2014 Proxy Statement and Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Register of Lords' Interests

REGISTER OF LORDS’ INTERESTS _________________ The following Members of the House of Lords have registered relevant interests under the code of conduct: ABERDARE, L. Category 1: Directorships Director, WALTZ Programmes Limited (training for work/apprenticeships in London) Category 10: Non-financial interests (a) Director, F.C.M. Limited (recording rights) Category 10: Non-financial interests (c) Trustee, Berlioz Society Trustee, St John Cymru-Wales Trustee, National Library of Wales Category 10: Non-financial interests (e) Trustee, West Wycombe Charitable Trust ADAMS OF CRAIGIELEA, B. Nil No registrable interests ADDINGTON, L. Category 1: Directorships Chairman, Microlink PC (UK) Ltd (computing and software) Category 7: Overseas visits Visit to Azerbaijan, 30 May - 3 June 2013, to meet ministers and other political leaders, NGOs and business figures; cost of visit met by European Azerbaijan Society Category 8: Gifts, benefits and hospitality One ticket for final of men's badminton, Olympic Games, 5 August 2012; two tickets for opening ceremony of Paralympic Games, 29 August 2012, as a part of duties as a parliamentary ambassador for the London Olympic Games 2012 * Category 10: Non-financial interests (d) Vice President, British Dyslexia Association Category 10: Non-financial interests (e) Vice President, UK Sports Association Vice President, Lakenham Hewitt Rugby Club ADEBOWALE, L. Category 1: Directorships Director, Leadership in Mind Ltd (business activities; certain income from services provided personally by the Member is or will -

2005 Catalyst Annual Report

2005 Annual Report Convening Leaders, Inspiring Change “DuPont is proud to support this organization and considers participation critical to our business. Catalyst provides DuPont with information based on hard research and facts, benchmarking information with leading trends, and a membership which is committed to building inclusive environments and expanding opportunities for women. The recognition of the annual Catalyst Award is a coveted place for any business that wishes to be a leader in the global industry. Innovation and excellence are the natural results when people are engaged and feel valued for the skills and talents they bring to the table.” — Chad Holliday, Chairman and CEO, DuPont 2005 Annual Report Expanding opportunities for women and business atalyst is the leading research and advisory organization working with businesses and the professions to build inclusive environments and expand opportunities for women at work. As an Cindependent, nonprofit membership organization, Catalyst conducts research on all aspects of women’s career advancement and provides strategic and web-based consulting services globally. With the support and confidence of member corporations and firms, Catalyst remains connected to business and its changing needs. In addition, Catalyst honors exemplary business initiatives that promote women’s leadership with the annual Catalyst Award. With offices in New York, San Jose, and Toronto, Catalyst is consistently ranked No. 1 among U.S. nonprofits focused on women’s issues by The American Institute of Philanthropy. Letter From the President 1 Letter From the Chair of the Board 2 Research 3 Catalyst in the News 3 Advisory Services 4 Membership 4 Events and Forums 5 2005 Catalyst Awards Dinner and Conference 6 2005 Catalyst Awards Dinner Contributors 7 Change Makers 8 Special Project Funding 9 Catalyst Members 10 Financials and Notes to Consolidated Financial Statements 11 Catalyst Boards 13 Letter From the President or Catalyst, 2005 was an eventful year convening leaders and inspiring change. -

Deutsche Bank AG, London Branch

Securities Note & Summary 18 January 2008 Deutsche Bank AG, London Branch Issue of U.S.$30,000,000 108% Capital Protected Notes due 2021 linked to the KKR Protected Private Equity Index (to be consolidated and form a single series with the existing U.S.$10,000,000 108% Capital Protected Notes due 2021 linked to the KKR Protected Private Equity Index issued on 30 November 2007) Issue Price 100% The issuer (the “Issuer”) of the securities described in the “Prospectus” (consisting of a registration document dated 3 May 2007 (the “Registration Document”) and this Securities Note & Summary) is Deutsche Bank Aktiengesellschaft, acting through its London branch (“Deutsche Bank AG, London Branch”). Application has been made to the Commission de Surveillance du Secteur Financier (the "CSSF") in its capacity as competent authority under the Luxembourg Act relating to prospectuses for securities (Loi relative aux Prospectus pour valeurs mobilières) to approve the Prospectus as a prospectus for the purposes of Directive 2003/71/EC (the "Prospectus Directive"). Application has also been made to the Luxembourg Stock Exchange for the admission to trading on the Bourse de Luxembourg (“Regulated Market”) of the Luxembourg Stock Exchange and the listing on the Official List of the Luxembourg Stock Exchange of the Notes (as defined below) which are to be issued by the Issuer pursuant to its U.S.$40,000,000,000 Global Structured Note Programme (the “Programme”). This is an offering of U.S.$30,000,000 in aggregate principal amount of 108% Capital Protected Notes due 2021 issued on 12 December 2007 (the “Notes”, ) linked to the KKR Protected Private Equity Index (the “Index”), which is an index established and administered by Deutsche Bank AG, London Branch as index sponsor (the “Index Sponsor”) and index administrator (the “Index Administrator”) and managed by Kohlberg Kravis Roberts & Co. -

Consumer and Retail Industry Update June 2011

Consumer and Retail Industry Update June 2011 Member FINRA/SIPC www.harriswilliams.com Consumer and Retail Industry Update June 2011 What We’ve Been Reading • The Wall Street Journal reports U.S. consumer confidence remained relatively flat in May, as both spending expectations and economic confidence saw little change from the prior two months. Discover Financial Services’ (“DFS”) spending monitor rose from 89.4 in April to 89.5 in May, but remains well below the 2011 high of 93.1, reported in January. The Wall Street Journal attributes the downward trend to high gas prices and continued high unemployment, placing added pressure on consumer budgets. Read the article here. • In a recent article, The New York Times (“NYT”) reported only 54,000 jobs were added in the U.S. in May, the smallest gain in eight months, as high oil prices and natural disasters continued to place added stress on the economy. The article states “the gain in May was about a third of what economists had been forecasting. The unemployment rate, meanwhile, edged up to 9.1 percent from 9.0 percent in April.” NYT goes on to say that “while most analysts do not believe that the country will slide back into a recession — which would technically mean that the economy would start shrinking again — they acknowledge that with such low levels of hiring, the recovery is barely perceptible to many Americans.” Read the article here. • The Wall Street Journal reports U.S. households saw their net worth increase in the first quarter of 2011, due to strong equity market performance, increased savings, and debt reductions outpacing falling real-estate prices. -

KKR Annual Report

THE POWER OF PARTNERSHIP 2010 ANNUAL REPORT KKR 2010 ANNUAL REPORT A 01 THE POWER OF PARTNERSHIP 18 LETTER TO UNITHOLDERS 25 FINANCIAL OVERVIEW 30 BUSINESS OVERVIEW 32 ENVIRONMENTAL, SOCIAL AND GOVERNANCE OVERVIEW 34 VALUES 36 KKR LEADERSHIP 37 CONSOLIDATED FINANCIAL REVIEW 100 UNITHOLDER INFORMATION B KKR 2010 ANNUAL REPORT Partnership POWERS MOVES CONNECTS PAYS ENERGIZES FLAVORS GROWS CARES NOURISHES COMFORTS FERMENTS BUILDS SECURES AND GUIDES everything we do. INVESTMENT EXPANDED DEVELOPMENT FROM 1 WELL TO 75 NEW WELLS PARTNERSHIP POWERSEast Resources mansfield, pennsylvania 2 KKR 2010 ANNUAL REPORT KKR 2010 ANNUAL REPORT 3 New technology has transformed the world’s energy supply by enhancing successful and safe exploration for natural gas from shale rock formations. Recognizing this revolutionary change, our energy team identified East Resources, Inc., a leading oil and gas company with a stable portfolio of produc ing assets and more than 650,000 net acres of highly contiguous, operated acreage in some of the most attractive areas of the Marcellus Shale in Pennsylvania. East’s regional concentration and entrepreneurial approach provided operational and cost advantages that made it an attractive invest ment. In June 2009, KKR invested $330 million in East through a convertible security, which enabled the company to expand development — drilling 75 horizontal wells, compared to only one horizontal well prior to KKR’s investment. This expanded development demonstrated the value of East’s asset position. In late 2010, Royal Dutch Shell Plc acquired East for $4.7 billion, a $1.2 billion gain for KKR and our investors. 2 KKR 2010 ANNUAL REPORT KKR 2010 ANNUAL REPORT 3 BMG Rights Management berlin, germany BMG Rights Management (“BMG”) is a joint venture between KKR and Bertelsmann, an international media company active in more than 50 countries, to develop a global music rights management business. -

The Flash Crash: Effects on S&P 500 Index Versus Non-Index Stocks

The Flash Crash: Effects on S&P 500 Index versus non-Index stocks Aaron Carlton The Leonard N. Stern School of Business Glucksman Institute for Research in Securities Markets Faculty Advisor: Jeffrey Wurgler April 1, 2011 I. INTRODUCTION On the afternoon of May 6, 2010, the US stock markets experienced a sudden crash and an almost equally sudden recovery. This “Flash Crash” occurred without any obvious external news, and while some firms experienced a complete drop in market capitalization, other firms experienced equally impressive gains during the same time period. In many ways, this 2010 crash is reminiscent of the crash that began on October 19, 1987 when the market declined 20% also without any obvious villains to blame. This paper focuses on two findings from the October 1987 and investigates whether the same anomalies were present, and to what degree, in the Flash Crash. The two findings in question are whether the S&P 500 was more adversely affected by the crash than the broader market, and if ‘beta’ was the best predictor of stock vulnerability during a sudden crash. Preliminary findings indicate that the S&P 500 was more adversely impacted during the Flash Crash, although to a much smaller degree than the 7% difference seen in 1987. Additionally, the significance of beta appears to be consistent with the findings from 1987. II. BACKGROUND AND HYPOTHESIS II.1 1987 October Crash On October 19, 1987, commonly referred to as Black Monday, the stock market dropped more than 20%, resulting in a loss of close to $1 trillion in market capitalization in the US markets. -

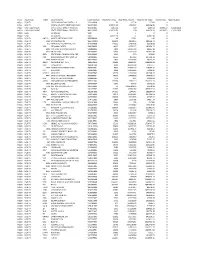

Fund Asset Class Ticker Security Name CUSIP Number Shares/Par

Fund Asset Class Ticker Security Name CUSIP Number Shares/Par Value Base Price Amount Base Market Value Interest Rate Maturity Date NQ11 EQUITY GREEN MOUNTAIN CAPITAL L.P '394990998 50 427.38 21369 0 NQ11 EQUITY NORTH ATLANTIC VENTURE FUND II '651991929 275572.22 1.959947 540106.95 0 NQ11 CASH EQUIVALENT STATE STREET BANK + TRUST CO '8611239B5 4483.64 100 4483.64 0.190652 12/31/2030 NQ20 CASH EQUIVALENT STATE STREET BANK + TRUST CO '8611239B5 196470.54 100 196470.54 0.190652 12/31/2030 NQ20 CASH US DOLLAR 'USD 0 1 0 0 NQ20 CASH US DOLLAR 'USD 12907.48 1 12907.48 0 NQ20 EQUITY NRTLQ NORTEL NETWORKS CORP '656568508 48 0.031 1.49 0 NQ2A EQUITY 5020 JX HOLDINGS INC 'B627LW906 202200 4.938411 998546.73 0 NQ2A EQUITY 510 HIAP SENG ENGINEERING LTD '616207908 132000 0.454838 60038.68 0 NQ2A EQUITY VOR SEQUANA CAPITAL '546924903 14919 12.255127 182834.25 0 NQ2A EQUITY 9842 ARC LAND SAKAMOTO CO LTD '604800904 5800 14.645723 84945.19 0 NQ2A EQUITY 7279 HI LEX CORP '664347002 12500 13.120127 164001.58 0 NQ2A EQUITY SBIDl STATE BANK OF INDIA SPON GDR '513109900 2000 99.9 199800 0 NQ2A EQUITY PKN POLSKI KONCERN NAFTOWY SA '581006905 10236 10.5059 107538.39 0 NQ2A EQUITY 9945 PLENUS CO LTD '669270902 3800 15.335066 58273.25 0 NQ2A EQUITY GIB/A CGI GROUP INC CL A '39945C950 80496 14.906131 1199883.91 0 NQ2A EQUITY CGO COGECO INC '19238T100 1200 28.231309 33877.57 0 NQ2A EQUITY 9936 OHSHO FOOD SERVICE CORP '666093901 4600 25.663917 118054.02 0 NQ2A EQUITY KIN KINEPOLIS '543952907 1419 52.854446 75000.46 0 NQ2A EQUITY SAAB B SAAB AB B '546955907 34176 11.449499 -

View Annual Report

KKR & CO. INC. FORM 10-K (Annual Report) Filed 02/24/14 for the Period Ending 12/31/13 Address 9 WEST 57TH STREET, SUITE 4200 NEW YORK, NY, 10019 Telephone 212-750-8300 CIK 0001404912 Symbol KKR SIC Code 6282 - Investment Advice Industry Investment Management & Fund Operators Sector Financials Fiscal Year 12/31 http://www.edgar-online.com © Copyright 2020, EDGAR Online, a division of Donnelley Financial Solutions. All Rights Reserved. Distribution and use of this document restricted under EDGAR Online, a division of Donnelley Financial Solutions, Terms of Use. Use these links to rapidly review the document TABLE OF CONTENTS ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the fiscal year ended December 31, 2013 Or TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the Transition period from to . Commission File Number 001-34820 KKR & CO. L.P. (Exact name of Registrant as specified in its charter) Delaware 26 -0426107 (State or other Jurisdiction of (I.R.S. Employer Incorporation or Organization) Identification Number) 9 West 57 th Street, Suite 4200 New York, New York 10019 Telephone: (212) 750-8300 (Address, zip code, and telephone number, including area code, of registrant's principal executive office.) Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common units representing limited New York Stock Exchange partner interests Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

2006 Pension Fund 5500

FORM 5500 CENTRAL STATES, SOUTHEAST AND SOUTHWEST AREAS PENSION FUND ANNUAL RETURN/REPORT DECEMBER 31, 2006 SAME 451623 154926 180234 88025 423185 28440 451625 13612 X 1B 1E 1G X X X X 0 2 0 6 0 3 0 2 0 D X X X X 1 X X X X 0 2 0 6 0 3 0 3 0 E CENTRAL STATES, SE AND SW AREAS PENSION PLAN 001 TRUSTEES OF CENTRAL STATES PENSION FUND 36-6044243 JOHN HANCOCK MUTUAL LIFE INSURANCE COMPANY 04-1414660 65099 GAC 461 ASSN 0 14 01/01/2006 12/31/2006 0 0 0 6 0 6 0 3 0 1 0 G 0 6 0 6 0 3 0 2 0 H X 0 6 0 6 0 3 0 3 0 I 0 6 0 6 0 3 0 4 0 J CENTRAL STATES, SE AND SW AREAS PENSION PLAN 001 TRUSTEES OF CENTRAL STATES PENSION FUND 36-6044243 19077948 BARCLAYS GLOBAL INVESTORS 94-3112180 9260205 21 1 0 0 6 0 3 0 1 0 B GOLDMAN SACHS ASSET MANAGEMENT LP 13-3575636 5831543 99 BRIDGEWATER ASSOCIATES, INC. 13-2871809 5475761 21 THE BOSTON COMPANY ASSET MANAGEMENT 04-3404987 5220740 21 1 0 0 6 0 3 0 2 0 C WELLINGTON MANAGEMENT COMPANY LLP 04-2683227 4995401 21 MELLON BANK, N.A. 25-0659306 4657563 18 INVESCO 58-1707262 3899975 21 1 0 0 6 0 3 0 2 0 C LSV ASSET MANAGEMENT 23-2772200 3871092 21 CAPITAL GUARDIAN TRUST COMPANY 95-2553868 3416482 21 NORTHERN TRUST GLOBAL ADVISORS, INC 06-1438425 3251448 99 1 0 0 6 0 3 0 2 0 C OECHSLE INTERNATIONAL ADVISOR, LLC 04-2929117 2633749 21 WILLIAM BLAIR & COMPANY, LLC 36-2214610 2506506 21 STATE STREET CORPORATION 04-1867445 2246813 21 1 0 0 6 0 3 0 2 0 C TRUST COMPANY OF THE WEST 95-2749628 1999447 21 PZENA INVESTMENT MANAGEMENT LLC 13-3860154 1599088 21 DONALD SMITH & CO., INC. -

Securities and Exchange Commission Form S-1 Kkr

S-1/A 1 a2199239zs-1a.htm S-1/A Table of Contents As filed with the Securities and Exchange Commission on July 6, 2010 Registration No. 333-165414 SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Amendment No. 5 to FORM S-1 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 KKR & CO. L.P. (Exact name of Registrant as specified in its charter) Delaware 6282 26-0426107 (State or other jurisdiction of (Primary Standard Industrial (I.R.S. Employer incorporation or organization) Classification Code Number) Identification No.) 9 West 57th Street, Suite 4200 New York, NY 10019 Telephone: (212) 750-8300 (Address, including zip code, and telephone number, including area code, of Registrant's principal executive offices) David J. Sorkin, Esq. General Counsel KKR & Co. L.P. 9 West 57th Street, Suite 4200 New York, NY 10019 Telephone: (212) 750-8300 (Name, address, including zip code, and telephone number, including area code, of agent for service) Copy to: Joseph H. Kaufman, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017-3954 Telephone: (212) 455-2000 Facsimile: (212) 455-2502 Approximate date of commencement of the proposed sale of the securities to the public: As soon as practicable after the Registration Statement becomes effective. If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. -

1% Converticble Securities Exchangable Mge.A

MNV.A; 1% CONVERTICBLE SECURITIES EXCHANGABLE MGE.A; 1.25% GE CO EXCHANGABLE NOTES BOA.K; 1.5% CAP PROTECTED LINKED TO S&P 500 INDEX MWB.A; 1.5% EXCHANGABLE NOTES EXCHANGABLE FOR BYF.E; 1.5% PRINCIPAL PROTECTED NOTES S&P 500 INDEX PGG.A; 2% EXCHANGEABLE NOTES FOR SHARES OF PG COM SPE.A; 3% NOTES EXCHANGEABLE FOR COMMON STOCK OF PFIZER SXN.E; 5.875% SELECT NOTES TRUST SECURITIES LONG TERM SXN.F; 6.30 SELECT NOTES TRUST SECURITIES LONG TERM TLX.D; 8.25%LT CNVT SR SUB NOTES DUE 2012 AAA; AAA FAX; Aberdeen Asia-Pacific Income Fund Inc IAF; Aberdeen Australia Equity Fund Inc FCO; Aberdeen Global Income Fund, Inc. AAC; Ableauctions.Com Inc AIH; Ablest Inc. ABP; Abraxas Petroleum Corporation AXK; Accelr8 Technology Corporation ACU; Acme United Corporation. BRR; ACR Group, Inc. AE; Adams Resources & Energy, Inc. ADK; Adcare Health Systems Inc ADK/WS; ADCARE HEALTH SYSTEMS INC AEY; ADDvantage Technologies Group, Inc. ADH; Adherex Technologies Inc API; Advanced Photonix, Inc. AMM; Advantage Marketing Systems, Inc. ANX; ADVENTRX Pharmaceuticals, Inc. ACY; AeroCentury Corp. AIM; Aerosonic Corporation RIF; AEW REAL ESTATE INCOME FD ANS; AirNet Systems, Inc. AAI; AirTran Holdings, Inc. AA^; Alcoa Inc. ADG; Allied Defense Group (The) ANV; Allied Nevada Gold Corp ALY; Allis-Chalmers Corporation AAU; Almaden Minerals, Ltd. APT; Alpha Pro Tech, Ltd. ALT; Alteon Inc. DIT; AMCON Distributing Company ADL; AMDL INC ABL; American Biltrite Inc. XSI; American Caresource Holdings Inc APO; American Community Properties Trust GMC.AIW; AMERICAN CORP .121507 GMC.AVA; AMERICAN CORP 061507 GMC.AXG; AMERICAN CORP 061508 AIP; American Israeli Paper Mills, Ltd. -

FORM S−1 KKR Co

FORM S−1 KKR Co. L.P. − N/A Filed: July 03, 2007 (period: ) General form of registration statement: Initial statement Table of Contents PART I INFORMATION REQUIRED IN PROSPECTUS SUMMARY RISK FACTORS USE OF PROCEEDS CAPITALIZATION UNAUDITED PRO FORMA FINANCIAL INFORMATION MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS BUSINESS Properties MANAGEMENT Executive Compensation UNDERWRITING LEGAL MATTERS EXPERTS INDEX TO FINANCIAL STATEMENTS PART II ITEM 13. OTHER EXPENSES OF ISSUANCE AND DISTRIBUTION. ITEM 14. INDEMNIFICATION OF DIRECTORS AND OFFICERS. ITEM 15. RECENT SALES OF UNREGISTERED SECURITIES. ITEM 16. EXHIBITS AND FINANCIAL STATEMENT SCHEDULES. ITEM 17. UNDERTAKINGS (a)The undersigned Registrant hereby undertakes to provide to the underwriters SIGNATURES Signature EX−3.1 (EXHIBIT 3.1) EX−3.3 (EXHIBIT 3.3) EX−23.1 (EXHIBIT 23.1) QuickLinks −− Click here to rapidly navigate through this document As filed with the Securities and Exchange Commission on July 3, 2007. Registration No. 333− SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM S−1 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 KKR & CO. L.P. (Exact name of Registrant as specified in its charter) Delaware 6282 26−0426107 (State or other jurisdiction of (Primary Standard Industrial (I.R.S. Employer incorporation or organization) Classification Code Number) Identification No.) 9 West 57th Street, Suite 4200 New York, NY 10019 Telephone: (212) 750−8300 (Address, including zip code, and telephone number, including area code, of Registrant's principal executive offices) William J. Janetschek Chief Financial Officer KKR & Co. L.P. 9 West 57th Street, Suite 4200 New York, NY 10019 Telephone: (212) 750−8300 (Name, address, including zip code, and telephone number, including area code, of agent for service) Copies to: Joseph H.