Do CDS Spread Determinants Affect the Probability of Default? a Study on the EU Banks

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Jyske Bank H1 2014 Agenda

Jyske Bank H1 2014 Agenda • Jyske Bank in brief • Jyske Banks Performance 1968-2013 • Merger with BRFkredit • Focus in H1 2014 • H1 2014 in figures • Capital Structure • Liquidity • Credit Quality • Strategic Issues • Macro Economy & Danish Banking 2013-2015 • Danish FSA • Fact Book 2 Jyske Bank in brief 3 Jyske Bank in brief Jyske Bank focuses on core business Description Branch Network • Established and listed in 1967 • 2nd largest Danish bank by lending • Total lending of DKK 344bn • 149 domestic branches • Approx. 900,000 customers • Business focus is on Danish private individuals, SMEs and international private and institutional investment clients • International units in Hamburg, Zürich, Gibraltar, Cannes and Weert • A de-centralised organisation • 4,352 employees (end of H1 2013) • Full-scale bank with core operations within retail and commercial banking, mortgage financing, customer driven trading, asset management and private banking • Flexible business model using strategic partnerships within life insurance (PFA), mortgage products (DLR), credit cards (SEB), IT operations (JN Data) and IT R&D (Bankdata) 4 Jyske Bank in brief Jyske Bank has a differentiation strategy “Jyske Differences” • Jyske Bank wants to be Denmark’s most customer-oriented bank by providing high standard personal financial advice and taking a genuine interest in customers • The strategy is to position Jyske Bank as a visible and distinct alternative to more traditional providers of financial services, with regard to distribution channels, products, branches, layout and communication forms • Equal treatment and long term relationships with stakeholders • Core values driven by common sense • Strategic initiatives: Valuebased management Differentiation Risk management Efficiency improvement Acquisitions 5 1990 1996 2002 2006 (Q4) 2011/2012 Jyske Bank performance 1968-2013 6 ROE on opening equity – 1968-2013 Pre-tax profit Average: (ROE on open. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

CAYMAN ISLANDS) LIMITED (Incorporated with Limited Liability in the Cayman Islands) As Issuer and EFG EUROBANK ERGASIAS S.A

– 6:46 pm – mac5 – 3485 Intro : 3485 Intro Prospectus EFG HELLAS PLC (incorporated with limited liability in England and Wales) as Issuer and EFG HELLAS (CAYMAN ISLANDS) LIMITED (incorporated with limited liability in the Cayman Islands) as Issuer and EFG EUROBANK ERGASIAS S.A. (incorporated with limited liability in the Hellenic Republic) as Guarantor €15,000,000,000 Programme for the Issuance of Debt Instruments Under this €15,000,000,000 Programme for the Issuance of Debt Instruments (the “Programme”), each of EFG Hellas PLC and EFG Hellas (Cayman Islands) Limited (each an “Issuer” and, together, the “Issuers”) may from time to time issue debt instruments (“Instruments”) guaranteed by EFG Eurobank Ergasias S.A. (the “Guarantor” or the “Bank”) and denominated in any currency agreed between the relevant Issuer and the relevant Dealer (as defined herein). Application has been made to the Commission de Surveillance du Secteur Financier (the “CSSF”) in its capacity as competent authority under the Luxembourg Act dated 10 July 2005 on prospectuses for securities to approve this document as a base prospectus. Application has also been made to the Luxembourg Stock Exchange for Instruments issued under the Programme to be admitted to trading on the Luxembourg Stock Exchange's regulated market and to be listed on the Official List of the Luxembourg Stock Exchange. References in this Prospectus to Instruments which are intended to be “listed” (and all related references) on the Luxembourg Stock Exchange shall mean that such Instruments have been admitted to trading on the Luxembourg Stock Exchange’s regulated market and have been listed on the Official List of the Luxembourg Stock Exchange. -

The Competition Council Has Authorized the Merger Between ALPHA BANK AE and EFG EFG EUROBANK ERGASIAS SA

The Competition Council has authorized the merger between ALPHA BANK AE and EFG EFG EUROBANK ERGASIAS SA The Competition Council has authorized the economic concentration consisting in merger by absorbtion of EFG Eurobank Ergasias SA by Alpha Bank AE. The analysis of the competition authority found that the notified economic concentration does not raise significant obstacles to effective competition on the Romanian market, respectively does not lead to the creation or strengthening of a dominant position of the merged company to have as effect restriction, prevention or significant distortion of competition on the Romanian market or on a part of it. Since both Alpha Bank AE and EFG Eurobank Ergasias SA hold in Greece more than 2/3 of turnover at European level, there is no obligation this merger to be notified to the European Commission. Community legislation provides that where each of the companies involved achieves more than 2/3 of total turnover in one of member states, the operation is analyzed by the competition authority of respective state as well as by each of the states where the involved parties activate. The merged company shall be called Alpha Eurobank SA. Alpha Bank AE is a company that is part of Alpha group, one of the most important banking and financial services groups in Greece. Alpha Group offers a wide range of services including retail banking, corporate banking, asset management, private sector banking, distribution of insurance products, investment banking, leasing, factoring, management of brokerage services and of estate assets, and brokerage services. In Romania, Alpha group holds control over Alpha Bank Romania S.A., Alpha Leasing Romania IFN S.A., SSIF Alpha Finance Romania S.A., Alpha Insurance Brokers S.R.L., Alpha Astika Akinita Romania S.R.L. -

Beholdningsoversigt 31.03.2021 Jyske Bank.Xlsx

INSTRUMENT_TYPE ISIN ISSUER_NAME Formue Københavns Kommune i kr. 4.069.081.439,62 Equity GB00B0SWJX34 London Stock Exchange Group PLC 1.701.893,31 Equity GB00B24CGK77 Reckitt Benckiser Group PLC 3.564.881,56 Equity AU000000SYD9 Sydney Airport 1.337.059,47 Equity JP3435000009 Sony Corp 6.910.276,86 Equity US0091581068 Air Products and Chemicals Inc 3.520.243,74 Equity US87918A1051 Teladoc Health Inc 1.795.360,11 Equity NL0012169213 QIAGEN NV 1.219.259,56 Equity US12504L1098 CBRE Group Inc 1.615.018,42 Equity FR0013154002 Sartorius Stedim Biotech 1.136.250,30 Equity CH0432492467 Alcon Inc 1.661.975,62 Equity FR0000121667 EssilorLuxottica SA 2.339.599,76 Equity CH0010645932 Givaudan SA 2.497.439,42 Equity CH0013841017 Lonza Group AG 2.547.489,13 Equity FR0010533075 Getlink SE 1.081.032,87 Equity AU0000030678 Coles Group Ltd 1.716.338,55 Equity NO0003054108 Mowi ASA 988.624,03 Equity GB00BHJYC057 InterContinental Hotels Group PLC 1.324.892,92 Equity NL0013267909 Akzo Nobel NV 2.081.864,14 Equity CA12532H1047 CGI Inc 1.974.562,46 Equity SE0012455673 Boliden AB 1.168.396,04 Equity BMG475671050 IHS Markit Ltd 1.720.814,54 Equity CA82509L1076 Shopify Inc 5.815.734,65 Equity CA7677441056 Ritchie Bros Auctioneers Inc 1.079.486,62 Equity JP3198900007 Oriental Land Co Ltd/Japan 2.377.930,50 Equity US6516391066 Newmont Corp 3.214.940,55 Equity IE00BK9ZQ967 Trane Technologies PLC 1.962.517,98 Equity GB00B39J2M42 United Utilities Group PLC 1.586.616,23 Equity US0036541003 ABIOMED Inc 1.469.304,62 Equity US9553061055 West Pharmaceutical Services Inc 1.484.522,98 -

EMTN-2020-Prospectus.Pdf

Prospectus JYSKE BANK A/S (incorporated as a public limited company in Denmark) U.S.$8,000,000,000 Euro Medium Term Note Programme On 22 December 1997, the Issuer (as defined below) entered into a U.S.$1,000,000,000 Euro Medium Term Note Programme (the “Programme”). This document supersedes the Prospectus dated 11 June 2019 and any previous Prospectus and/or Offering Circular. Any Notes (as defined below) issued under the Programme on or after the date of this Prospectus are issued subject to the provisions described herein. This Prospectus does not affect any Notes issued before the date of this Prospectus. Under the Programme, Jyske Bank A/S (the “Issuer”, “Jyske Bank” or the “Bank”) may from time to time issue notes (the ”Notes”), which may be (i) preferred senior notes (“Preferred Senior Notes”), (ii) non-preferred senior notes (“Non-Preferred Senior Notes”), (iii) subordinated and, on issue, constituting Tier 2 Capital (as defined in the Terms and Conditions of the Notes) (“Subordinated Notes”) or (iv) subordinated and, on issue, constituting Additional Tier 1 Capital (as defined in the Terms and Conditions of the Notes) (“Additional Tier 1 Capital Notes”) as indicated in the applicable Final Terms (as defined below). Notes may be denominated in any currency (including euro) agreed between the Issuer and the relevant Dealer (as defined below). The maximum aggregate principal amount of all Notes from time to time outstanding under the Programme will not exceed U.S.$8,000,000,000 (or its equivalent in other currencies calculated as described herein), subject to any increase as described herein. -

School of Economics & Business Administration Master of Science in Management “MERGERS and ACQUISITIONS in the GREEK BANKI

School of Economics & Business Administration Master of Science in Management “MERGERS AND ACQUISITIONS IN THE GREEK BANKING SECTOR.” Panolis Dimitrios 1102100134 Teti Kondyliana Iliana 1102100002 30th September 2010 Acknowledgements We would like to thank our families for their continuous economic and psychological support and our colleagues in EFG Eurobank Ergasias Bank and Marfin Egnatia Bank for their noteworthy contribution to our research. Last but not least, we would like to thank our academic advisor Dr. Lida Kyrgidou, for her significant assistance and contribution. Panolis Dimitrios Teti Kondyliana Iliana ii Abstract M&As is a phenomenon that first appeared in the beginning of the 20th century, increased during the first decade of the 21st century and is expected to expand in the foreseeable future. The current global crisis is one of the most determining factors affecting M&As‟ expansion. The scope of this dissertation is to examine the M&As that occurred in the Greek banking context, focusing primarily on the managerial dimension associated with the phenomenon, taking employees‟ perspective with regard to M&As into consideration. Two of the largest banks in Greece, EFG EUROBANK ERGASIAS and MARFIN EGNATIA BANK, which have both experienced M&As, serve as the platform for the current study. Our results generate important theoretical and managerial implications and contribute to the applicability of the phenomenon, while providing insight with regard to M&As‟ future within the next years. Keywords: Mergers &Acquisitions, Greek banking sector iii Contents 1. Introduction ................................................................................................................ 1 2. Literature Review .......................................................................................................... 4 2.1 Streams of Research in M&As ................................................................................ 4 2.1.1 The Effect of M&As on banks‟ performance .................................................. -

Jyske Bank Q4 2020

Jyske Bank Q4 2020 23 February 2021 2020 in brief Clients experienced Negative rates – for better or worse All Progress Counts A changing organisation • More online meetings. • More clients began to invest • Own wind turbine to offset CO2 • An organisational change in the instead of having cash deposits. emission from direct and development organisation with • More specialists. indirect power consumption a view to becoming even more • To an increasing degree, the covered by means of own agile. • Fewer branches to visit. negative interest rate renewable energy production. environment was reflected in • Organisational changes in • A brand new mobile banking deposit rates for personal • First estimate of CO e emission Personal Clients to become platform. 2 clients. from business volumes. more focused and specialized. • Increased flexibility with Jyske • Targets for sustainability in all Frihed. • Advantageous interest rates • Many employees experienced and remortgaging opportunities material business areas. changed working conditions due for home owners remained. to COVID-19. • Energy loans and CO2 calculator facilitating energy retrofitting. • The sale of Jyske Bank Gibraltar • A new equity fund offering more was finalized. sustainable investment solutions. • New VISA card without Dankort. COVID-19 • Lockdown and restrictions affected Danish society in 2020. • Clients received individual advice and guidance about the COVID-19 situation. • Jyske Bank's employees were most flexible and adaptive, and the bank remained accessible. • A COVID-19 -

Remuneration for Bank Executives

Remuneration for bank execu- tives A study on the impacts of corporate governance codes on executive re- muneration in Sweden, Denmark and the United Kingdom between 2004 and 2010 Degree Project within Business Administration Author: Andreas Klang and Niclas Kristoferson Tutor: Assoc. Prof. Dr. Dr. Petra Inwinkl Jönköping May 2011 Acknowledgements The process of this degree project, would not have been what it is without a number of people whom have contributed and played a part in shaping it to what it is today We would like to thank our tutor Assoc. Prof. Dr. Dr. Petra Inwinkl for herr advice and guidance throughout the process of the whole thesis. This thesis would not have been the same without her influential ideas and constructive criticism. We would also like to thank our seminare partners for their constructive feedback dur- ing all seminars. At last we would like to thank our families and girlfriends whom have endure us during the past six months with constant support and love. Andreas Klang Niclas Kristoferson Division of work The authors of the Remuneration for bank executives, a study on the impacts of corporate go- vernance codes on executive remuneration in Sweden, Denmark and the United Kingdom be- tween 2004 and 2010 are Andreas Klang and Niclas Kristoferson. Andreas Klang have done fif- ty per cent and Niclas Kristoferson have done fifty per cent. Degree Project within Business Administration Title: Remuneration for Bank Executive- A study on the impacts of corporate governance on executive remuneration Author: Andreas Klang and Niclas Kristoferson Tutor: Assoc. Prof. Dr. Dr. -

EUROBANK ERGASIAS S.A. €5 Billion Global Covered Bond

BASE PROSPECTUS EUROBANK ERGASIAS S.A. (incorporated with limited liability in the Hellenic Republic with registration number 000223001000) €5 billion Global Covered Bond Programme Under this €5 billion global covered bond programme (the Programme), Eurobank Ergasias S.A. (the Issuer) (formerly known as EFG Eurobank Ergasias S.A., which changed its name to Eurobank Ergasias S.A. on 2 August 2012) may from time to time issue bonds (the Covered Bonds) denominated in any currency agreed between the Issuer and the relevant Dealer(s) (as defined below). Application has been made to the Commission de Surveillance du Secteur Financier (the CSSF) in its capacity as competent authority under the Luxembourg Act dated 10 July 2005 on prospectuses for securities (as amended) (the Prospectus Act 2005) to approve this document as a base prospectus (the Base Prospectus). By approving this base prospectus, the CSSF does not give any undertaking as to the economic and financial soundness of the operation or the quality or solvency of the Issuer in accordance with Article 7(7) of the Prospectus Act 2005. Application has also been made to the Luxembourg Stock Exchange for Covered Bonds issued under the Programme to be admitted to trading on the Luxembourg Stock Exchange’s regulated market and to be listed on the official list of the Luxembourg Stock Exchange (the Official List). This document comprises a base prospectus for the purposes of Article 5.4 of Directive 2003/71/EC as amended (which includes amendments made by Directive 2010/73/EU to the extent that such amendments have been implemented in a relevant Member State of the European Economic Area) (the Prospectus Directive) but is not a base prospectus for the purposes of Section 12(a)(2) or any other provision of or rule under the United States Securities Act of 1933 (as amended) (the Securities Act). -

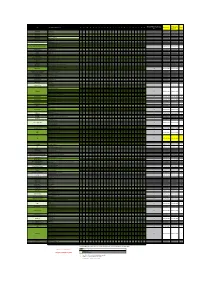

Updated As of 01/06/2017 Changes Highlighted in Yellow

NEW QUARTER TOTAL PDship per Previous Quarter Firm Legal Entity Holding Dealership AT BE BG CZ DE DK ES FI FR GR HU IE IT LV LT NL PL PT RO SE SI SK UK Current Quarter Changes Bank March 2016) ABLV Bank ABLV Bank, AS 1 bank customer bank customer 0 Abanka Vipa Abanka Vipa d.d. 1 bank customer bank customer 0 ABN Amro ABN Amro Bank N.V. 3 bank inter dealer bank inter dealer 0 Alpha Bank Alpha Bank S.A. 1 bank customer bank customer 0 Allianz Group Allianz Bank Bulgaria AD 1 bank customer bank customer 0 Banca IMI Banca IMI S.p.A. 3 bank inter dealer bank inter dealer 0 Banca Transilvania Banca Transilvania 1 bank customer bank customer 0 Banco BPI Banco BPI + 1 bank customer bank customer 0 Banco Comercial Português Millenniumbcp + 1 bank customer bank customer 0 Banco Cooperativo Español Banco Cooperativo Español S.A. + 1 bank customer bank customer 0 Banco Santander S.A. + Banco Santander / Santander Group Santander Global Banking & Markets UK 6 bank inter dealer bank inter dealer 0 Bank Zachodni WBK S.A. Bank Millennium Bank Millennium S.A. 1 bank customer bank customer 0 Bankhaus Lampe Bankhaus Lampe KG 1 bank customer bank customer 0 Bankia Bankia S.A.U. 1 bank customer bank customer 0 Bankinter Bankinter S.A. 1 bank customer bank customer 0 Bank of America Merrill Lynch Merrill Lynch International 9 bank inter dealer bank inter dealer 0 Barclays Barclays Bank PLC + 17 bank inter dealer bank inter dealer 0 Bayerische Landesbank Bayerische Landesbank 1 bank customer bank customer 0 BAWAG P.S.K. -

Eurobank EFG Cyprus Ltd Report and Financial Statements for the Year

Eurobank EFG Cyprus Ltd Report and financial statements for the year ended 31 December 2009 Contents Page Board of Directors and other officers 1 Report of the Board of Directors 2 – 4 Independent Auditor’s Report 5 – 6 Income statement 7 Statement of comprehensive income 8 Balance sheet 9 Statement of changes in equity 10 Statement of cash flows 11 Summary of significant accounting policies and 12 – 70 notes to the financial statements Additional information to the financial statements 71 Eurobank EFG Cyprus Ltd Board of Directors and other officers Board of Directors N. Karamouzis Chairman M. Zampelas Vice Chairman, Non Executive M. Louis Executive D. Shacallis Executive M. Colakides Non Executive P. Hadjisotiriou Non Executive K. Morianos Non Executive K. Vasiliou Non Executive D. Hadjiargyrou Non Executive V. Nicolaides Non Executive C. Papaellinas Non Executive C. Zachariou Non Executive Executive Committee Michalis Louis Demetris Shacallis Charalambos Hambakis Achilleas Malliotis Andreas Petsas Antonis Antoniou Stefanos Kassianides Company Secretary D. Shacallis Registered office 41 Arch. Makariou Avenue 5th floor CY-1065 Nicosia Cyprus EFGH CYP 2009 FS. (1) Eurobank EFG Cyprus Ltd Report of the Board of Directors The Board of Directors presents its report together with the audited financial statements of Eurobank EFG Cyprus Ltd (the “Bank”) for the year ended 31 December 2009. Principal activity Eurobank EFG Cyprus Ltd was incorporated on 21 December 2007 and remained dormant until the date of transfer of assets and activities of EFG Eurobank Ergasias S.A. – Cyprus Branch which took place on 26 March 2008. The transfer of assets and activities was effected following the permit granted by the Central Bank of Cyprus dated 11 March 2008 to carry out banking services through the operation of a Cyprus subsidiary company and in accordance with the Transfer of Banking Business and Securities Law 64 (I)/1997, as amended (the “Transfer Law’) N 118(I)/2002 (as amended) articles 26-30.