Systemic Stress Test Model for Shared Portfolio Networks Irena Vodenska1,2*, Nima Dehmamy3, Alexander P

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CAYMAN ISLANDS) LIMITED (Incorporated with Limited Liability in the Cayman Islands) As Issuer and EFG EUROBANK ERGASIAS S.A

– 6:46 pm – mac5 – 3485 Intro : 3485 Intro Prospectus EFG HELLAS PLC (incorporated with limited liability in England and Wales) as Issuer and EFG HELLAS (CAYMAN ISLANDS) LIMITED (incorporated with limited liability in the Cayman Islands) as Issuer and EFG EUROBANK ERGASIAS S.A. (incorporated with limited liability in the Hellenic Republic) as Guarantor €15,000,000,000 Programme for the Issuance of Debt Instruments Under this €15,000,000,000 Programme for the Issuance of Debt Instruments (the “Programme”), each of EFG Hellas PLC and EFG Hellas (Cayman Islands) Limited (each an “Issuer” and, together, the “Issuers”) may from time to time issue debt instruments (“Instruments”) guaranteed by EFG Eurobank Ergasias S.A. (the “Guarantor” or the “Bank”) and denominated in any currency agreed between the relevant Issuer and the relevant Dealer (as defined herein). Application has been made to the Commission de Surveillance du Secteur Financier (the “CSSF”) in its capacity as competent authority under the Luxembourg Act dated 10 July 2005 on prospectuses for securities to approve this document as a base prospectus. Application has also been made to the Luxembourg Stock Exchange for Instruments issued under the Programme to be admitted to trading on the Luxembourg Stock Exchange's regulated market and to be listed on the Official List of the Luxembourg Stock Exchange. References in this Prospectus to Instruments which are intended to be “listed” (and all related references) on the Luxembourg Stock Exchange shall mean that such Instruments have been admitted to trading on the Luxembourg Stock Exchange’s regulated market and have been listed on the Official List of the Luxembourg Stock Exchange. -

The Competition Council Has Authorized the Merger Between ALPHA BANK AE and EFG EFG EUROBANK ERGASIAS SA

The Competition Council has authorized the merger between ALPHA BANK AE and EFG EFG EUROBANK ERGASIAS SA The Competition Council has authorized the economic concentration consisting in merger by absorbtion of EFG Eurobank Ergasias SA by Alpha Bank AE. The analysis of the competition authority found that the notified economic concentration does not raise significant obstacles to effective competition on the Romanian market, respectively does not lead to the creation or strengthening of a dominant position of the merged company to have as effect restriction, prevention or significant distortion of competition on the Romanian market or on a part of it. Since both Alpha Bank AE and EFG Eurobank Ergasias SA hold in Greece more than 2/3 of turnover at European level, there is no obligation this merger to be notified to the European Commission. Community legislation provides that where each of the companies involved achieves more than 2/3 of total turnover in one of member states, the operation is analyzed by the competition authority of respective state as well as by each of the states where the involved parties activate. The merged company shall be called Alpha Eurobank SA. Alpha Bank AE is a company that is part of Alpha group, one of the most important banking and financial services groups in Greece. Alpha Group offers a wide range of services including retail banking, corporate banking, asset management, private sector banking, distribution of insurance products, investment banking, leasing, factoring, management of brokerage services and of estate assets, and brokerage services. In Romania, Alpha group holds control over Alpha Bank Romania S.A., Alpha Leasing Romania IFN S.A., SSIF Alpha Finance Romania S.A., Alpha Insurance Brokers S.R.L., Alpha Astika Akinita Romania S.R.L. -

School of Economics & Business Administration Master of Science in Management “MERGERS and ACQUISITIONS in the GREEK BANKI

School of Economics & Business Administration Master of Science in Management “MERGERS AND ACQUISITIONS IN THE GREEK BANKING SECTOR.” Panolis Dimitrios 1102100134 Teti Kondyliana Iliana 1102100002 30th September 2010 Acknowledgements We would like to thank our families for their continuous economic and psychological support and our colleagues in EFG Eurobank Ergasias Bank and Marfin Egnatia Bank for their noteworthy contribution to our research. Last but not least, we would like to thank our academic advisor Dr. Lida Kyrgidou, for her significant assistance and contribution. Panolis Dimitrios Teti Kondyliana Iliana ii Abstract M&As is a phenomenon that first appeared in the beginning of the 20th century, increased during the first decade of the 21st century and is expected to expand in the foreseeable future. The current global crisis is one of the most determining factors affecting M&As‟ expansion. The scope of this dissertation is to examine the M&As that occurred in the Greek banking context, focusing primarily on the managerial dimension associated with the phenomenon, taking employees‟ perspective with regard to M&As into consideration. Two of the largest banks in Greece, EFG EUROBANK ERGASIAS and MARFIN EGNATIA BANK, which have both experienced M&As, serve as the platform for the current study. Our results generate important theoretical and managerial implications and contribute to the applicability of the phenomenon, while providing insight with regard to M&As‟ future within the next years. Keywords: Mergers &Acquisitions, Greek banking sector iii Contents 1. Introduction ................................................................................................................ 1 2. Literature Review .......................................................................................................... 4 2.1 Streams of Research in M&As ................................................................................ 4 2.1.1 The Effect of M&As on banks‟ performance .................................................. -

EUROBANK ERGASIAS S.A. €5 Billion Global Covered Bond

BASE PROSPECTUS EUROBANK ERGASIAS S.A. (incorporated with limited liability in the Hellenic Republic with registration number 000223001000) €5 billion Global Covered Bond Programme Under this €5 billion global covered bond programme (the Programme), Eurobank Ergasias S.A. (the Issuer) (formerly known as EFG Eurobank Ergasias S.A., which changed its name to Eurobank Ergasias S.A. on 2 August 2012) may from time to time issue bonds (the Covered Bonds) denominated in any currency agreed between the Issuer and the relevant Dealer(s) (as defined below). Application has been made to the Commission de Surveillance du Secteur Financier (the CSSF) in its capacity as competent authority under the Luxembourg Act dated 10 July 2005 on prospectuses for securities (as amended) (the Prospectus Act 2005) to approve this document as a base prospectus (the Base Prospectus). By approving this base prospectus, the CSSF does not give any undertaking as to the economic and financial soundness of the operation or the quality or solvency of the Issuer in accordance with Article 7(7) of the Prospectus Act 2005. Application has also been made to the Luxembourg Stock Exchange for Covered Bonds issued under the Programme to be admitted to trading on the Luxembourg Stock Exchange’s regulated market and to be listed on the official list of the Luxembourg Stock Exchange (the Official List). This document comprises a base prospectus for the purposes of Article 5.4 of Directive 2003/71/EC as amended (which includes amendments made by Directive 2010/73/EU to the extent that such amendments have been implemented in a relevant Member State of the European Economic Area) (the Prospectus Directive) but is not a base prospectus for the purposes of Section 12(a)(2) or any other provision of or rule under the United States Securities Act of 1933 (as amended) (the Securities Act). -

Updated As of 01/06/2017 Changes Highlighted in Yellow

NEW QUARTER TOTAL PDship per Previous Quarter Firm Legal Entity Holding Dealership AT BE BG CZ DE DK ES FI FR GR HU IE IT LV LT NL PL PT RO SE SI SK UK Current Quarter Changes Bank March 2016) ABLV Bank ABLV Bank, AS 1 bank customer bank customer 0 Abanka Vipa Abanka Vipa d.d. 1 bank customer bank customer 0 ABN Amro ABN Amro Bank N.V. 3 bank inter dealer bank inter dealer 0 Alpha Bank Alpha Bank S.A. 1 bank customer bank customer 0 Allianz Group Allianz Bank Bulgaria AD 1 bank customer bank customer 0 Banca IMI Banca IMI S.p.A. 3 bank inter dealer bank inter dealer 0 Banca Transilvania Banca Transilvania 1 bank customer bank customer 0 Banco BPI Banco BPI + 1 bank customer bank customer 0 Banco Comercial Português Millenniumbcp + 1 bank customer bank customer 0 Banco Cooperativo Español Banco Cooperativo Español S.A. + 1 bank customer bank customer 0 Banco Santander S.A. + Banco Santander / Santander Group Santander Global Banking & Markets UK 6 bank inter dealer bank inter dealer 0 Bank Zachodni WBK S.A. Bank Millennium Bank Millennium S.A. 1 bank customer bank customer 0 Bankhaus Lampe Bankhaus Lampe KG 1 bank customer bank customer 0 Bankia Bankia S.A.U. 1 bank customer bank customer 0 Bankinter Bankinter S.A. 1 bank customer bank customer 0 Bank of America Merrill Lynch Merrill Lynch International 9 bank inter dealer bank inter dealer 0 Barclays Barclays Bank PLC + 17 bank inter dealer bank inter dealer 0 Bayerische Landesbank Bayerische Landesbank 1 bank customer bank customer 0 BAWAG P.S.K. -

Eurobank EFG Cyprus Ltd Report and Financial Statements for the Year

Eurobank EFG Cyprus Ltd Report and financial statements for the year ended 31 December 2009 Contents Page Board of Directors and other officers 1 Report of the Board of Directors 2 – 4 Independent Auditor’s Report 5 – 6 Income statement 7 Statement of comprehensive income 8 Balance sheet 9 Statement of changes in equity 10 Statement of cash flows 11 Summary of significant accounting policies and 12 – 70 notes to the financial statements Additional information to the financial statements 71 Eurobank EFG Cyprus Ltd Board of Directors and other officers Board of Directors N. Karamouzis Chairman M. Zampelas Vice Chairman, Non Executive M. Louis Executive D. Shacallis Executive M. Colakides Non Executive P. Hadjisotiriou Non Executive K. Morianos Non Executive K. Vasiliou Non Executive D. Hadjiargyrou Non Executive V. Nicolaides Non Executive C. Papaellinas Non Executive C. Zachariou Non Executive Executive Committee Michalis Louis Demetris Shacallis Charalambos Hambakis Achilleas Malliotis Andreas Petsas Antonis Antoniou Stefanos Kassianides Company Secretary D. Shacallis Registered office 41 Arch. Makariou Avenue 5th floor CY-1065 Nicosia Cyprus EFGH CYP 2009 FS. (1) Eurobank EFG Cyprus Ltd Report of the Board of Directors The Board of Directors presents its report together with the audited financial statements of Eurobank EFG Cyprus Ltd (the “Bank”) for the year ended 31 December 2009. Principal activity Eurobank EFG Cyprus Ltd was incorporated on 21 December 2007 and remained dormant until the date of transfer of assets and activities of EFG Eurobank Ergasias S.A. – Cyprus Branch which took place on 26 March 2008. The transfer of assets and activities was effected following the permit granted by the Central Bank of Cyprus dated 11 March 2008 to carry out banking services through the operation of a Cyprus subsidiary company and in accordance with the Transfer of Banking Business and Securities Law 64 (I)/1997, as amended (the “Transfer Law’) N 118(I)/2002 (as amended) articles 26-30. -

To the Challenges of a New Era

Open to the challenges of a new era ANNUAL REPORT2006 WorldReginfo - 9eefdb0a-d062-4b3b-b28d-bb9fee2e478a LONDON • One branch LUXEMBOURG • Presence through subsidiaries BULGARIA • 281 Branches • 287 Total points of presence • Loans of €1.5 bn. ROMANIA • 189 Branches • 201 Total points of presence • Loans of €1.7 bn. SERBIA • 103 Branches • 108 Total points of presence • Loans of €0.4 bn. WorldReginfo - 9eefdb0a-d062-4b3b-b28d-bb9fee2e478a POLAND POLAND • 70 Branches • 130 Total points of presence UKRAINE • Loans of €0.2 bn. ROMANIA UKRAINE • Universal Bank UKRAINE • 33 Branches SERBIA BULGARIA TURKEY GREECE TURKEY 31 Branches GREECE • 367 Branches • 520 Total points of presence • Loans of €31.1 bn. WorldReginfo - 9eefdb0a-d062-4b3b-b28d-bb9fee2e478a WorldReginfo - 9eefdb0a-d062-4b3b-b28d-bb9fee2e478a CONTENTS THE YEAR IN REVIEW 4 Members of the Strategic Planning Committee and the Executive Committee Financial Highlights Review Letter to Shareholders Financial Review The Eurobank EFG Share RETAIL BANKING 21 Retail Banking Service Networks Consumer Lending Mortgage Lending Small Business Banking CORPORATE BANKING 27 Lending to Large Corporates Lending to Medium-Sized Enterprises Shipping Leasing Factoring INVESTMENT BANKING & CAPITAL MARKETS 33 Investment Banking Equity Brokerage Treasury WEALTH MANAGEMENT 36 Mutual Funds Insurance Asset Management Private Banking INTERNATIONAL PRESENCE 40 Bulgaria Romania Serbia Poland Turkey Ukraine OTHER ACTIVITIES OF THE GROUP 46 Securities Services Payment Services Payroll Services Real Estate E-Commerce e-Banking and Internet Services RISK MANAGEMENT 48 CORPORATE GOVERNANCE 52 APPENDICES 55 Consolidated Financial Statements 2006 Eurobank EFG Group and EFG Group ANNUAL REPORT 2006 3 WorldReginfo - 9eefdb0a-d062-4b3b-b28d-bb9fee2e478a Members of the Strategic Planning Committee and the Executive Committee Xenophon C. -

Efg Eurobank Ergasias S.A

GR030 OK 0 0 0 1. CAPITAL Period 0 0 0 0 GR030 EUROBANK ERGASIAS S.A. 31/12/2012 30/6/2013 Capital position CRD3 rules References to COREP reporting Million EUR % RWA Million EUR % RWA A) Common equity before deductions (Original own funds without hybrid instruments and government COREP CA 1.1 without Hybrid instruments and government support measures other 3.499 3.656 support measures other than ordinary shares) (+) than ordinary shares Of which: adjustment to valuation differences in other AFS assets (1) (-/+) 26 18 Prudential filters for regulatory capital (COREP line 1.1.2.6.06) B) Deductions from common equity (Elements deducted from original own funds) (-) -348 -326 COREP CA 1.3.T1* (negative amount) As defined by Article 57 (q) of Directive 2006/48/EC (COREP line 1.3.8 included in Of which: IRB provision shortfall and IRB equity expected loss amounts (before tax) (-) -285 -342 1.3.T1*) C) Common equity (A+B) 3.151 8,3% 3.330 9,6% Of which: ordinary shares subscribed by government 0 0 Paid up ordinary shares subscribed by government D) CoCos issued before 30 June 2012 according to EBA Common Term Sheet (+) 0 0 EBA/REC/2011/1 E) Other Existing government support measures (+) 950 950 F) Core Tier 1 including other intruments eligible and existing government support measures (C+D+E) 4.101 10,8% 4.280 12,4% Net amount included in T1 own funds (COREP line 1.1.4.1a + COREP lines from G) Hybrid instruments not subscribed by government 367 77 1.1.2.2***01 to 1.1.2.2***05 + COREP line 1.1.5.2a (negative amount)) not subscribed by government -

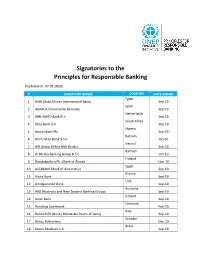

Signatories to the Principles for Responsible Banking

Signatories to the Principles for Responsible Banking Last updated: 03.12.2020 REMOVAL FROM THE FIRST FIRST END OF 4 YEAR WITHDRAWAL DATE REPORTING SIGNATORIES # SIGNATORY BANKS COUNTRY REPORTING CONTACT DETAILS REPORTING IMPLEMENTATION FROM SIGNED LINK LIST BY THE DUE PUBLISHED PERIOD INITIATIVE BANKING BOARD AAIB (Arab African 1 Egypt Sep-19 Mar-21 Sep-23 International Bank) ABANCA 2 Corporación Spain Sep-19 Mar-21 Sep-23 Bancaria ABN AMRO Bank 3 Netherlands Sep-19 Mar-21 Jun-20 Report Sep-23 N.V. 4 Absa Bank Ltd. South Africa Sep-19 Mar-21 Sep-23 5 Access Bank Plc Nigeria Sep-19 Mar-21 Sep-23 Ahli United Bank 6 Bahrain Jan-20 Jul-21 Jan-24 B.S.C AIB Group (Allied 7 Ireland Sep-19 Mar-21 Sep-23 Irish Banks) Al Baraka Banking 8 Bahrain Oct-19 Apr-21 Oct-23 Group B.S.C. Ålandsbanken Plc. 9 Finland Nov-19 May-21 Nov-23 (Bank of Åland) ALEXBANK (Bank of 10 Egypt Sep-19 Mar-21 Sep-23 Alexandria) 11 Alpha Bank Greece Sep-19 Mar-21 Sep-23 12 Amalgamated Bank USA Sep-19 Mar-21 Sep-23 ANZ (Australia and 13 New Zealand Australia Sep-19 Mar-21 Nov-20 Report Sep-23 Banking Group) 14 Arion Bank Iceland Sep-19 Mar-21 Sep-23 15 Aurskorg Sparebank Denmark Feb-20 Aug-21 Feb-24 Banca MPS (Banca 16 Monte dei Paschi di Italy Sep-19 Mar-21 Oct-20 Report Sep-23 Siena) 17 Banco Bolivariano Ecuador Dec-19 Jun-21 Dec-23 Banco Bradesco 18 Brazil Sep-19 Mar-21 Sep-23 S.A. -

Greek Debt Standoff Weighs on Credit Profiles of Banks by Dexter Tan

NUS Risk Management Institute rmicri.org Greek debt standoff weighs on credit profiles of banks by Dexter Tan The financial situation of Greece’s four largest banks has worsened as continued deposit outflows have apparently accelerated to record levels in January. Withdrawals between Jan 19 and Jan 23 this year were larger than in May 2012, when Greece was on the verge of exiting the EU. Depositor sentiment has been affected by negative political developments and the country’s inability to repay its debt obligations on time. The banks depend on cheap ECB funding to fund day to day operations but the ECB could stop funding Greek lenders if the newly elected government rejects the bailout program obligations with its international creditors. These factors constitute a major liquidity risk for the four largest Greek lenders, which account for more than 90% of the domestic banking sector assets. The RMI 1-year probabilities of default (RMI 1-year PD) for the National Bank of Greece, Piraeus Bank, Eurobank Ergasias and Alpha Bank have increased markedly over the recent weeks (see Figure 1). An election victory by the leftwing, anti-austerity Syriza party triggered a sharp sell-off in Greek bank shares; National Bank of Greece (NBG) and Piraeus Bank witnessed a 37% and 43% decline in market cap respectively in January (see Table 1) as actions and comments by the newly appointed Ministers reignited fears of another Greek debt crisis. This has led to a decline in the companies’ RMI distance-to-default (RMI DTD) measure and, consequently, an increase in the RMI 1-year PD. -

Signatories to the Principles for Responsible Banking

Signatories to the Principles for Responsible Banking (Updated on: 07.09.2020) # SIGNATORY BANKS COUNTRY DATE SIGNED Egypt 1 AAIB (Arab African International Bank) Sep-19 Spain 2 ABANCA Corporación Bancaria Sep-19 Netherlands 3 ABN AMRO Bank N.V. Sep-19 South Africa 4 Absa Bank Ltd. Sep-19 Nigeria 5 Access Bank Plc Sep-19 Bahrain 6 Ahli United Bank B.S.C Jan-20 Ireland 7 AIB Group (Allied Irish Banks) Sep-19 Bahrain 8 Al Baraka Banking Group B.S.C. Oct-19 Finland 9 Ålandsbanken Plc. (Bank of Åland) Nov-19 Egypt 10 ALEXBANK (Bank of Alexandria) Sep-19 Greece 11 Alpha Bank Sep-19 USA 12 Amalgamated Bank Sep-19 Australia 13 ANZ (Australia and New Zealand Banking Group) Sep-19 Iceland 14 Arion Bank Sep-19 Denmark 15 Aurskorg Sparebank Feb-20 Italy 16 Banca MPS (Banca Monte dei Paschi di Siena) Sep-19 Ecuador 17 Banco Bolivariano Dec-19 Brazil 18 Banco Bradesco S.A. Sep-19 Brazil 19 Banco da Amazônia Jan-20 Argentina 20 Banco de Galicia y Buenos Aires SA Sep-19 Ecuador 21 Banco de la Produccion S.A Produbanco Sep-19 Ecuador 22 Banco de Machala S.A. Sep-19 Mexico 23 Banco del Bajio, S.A. Aug-20 Ecuador 24 Banco Diners Club del Ecuador S.A. Nov-19 Nicaragua 25 Banco Grupo Promerica Nicaragua Sep-19 Ecuador 26 Banco Guayaquil Sep-19 El Salvador 27 Banco Hipotecario de El Salvador S.A. Sep-19 Ecuador 28 Banco Pichincha Sep-19 Dominican Republic 29 Banco Popular Dominicano Sep-19 Costa Rica 30 Banco Promerica Costa Rica Sep-19 Paraguay 31 Banco Regional Jul-20 Spain 32 Banco Sabadell Sep-19 Ecuador 33 Banco Solidario Nov-19 Colombia 34 Bancolombia -

Dexia – Rise & Fall of a Banking Giant ______

DEXIA – RISE & FALL OF A BANKING GIANT __________________________________________________ LES ETUDES DU CLUB N° 100 DECEMBRE 2013 DEXIA – RISE & FALL OF A BANKING GIANT __________________________________________________ LES ETUDES DU CLUB N° 100 DECEMBRE 2013 Etude réalisée par Monsieur Nicholas Whitbeck (HEC 2013) sous la direction de Monsieur Ulrich Hege Professeur à HEC Paris Introduction .................................................................................................................................................... 3 I. How Dexia conquered the world ............................................................................................................ 4 A. Marriage of convenience ............................................................................................................................................... 4 B. Consolidation .................................................................................................................................................................. 6 C. Expansion in all directions ........................................................................................................................................... 8 D. Kempen & Labouchère – Dexia’s first warnings ................................................................................................... 10 E. Short-term liabilities fuelled the expansion of Dexia’s balance sheet ................................................................. 11 F. Under the leadership of Axel Miller, Dexia continued