Small-Cap Research [email protected]

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WO 2016/106159 Al 30 June 2016 (30.06.2016) W P O P C T

(12) INTERNATIONAL APPLICATION PUBLISHED UNDER THE PATENT COOPERATION TREATY (PCT) (19) World Intellectual Property Organization International Bureau (10) International Publication Number (43) International Publication Date WO 2016/106159 Al 30 June 2016 (30.06.2016) W P O P C T (51) International Patent Classification: (74) Agents: BALICKY, Eric, M. et al; Hamilton, Brook, C07K 16/28 (2006.01) Smith & Reynolds, P.C., 530 Virginia Rd, P.O. Box 9133, Concord, MA 01742-9133 (US). (21) International Application Number: PCT/US20 15/066954 (81) Designated States (unless otherwise indicated, for every kind of national protection available): AE, AG, AL, AM, (22) Date: International Filing AO, AT, AU, AZ, BA, BB, BG, BH, BN, BR, BW, BY, 19 December 2015 (19. 12.2015) BZ, CA, CH, CL, CN, CO, CR, CU, CZ, DE, DK, DM, (25) Filing Language: English DO, DZ, EC, EE, EG, ES, FI, GB, GD, GE, GH, GM, GT, HN, HR, HU, ID, IL, IN, IR, IS, JP, KE, KG, KN, KP, KR, (26) Publication Language: English KZ, LA, LC, LK, LR, LS, LU, LY, MA, MD, ME, MG, (30) Priority Data: MK, MN, MW, MX, MY, MZ, NA, NG, NI, NO, NZ, OM, 62/095,675 22 December 2014 (22. 12.2014) US PA, PE, PG, PH, PL, PT, QA, RO, RS, RU, RW, SA, SC, 62/220,199 17 September 2015 (17.09.2015) US SD, SE, SG, SK, SL, SM, ST, SV, SY, TH, TJ, TM, TN, 62/25 1,082 4 November 2015 (04. 11.2015) US TR, TT, TZ, UA, UG, US, UZ, VC, VN, ZA, ZM, ZW. -

(12) Patent Application Publication (10) Pub. No.: US 2016/0319019 A1 Amirina Et Al

US 201603.19019A1 (19) United States (12) Patent Application Publication (10) Pub. No.: US 2016/0319019 A1 Amirina et al. (43) Pub. Date: Nov. 3, 2016 (54) ANTI-PD-1 ANTIBODIES (22) Filed: May 11, 2016 (71) Applicant: Enumeral Biomedical Holdings, Inc., Related U.S. Application Data Cambridge, MA (US) (62) Division of application No. 14/975,769, filed on Dec. 19, 2015. (72) Inventors: Najmia Amirina, Cambridge, MA (60) Provisional application No. 62/095.675, filed on Dec. (US); Hareesh Chamarthi, Allston, 22, 2014, provisional application No. 62/220,199, MA (US); Maria Isabel Chiu, Newton filed on Sep. 17, 2015, provisional application No. Centre, MA (US); Daniel Doty, 62/251,082, filed on Nov. 4, 2015, provisional appli Arlington, MA (US); Bin Feng, cation No. 62/261,118, filed on Nov. 30, 2015. Newton, MA (US); Aleksander Jonca, Publication Classification Boston, MA (US); Thomas McQuade, Cambridge, MA (US); Anhco Nguyen, (51) Int. Cl. Needham, MA (US); Sheila C07K 6/28 (2006.01) Ranganath, Arlington, MA (US); Hans (52) U.S. Cl. Albert Felix Scheuplein, Arlington, CPC ..... C07K 16/2803 (2013.01); C07K 231 7/567 MA (US); Vikki A. Spaulding, Acton, (2013.01); C07K 23.17/34 (2013.01); A61 K MA (US); Lei Wang, Braintree, MA 2039/507 (2013.01) (US); Jennifer Watkins-Yoon, Brighton, MA (US) (57) ABSTRACT Antibodies that bind to programmed cell death protein 1 (PD-1), compositions comprising Such antibodies, and (21) Appl. No.:y x- - - 15/152,1929 methods of making and using Such antibodies are disclosed. Patent Application Publication Nov. 3, 2016 Sheet 3 of 27 US 2016/0319019 A1 s's is 5 w c. -

Developing a Novel Concept Regenerative Treatment for DPN: Engensis (VM202) Phase 3 Results and Future Plans

Developing a Novel Concept Regenerative Treatment for DPN: Engensis (VM202) Phase 3 Results and Future Plans Seung Shin Yu Disclosure Disclaimer This presentation has been prepared by Helixmith Co., Ltd. (“Company”) solely for your information and for your use and may not be taken away, distributed, reproduced, or redistributed or passed on, directly or indirectly, to any other person (whether within or outside your organization or firm) or published in whole or in part, for any purpose by recipients directly or indirectly to any other person. By accessing this presentation, you are agreeing to be bound by the trailing restrictions and to maintain absolute confidentiality regarding the information disclosed in these materials. Forward-Looking Statements This presentation may contain statements that constitute forward-looking statements. Forward-looking statements can generally by identified by the use of language such as “may”, “will”, “expect”, “estimate”, “anticipate”, “plan”, “intend”, “believe”, “potential”, “anticipate” and “continue” or the negative thereof or similar variations. These forward-looking statements are based on the current beliefs, expectations and assumptions of the Company’s management about the Company’s business, planned acquisitions, future plans, anticipated events and other future conditions. In addition, the forward- looking statements are subject to a number of factors and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements, including the risks and uncertainties related to the progress, timing, cost, and result of clinical trials; difficulties or delays of regulatory filings and approvals; competition from other pharmaceutical or biotechnology companies; and our ability to obtain additional funding required to conduct our research, development, and commercialization activities, and others, all of which could cause the actual results or performance of the Company to differ materially from those contemplated in such forward-looking statements. -

( 12 ) United States Patent

US010738128B2 (12 ) United States Patent ( 10 ) Patent No.: US 10,738,128 B2 Chappel et al. (45 ) Date of Patent : Aug. 11, 2020 ( 54 ) ANTIBODIES THAT BIND CD39 AND USES 5,571,698 A 11/1996 Ladner et al . THEREOF 5,580,717 A 12/1996 Dower et al . 5,624,821 A 4/1997 Winter et al . 5,648,260 A 7/1997 Winter et al. (71 ) Applicant: Surface Oncology , Inc., Cambridge, 5,658,727 A 8/1997 Barbas et al . MA (US ) 5,698,426 A 12/1997 Huse 5,733,743 A 3/1998 Johnson et al. (72 ) Inventors : Scott Chappel, Milton , MA (US ) ; 5,750,753 A 5/1998 Kimae et al. 5,780,225 A 7/1998 Wigler et al. Andrew Lake , Westwood , MA (US ) ; 5,821,047 A 10/1998 Garrard et al . Michael Warren , North Chelmsford , 5,858,358 A 1/1999 June et al. MA (US ) ; Austin Dulak , Reading , MA 5,883,223 A 3/1999 Gray (US ) ; Erik Devereaux, Hanover , MA 5,969,108 A 10/1999 McCafferty et al. (US ) ; Pamela M. Holland , Belmont, 6,001,329 A 12/1999 Buchsbaum et al. 6,005,079 A 12/1999 Casterman et al . MA (US ) ; Tauqeer Zaidi, Sharon , MA 6,194,551 B1 2/2001 Idusogie et al . (US ) ; Matthew Rausch , Cambridge , 6,300,064 B1 10/2001 Knappik et al . MA (US ) ; Bianka Prinz , Lebanon , NH 6,352,694 B1 3/2002 June et al . ( US ) ; Nels P. Nielson , Lebanon , NH 6,534,055 B1 3/2003 June et al . -

Analytics for Accelerating Biomedical Innovation Kien Wei Siah

Analytics for Accelerating Biomedical Innovation by Kien Wei Siah B.Eng., National University of Singapore (2015) S.M., Massachusetts Institute of Technology (2017) Submitted to the Department of Electrical Engineering and Computer Science in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Electrical Engineering and Computer Science at the MASSACHUSETTS INSTITUTE OF TECHNOLOGY February 2021 ○c Massachusetts Institute of Technology 2021. All rights reserved. Author.............................................................. Department of Electrical Engineering and Computer Science December 17, 2020 Certified by. Andrew W. Lo Charles E. and Susan T. Harris Professor, Sloan School of Management Thesis Supervisor Accepted by . Leslie A. Kolodziejski Professor of Electrical Engineering and Computer Science Chair, Department Committee on Graduate Students 2 Analytics for Accelerating Biomedical Innovation by Kien Wei Siah Submitted to the Department of Electrical Engineering and Computer Science on December 17, 2020, in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Electrical Engineering and Computer Science Abstract Despite the many breakthroughs in biomedical research and the increasing demand for new drugs to treat unmet medical needs, the productivity of research and development in the pharmaceutical industry has been steadily declining for the past two decades and is at its lowest level today. Traditional sources of financing in biopharma are no longer compatible nor aligned with the new realities of biomedical innovation, a process which has become more challenging, complex, expensive, time-consuming, and risky in the past twenty years. This has led to an outflow of capital from the biopharma industry, creating an ever-widening gap in funding between early-stage basic biomedical research and late-stage clinical development, where many promising academic discoveries fail not because of bad science but due to financial reasons. -

Immuno-Oncology

IT SAR* Targeted with a mAb Alternatively spliced extradomain-B of fibronectin Philogen (Fibromun/L19-TNF) •• TNFα *Soft Tissue Sarcoma Clinical stage codes M MEL Toxic to tumor neovasculature and activates the endothelium; highly toxic if used systemically Preclinical/Discovery OTC Over-the-Counter Not targeted with a mAb Boehringer Ingelheim (Beromun; isolated limb perfusion) M SAR • Phase 1 NDA New Drug Application Beromun Limited to use in isolated limb perfusion •• Phase 2 BLA Biologics License Application ••• Phase 3 MAA Marketing Authorization Application (Europe's NDA) Long-acting SC Merck (Sylatron/peginterferon α-2b) M MEL Class has M Marketed D Dormant/discontinued Less frequent injections Ñ february 2017 known G Generic Failed survival IB FKD Therapies Oy (Instiladrin/rAdIFN w/ Syn3) •• UCC RCT Randomized Controlled Trial CP Compounding Pharmacy benefit Interferon-α (IFNα) Genetically modified non-replicating virus to the tumor Adenovirus expressing IFNα2b IST Investigator-Sponsored Trial PD(L)1 immuno-oncology 21 22 M NHL PDUFA PDUFA POC: Unknown • Enhances T-cell and DC response via a poorly-characterized MoA M MEL • Associated with dose-limiting AEs, including influenza-like symptoms (fatigue, fever, headache and muscle SC/IM/IC Merck (Intron-A/interferon α-2b) M CLL ANDA Abbreviated New Drug Application POC: Validated aches), nausea, dizziness, anorexia, depression and leukopenia Merck (SC Intron-A/interferon α-2b + IV Keytruda/pembrolizumab) MEL FAILED OL Off-label POC: Failed IFNα2b Roche (IV Tecentriq/atezolizumab -

(51) International Patent Classification: (84) Designated States (Unless

( (51) International Patent Classification: (84) Designated States (unless otherwise indicated, for every C07K 16/28 (2006.01) A61P 35/00 (2006.01) kind of regional protection available) . ARIPO (BW, GH, GM, KE, LR, LS, MW, MZ, NA, RW, SD, SL, ST, SZ, TZ, (21) International Application Number: UG, ZM, ZW), Eurasian (AM, AZ, BY, KG, KZ, RU, TJ, PCT/US20 19/025623 TM), European (AL, AT, BE, BG, CH, CY, CZ, DE, DK, (22) International Filing Date: EE, ES, FI, FR, GB, GR, HR, HU, IE, IS, IT, LT, LU, LV, 03 April 2019 (03.04.2019) MC, MK, MT, NL, NO, PL, PT, RO, RS, SE, SI, SK, SM, TR), OAPI (BF, BJ, CF, CG, Cl, CM, GA, GN, GQ, GW, (25) Filing Language: English KM, ML, MR, NE, SN, TD, TG). (26) Publication Language: English Declarations under Rule 4.17: (30) Priority Data: — as to applicant's entitlement to apply for and be granted a 62/652,790 04 April 2018 (04.04.2018) US patent (Rule 4.17(H)) (71) Applicant: BRISTOL-MYERS SQUIBB COMPANY — as to the applicant's entitlement to claim the priority of the [US/US]; Route 206 and Province Line Road, Princeton, earlier application (Rule 4.17(iii)) New Jersey 08543 (US). — of inventorship (Rule 4.17(iv)) (72) Inventors: LU, Li-Sheng; 117 Gladys Avenue, Mountain Published: View, California 94043 (US). SELBY, Mark J.; 136 Gale- — with international search report (Art. 21(3)) wood Cirlce, San Francisco, California 9413 1 (US). KO- — before the expiration of the time limit for amending the RMAN, Alan J.; 1207 Oakland Avenue, Piedmont, Cali¬ claims and to be republished in the event of receipt of fornia 9461 1 (US). -

Immuno-Oncology IO

AUGUST 29-SEPTEMBER 2, 2016 Cover MARRIOTT LONG WHARF CAMBRIDGE HEALTHTECH INSTITUTE’S 4TH ANNUAL BOSTON, MA Conference- at-a-Glance IO Immuno-Oncology SUMMIT Collaborating to Develop the Next Generation of Targeted Immunotherapy Keynotes REGISTER BY JULY 29 AND SAVE UP TO $200! Faculty Short Courses Sponsor & Exhibit Opportunities Conference Programs Plenary Keynote Speakers Training Seminar Immunomodulatory Combination Adoptive T Cell Antibodies Immunotherapy Therapy Agenda Oncolytic Virus Personalized Biomarkers Immunotherapy Immunotherapy for Immuno-Oncology Edward Michael Morganna Hotel & Travel Fritsch Rosenzweig Freeman Information Ph.D., Chief Ph.D., Executive D.O., Associate Director, Training Seminar: Preclinical & Clinical Trials Technology Director, Biology- Melanoma & Cutaneous Ts Immunology for Drug Translational for Cancer Officer, Neon Discovery, IMR Early Oncology Program, Discovery Scientists Immuno-Oncology Immunotherapy Therapeutics, Inc Discovery, Merck Re- The Angeles Clinic and Registration search Laboratories Research Institute Information CORPORATE SPONSORS CORPORATE SUPPORT SPONSORS Click Here to Register Online! Immuno-Oncology Summit.com 250 First Avenue Needham, MA 02494 www.healthtech.com Cover IO Immuno-Oncology SUMMIT Conference- at-a-Glance MEET THOUGHT LEADERS IN CANCER IMMUNOTHERAPY AT THE PREMIER ANNUAL IO EVENT As our understanding of tumor immunology combinations through clinical development and Who Will Attend? Keynotes has advanced, immuno-oncology has made into the market. This weeklong, nine-meeting set Scientific leaders, C-level executives, professors, unprecedented progress in improving the will include topics ranging from early discovery site directors and researchers from pharma, outcomes for cancer patients. Still, with the field through clinical development as well as emerging biotech, academia, and government working in Faculty in its infancy, the full curative potential of IO has areas such as oncolytic virus immunotherapy. -

WO 2018/098352 A2 O

(12) INTERNATIONAL APPLICATION PUBLISHED UNDER THE PATENT COOPERATION TREATY (PCT) (19) World Intellectual Property Organization International Bureau (10) International Publication Number (43) International Publication Date WO 2018/098352 A2 31 May 2018 (31.05.2018) W !P O PCT (51) International Patent Classification: (74) Agent: MURPHY, Amanda, K. et al; Finnegan, Hender 59/595 (2006.01) A61K 31/343 {2006.01) son, Farabow, Garrett & Dunner, LLP, 901 New York Av C07K 16/28 (2006.01) A61K 31/427 {2006.01) enue, NW, Washington, DC 20001-4413 (US). C12N 15/113 (2010.01) A61K 31/437 {2006.01) (81) Designated States (unless otherwise indicated, for every A61K 45/06 (2006.01) A61K 31/713 (2006.01) kind of national protection available): AE, AG, AL, AM, A61K 31/277 (2006.01) A61P 35/00 (2006.01) AO, AT, AU, AZ, BA, BB, BG, BH, BN, BR, BW, BY, BZ, A61K 31/337 (2006.01) CA, CH, CL, CN, CO, CR, CU, CZ, DE, DJ, DK, DM, DO, (21) International Application Number: DZ, EC, EE, EG, ES, FI, GB, GD, GE, GH, GM, GT, HN, PCT/US2017/0631 16 HR, HU, ID, IL, IN, IR, IS, JO, JP, KE, KG, KH, KN, KP, KR, KW, KZ, LA, LC, LK, LR, LS, LU, LY, MA, MD, ME, (22) International Filing Date: MG, MK, MN, MW, MX, MY, MZ, NA, NG, NI, NO, NZ, 22 November 201 7 (22. 11.201 7) OM, PA, PE, PG, PH, PL, PT, QA, RO, RS, RU, RW, SA, (25) Filing Language: English SC, SD, SE, SG, SK, SL, SM, ST, SV, SY, TH, TJ, TM, TN, TR, TT, TZ, UA, UG, US, UZ, VC, VN, ZA, ZM, ZW. -

3Rd Annual Sachs Cancer

WELCOME SPEAKERS 3rd Annual Sachs Cancer Bio Partnering & PRESENTING COMPANIES Investment Forum Promoting Public & Private Sector, Collaboration & Investment in Drug Development SUPPORTING ORGANISATIONS SUPPORTING 23rd February 2015 New York Academy of Sciences • USA Conference Guide ORGANISERS www.sachsforum.com 3RD ANNUAL SACHS CANCER BIO PARTNERING & INVESTMENT FORUM BIO PARTNERING 3RD ANNUAL SACHS CANCER 3rd ANNUAL t WELCOME Cancer Bio Partnering & Investment Forum back :: next u Sachs Associates are delighted to welcome you to the: 3rd Annual Sachs Cancer SPEAKERS Bio Partnering & Investment Forum Promoting Public & Private Sector, Collaboration & Investment in Drug Development 23rd February 2015 • New York Academy of Sciences • USA PRESENTING COMPANIES Sachs Associates, building upon it’s many years of expertise in organizing premier partnering and investor meetings in Europe and the United States, is proud to welcome you to the 3rd Annual Sachs Cancer Bio Partnering & Investment Forum being held on 23rd February 2015 at the New York Academy of Sciences. This forum is designed to bring together thought leaders from cancer research institutes, patient advocacy groups, pharma and biotech to facilitate partnering and funding/investment. Sachs Associates would like to thank our sponsors and partners who have helped make this event possible. ORGANISATIONS SUPPORTING General Information • The registration desk is open from 8.00am on 23rd February although you are welcome to join the event at any time. Please collect a copy of the agenda for information on timing and room allocation for each session. • One-to-one meetings Please bring with you a copy of your diary. Should you have any queries about your schedule, the laptop situated by the meeting tables is available for your assistance. -

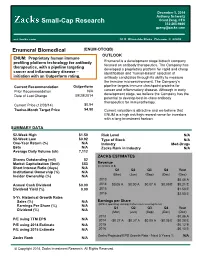

Small-Cap Research 312-265-9466 [email protected]

December 5, 2014 Anthony Schwartz Grant Zeng, CFA Small-Cap Research 312-265-9466 [email protected] scr.zacks.com 10 S. Riverside Plaza, Chicago, IL 60606 Enumeral Biomedical (ENUM-OTCQB) OUTLOOK ENUM: Proprietary human immune profiling platform technology for antibody Enumeral is a development stage biotech company focused on antibody therapeutics. The Company has therapeutics, with a pipeline targeting developed a proprietary platform for rapid and cheap cancer and inflammatory disease identification and human-based selection of initiation with an Outperform rating. antibody candidates through its ability to measure the immune microenvironment. The Company s Current Recommendation Outperform pipeline targets immune checkpoint proteins for Prior Recommendation N/A cancer and inflammatory disease. Although in early development stage, we believe the Company has the Date of Last Change 09/29/2014 potential to develop best-in-class antibody therapeutics for immunotherapy. Current Price (12/03/14) $0.94 Twelve-Month Target Price $4.50 Current valuation is attractive and we believe that ENUM is a high risk/high reward name for investors with a long investment horizon. SUMMARY DATA 52-Week High $1.50 Risk Level N/A 52-Week Low $0.92 Type of Stock N/A One-Year Return (%) N/A Industry Med-Drugs Beta N/A Zacks Rank in Industry N/A Average Daily Volume (sh) 7,112 ZACKS ESTIMATES Shares Outstanding (mil) 52 Market Capitalization ($mil) $53 Revenue (in millions of $) Short Interest Ratio (days) N/A Q1 Q2 Q3 Q4 Year Institutional Ownership (%) N/A Insider Ownership (%) N/A (Mar) (Jun) (Sep) (Dec) (Dec) 2013 $0.45 A Annual Cash Dividend $0.00 2014 $0.05 A $0.00 A $0.07 A $0.09 E $0.21 E Dividend Yield (%) 0.00 2015 $1.50 E 2016 $2.50 E 5-Yr. -

Gene Therapy - Near-Term Revolution Or Continued Evolution? STRATEGIC ADVICE and FINANCING Part 1: Global Proprietary Data (Abbreviated Version) Ravi Mehrotra, Ph.D

Strategic Advisory Analytics Gene Therapy - Near-term Revolution or Continued Evolution? STRATEGIC ADVICE AND FINANCING Part 1: Global Proprietary Data (Abbreviated Version) Ravi Mehrotra, Ph.D. August 2017 [email protected] 212-887-2112 MTS Securities, LLC., an affiliate of MTS Health Partners, L.P., (“MTS”) offers investment banking services to the healthcare industry. Our professionals distinguish themselves by providing experienced, attentive and independent counsel, and expertise in the context of long-term relationships. Our "Strategic Advisory Analytics" reports exemplify our value add strategic advisory services to clients across all healthcare industry sub-sectors. The reports are also distributed to institutional investors, providing a differentiated macro- perspective on key themes and therapeutic areas within Biopharma. Previously published Strategic Advisory Analytics reports can be accessed at http://www.mtspartners.com/investment-banking/news/ To be added to the mailing list for future Strategic Advisory Analytics reports, please email [email protected] Securities related transactions are provided exclusively by our affiliate, MTS Securities, LLC, a broker-dealer registered with the SEC and a member of FINRA and SIPC. Our affiliate, MTS Health Investors, LLC, an SEC registered investment adviser, provides investment advisory services to private equity investors. This publication may not be copied, reproduced or transmitted in whole or in part in any form, or by any means, whether electronic or otherwise, without first receiving written permission from MTS Health Partners, L.P. and/or its affiliated companies (collectively, “MTS”). The information contained herein has been obtained from sources believed to be reliable, but the accuracy and completeness of the information are not guaranteed.