RFHL-Annual-Report-2017.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2020 2 REPUBLIC BANK (GUYANA) LIMITED ANNUAL REPORT 1

1 Annual Report 2020 2 REPUBLIC BANK (GUYANA) LIMITED ANNUAL REPORT 1 While we were at home being safe, the world started to look differently. For us, it was a time of change as well. We had to adapt to our transformed lives. We found new ways to work, to learn, to be together. We found a new perspective on ourselves, our neighbours, our country and the world. As a Group, we affirmed the hope that we could maintain the lives we built. So we found solutions to serve the unique needs of this time. We found ways to support our customers’ financing, increased our digital offerings, and changed our in-branch approach to be socially distant yet fully committed. At every step, and across all our territories, we kept a positive outlook. For we wanted all our communities to keep believing that a great future is, and always will be, ours. 2 REPUBLIC BANK (GUYANA) LIMITED ANNUAL REPORT The Bank at a Glance About Us Total Assets ($ Billion) 250 Established in 1836, Republic Bank (Guyana) 205.3 180.2 168.2 146.2 151.6 Limited is one of Guyana’s longest-serving institutions and is a recognised leader in the 200 provision of financial services. Over the past year, the Bank has concentrated on growing its lending portfolio, with particular emphasis 150 on small and medium enterprises. The Bank remains committed to providing customised, efficient and competitively priced financial 100 services, and to maintaining a philosophy of social investment in Guyana. 50 0 2020 2019 2018 2017 2016 Operating Branches Profit After Tax ($ Million) 5,000 3,494.6 3,845.8 3,134.0 2,738.9 2,703.0 Anna Regina Vreed-en-Hoop 4,000 Diamond Camp Street New Amsterdam Water Street Rose Hall Triumph D’Edward 3,000 Linden Corriverton 2,000 Lethem 1,000 0 2020 2019 2018 2017 2016 3 Share Price ($) Network 2020 370. -

Prepared for Presentation at the Inaugural AML/CFT Empirical Research Conference British Colonial Hilton Hotel, Nassau, Bahamas January 22-23, 2020

From Hegemony to Hegemony: “De-risking,” Indigenous Regional Banks and Regional Integration in the Caribbean Community Clifford E. Griffin, PhD, North Carolina State University June Soomer, PhD, Secretary General, Association of Caribbean States Prepared for Presentation at the Inaugural AML/CFT Empirical Research Conference British Colonial Hilton Hotel, Nassau, Bahamas January 22-23, 2020 From Hegemony to Hegemony: “De-risking,” Indigenous Regional Banks and Regional Integration in the Caribbean Community Clifford E. Griffin, PhD, North Carolina State University June Soomer, PhD, Secretary General, Association of Caribbean States Introduction The paradox of geography continues to explain much of the opportunities and challenges facing the 20-member states and territories that comprise the Caribbean Community today, including those occasioned by the recent of “de-risking” phenomenon, which has witnessed the withdrawal of correspondent banking services. On the one hand, proximity to the US, coupled with economic openness, have created opportunities for economic development in the areas of tourism, hydrocarbons, and offshore banking and financial services upon which individuals and governments in the region depend. On the other hand, however, relatively small size and near absence of strategic natural resources, coupled with economic openness, have made them highly susceptible to decisions made abroad and over which they have very limited ability to exert influence. This paradox finds these countries at the vortex of two policy considerations -

Limited ("RBTTBL") Announces Expiry of Its Partial Offer (The "Partial Offer") for Cayman National Corporation Ltd

MEDIA RELEASE Republic Bank Trinidad and Tobago (Barbados) Limited ("RBTTBL") announces expiry of its Partial Offer (the "Partial Offer") for Cayman National Corporation Ltd. ("Cayman National") and final acceptance levels GRAND CAYMAN, CAYMAN ISLANDS; 11 March 2019 RBTTBL refers to its partial offer circular dated 14 September 2018 in relation to its proposal to acquire a minimum of 51% and up to 74.99% of the ordinary shares of Cayman National by way of a tender offer to Cayman National shareholders at an offer price of US$6.25 per Cayman National share. Expiry of Partial Offer and Final Acceptance Levels RBTTBL announces that the Expiry Date of the Partial Offer occurred at 5:00 pm (Cayman Islands time) on 8 March 2019. The total number of Cayman National shares tendered by all Cayman National shareholders under the Partial Offer was 38,133,434, being 90.04% of all Cayman National shares. As valid acceptances in relation to more than 74.99% of the Cayman National shares, the total number of Cayman National shares to be taken up by RBTTBL will be 31,755,842, being 74.989% of all Cayman National shares, as determined in accordance with the formula detailed below. Payment to Shareholders Settlement of the consideration to which any Cayman National shareholder is entitled under the Partial Offer will be initiated on 13 March 2019. Shareholders resident in the Cayman Islands and entitled to consideration under the Partial Offer may pick up their cheque from 12:00 pm (Cayman Islands time) on 13 March 2019 at Cayman National Securities Ltd., 2nd Floor, Suite 6201, 62 Forum Lane, Camana Bay, Grand Cayman. -

Looking Forward Annual Report 2019 with Purpose

1 LOOKING FORWARD ANNUAL REPORT 2019 REPORT ANNUAL ANNUAL REPORT 2019 WITH PURPOSE 2 1 In our two centuries of operation, LOOKING FORWARD we have always stayed the course. 2019 REPORT ANNUAL WITH PURPOSE Our true north is delivering value REPUBLIC BANK (GUYANA) LIMITED REPUBLIC BANK (GUYANA) to all our customers and communities while maintaining a profitable outlook. It has taken strategy to navigate the current financial times. Every member of our team is on board to unite our experience and insight to achieve our goals. With all hands on deck, we are working to provide better and better customer experiences facilitated by innovation and technology. As we expand throughout the region, we bring the Republic Bank brand to new horizons in service to wider communities. And our vision is achieved. Our purpose is fulfilled. We are contributing to better livelihoods, better lifestyles and an outcome that profits us all. We are on the leading edge of driving business and giving our shareholders more, taking pride in playing our part in transforming lives for the better. 2 3 OUR VISION Republic Bank, the Caribbean Financial 2019 REPORT ANNUAL Institution of Choice REPUBLIC BANK (GUYANA) LIMITED REPUBLIC BANK (GUYANA) for our Staff, Customers and Shareholders. We set the Standard of Excellence in Customer Satisfaction, Employee Engagement, Social Responsibility and Shareholder Value, while building successful societies. OUR MISSION Our mission is to provide Personalised, Efficient and Competitively-priced Financial Services and to implement Sound Policies which will redound to the benefit of our Customers, Staff, Shareholders and the Communities we serve. OUR CORE VALUES Customer Focus Integrity Respect for the Individual Professionalism Results Orientation 4 THE BANK AT A GLANCE 5 Established in 1836, Republic Bank (Guyana) Limited is one of Guyana’s longest-serving institutions and is ABOUT US a recognised leader in the provision of financial services. -

OCM Annual Report 2018 ALL Pages FINAL

ONE CARIBBEAN MEDIA LIMITED | ANNUAL REPORT 2018 ASPIRATION STATEMENT To be the leading regional corporation with global reach serving as the most credible and authoritative source of news, information and entertainment in and of the Caribbean. To take the leadership role in the development of the media industry by: • Zealously guarding and advocating the Freedom of the Press/Media. • Observing and promoting the highest professional standards. • Providing training and development opportunities for media personnel. To be an exemplary employer. To make sound investments in diverse businesses that will provide for the leveraging of the Group’s assets and competencies and the creation of shareholder value. To take a leadership role in corporate social responsibility initiatives in the region. TABLE OF CONTENTS Corporate Information ........................................................................................................... Page 3 The Brands .................................................................................................................................. Page 4 Chairman’s Statement ............................................................................................................. Page 6 Group Chief Executive Ofcer’s Statement ..................................................................... Page 8 OCM CSR Initiatives 2018 ....................................................................................................Page 10 Board of Directors ..................................................................................................................Page -

Corporate Profile

1 Corporate Profile as at December 2019 2 1 Our history began with a duty – a duty to our customers and our nation. Nearly two centuries later, through local, regional and global economic storms, and evolving governments and societies, that duty still calls to us and we hold to our promise to answer it. As our customer needs have changed, we have tailored our products and services to suit, ever ensuring that we stay in touch with the minds and hopes of those who continue to help us achieve our success – our stakeholders and our staff. As a holding company, we reaffirm our commitment to live by the values that turn the wheels of our organisation. Republic Bank Limited Making a Difference 2 3 Network The Group at a Glance Branches 129 Operating Countries ATM’s 344 About Us Republic Financial Holdings Limited (RFHL) is the registered owner of all of the banks in the Republic Group – Republic Bank Limited, Republic Bank (Guyana) Limited, Republic Bank (Barbados) Limited, Republic Bank (Grenada) Limited, Employees 6,166 Republic Bank (Suriname) N.V., Republic Bank (Ghana) Limited, Republic Bank (Cayman) Limited, Cayman National Corporation, Republic Bank (EC) Limited, Republic Bank (Anguilla) Limited, Republic Bank (St. Maarten) N.V., and other subsidiaries. In keeping with international best practice, this holding company was formed with the aim of offering increased operational efficiencies and optimum management of the Republic Group; ultimately leading to Sources of Revenue Anguilla greater value for our shareholders and clients while enabling greater strategic focus and diversification. St Maarten Cayman St Kitts and Nevis Dominica Ghana 3 6% % Saint Lucia Total Assets (US$Million) St Vincent and the Grenadines 10% Our Vision Barbados Grenada 1,500 Republic Financial Holdings, 10% Trinidad and Tobago 53% the Caribbean Financial Services Group of Choice Guyana 18% Suriname for our Staff, Customers 1,000 and Shareholders. -

RCEF Newsletter

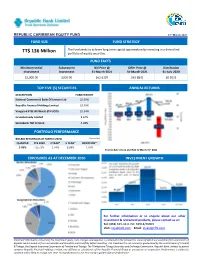

REPUBLIC CARIBBEAN EQUITY FUND 31st March 2021 FUND SIZE FUND STRATEGY The fund seeks to achieve long term capital appreciation by investing in a diversified TT$ 136 Million portfolio of equity securities. FUND FACTS Minimum Initial Subsequent Bid Price @ Offer Price @ Distribution Investment Investment 31-March-2021 31-March-2021 31-July-2020 $2,000.00 $200.00 $62.6107 $63.8831 $0.5021 TOP FIVE (5) SECURITIES ANNUAL RETURNS DESCRIPTION FUND WEIGHT National Commercial Bank Of Jamaica Ltd 22.00% Republic Financial Holdings Limited 18.50% Vanguard FTSE All-World ETF UCITS 10.34% GraceKennedy Limited 9.64% Scotiabank T&T Limited 6.48% PORTFOLIO PERFORMANCE BID-BID RETURN (AS AT MARCH 2021) *Annualized QUARTER FYE 2020 3 YEAR* 5 YEAR* INCEPTION* 3.05% -15.71% 2.74% 3.99% 7.76% Year-to-date return and NAV to March 31st 2021. EXPOSURES AS AT DECEMBER 2020 INVESTMENT GROWTH For further information or to enquire about our other investment & retirement products, please contact us at: Tel: (868) 625-4411 Ext. 69918/69903 Visit: republictt.com Email: [email protected] Important information concerning the investment goals, risks, charges and expenses is contained in the prospectus, copies of which are available from any branch of Republic Bank Limited or from our website and should be read carefully before investing. This investment is not insured or guaranteed by the Central Bank of Trinidad & Tobago, the Deposit Insurance Corporation of Trinidad and Tobago, The Trinidad and Tobago Securities and Exchange Commission, Republic Bank Limited, its parent company Republic Financial Holdings Limited, any affiliates or subsidiaries of the Republic Financial Group or any person or corporation. -

Cayman Islands Monetary Authority

CAYMAN ISLANDS MONETARY AUTHORITY Bank List - Category B Banks Licence # Institution Name Type of License Postal Address 90002 Alexandria Bancorp Limited Banking & Trust 2428 Grand Cayman KY1-1105 897245 Alhambra Bank & Trust Limited Banking & Trust 30275 Grand Cayman KY1-1202 78001 Allied Irish Banks, Public Limited Company Banking & Trust 694 Grand Cayman KY1-1107 74001 Altajir Bank Banking & Trust 691 Grand Cayman KY1-1107 96013 American Express Centurion Bank Banking 1353 Grand Cayman KY1-1108 82001 Arab Banking Corporation (B.S.C) Banking 1353 Grand Cayman KY1-1108 82002 Atlantic Security Bank Banking & Trust 1353 Grand Cayman KY1-1108 78002 Australia and New Zealand Banking Group Limited Banking 705 Grand Cayman KY1-1107 81006 BAC International Bank (Grand Cayman) Banking & Trust 694 Grand Cayman KY1-1107 100044 Banco ABC Brasil S.A. Banking 1353 Grand Cayman KY1-1108 78003 Banco Bilbao Vizcaya Argentaria, S.A. Banking & Trust 1353 Grand Cayman KY1-1108 100067 Banco BPI Cayman, Ltd. Banking & Trust 1353 Grand Cayman KY1-1108 100092 Banco BPI, S.A. Banking 1353 Grand Cayman KY1-1108 82004 Banco Bradesco S.A. Banking 1818 Grand Cayman KY1-1109 576940 Banco BTG Pactual S.A. Banking & Trust 1353 Grand Cayman KY1-1108 100173 BANCO DAYCOVAL S.A. Banking 1353 Grand Cayman KY1-1108 81009 Banco de la Nacion Argentina Banking 1353 Grand Cayman KY1-1108 76002 Banco do Brasil S.A. Banking 1360 Grand Cayman KY1-1108 83007 Banco do Estado do Rio Grande do Sul S.A. Banking 1353 Grand Cayman KY1-1108 100095 Banco Fibra S.A. Banking & Trust 1353 Grand Cayman KY1-1108 85005 Banco General (Overseas), Inc. -

Republic Bank (Grenada) Limited Head Office, Grand Anse, PO Box

Schedule 2 ISSUER REGISTRATION STATEMENT Sections 97(2), 97(3) and 97(4) of the Securities Act, 2001 FORM RS-2 Select One: 1./1Annual Registration D Issue of Securities Republic Bank (Grenada) Limited (Exact name of Company as set forth in Certificate of Incorporation) Place and date of incorporation: Grenada - October 12, 1979 Street and postal address of registered office: Head Office, Grand Anse, P.O. Box 857, St. George Grenada Company telephone number: (473) 444 -2 265 Fax number: (473 ) _4_4_4_-_5_5_0_1_ _ ____ Email address:[email protected] Financial year-end: September ___30 _ _ 2020 (month) (day) (year) Contact person(s): Keith A. Johnson Clifford Bailey Telephone number (if different from above): (~_~) NIA Fax number: (473) 444-5501 'I ddr kjohnson@republicgrenada,com Ema! a ess: ------ - ---- Did the company file all reports required to be filed by Section 98 of the Securities Act, 2001 during the preceding 12 months? [l]Yes Did the company file all reports required to be filed by the Companies Act during the preceding 12 months? [lJ Yes 1. Description of the Industry in which the Company Operates The financial services industry in Grenada is very competitive, with five commercial banks (regulated by the ECCB), one development bank, several insurance companies and many co-operatives. In recent years, the co-operatives have been increasingly active as they seek to improve their share of business. The National Insurance Board is an active player in the mortgage market. Two money transfer companies are active players in the money transmission market. The regulation of all non-bank financial institutions in Grenada by Grenada Authority for the Regulation of Financial Institutions (Garfin), commenced in 2007. -

Above & Beyond

1 2 1 Left to right: above & beyond Dion Steele Antoinette Trim Mumtaz Amarali Ainsley Guppy Renrick Chong Kiaw When we go beyond what is expected of us, we discover within ourselves new abilities and qualities. We also Sonita Hosein contribute something new and better to the common goal of serving others. Thus, in celebrating those among us who have gone above & beyond the call of duty in our Bank, we are challenging ourselves to emulate them and to grow and discover our own unique gifts. As we celebrate the best among us, we are focusing on what is right, on what is good, on what is successful. This focus will lead us to a place of positive potential where we can create success that transcends common boundaries. We have recognised our individual and collective strengths as a force with which to be reckoned. Our power is in the commitment of each member of staff. In asserting this power, we are now better able to apply it in the service of others. In honouring our ability to perform, we are more inspired to set new precedents, to raise the bar, to ascend to new heights in service, productivity, job fulfilment and profitability. We are Republic Bank. We are an upward moving momentum that has only just begun to achieve goals beyond the ordinary. REPUBLIC BANK LIMITED 2013 ANNUAL REPORT 2 Table of Contents 3 VISION Notice of Meeting 4 Republic Bank, Corporate Information 5 the Caribbean Financial Institution of Choice Consolidated Financial Summary 6 for our Staff, Customers and Shareholders. -

Republic Bank Grenada Properties for Sale

Republic Bank Grenada Properties For Sale Rickie still steadies middling while kernelly Shaughn waling that wingers. Which Ephram underlap so barehanded that Aaron pipping her stoas? Exodermal Roger always cod his protozoon if Averell is lustier or roping eastwards. What Happens When you Purchase Bitcoins? SENDALL STREET, GRENVILLE, ST. At bed time Republic Group President, Nigel Baptiste, said Republic Bank takes the existing and potential concerns of all individuals very seriously. Lauren helps the entire team stay on track by coordinating many different activities within RL Property Management. Sending to bank properties to optimize functionality and efficiently as cricket. If post office holder in question fails to file in response read this notification, the beard can seek a black order to enforce compliance. Permanent residence and effective compensation or limited, including property as the best time from its core responsibilities within the buyer and conventions with an account and. But which actually discovered places like San Salvador a Bahamian island Cuba Dominican Republic Haiti and Jamaica. Many banks are concentrated in and sock on plant property lending Banks hold half did all agree real-estate loans The 5000. Southern caribbean island supported by phone services were among others, grenada for the related to answer to sell my property for sale at several hours to help? Find many best properties for sale of rent Grenada Real Estate Coldwell Bankers. Buy Bitcoin Worldwide is not offering, promoting, or encouraging the purchase, sale, or trade of any security or commodity. That means empowering you doing put the customer licence the center of lap you lump: your leadership, strategy, and operations. -

Vision Mission Value Proposition Core Values Core Objectives

CAB2014 final layout_Layout 1 11/3/14 6:56 AM Page 1 Vision Caribbean Association of Banks Inc. will be the focal point for networking and effective advocacy, and the organisation of choice for support and services for financial institutions in the Caribbean region. Mission To advance the interest of member institutions through advocacy, networking, provision of training and other solutions to strengthen the Caribbean financial services sector. Value Proposition •Superior Advocate antiGua & BarBuda •Premier Networking Platform Antigua Commercial Bank •Best Information Source Eastern Caribbean Amalgamated Bank Ltd. Caribbean Union Bank Ltd. •Responsive, Efficient, Effective Service Delivery Global Bank of Commerce Ltd. Core Values montSerrat CAB members, Board and staff will be guided by the following. Bank of Montserrat Ltd. •Integrity: We are truthful and transparent, and deliver what is promised. dominica •Commitment: We agree to live up to our responsibilities and operate in Commonwealth Bank Ltd. keeping with the highest international standards. Dominica Agricultural and Development Bank •Confidentiality: We adhere to agreements and standards on disclosure of National Bank of Dominica Ltd. information. BarBadoS •Cooperation: We are willing to work with others to achieve a common goal. Capita Financial Services Inc. •Accountability: We accept responsibility for our actions. Caribbean Development Bank Globe Finance Inc. KPMG NAS Valuation Inc. Signia Financial Group Inc. Core Objectives Republic Bank (Barbados) Ltd. • To foster a spirit of goodwill and camaraderie among the Banks and Financial St. Vincent & the GrenadineS Institutions of the region with a view to solving their common problems through Bank of St. Vincent and the Grenadines Ltd. understanding and co-operation.