Chapter 5 Natural Gas Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

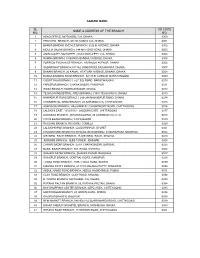

Agrani Bank Sl No. Name & Address of the Branch Ad Code

AGRANI BANK SL AD CODE NAME & ADDRESS OF THE BRANCH NO. NO. 1 HEAD OFFICE, MOTIJHEEL C/A, DHAKA 0000 2 PRINCIPAL BRANCH, 9/D DILKUSHA C/A, DHAKA 0001 3 BANGA BANDHU AVENUE BRANCH, 32 B.B. AVENUE, DHAKA 0002 4 MOULVI BAZAR BRANCH, 144 MITFORD ROAD, DHAKA. 0003 5 AMIN COURT, MOTIJHEEL, 62/63 MOTIJHEEL C/A, DHAKA 0004 6 RAMNA BRANCH, 18 BANGA BANDHU AVENUE, DHAKA 0005 7 FOREIGN EXCHANGE BRANCH, 1/B RAJUK AVENUE, DHAKA 0006 8 SADARGHAT BRANCH,3/7/1&2 JONSON RD,SADARGHAT, DHAKA. 0007 9 BANANI BRANCH, 26 KAMAL ATATURK AVENUE, BANANI, DHAKA. 0008 10 BANGA BANDHU ROAD BRANCH, 32/1 B.B. AVENUE, NARAYANGONJ 0009 11 COURT ROAD BRANCH, 52/1 B.B.ROAD, NARAYANGONJ 0010 12 FARIDPUR BRANCH, CHAWK BAZAR, FARIDPUR 0011 13 WASA BRANCH, KAWRAN BAZAR, DHAKA. 0012 14 TEJGAON INDUSTRIAL AREA BRANCH, 315/A TEJGAON I/A, DHAKA 0013 15 NAWABPUR ROAD BRANCH, 243-244 NAWABPUR ROAD, DHAKA 0014 16 COMMERCIAL AREA BRANCH, 28 AGRABAD C/A, CHITTAGONG 0015 17 ASADGONJ BRANCH, HAJI AMIR ALI CHOWDHURY ROAD, CHITTAGONG 0016 18 LALDIGHI EAST, 1012/1013 - LALDIGHI EAST, CHITTAGONG 0017 19 AGRABAD BRANCH, JAHAN BUILDING, 24 AGRABAD C/A, CTG 0018 20 COX'S BAZAR BRANCH, COX'S BAZAR 0019 21 RAJGANJ BRANCH, RAJGANJ, COMILLA 0020 22 LALDIGHIRPAR BRANCH, LALDIGHIRPAR, SYLHET 0021 23 CHAUMUHANI BRANCH,D.B.ROAD, BEGUMGONJ, CHAUMUHANI, NOAKHALI 0022 24 SIR IQBAL RAOD BRANCH, 25 SIR IQBAL RAOD, KHULNA 0023 25 JESSORE BRANCH, JESS TOWER, JESSORE 0024 26 CHAWK BAZAR BRANCH, 02/01 CHAWK BAZAR, BARISAL 0025 27 BARA BAZAR BRANCH, N.S. -

Performance of Sweet Pepper Under Protective

INTERNATIONAL JOURNAL OF ENVIRONMENT Volume-3, Issue-1, Dec-Feb 2013/14 ISSN 2091-2854 Received:17 January Revised:11February Accepted:17Feburary INVENTORY OF THREATENED PLANTS OF BANGLADESH AND THEIR CONSERVATION MANAGEMENT M. Harun-ur-Rashid, M. Enamur Rashid and M. Atiqur Rahman* Department of Botany, University of Chittagong Chittagong 4331, Bangladesh *Corresponding author: [email protected] Abstract The study aimed at inventorying of threatened plant species of Bangladesh to determine their status of occurrence for emphasizing the setting-up of national conservation strategies and sustainable management. Complete inventory of two families, the Apocynaceae and Vitaceae, has been made and recognized 28 threatened species facing environmental threats, and need sustainable conservation management. The study was based on long-term field investigation, survey of relevant floristic literature and examination of herbarium specimens. An enumeration of threatened taxa is prepared with updated field data on conservation status to include into Red Data Book of Bangladesh. Key words: Inventory, threatened plant species, conservation, management, Bangladesh. Introduction Global biodiversity is depleting at an alarming rate due to human interferences and environmental degradation, causing high risk of extinction. Human impact on nature has reached at such a high proportion that the world is today witnessing an unprecedented rate of species loss. Many more species are disappearing from the nature before their discovery and determination. The 1997 IUCN Red List of Threatened Plants revealed that 12.5% or c.34,000 of the world’s vascular plant species are at risk of extinction, including 7% of family International Journal of Environment ISSN 2091-2854 141 | P a g e Apocynaceae and 5% of Vitaceae (Walter & Gillett, 1998). -

Annual Gas Production and Consumption, 2010-2011

Annual Gas Production and Consumption, 2010-2011 October 2011 Hydrocarbon Unit Energy and Mineral Resources Division 1 Table of Content 1. Summary 1 2. Production 3 2.1. National Companies 3 2.1.1. Bangladesh Gas Fields Ltd 3 2.1.1.1. Titas Gas Field 4 2.1.1.2. Habiganj Gas Field 4 2.1.1.3. Bakhrabad Gas Field 4 2.1.1.4. Narshingdi Gas Field 4 2.1.1.5. Meghna Gas Field 4 2.1.1.6. Feni Gas Field 4 2.1.2. Sylhet Gas Field Ltd 4 2.1.2.1. Kailas Tila Gas Field 5 2.1.2.2. Rashidpur Gas Field 5 2.1.2.3. Beani Bazar Gas Field 5 2.1.2.4. Sylhet Gas Field 5 2.1.3. Bangladesh Petroleum Exploration and Production Co. Ltd 5 2.1.3.1. Fenchuganj Gas Field 5 2.1.3.2. Salda Gas Field 6 2.1.3.3. Shahbazpur Gas Field 6 2.1.3.4 Semutang gas Field 6 2.1.3.5 Sundalpur Gas Field 6 2.2. International Oil Companies 6 2.2.1. Chevron Bangladesh 7 2.2.1.1. Bibiyana Gas Field 7 2.2.1.2. Jalalabad Gas Field 7 2.2.1.3. Moulavi Bazar Gas Field 7 2.2.2. Tullow Oil 7 2.2.2.1. Bangura Gas Field 7 2.2.3. Santos (Former Cairn) 8 3. Gas Supply and Consumption 8 4. Figures 1 – 27 9-24 \\HCUCOMMONSERVER\Common Server L\01-039 Strategy Policy Expert\IMP\Annual Report 2010-11\Annual Gas Production and Consumption 2010-11.doc 2 1. -

APL Services to Bangladesh – Intra-Asia Services

APL Services to Bangladesh – Intra-Asia Services THE APL ADVANTAGE • Reliable and dedicated services that connect the sea ports of Chittagong, Mongla and Dhaka • Availability of D45’, GOH and all types of ground equipment, enabling APL to fulfil customer’s unique (by rail and river-barge) with the world’s major markets requirements • Extensive feeders connecting Chittagong with Singapore, Colombo and Port Klang, providing • Dedicated and experienced customer support representatives to serve your ocean shipping needs links to global destinations • APL Bangladesh accepts single buyer consolidating business - CFS/CY JAPAN SOUTH Nagoya Qingdao KOREA Tokyo CHINA Busan SKX APL Offices Hakata Yokohama JORDAN Shanghai Olta Kobe Aqaba PAKISTAN Hososhima Chittagong Sokhna Doha (Hamad Port) Ningbo Jubail Shibushi APL Bangladesh Pvt. Ltd. Karachi (SAPT) Xiamen JSX World Trade Center, 5th Floor EGYPT Dammam Jebel Ali BANGLADESH Port Qasim Dhaka Yantian Holding No. 102-103 SAUDI ARABIA UAE Mundra Khulna Nansha Taipei Agrabad Commercial Area Chittagong Shekou TAIWAN Jeddah Pipavav Kaohsiung Chittagong-4100, Bangladesh Nhava Sheva Hong Kong Tel: (88) (31) 714 063, (88) (031) 724 907 INDIA AS1 Dhaka CS1 APL Bangladesh Pvt. Ltd. WAX I-K TOWER, 3rd Floor, Unit D, Plot # CEN(A)-2 SRI LANKA MALAYSIA Colombo CIX North Avenue, Gulshan-2 RSX Port Klang Dhaka-1212, Bangladesh Westport Tel: (88) (02) 5881 3705, (88) (02) 5881 3591 Khulna Tanjung Pelepas APL Bangladesh Pvt. Ltd. Singapore United Tower, 4th Floor, 4, KDA Avenue Khulna Sadar, Khulna, Bangladesh Tel: -

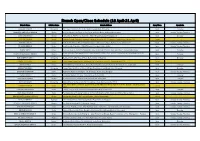

Branch Open/Close Schedule (16 April-21 April)

Branch Open/Close Schedule (16 April-21 April) Branch Name Division Name Branch Address Open/Close Open Date AGRABAD BRANCH Chittagong C&F Tower ( 1st Floor), 1712, Sk. Mujib Road, Agrabad, Chittaging. Open Everyday ARAIHAZAR SME/KRISHI BRANCH Dhaka Shahjalal Market (1st Floor), College Road, Araihazar Bazar, Araihazar,Narayangonj. Open Sunday, Tuesday, Thursday ASAD GATE BRANCH Dhaka House No: 01, Plot No: 01, Asad Gate, Mirpur Road, Dhaka-1207.Bangladesh Open Everyday ASHKONA BRANCH Dhaka Ashkona Branch, Ashkona Community Center & Decorator, 567/1, Ashkona, Dakhin Khan, Dhaka-1230. Closed ASHULIA BRANCH Dhaka BRAC Bank Limited, “Abbas Shopping Complex” (1st Floor), Jamgara, Ashulia, Savar, Dhaka-1341 Open Sunday, Tuesday, Thursday ATI BAZAR BRANCH Dhaka Hazi Nuruddin Plaza House#13,ATI Bazar, Keranigonj ,Dhaka -1312 Open Sunday, Tuesday, Thursday BADDA SMESC Dhaka The Pearl Trade Center (PTC),Holding No: Cha- 90/3,Progoti Shoroni Road, Ward No-21,Thana-Badda,Dhaka Open Everyday Shaikh Mansion, Holding# 226, Main road, Ward# 05, Rahater Mor, 1st floor, Pourashava & Thana# Bagerhat, Dist. BAGERHAT SME/KRISHI BRANCH Khulna Open Everyday Bagerhat BAHADDERHAT SMESC Chittagong Mamtaz Tower, 4540 Arakan Road, Bahaddarhat, Chittagong. Open Everyday BANANI - 11 BRANCH Dhaka South Breeze Center,Plot # 5, Building-G (1st & 2nd Floor), Road-11, Banani,Dhaka-1213 Closed BANANI BRANCH Dhaka Borak Mehnoor, Holding # 51/B, Kamal Ataturk Avenue, Banani C/A, Ward: 19; Dhaka-1213, Bangladesh Open Everyday BANDARTILA SMESC Chittagong Osman Plaza, 1st Floor, 800/new, MA Aziz Road, Airport road, Bondortila, Chittagong. Open Everyday BANIACHONG BRANCH Sylhet Hazi Harun Mansion, Holding No # 5, BoroBazar, Baniachong, Habigonj. Open Sunday, Tuesday, Thursday BARISALBRANCH Barisal S. -

Study of Water Quality of Sylhet City and Its Restaurants: Health Associated Risk Assessment

Iran. J. Environ. Health. Sci. Eng., 2006, Vol. 3, No. 1, pp. 9-18 STUDY OF WATER QUALITY OF SYLHET CITY AND ITS RESTAURANTS: HEALTH ASSOCIATED RISK ASSESSMENT *1R. Alam, 1J. B. Alam, 2M. M. Hasan, 1 S. R. Das, 1K. Rahman, 1B. K. Banik 1Civil and Environmental Engineering Department, Shahjalal University of Science and Technology, Sylhet, Bangladesh 2Industrial and Production Engineering Department, Shahjalal University of Science and Technology, Sylhet, Bangladesh Received 13 July 2005; revised 20 August 2005; accepted 25 November 2005 ABSTRACT A study of the water quality conditions of Sylhet city of Bangladesh and its restaurants was carried out to assess risks to human health. The investigation was based on questionnaire survey of restaurants and laboratory tests on water samples obtained from the restaurants, tube wells of the city and Surma River the two main sources of water supply to the city. The test parameters were dissolved oxygen; conductance, hardness, pH, temperature, turbidity, essential and trace elements, dissolved and suspended solids and coliform bacteria. The quality of sanitary facilities and handling of food in the restaurants were also examined. It was found that the drinking water of each restaurant was contaminated with fecal coliforms and 25% restaurants had unsafe levels of iron in the water supply. Improper solid waste dumping was found as one of the reasons of groundwater pollution. Statistical analysis based on Pearson’s correlation coefficient revealed significant correlation between the extent of groundwater pollution and dumping of solid waste effluents in the immediate vicinity of ground water (tube wells). It was observed that 75.69% (coefficient of determination r2= 0.7569) variation in the value of groundwater near the dumping place showed association with variation in the value of water quality within the dumping place. -

127 Branches

মেটলাইফ পলললির প্রিপ্রিয়াি ও অꇍযাꇍয মপমেন্ট বযা廬ক এপ্রিয়ার িকল শাখায় ꇍগদে প্রদান কমর তাৎক্ষপ্রিকভাদব বমু ে লনন ররপ্রভপ্রꇍউ স্ট্যাম্প ও সীলসহ রিটলাইদের প্ররপ্রসট এই িলু বধা পাওয়ার জনয গ্রাহকমক মকান অলিলরক্ত লফ অথবা স্ট্যাম্প চাজ জ প্রদান করমি হমব না Sl. No. Division District Name of Branches Address of Branch 1 Barisal Barisal Barishal Branch Fakir Complex 112 Birshrashtra Captain Mohiuddin Jahangir Sarak 2 Barisal Bhola Bhola Branch Nabaroon Center(1st Floor), Sadar Road, Bhola 3 Chittagong Chittagong Agrabad Branch 69, Agrabad C/ A, Chittagong 4 Chittagong Chittagong Anderkilla Branch 184, J.M Sen Avenue Anderkilla 5 Chittagong Chittagong Bahadderhat Branch Mamtaz Tower 4540, Bahadderhat 6 Chittagong Chittagong Bank Asia Bhaban Branch 39 Agrabad C/A Manoda Mansion (2nd Floor), Holding No.319, Ward No.3, College 7 Chittagong Comilla Barura Branch Road, Barura Bazar, Upazilla: Barura, District: Comilla. 8 Chittagong Chittagong Bhatiary Branch Bhatiary, Shitakunda 9 Chittagong Brahmanbaria Brahmanbaria Branch "Muktijoddha Complex Bhaban" 1061, Sadar Hospital Road 10 Chittagong Chittagong C.D.A. Avenue Branch 665 CDA Avenue, East Nasirabad 1676/G/1 River City Market (1st Floor), Shah Amant Bridge 11 Chittagong Chaktai Chaktai Branch connecting road 12 Chittagong Chandpur Chandpur Branch Appollo Pal Bazar Shopping, Mizanur Rahman Road 13 Chittagong Lakshmipur Chandragonj Branch 39 Sharif Plaza, Maddho Bazar, Chandragonj, Lakshimpur 14 Chittagong Noakhali Chatkhil Branch Holding No. 3147 Khilpara Road Chatkhil Bazar Chatkhil 15 Chittagong Comilla Comilla Branch Chowdhury Plaza 2, House- 465/401, Race Course 16 Chittagong Comilla Companigonj Branch Hazi Shamsul Hoque Market, Companygonj, Muradnagar J.N. -

Bangladesh Investigation (IR)BG-6 BG-6

BG-6 UNITED STATES DEPARTMENT OF THE INTERIOR GEOLOGICAL SURVEY PROJECT REPORT Bangladesh Investigation (IR)BG-6 GEOLOGIC ASSESSMENT OF THE FOSSIL ENERGY POTENTIAL OF BANGLADESH By Mahlon Ball Edwin R. Landis Philip R. Woodside U.S. Geological Survey U.S. Geological Survey Open-File Report 83- ^ 0O Report prepared in cooperation with the Agency for International Developme U.S. Department of State. This report is preliminary and has not been reviewed for conformity with U.S. Geological Survey editorial standards. CONTENTS INTPDDUCTION...................................................... 1 REGIONAL GEOLOGY AND STRUCTURAL FRAMEWORK......................... 3 Bengal Basin................................................. 11 Bogra Slope.................................................. 12 Offshore..................................................... 16 ENERGY RESOURCE IDENTIFICATION............................."....... 16 Petroleum.................................................... 16 History of exploration.................................. 17 Reserves and production................................. 28 Natural gas........................................ 30 Recent developments................................ 34 Coal......................................................... 35 Exploration and Character................................ 37 Jamalganj area..................................... 38 Lamakata-^hangarghat area.......................... 40 Other areas........................................ 41 Resources and reserves.................................. -

Lions Clubs International Club Membership Register Summary 116 111 4 04-2014 315B4 025887 5 0 0 0 5 4080 23 24 4 04-2014 315B4 0

LIONS CLUBS INTERNATIONAL CLUB MEMBERSHIP REGISTER SUMMARY THE CLUBS AND MEMBERSHIP FIGURES REFLECT CHANGES AS OF APRIL 2014 MEMBERSHI P CHANGES CLUB CLUB LAST MMR FCL YR TOTAL IDENT CLUB NAME DIST NBR COUNTRY STATUS RPT DATE OB NEW RENST TRANS DROPS NETCG MEMBERS 4080 025887 CHITTAGONG REP OF BANGLADESH 315B4 4 04-2014 111 5 0 0 0 5 116 4080 025888 CHITTAGONG AGRABAD REP OF BANGLADESH 315B4 4 04-2014 24 4 0 0 -5 -1 23 4080 025891 CHITTAGONG KARNAPHULI REP OF BANGLADESH 315B4 4 04-2014 57 14 0 0 0 14 71 4080 025892 CHITTAGONG KHATUNGANJ REP OF BANGLADESH 315B4 4 04-2014 31 14 0 0 0 14 45 4080 032270 CHITTAGONG KHULSHI REP OF BANGLADESH 315B4 4 04-2014 69 7 0 0 0 7 76 4080 034333 CHITTAGONG COSMOPOLITAN REP OF BANGLADESH 315B4 4 04-2014 26 0 0 0 0 0 26 4080 034568 CHITTAGONG PRESIDENCY REP OF BANGLADESH 315B4 4 04-2014 81 12 0 0 -3 9 90 4080 039753 CHITTAGONG METROPOLITAN REP OF BANGLADESH 315B4 4 04-2014 19 14 0 0 0 14 33 4080 040917 CHITTAGONG PANORAMA CITY REP OF BANGLADESH 315B4 4 03-2014 10 0 0 0 0 0 10 4080 048222 CHITTAGONG CITY REP OF BANGLADESH 315B4 4 04-2014 52 2 0 1 -10 -7 45 4080 048920 CHITTAGONG CENTRAL REP OF BANGLADESH 315B4 4 04-2014 50 8 1 0 0 9 59 4080 050434 CHITTAGONG PROGRESSIVE WEST REP OF BANGLADESH 315B4 4 11-2013 15 0 0 0 0 0 15 4080 053972 CHITTAGONG ACTION CITY REP OF BANGLADESH 315B4 4 04-2014 20 0 0 0 0 0 20 4080 054152 CHITTAGONG PROGRESSIVE SOUTHREP OF BANGLADESH 315B4 4 04-2014 18 2 0 0 0 2 20 4080 057313 CHITTAGONG GREEN CITY REP OF BANGLADESH 315B4 4 04-2014 25 12 0 0 0 12 37 4080 057684 CHITTAGONG PARIJAT -

Annual Report July 2016 – June 2017 Bangladesh Atomic Energy

Annual Report July 2016 – June 2017 Bangladesh Atomic Energy Commission Introduction Bangladesh Atomic Energy Commission (BAEC) was founded in February 1973 through the promulgation of Presidential Order 15 of 1973 with the objective of promoting peaceful applications of nuclear energy in Bangladesh. By this time BAEC emerged as the largest organization for scientific and technological research especially in the field of nuclear energy in this country. The essentially goal-oriented research & development (R&D) programmes in physical sciences, biological sciences, engineering sciences and nuclear power field have been undertaken in the light of the overall need of the country so that the outcome of the activities can be directly contributed for socio-economic betterment. Programmes of BAEC are chosen in a manner so that the priority, aspiration and needs of the country are amply reflected in their execution. Notable services of BAEC include modern nuclear medicine services to mass people, specially to the poorest section of the society, protection of public health and the environment through radioactivity monitoring of all imported food items, practice of safety culture against all kinds of radiation hazards, sterilization of medicine and medical equipment, food preservation, development of high quality polymer materials, chemical analysis of industrial products for QC purposes, chemical analysis of food and environmental samples for protection against pollution, industrial NDT and material testing services etc. In the last few years, the BAEC has undertaken the challenge of implementing the Rooppur Nuclear Power Project (RNPP) as one of its highest priority task. The R&D programmes of BAEC are executed through its different institutes, centres and divisional laboratories equipped with state-of the-art facilities and installation. -

Gas Production in Bangladesh

Annual Report PETROBANGLA2018 PETROBANGLA PETROBANGLA Petrocentre, 3 Kawran Bazar Commercial Area Dhaka-1215, Bangladesh, GPO Box No-849 Tel : PABX : 9121010–16, 9121035–41 Fax : 880–2–9120224 E-mail : [email protected] Website : www.petrobangla.org.bd 04 Message of the Adviser (Minister) to the Hon’ble Prime Minister 05 Message of the Hon’ble State Minister, MoPEMR 06 Message of the Senior Secretary, EMRD 07 Introduction by Chairman, Petrobangla 10 Board of Directors (Incumbent) Contents 11 Past and Present Chairmen of Petrobangla 12 The Genesis and Mandate 14 Petrobangla and the Government 16 A Brief History of Oil, Gas and Mineral Industry in Bangladesh 19 Activities of Petrobangla 42 Companies of Petrobangla 62 Development Programmes for FY 2017-18 67 Future Programmes 68 Plan for Production Augmentation 69 Data Sheets 77 Statement of Profit or Loss and Other Comprehensive Income 78 Statement of Financial Position 79 Statement of Cash Flows 02 Annual Report 2018 PETROBANGLA Our To provide energy for sustainable economic growth and maintain energy security Vision of the country • To enhance exploration and exploitation of natural gas Our • To provide indigenous Mission primary energy to all areas and all socio economic groups • To diversify indigenous energy resources • To develop coal resources as an alternative source of energy • To promote CNG, LNG and LPG to minimize gas demand and supply gap as well as to improve environment • To contribute towards environmental conservation of the country • To promote efficient use of gas with a view to ensuring energy security for the future Annual Report 2018 03 Tawfiq-e-Elahi Chowdhury, BB, PhD Adviser (Minister) to the Hon’ble Prime Minister Power, Energy & Mineral Resources Affairs Govt. -

Bangladesh Gas Fields Company Limited for the Asian Development Bank

Initial Environmental Examination Document Stage: Update Project Number: P45203 (BAN) September 2016 People’s Republic of Bangladesh: Natural Gas Infrastructure and Efficiency Improvement Project (Component 1 - Installation of Wellhead Gas Compressors at Location “A” of Titas Gas Field) Prepared by Bangladesh Gas Fields Company Limited for the Asian Development Bank. This is an updated version of the draft originally posted in August 2016 available on https://www.adb.org/sites/default/files/project-document/190161/45203-006-iee-01.pdf. CURRENCY EQUIVALENTS (as of 3 August 2016) Currency unit – Taka (Tk) Tk 1.00 = $0.012755 $1.00 = Tk78.40 ABBREVIATIONS ADB - Asian Development Bank AIIB - Asian Infrastructure Investment Bank BGFCL - Bangladesh Gas Fields Company Limited CITES - Convention on International Trade in Endangered Species of Wild Fauna and Flora DOE - Department of Environment EA - Executing Agency ECA - Environment Conservation Act ECC - Environmental Clearance Certificate ECR - Environment Conservation Rules EIA - Environmental Impact Assessment EMP - Environmental Management Plan EMRD - Energy and Mineral Resources Division ESMS - Environment and Safety Management System GoB - Government of Bangladesh GRC - Grievance Redress Committee IEE - Initial Environmental Examination LCC - Locational Clearance Certificate MOEF - Ministry of Environment and Forests MPEMR - Ministry of Power, Energy and Mineral Resources NOC - No Objection Certificate PIU - Project Implementation Unit ROW - Right of Way SPS - Safeguard Policy Statement WEIGHTS AND MEASURES oC - degree Celsius dB(A) - A-weighted decibel ha - hectare Hp - horsepower lahk - 100,000 ppb - parts per billion ppm - parts per million µg/m3 - microgram per cubic meter m2 - square meter NOTE In this report, "$" refers to US dollars. This initial environmental examination is a document of the borrower.