Southern Africa – CISO Alliances Tom Williams – Director Namibia – CISO Alliances Session 1 9:20 - 9:35 - Use Case Overview 9:35 - 10:00 - Open Forum Does the Namibian IT climate understand what InfoSec is? Russell Nel – Director Southern Africa – CISO Alliances Session 2 10:00 - 10:15 - Use Case Overview 10:15 - 10:45 - Open Forum What are we missing with regard to InfoSec within our business’? Russell Nel – Director Southern Africa – CISO Alliances 10:45 - 11:10 Networking Break Session 3 11:10 - 11:35 - Use Case Overview 11:35 - 12:00 - Open Forum Molecular Security Sonja Coetzer – Solutions Advocate – Salt Essential IT 12:00 - 13:00 Networking Lunch Session 4 13:00 - 13:15 - Use Case Overview 13:15 - 14:00 - Open Forum Unconference Russell Nel – Director Southern Africa – CISO Alliances Tom Williams – Director Namibia – CISO Alliances Session 5 14:00 - 14:15 - Use Case Overview 14:15 - 14:45 - Open Forum Go your own way Russell Nel – Director Southern Africa – CISO Alliances Richard Bastiaans Tiaan Bazuin Holger Bössow Derick Briers Head Information CEO Head IT Security CEO Communication Namibian Stock Standard Bank inTouch Technology Exchange Interactive Nedbank Namibia Marketing Shaun Fobian Valerie Garises Martin Hamukwaya Marsorry Ickua Manager: CTO Information System Director: IT Security Officer Information And Namibia Institute -

West and Central Africa Regional Report BTI 2016

West and Central Africa Beyond catastrophes Religiously motivated violence, the Ebola epidemic and widespread poverty: West and Central Africa has repeatedly made negative headlines in recent years. By contrast, the trends and developments giving rise to hope remain largely unnoticed. For international observers, the verdict of- political force. In Mauritania, for example, democracies. This is a fi rst, as the BTI has ten seems clear: Sub-Saharan Africa, par- the military consolidated its power from never before classified a greater number ticularly the countries in West and Central within the shadows of a façade democracy, of countries in West and Central Africa Africa, stand for civil war, crisis, disease while in Burkina Faso, the military over- as being democratically governed. Peace- and catastrophe. And there is plenty of evi- threw longtime President Blaise Compaoré, ful transfers of power at the ballot box are dence for this to be found in the BTI 2016. whose plans to extend his rule had trig- happening more frequently. During this edition’s review period, sectar- gered unrest. There are also encouraging signs to be ian violence appears to have gained ground. All of this is countered by positive de- found in socioeconomic terms. An improve- Islamist terror raged in Nigeria and began velopments and events, often unnoticed by ment in living standards is evident despite to spill over into neighboring states, while the Western public, which give cause for the persistence of poverty. Particularly since bloody clashes between Christians and Mus- hope. Classical assumptions about success- 2000, the region’s Human Development In- lims claimed numerous victims in the Cen- ful democratization that draw on moderniza- dex (HDI) scores, as calculated by the United tral African Republic. -

Organized Crime and Instability in Central Africa

Organized Crime and Instability in Central Africa: A Threat Assessment Vienna International Centre, PO Box 500, 1400 Vienna, Austria Tel: +(43) (1) 26060-0, Fax: +(43) (1) 26060-5866, www.unodc.org OrgAnIzed CrIme And Instability In CenTrAl AFrica A Threat Assessment United Nations publication printed in Slovenia October 2011 – 750 October 2011 UNITED NATIONS OFFICE ON DRUGS AND CRIME Vienna Organized Crime and Instability in Central Africa A Threat Assessment Copyright © 2011, United Nations Office on Drugs and Crime (UNODC). Acknowledgements This study was undertaken by the UNODC Studies and Threat Analysis Section (STAS), Division for Policy Analysis and Public Affairs (DPA). Researchers Ted Leggett (lead researcher, STAS) Jenna Dawson (STAS) Alexander Yearsley (consultant) Graphic design, mapping support and desktop publishing Suzanne Kunnen (STAS) Kristina Kuttnig (STAS) Supervision Sandeep Chawla (Director, DPA) Thibault le Pichon (Chief, STAS) The preparation of this report would not have been possible without the data and information reported by governments to UNODC and other international organizations. UNODC is particularly thankful to govern- ment and law enforcement officials met in the Democratic Republic of the Congo, Rwanda and Uganda while undertaking research. Special thanks go to all the UNODC staff members - at headquarters and field offices - who reviewed various sections of this report. The research team also gratefully acknowledges the information, advice and comments provided by a range of officials and experts, including those from the United Nations Group of Experts on the Democratic Republic of the Congo, MONUSCO (including the UN Police and JMAC), IPIS, Small Arms Survey, Partnership Africa Canada, the Polé Institute, ITRI and many others. -

African Dialects

African Dialects • Adangme (Ghana ) • Afrikaans (Southern Africa ) • Akan: Asante (Ashanti) dialect (Ghana ) • Akan: Fante dialect (Ghana ) • Akan: Twi (Akwapem) dialect (Ghana ) • Amharic (Amarigna; Amarinya) (Ethiopia ) • Awing (Cameroon ) • Bakuba (Busoong, Kuba, Bushong) (Congo ) • Bambara (Mali; Senegal; Burkina ) • Bamoun (Cameroons ) • Bargu (Bariba) (Benin; Nigeria; Togo ) • Bassa (Gbasa) (Liberia ) • ici-Bemba (Wemba) (Congo; Zambia ) • Berba (Benin ) • Bihari: Mauritian Bhojpuri dialect - Latin Script (Mauritius ) • Bobo (Bwamou) (Burkina ) • Bulu (Boulou) (Cameroons ) • Chirpon-Lete-Anum (Cherepong; Guan) (Ghana ) • Ciokwe (Chokwe) (Angola; Congo ) • Creole, Indian Ocean: Mauritian dialect (Mauritius ) • Creole, Indian Ocean: Seychelles dialect (Kreol) (Seychelles ) • Dagbani (Dagbane; Dagomba) (Ghana; Togo ) • Diola (Jola) (Upper West Africa ) • Diola (Jola): Fogny (Jóola Fóoñi) dialect (The Gambia; Guinea; Senegal ) • Duala (Douala) (Cameroons ) • Dyula (Jula) (Burkina ) • Efik (Nigeria ) • Ekoi: Ejagham dialect (Cameroons; Nigeria ) • Ewe (Benin; Ghana; Togo ) • Ewe: Ge (Mina) dialect (Benin; Togo ) • Ewe: Watyi (Ouatchi, Waci) dialect (Benin; Togo ) • Ewondo (Cameroons ) • Fang (Equitorial Guinea ) • Fõ (Fon; Dahoméen) (Benin ) • Frafra (Ghana ) • Ful (Fula; Fulani; Fulfulde; Peul; Toucouleur) (West Africa ) • Ful: Torado dialect (Senegal ) • Gã: Accra dialect (Ghana; Togo ) • Gambai (Ngambai; Ngambaye) (Chad ) • olu-Ganda (Luganda) (Uganda ) • Gbaya (Baya) (Central African Republic; Cameroons; Congo ) • Gben (Ben) (Togo -

France À Fric: the CFA Zone in Africa and Neocolonialism

France à fric: the CFA zone in Africa and neocolonialism Ian Taylor Date of deposit 18 04 2019 Document version Author’s accepted manuscript Access rights Copyright © Global South Ltd. This work is made available online in accordance with the publisher’s policies. This is the author created, accepted version manuscript following peer review and may differ slightly from the final published version. Citation for Taylor, I. C. (2019). France à fric: the CFA Zone in Africa and published version neocolonialism. Third World Quarterly, Latest Articles. Link to published https://doi.org/10.1080/01436597.2019.1585183 version Full metadata for this item is available in St Andrews Research Repository at: https://research-repository.st-andrews.ac.uk/ FRANCE À FRIC: THE CFA ZONE IN AFRICA AND NEOCOLONIALISM Over fifty years after 1960’s “Year of Africa,” most of Francophone Africa continues to be embedded in a set of associations that fit very well with Kwame Nkrumah’s description of neocolonialism, where postcolonial states are de jure independent but in reality constrained through their economic systems so that policy is directed from outside. This article scrutinizes the functioning of the CFA, considering the role the currency has in persistent underdevelopment in most of Francophone Africa. In doing so, the article identifies the CFA as the most blatant example of functioning neocolonialism in Africa today and a critical device that promotes dependency in large parts of the continent. Mainstream analyses of the technical aspects of the CFA have generally focused on the exchange rate and other related matters. However, while important, the real importance of the CFA franc should not be seen as purely economic, but also political. -

Central African Republic Giraffe Conservation Status Report February 2020

Country Profile Central African Republic Giraffe Conservation Status Report February 2020 General statistics Size of country: 622,984 km² Size of protected areas / percentage protected area coverage: 13% Species and subspecies In 2016 the International Union for the Conservation of Nature (IUCN) completed the first detailed assessment of the conservation status of giraffe, revealing that their numbers are in peril. This was further emphasised when the majority of the IUCN recognised subspecies where assessed in 2018 – some as Critically Endangered. While this update further confirms the real threat to one of Africa’s most charismatic megafauna, it also highlights a rather confusing aspect of giraffe conservation: how many species/subspecies of giraffe are there? The IUCN currently recognises one species (Giraffa camelopardalis) and nine subspecies of giraffe (Muller et al. 2016) historically based on outdated assessments of their morphological features and geographic ranges. The subspecies are thus divided: Angolan giraffe (G. c. angolensis), Kordofan giraffe (G. c. antiquorum), Masai giraffe (G. c. tippleskirchi), Nubian giraffe (G. c. camelopardalis), reticulated giraffe (G. c. reticulata), Rothschild’s giraffe (G. c. rothschildi), South African giraffe (G. c. giraffa), Thornicroft’s giraffe (G. c. thornicrofti) and West African giraffe (G. c. peralta). However, over the past decade GCF together with their partner Senckenberg Biodiversity and Climate Research Centre (BiK-F) have performed the first-ever comprehensive DNA sampling and analysis (genomic, nuclear and mitochondrial) from all major natural populations of giraffe throughout their range in Africa. As a result, an update to the traditional taxonomy now exists. This study revealed that there are four distinct species of giraffe and likely five subspecies (Fennessy et al. -

History, External Influence and Political Volatility in the Central African Republic (CAR)

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Journal for the Advancement of Developing Economies Economics Department 2014 History, External Influence and oliticalP Volatility in the Central African Republic (CAR) Henry Kam Kah University of Buea, Cameroon Follow this and additional works at: https://digitalcommons.unl.edu/jade Part of the Econometrics Commons, Growth and Development Commons, International Economics Commons, Political Economy Commons, Public Economics Commons, and the Regional Economics Commons Kam Kah, Henry, "History, External Influence and oliticalP Volatility in the Central African Republic (CAR)" (2014). Journal for the Advancement of Developing Economies. 5. https://digitalcommons.unl.edu/jade/5 This Article is brought to you for free and open access by the Economics Department at DigitalCommons@University of Nebraska - Lincoln. It has been accepted for inclusion in Journal for the Advancement of Developing Economies by an authorized administrator of DigitalCommons@University of Nebraska - Lincoln. Journal for the Advancement of Developing Economies 2014 Volume 3 Issue 1 ISSN:2161-8216 History, External Influence and Political Volatility in the Central African Republic (CAR) Henry Kam Kah University of Buea, Cameroon ABSTRACT This paper examines the complex involvement of neighbors and other states in the leadership or political crisis in the CAR through a content analysis. It further discusses the repercussions of this on the unity and leadership of the country. The CAR has, for a long time, been embroiled in a crisis that has impeded the unity of the country. It is a failed state in Africa to say the least, and the involvement of neighboring and other states in the crisis in one way or the other has compounded the multifarious problems of this country. -

Great Green Wall for the Sahara and the Sahel Initiative

Great Green Wall for the Sahara and the Sahel initiative The African wall An African partnership to tackle desertification and land degradation Desertification affects millions of the most vulnerable people in Africa, where two-thirds of the land cover consists of drylands and deserts. Contrary to popular perception, desertification is not the loss of land to the desert or through sand-dune movement. Desertification refers to land degradation in arid, semi-arid and sub-humid areas resulting from factors such as human pressure on fragile eco-systems, deforestation and climate change. Desertification and land degradation have a strong negative impact on the food security and livelihoods of the local communities in Africa’s drylands, home to the world’s poorest populations. In 2007, African Heads of State and Government endorsed the Great Green Wall for the Sahara and the Sahel Initiative with the objective of tackling the detrimental social, economic and environmental impacts of land degradation and desertification in the region. The initiative aims to support the efforts of local communities in the sustainable management and use of forests, rangelands and other natural resources in drylands. It also seeks to contribute to climate change mitigation and adaptation, as well improve the food security and livelihoods of the people in the Sahel and the Sahara. From the initial idea of a line of trees from east to west through the African desert, the vision for a Great Green Wall has evolved into that of a mosaic of interventions addressing the challenges facing the people in the Sahel and Sahara. The overall goal of the Great Green Wall initiative is to strengthen the resilience of the region’s people and natural systems with sound ecosystems’ management, sustainable development of land resources, the protection of rural heritage and the improvement of the living conditions of the local population.