Paris, Amsterdam, February 12, 2020 Press Release UNIBAIL-RODAMCO

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Developing Employees As Organisational Assets

Developing Employees as Organisational Assets INTRODUCTION The Kingfisher Recruitment • The Person Specification How KMDS is evolving commercial and afterwards in key functions The Group requires from prospec- Kingfisher plc is one of Europe’s leading retailers based Management Development Scheme Investing in a trainee over ten years tive KMDS trainees: The KMDS was launched in 1995 and • a post-graduate certificate in man- around three main sectors - DIY, electrical and general involves significant cost as well as today has 172 individuals on the scheme agement studies from Templeton • excellent interpersonal skills merchandise. The company employs over 130,000 people in invest- risk. The risk includes choosing the working across the Group. All individu- College, Oxford The KMDS represents a key • enthusiasm and drive to become ment by the organisation in its human wrong type of person and equally als following the KMDS route joined in • a ‘skills tool-box’ consisting of 2,900 stores across 15 countries and has some of the best senior managers within 7-10 years assets. The scheme takes high-poten- importantly losing the person to anoth- their early 20s. Recently Kingfisher has day-release training to develop per- known retail brands in Europe, including B&Q, Castorama, • innovative approach to challenges tial graduates who want to make a er organisation during the training recognised that there are benefits in sonal skills Comet, Darty, BUT, Woolworths and Superdrug among opening up the process to existing high- career in retail, and provides them with process. For this reason, Kingfisher • the ability to analyse and make • a ‘buddy’ who is already on the others. -

Case No COMP/M.2951 - A.S

EN Case No COMP/M.2951 - A.S. WATSON / KRUIDVAT Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 27/09/2002 Also available in the CELEX database Document No 302M2951 Office for Official Publications of the European Communities L-2985 Luxembourg COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 27.09.2002 SG (2002) D/231850 In the published version of this decision, some PUBLIC VERSION information has been omitted pursuant to Article 17(2) of Council Regulation (EEC) No 4064/89 concerning non-disclosure of business secrets and other confidential information. The omissions are MERGER PROCEDURE shown thus […]. Where possible the information ARTICLE 6(1)(b) DECISION omitted has been replaced by ranges of figures or a general description. To the notifying party Dear Sir/Madam, Subject: Case No COMP/M.2951 - A.S. Watson/Kruidvat Notification of 29.08.2002 pursuant to Article 4 of Council Regulation No 4064/891 1. On 29 August 2002, the Commission received a notification of a proposed concentration whereby A.S. Watson & Co., Limited (“A.S. Watson”), which belongs to the Hong Kong based group Hutchison Whampoa Limited (“Hutchison”), intends to acquire within the meaning of Article 3(1)(b) of the Council Regulation (EEC) No 4064/89 (“the Merger Regulation”) control over Dutch companies Kruidvat Holding B.V., and Kruidvat Superdrug B.V. (hereinafter ”Kruidvat”). The companies are presently controlled by Kruidvat Beheer B.V. (”Kruidvat Beheer”). 2. After examination of the notification, the Commission has concluded that the notified operation falls within the scope of the Merger Regulation and does not raise serious doubts as to its compatibility with the common market and the functioning of the EEA Agreement. -

N°10 La Gazette Mercredi 21 Novembre 2018 De La Défense Lagazette-Ladefense.Fr Hebdomadaire Gratuit D’Informations Locales

N°10 La Gazette Mercredi 21 novembre 2018 de la Défense lagazette-ladefense.fr Hebdomadaire gratuit d’informations locales Le conseil départemental des Hauts-de-Seine étudie la création « à moyen terme » d’un nouveau siège au sein des bâtiments du Pôle universitaire Léonard de Vinci. Actualités p. 4 ILE-DE-FRANCE LA DEFENSE DépartementDépartement NouveauNouveau déménagementdéménagement Fintech : l’incubateur dansdans quelquesquelques annéesannées ?? met en avant la finance Dossier - P. 2 responsable Actualités p. 9 Actualités p. 5 P. 4 ARCHE NORD Regnault : série LA DEFENSE NANTERRE de réunions d’information Terrasses de P. 6 HAUTS-DE-SEINE En grève, l’Arche : aire de la Poste toujours perturbée jeu et pétanque P. 7 LA DEFENSE Probono factory : des Actualités p. 6 salariés au service des associations LA DEFENSE P. 9 ESPLANADE NORD Total solar La CFDT parle en flex office dans la tour CBX différemment aux cadres P. 10 NANTERRE Le toit de la fac prend feu Actualités p. 8 P. 12 BASKET BALL Double incendie Les salariés DE VINCI dans la commune de la Défense L’e-sport érigé P. 14 NANTERRE moins exposés au même niveau Le théâtre étudiant au diabète ? que les autres à l’honneur N° 10 02 Mercredi 21 novembre 2018 Dossier HAUTS-DE-SEINE Département : nouveau déménagement dans quelques années ? Dans le cadre d’un récent appel d’offres, le conseil mobilier de développement incluant a départemental des Hauts-de-Seine, qui vient à peine minima le futur hôtel départemental. » d’emménager dans ses nouveaux bureaux au sein du bâtiment de Paris La Défense Arena, indique son souhait de Le Département est par ailleurs déménager de nouveau « à moyen terme ». -

2009 Annual Report

2009 ANNUAL REPORT UNIBAIL-RODAMCO / 2009 ANNUAL REPORT 1 Profile 2 Message from the CEO 4 Message from the Chairman of the Supervisory Board 6 Strategy & key figures Stock market performance PROFILE 10 & shareholding structure 2009 Unibail-Rodamco is Europe’s leading listed commercial property company ANNUAL with a portfolio valued at €22.3 billion on December 31, 2009. REPORT A clear strategy The Group is the leading investor, operator and developer of large shopping centres in 14 An unprecedented climate Europe. Its 95 shopping centres, 47 of which receive more than 7 million visits per annum, 12 16 Expertise in retail operations are generally located in major continental European cities with superior purchasing power 18 Differentiation: the key to success and extensive catchment areas. The Group continuously reinforces the attractiveness of 22 An attractive development pipeline 24 Financial firepower for future growth its assets by upgrading the layout, renewing the tenant mix and enhancing the shopping 26 Talented, motivated teams experience. Present in 12 European Union countries, Unibail-Rodamco is a natural business partner for any retailer seeking to penetrate or expand in this market and for any public or Business private institution interested in developing large, integrated retail schemes. Overview A commitment to value creation The Group is also a key player in the Paris region office market, where it focuses on modern, efficient buildings of more than 10,000 m2. Finally, in joint venture with the Paris Chamber 32 Shopping Centres of Commerce and Industry, Unibail-Rodamco owns, operates and develops the major 30 34 France 36 Netherlands convention and exhibition centres of the Paris region. -

Alabama Arizona Arkansas California Riverchase Galleria | Hoover, AL

While we are all eager to get back to business as soon as possible, the timing of our reopening plans is subject to federal, state and local regulations, so projected reopening dates are subject to change. Reopening plans and policies will adhere to federal, state, and local regulations and guidance, and be informed by industry best practices, which will vary based on location and other circumstances. Last Updated: May 27, 2020 Open Properties with Restrictions Alabama Arizona Arkansas California Riverchase Galleria | Hoover, AL Park Place | Tucson, AZ Pinnacle Hills Promenade | Rogers, AR Chula Vista Center | Chula Vista, CA The Shoppes at Bel Air | Mobile, AL The Mall at Sierra Vista | Sierra Vista, AZ Fig Garden Village | Fresno, CA Tucson Mall | Tucson, AZ Galleria at Tyler | Riverside, CA Mt. Shasta Mall | Redding, CA Otay Ranch Town Center | Chula Vista, CA Promenade Temecula | Temecula, CA The Shoppes at Carlsbad | Carlsbad, CA Valley Plaza Mall | Bakersfield, CA Victoria Gardens | Rancho Cucamonga, CA Colorado Connecticut Florida Georgia Park Meadows | Lone Tree, CO Brass Mill Center | Waterbury, CT Altamonte Mall | Altamonte Springs, FL Augusta Mall | Augusta, GA The Shoppes at Buckland Hills | Manchester, CT Coastland Center | Naples, FL Cumberland Mall | Atlanta, GA The Shops at Somerset Square | Glastonbury, CT Governor's Square | Tallahassee, FL North Point Mall | Alpharetta, GA The SoNo Collection | Norwalk, CT Lakeland Square Mall | Lakeland, FL Oglethorpe Mall | Savannah, GA Mizner Park | Boca Raton, FL Peachtree Mall | -

Finance Project

MASTER OF SCIENCE IN FINANCE MASTERS FINAL WORK PROJECT EQUITY RESEARCH: HORNBACH BAUMARKT AG JOÃO MARIA GONÇALVES PAIVA DÓRDIO RODRIGUES SUPERVISOR: ANA ISABEL ORTEGA VENÂNCIO OCTOBER 2020 Acknowledgements This paper represents the end of a journey started in 2018 and I would like to express my sincerest gratitude to all persons involved in these 2 years of the Masters. Firstly, to Professor Ana Venâncio for the guidance, time and patience, not only during this project, but also during classes. Secondly, to my family, parents, sister and grandmother, for supporting and believing in me. And last but not least, to my friends, new and old, for the moments shared in these past 2 years. i Abstract The following project is a valuation of the company Hornbach Baumarkt AG, based on publicly available information until the 6th November 2020. It follows the format recommended by the CFA Institute. Hornbach Baumarkt AG was chosen due to the interest in wanting to explore and learn about the DIY sector and by it being the only publicly traded German company. Hornbach Baumarkt AG is a Top 10 player in the DIY Home Improvement sector in Europe. It was created in 1993 after an IPO that saw Hornbach AG being subdivided in Hornbach Holding AG (Parent Company) and Hornbach Baumarkt AG, having the original company being founded in 1877, in Landau, Germany, but only making their first IPO in 1987. Today, Hornbach Baumarkt AG is a Child company of Hornbach Holding AG. The valuation was derived from an intrinsic valuation, based on a Discounted Cash Flow (DFC) method, more specifically, through a Free Cash Flow to the Firm (FCFF) perspective. -

European Transplant Sport Week 2016 Vantaa, Finland 10

European Transplant Sport Week 2016 Vantaa, Finland 10. - 17.7. Publisher: Suomen Vammaisurheilu ja -liikunta VAU ry Finnish Sports Association of Persons with Disabilities Pictures: Anna Tervahartiala, Lauri Jaakkola, Anssi Walta, Hannes Penttilä, Teemu Lakkasuo Advertising Sales: Printmix Oy, tel. +358 20 710 9510 www.printmix.fi Layout and print: 2 Printmix Oy Table of Contents 1. Welcome words from Ilkka Vass ........................................................................ 4 2. Welcome words from Kari Nenonen ................................................................. 5 3. Vantaa 2016 in a nutshell .................................................................................... 6 4. Organizing Committee ......................................................................................... 7 5. Website and Social Media .................................................................................... 9 6. Accommodation ......................................................................................................10 7. Meals ..........................................................................................................................11 8. Transportation ..........................................................................................................13 9. Accreditation Card .................................................................................................13 10. Vantaa Info and Travel Card .................................................................................14 -

Classic Pizza Restaurant and Hangonmakaronitehdas Won Kasvu Open 2016 Start Again- Series

CLASSIC PIZZA RESTAURANT HANGON MAKARONITEHDAS PRESS RELEASE 31.10.2016 Classic Pizza Restaurant and HangonMakaronitehdas won Kasvu Open 2016 Start again- series Kasvu Open is Finland´s largest sparring program for small and medium sized companies that are eager to grow and go to the international market. Throughout the competition these growth oriented companies have an opportunity to present their own growth plans to a great number of experts, free of charge. The program culminated last week with Kasvu Open Carneval event in Jyväskylä. Classic Pizza Restaurant / Hangon Makaronitehdas won the first prize in a series of companies already operating – Kasvu Open Start again. Classic Pizza Restaurant / Hangon Makaronitehdas have the best potential for growth and internationalization. The winners were selected from the 79 Kasvu Open finalists, who were chosen from over 700 companies that took part to Kasvu Open program by presenting their growth plans. Companies were from different industries and in different parts of the country. During the year, companies got free coaching from experts in various fields. The jury opened the selection criteria Classic Pizza Restaurant / Hangon Makaronitehdas stated that they prepare pizza and fresh pasta from high-quality ingredients and have surprising recipes and do all this better than anyone else. According to the jury, the company has caught the trend: people consume less, but better. They are not competing with price, but everyday luxury. The world's best pizza chain in Finland is a fine and brave idea. "Our country does not increase with technology alone, but needs the service and marketing expertise as well. -

Brookfield Property REIT Inc. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (MARK ONE) ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2018 or o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to COMMISSION FILE NUMBER 1-34948 Brookfield Property REIT Inc. (Exact name of registrant as specified in its charter) Delaware 27-2963337 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification Number) 250 Vesey Street, 15th Floor, New York, NY 10281-1023 (Address of principal executive offices) (Zip Code) (212) 417-7000 (Registrant's telephone number, including area code) Securities Registered Pursuant to Section 12(b) of the Act: Title of Each Class A Stock: Name of Each Exchange on Which Registered: Class A Stock, $.01 par value NASDAQ Global Select Market Securities Registered Pursuant to Section 12(g) of the Act: 6.375% Series A Cumulative Redeemable Preferred Stock Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

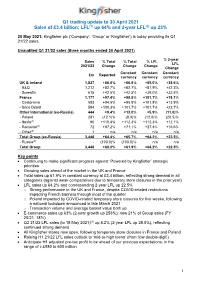

Q1 Trading Update to 30 April 2021 Sales of £3.4 Billion; LFL(1) up 64% and 2-Year LFL(2) up 23%

Q1 trading update to 30 April 2021 Sales of £3.4 billion; LFL(1) up 64% and 2-year LFL(2) up 23% 20 May 2021: Kingfisher plc (‘Company’, ‘Group’ or ‘Kingfisher’) is today providing its Q1 21/22 sales. Unaudited Q1 21/22 sales (three months ended 30 April 2021) % 2-year Sales % Total % Total % LFL LFL 2021/22 Change Change Change Change Constant Constant Constant £m Reported currency currency currency UK & Ireland 1,827 +66.8% +66.8% +65.0% +38.6% - B&Q 1,212 +82.7% +82.7% +81.9% +42.3% - Screwfix 615 +42.5% +42.5% +39.0% +32.5% France 1,177 +97.4% +98.8% +101.7% +18.1% - Castorama 583 +94.5% +95.8% +101.8% +13.9% - Brico Dépôt 594 +100.3% +101.7% +101.7% +22.7% Other International (ex-Russia) 444 +9.4% +13.0% +5.9% (11.0)% - Poland 281 (12.1)% (8.9)% (12.0)% (20.5)% - Iberia(3) 90 +110.8% +112.3% +112.3% +12.1% - Romania(4) 72 +67.2% +71.1% +27.4% +16.6% - Other(5) 1 n/a n/a n/a n/a Total Group (ex-Russia) 3,448 +64.4% +65.7% +64.2% +22.5% - Russia(6) - (100.0)% (100.0)% n/a n/a Total Group 3,448 +60.0% +61.9% +64.2% +22.5% Key points • Continuing to make significant progress against ‘Powered by Kingfisher’ strategic priorities • Growing sales ahead of the market in the UK and France • Total sales up 61.9% in constant currency at £3.4 billion, reflecting strong demand in all categories (against weak comparatives due to temporary store closures in the prior year) • LFL sales up 64.2% and corresponding 2-year LFL up 22.5% o Strong performance in the UK and France, despite COVID-related restrictions impacting French banners through most -

WHAT Architect WHERE Notes Arrondissement 1: Louvre Built in 1632 As a Masterpiece of Late Gothic Architecture

WHAT Architect WHERE Notes Arrondissement 1: Louvre Built in 1632 as a masterpiece of late Gothic architecture. The church’s reputation was strong enough of the time for it to be chosen as the location for a young Louis XIV to receive communion. Mozart also Church of Saint 2 Impasse Saint- chose the sanctuary as the location for his mother’s funeral. Among ** Unknown Eustace Eustache those baptised here as children were Richelieu, Jeanne-Antoinette Poisson, future Madame de Pompadour and Molière, who was also married here in the 17th century. Amazing façade. Mon-Fri (9.30am-7pm), Sat-Sun (9am-7pm) Japanese architect Tadao Ando has revealed his plans to convert Paris' Bourse de Commerce building into a museum that will host one of the world's largest contemporary art collections. Ando was commissioned to create the gallery within the heritage-listed building by French Bourse de Commerce ***** Tadao Ando businessman François Pinault, who will use the space to host his / Collection Pinault collection of contemporary artworks known as the Pinault Collection. A new 300-seat auditorium and foyer will be set beneath the main gallery. The entire cylinder will be encased by nine-metre-tall concrete walls and will span 30 metres in diameter. Opening soon The Jardin du Palais Royal is a perfect spot to sit, contemplate and picnic between boxed hedges, or shop in the trio of beautiful arcades that frame the garden: the Galerie de Valois (east), Galerie de Montpensier (west) and Galerie Beaujolais (north). However, it's the southern end of the complex, polka-dotted with sculptor Daniel Buren's Domaine National du ***** 8 Rue de Montpensier 260 black-and-white striped columns, that has become the garden's Palais-Royal signature feature. -

Brookfield Properties' Retail Group Overview

Retail Overview Brookfield Properties’ Retail Group Overview We are Great Gathering Places. We embrace our cultural core values of Humility, Attitude, Do The Right Thing, H Together and Own It. HUMILITY Brookfield Properties’ retail group is a company focused A ATTITUDE exclusively on managing, leasing, and redeveloping high- quality retail properties throughout the United States. D DO THE RIGHT THING T TOGETHER O HEADQUARTERS CHICAGO OWN IT RETAIL PROPERTIES 160+ STATES 42 INLINE & FREESTANDING GLA 68 MILLION SQ FT TOTAL RETAIL GLA 145 MILLION SQ FT PROFORMA EQUITY MARKET CAP $20 BILLION PROFORMA ENTERPRISE VALUE $40 BILLION Portfolio Map 2 7 1 4 3 5 3 6 2 1 2 1 1 2 1 3 3 3 1 1 2 4 1 2 1 3 2 1 1 10 4 2 5 1 4 10 2 3 3 1 48 91 6 5 6 2 7 6 4 5 11 7 4 1 1 1 2 2 2 5 7 1 2 1 2 1 1 1 1 6 1 3 5 3 4 15 19 2 14 11 1 1 3 2 1 2 1 1 3 6 2 1 3 4 18 2 17 3 1 2 1 3 2 2 5 3 6 8 2 1 12 9 7 5 1 4 3 1 2 1 2 16 3 4 13 3 1 2 6 1 7 9 1 10 5 4 2 1 4 6 11 5 3 6 2 Portfolio Properties 1 2 3 3 3 1 7 4 Offices 13 12 2 Atlanta, GA 7 3 1 1 Chicago, IL Baltimore, MD 8 5 2 Dallas, TX 4 Los Angeles, CA 6 New York, NY 8 2 9 5 Property Listings by State ALABAMA 7 The Oaks Mall • Gainesville 3 The Mall in Columbia • Columbia (Baltimore) 9 Brookfield Place • Manhattan WASHINGTON 8 Pembroke Lakes Mall • Pembroke Pines 4 Mondawmin Mall • Baltimore 10 Manhattan West • Manhattan 1 Riverchase Galleria • Hoover (Birmingham) 1 Alderwood • Lynnwood (Seattle) 5 Towson Town Center • Towson (Baltimore) 11 Staten Island Mall • Staten Island 2 The Shoppes at Bel Air • Mobile (Fort Lauderdale)