Comprehensive Annual Financial Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Central District Athletic Board Membership History 1926

Central District Athletic Board Membership History 1926 to 2019 Compiled by: Galen Kyre, Secretary (1974-2011) Doug Ute, Secretary (2011-Present) Central District Athletic Board Membership History The information contained herein of past membership on the Central District Athletic Board was gathered from District Board minutes, Central District Basketball Programs, and from publications stored in the Ohio High School Athletic Association Library. While care has been taken to insure that the information is correct, there may be errors and omissions. Should the reader find errors, omissions, or any other incorrect data, it would be appreciated if a contact would be made with Doug Ute, Secretary, Central District Athletic Board. Membership Trivia MOST YEARS ON THE STATE BOARD OF CONTROL 8 Years – B.A. Meiser – Superintendent, Canal Winchester 8 Years – D. O. Davis, Superintendent, Fairfield County Schools FIRST STATE BOARD OF CONTROL MEMBER H. P. Swain, Principal, Columbus City Schools 1926 to 27 FIRST CENTRAL DISTRICT ATHLETIC BOARD (ON RECORD) 1926 – H. P. Swain, Principal, Columbus, State Board Member, W.A. Kline, Principal, Westerville, L. B. Brown, Superintendent, Prospect FIRST FEMALE TO SERVE ON A DISTRICT ATHLETIC BOARD AND SERVE ON THE STATE BOARD OF CONTROL BARBARA HARRISON – Canal Winchester High School, elected to the Central District Board in 1985 and to the State Board of Control in 1993 FIRST PERSON ELECTED TO THE GENDER REPRESENTATIVE POSITION Beth Hill – Newark Catholic High School, 2007 FIRST PERSON ELECTED TO THE ETHNIC MINORITY REPRESENTATIVE POSITION Keith Bell – Westerville City Schools, 2007 FIRST PERSON ELECTED TO THE 7TH/8TH GRADE REPRESENTATIVE POSITION Chuck Byers – Ridgeview Jr. -

Big Walnut Local School District Delaware County

BIG WALNUT LOCAL SCHOOL DISTRICT DELAWARE COUNTY SINGLE AUDIT FOR THE YEAR ENDED JUNE 30, 2020 BIG WALNUT LOCAL SCHOOL DISTRICT DELAWARE COUNTY JUNE 30, 2020 TABLE OF CONTENTS TITLE PAGE Prepared by Management: Schedule of Expenditures of Federal Awards ....................................................................................... 1 Notes to the Schedule of Expenditures of Federal Awards ................................................................... 2 Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Required by Government Auditing Standards ........................................................................................... 3 Independent Auditor’s Report on Compliance with Requirements Applicable to the Major Federal Program and on Internal Control Over Compliance Required by the Uniform Guidance ....................................................................................... 5 Schedule of Findings ..................................................................................................................................... 9 Attachment: Comprehensive Annual Financial Report (CAFR) THIS PAGE INTENTIONALLY LEFT BLANK BIG WALNUT LOCAL SCHOOL DISTRICT DELAWARE COUNTY SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS FOR THE YEAR ENDED JUNE 30, 2020 FEDERAL GRANTOR Federal Pass Through Pass Through Grantor CFDA Entity Identifying Total Federal Program / Cluster Title Number Number Expenditures U.S. DEPARTMENT OF AGRICULTURE Passed Through Ohio Department -

Delawar Count

of Delawar Count Snap 2017 SHJanuary 25, 2018 TS 2 Thursday, January 25, 2018 Snapshot of Delawar Count 2017 The Delaware Gazette • The Sunbury News Photo Credit | D. Anthony Botkin Photo Credit | D. Anthony Botkin Delaware County dispatcher Catharine Dobyns assisted a father in delivering his baby girl by giving Retail giant IKEA opened its Columbus location in June 2017 at the junction of Interstate 71 and instructions over the phone in January 2017. Dobyns was honored as a recipient of the Stork Award, Gemini Place in Delaware County. The 354,000-square foot facility is the 44th store the Swedish which is given to dispatchers who provide assistance in the delivery of infants via phone. Dobyns was company has opened in the United States. IKEA Columbus employs approximately 325 people. The given a lapel pin of a stork and her name was be added to a plaque with the other recipients of the store features 10,000 exclusively-designed items, a 450-seat restaurant, 41 inspirational room award. The plaque is displayed on the first floor of the county commissioners’ office on Sandusky settings, three model home interiors, and a supervised children’s play area. Street. Photo Credit | D. Anthony Botkin FACES The 91-degree summer weather didn’t keep families from walking down William Street to the 2017 St. Mary Festival last June. The heat didn’t seem to bother either Isabella Cook, left, or Skyler Hatten, right, as they took a spin on a and crocodile’s back. Sunbury area residents gathered on Memorial PLACES Day 2017 to pay tribute to the men and women who have given their Photo Credit | Anthony Conchel lives in military to Memorial Day 2017 services were held at Oak Grove Cemetery in Delaware paying the United States. -

Big Walnut Local School District

BIG WALNUT LOCAL SCHOOL DISTRICT DELAWARE COUNTY SINGLE AUDIT JULY 1, 2013 - JUNE 30, 2014 Board of Education Big Walnut Local School District 105 Baughman Street, Suite A Sunbury, Ohio 43074 We have reviewed the Independent Auditor’s Report of the Big Walnut Local School District, Delaware County, prepared by Wilson, Shannon & Snow, Inc., for the audit period June 30, 2013 through July 1, 2014. Based upon this review, we have accepted these reports in lieu of the audit required by Section 117.11, Revised Code. The Auditor of State did not audit the accompanying financial statements and, accordingly, we are unable to express, and do not express an opinion on them. Our review was made in reference to the applicable sections of legislative criteria, as reflected by the Ohio Constitution, and the Revised Code, policies, procedures and guidelines of the Auditor of State, regulations and grant requirements. The Big Walnut Local School District is responsible for compliance with these laws and regulations. Dave Yost Auditor of State January 5, 2015 88 East Broad Street, Fifth Floor, Columbus, Ohio 43215‐3506 Phone: 614‐466‐4514 or 800‐282‐0370 Fax: 614‐466‐4490 www.ohioauditor.gov This page intentionally left blank. BIG WALNUT LOCAL SCHOOL DISTRICT DELAWARE COUNTY TABLE OF CONTENTS TITLE PAGE SCHEDULE OF FEDERAL AWARDS RECEIPTS AND EXPENDITURES 1 NOTES TO THE SCHEDULE OF FEDERAL AWARDS RECEIPTS AND EXPENDITURES 2 INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS REQUIRED BY GOVERNMENT -

CCP Advisors by School

School CCP Advisor Email ACADEMY FOR URBAN SCHOLARS Diane Jones [email protected] ALTERNATIVE EDUCATION ACADEMY Diane Jones [email protected] AMANDA-CLEARCREEK HIGH SCHOOL Andrea Bennett [email protected] ARTS COLLEGE PREPARATORY ACADEMY Diane Jones [email protected] BEECHCROFT HIGH SCHOOL Nicole Martin [email protected] BELLEFONTAINE HIGH SCHOOL Jordan Falb [email protected] BENJAMIN LOGAN HIGH SCHOOL Jordan Falb [email protected] BERNE UNION HIGH SCHOOL Andrea Bennett [email protected] BEXLEY HIGH SCHOOL Diane Jones [email protected] BIG WALNUT HIGH SCHOOL Andrea Bennett [email protected] BISHOP HARTLEY HIGH SCHOOL Diane Jones [email protected] BISHOP READY HIGH SCHOOL Michelle Miller-Owens [email protected] BISHOP ROSECRANS HIGH SCHOOL Andrea Bennett [email protected] BISHOP WATTERSON HIGH SCHOOL Jordan Falb [email protected] BLOOM-CARROLL HIGH SCHOOL Diane Jones [email protected] BRIGGS SENIOR HIGH SCHOOL Nicole Martin [email protected] BROOKPARK MIDDLE SCHOOL (SWCSD) Nicole Martin [email protected] BROOKWOOD ACADEMY Diane Jones [email protected] BUCKEYE ONLINE SCHOOL FOR SUCCESS Andrea Bennett [email protected] BUCKEYE VALLEY HIGH SCHOOL Jordan Falb [email protected] C-TEC CAREER CENTER Andrea Bennett [email protected] CANAL WINCHESTER HIGH SCHOOL Michelle Miller-Owens [email protected] CENTENNIAL HIGH SCHOOL Nicole Martin [email protected] CENTERBURG HIGH SCHOOL Michelle Miller-Owens [email protected] CENTRAL HIGH SCHOOL Michelle Miller-Owens [email protected] CHARLES SCHOOL AT OHIO DOMINICAN UNIVERSITY Simonne Gage [email protected] CHRISTIFIDELES -

Ohiohealth Grady Memorial Hospital

OhioHealth Grady Memorial Hospital Community Health Needs Assessment June 2016 OhioHealth Grady Memorial Hospital Grady Memorial Hospital provides the Delaware community with comprehensive quality healthcare delivered with compassionate, personal care. Our full range of services and programs meet the needs of one of the nation’s most rapidly growing counties. Steve Bunyard, President OhioHealth Grady Memorial Hospital 561 West Central Avenue Delaware, Ohio 43015 Board approval of CHNA Report: 06/14/2016 Initial web posting of CHNA Report: 06/27/2016 Tax identification number: 31-4379436 OhioHealth Grady Memorial Hospital Table of Contents Introduction ....................................................................................................................................................................1 A. Definition of community served and how community was determined ........................................... 2 B. Process and methods used to conduct the Community Health Needs Assessment (CHNA) ......... 3 B1. Data and other information used in the assessment ........................................................................... 3 B2. Methods of collecting and analyzing data and information ........................................................... 3 B3. Parties with whom hospital collaborated or contracted for assistance ....................................... 4 C. Input from persons who represent the broad interests of the community served .......................... 5 D. Description of significant health needs as -

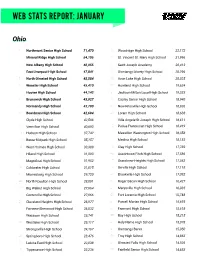

Web Stats Report: January

WEB STATS REPORT: JANUARY Ohio 1 Northmont Senior High School 71,470 31 Woodridge High School 22,172 2 Mineral Ridge High School 54,105 32 St. Vincent-St. Mary High School 21,996 3 New Albany High School 48,955 33 Saint Joseph Academy 20,413 4 East Liverpool High School 47,841 34 Olentangy Liberty High School 20,296 5 North Olmsted High School 45,584 35 Avon Lake High School 20,025 6 Wooster High School 45,410 36 Howland High School 19,634 7 Hoover High School 44,142 37 Jackson-Milton Local High School 19,333 8 Brunswick High School 43,927 38 Copley Senior High School 18,940 9 Normandy High School 43,780 39 New Knoxville High School 18,936 10 Boardman High School 42,694 40 Lorain High School 18,638 11 Clyde High School 42,506 41 Villa Angela-St Joseph High School 18,611 12 Vermilion High School 40,693 42 Padua Franciscan High School 18,419 13 Hudson High School 37,742 43 Massillon Washington High School 18,358 14 Berea-Midpark High School 35,157 44 Medina High School 18,183 15 West Holmes High School 33,389 45 Clay High School 17,782 16 Hiland High School 31,993 46 Austintown Fitch High School 17,586 17 Magnificat High School 31,952 47 Grandview Heights High School 17,562 18 Coldwater High School 31,815 48 Orrville High School 17,118 19 Miamisburg High School 29,720 49 Brookville High School 17,092 20 North Royalton High School 28,001 50 Roger Bacon High School 16,427 21 Big Walnut High School 27,664 51 Marysville High School 16,035 22 Centerville High School 27,066 52 Fort Loramie High School 15,748 23 Cleveland Heights High School 26,977 -

Fiscal Year 2018 Comprehensive Annual Financial Report

Comprehensive Annual Financial Report Board of Education Big Walnut Local School District Sunbury, Ohio For the Fiscal Year Ended June 30, 2018 This page intentionally left blank. Introduction This page intentionally left blank. BIG WALNUT LOCAL SCHOOL DISTRICT SUNBURY, OHIO COMPREHENSIVE ANNUAL FINANCIAL REPORT For The Fiscal Year Ended June 30, 2018 Prepared By: Treasurer’s Office Jeremy Buskirk, Treasurer i This Page Intentionally Left Blank ii BIG WALNUT LOCAL SCHOOL DISTRICT COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2018 TABLE OF CONTENTS INTRODUCTORY SECTION Title Page ............................................................................................................................................ i Table of Contents ............................................................................................................................... iii Letter of Transmittal ........................................................................................................................... vii Certificate of Achievement................................................................................................................. xii Organizational Chart .......................................................................................................................... xiii Big Walnut Local School District Principal Officials ........................................................................ xiv FINANCIAL SECTION Independent Auditor’s Report ........................................................................................................... -

Delaware County

EX. A.1 ~ October 24, 2018 Page 1 of 13 OLENTANGY LOCAL SCHOOL DISTRICT DELAWARE COUNTY Schedule of Revenue, Expenditures and Changes in Fund Balances for Fiscal Years ended June 30, 2016, 2017 and 2018 Forecasted Fiscal Years ending June 30, 2019 through 2023 Forecast Provided by Olentangy Local School District Treasurer’s Office Emily Hatfield, Treasurer/CFO October 24, 2018 EX. A.1 ~ October 24, 2018 Page 2 of 13 OLENTANGY LOCAL SCHOOL DISTRICT ‐ ‐ DELAWARE COUNTY Schedule Of Revenue, Expenditures and Changes In Fund Balances Actual and Forecasted Operating Fund ACTUAL FORECASTED Fiscal Year Fiscal Year Fiscal Year Fiscal Year Fiscal Year Fiscal Year Fiscal Year Fiscal Year 2016 2017 2018 2019 2020 2021 2022 2023 Revenue: 1.010 ‐ General Property Tax (Real Estate) 129,057,847 140,825,729 162,798,897 153,076,609 161,762,436 165,546,754 169,211,804 172,419,994 1.020 ‐ Public Utility Personal Property 6,894,709 9,133,832 10,980,009 11,394,404 11,625,031 11,857,532 12,094,683 12,337,607 1.030 ‐ Income Tax ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 1.035 ‐ Unrestricted Grants‐in‐Aid 11,525,017 11,477,555 12,542,496 12,965,570 13,708,400 14,318,583 14,964,231 15,638,165 1.040 ‐ Restricted Grants‐in‐Aid 235,653 348,360 440,437 349,599 350,986 353,579 356,205 358,901 1.045 ‐ Restricted Federal Grants‐in‐Aid ‐ SFSF ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ 1.050 ‐ Property Tax Allocation 16,510,061 16,984,415 17,552,496 17,798,736 18,154,068 18,567,156 18,985,321 19,350,371 1.060 ‐ All Other Operating Revenues 22,199,319 24,973,953 26,194,423 29,280,657 28,126,548 27,910,313 27,940,805 27,974,611 -

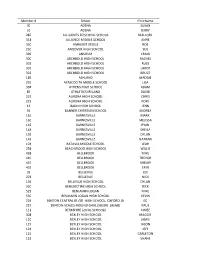

CLINIC ONLY for WEBSITE.Xlsx

Member # School First Name 30 ADENA SUSAN 31 ADENA JERRY 287 ALL SAINTS EPISCOPAL SCHOOL MALLORY 318 ALLIANCE MIDDLE SCHOOL ANNE 330 AMHERST STEELE ROB 250 ANDOVER HIGH SCHOOL SUE 399 ANSONIA CRAIG 300 ARCHBOLD HIGH SCHOOL RACHEL 303 ARCHBOLD HIGH SCHOOL RUSS 301 ARCHBOLD HIGH SCHOOL LAROY 302 ARCHBOLD HIGH SCHOOL BRUCE 189 ASHLAND MADGIE 291 ATASCOCITA MIDDLE SCHOOL LISA 394 ATHENS HIGH SCHOOL ADAM 85 ATHLETICS IRELAND DAVID 222 AURORA HIGH SCHOOL CHRIS 223 AURORA HIGH SCHOOL KORY 13 BADIN HIGH SCHOOL JENN 92 BANNER CHRISTIAN SCHOOL ANDREA 161 BARNESVILLE MARK 160 BARNESVILLE MELISSA 162 BARNESVILLE RYAN 144 BARNESVILLE SHEILA 159 BARNESVILLE DYLAN 143 BARNESVILLE NATHAN 104 BATAVIA MIDDLE SCHOOL LEAH 258 BEACHWOOD HIGH SCHOOL WILLIE 438 BELLBROOK MIKE 440 BELLBROOK TREVOR 437 BELLBROOK SHELBY 439 BELLBROOK ERIN 39 BELLEVUE LEE 278 BELLEVUE NICK 136 BELLEVUE HIGH SCHOOL DYLAN 360 BENEDICTINE HIGH SCHOOL RICK 529 BENJAMIN LOGAN MIKE 530 BENJAMIN LOGAN HIGH SCHOOL KEVIN 234 BENTON CENTRAL JR./SR. HIGH SCHOOL, OXFORD, IN ED 227 BENTON-SCALES MOUND-SHULLSBURG (BSMS) PAUL 112 BERKSHIRE LOCAL SCHOOLS AIMEE 308 BEXLEY HIGH SCHOOL MAGGIE 120 BEXLEY HIGH SCHOOL JAMIE 127 BEXLEY HIGH SCHOOL JASON 124 BEXLEY HIGH SCHOOL JEFF 121 BEXLEY HIGH SCHOOL CARLETON 122 BEXLEY HIGH SCHOOL SHANE 123 BEXLEY HIGH SCHOOL DANIEL 128 BEXLEY MIDDLE SCHOOL KIM 125 BEXLEY MIDDLE SCHOOL MICHAEL 126 BEXLEY MIDDLE SCHOOL DUSTIN 513 BIG WALNUT HIGH SCHOOL RYAN 497 BISHOP FENWICK CATHOLIC HIGH SCHOOL CHRIS 384 BISHOP HARTLEY CARL 418 BISHOP HARTLEY KIRA 387 BISHOP HARTLEY -

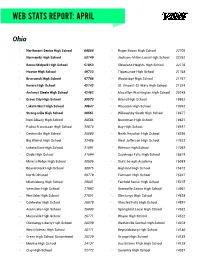

Web Stats Report: April

WEB STATS REPORT: APRIL Ohio 1 Northmont Senior High School 64084 31 Roger Bacon High School 22705 2 Normandy High School 53749 32 Jackson-Milton Local High School 22262 3 Berea-Midpark High School 51853 33 Cleveland Heights High School 22176 4 Hoover High School 49723 34 Tippecanoe High School 21768 5 Brunswick High School 47786 35 Woodridge High School 21747 6 Revere High School 42742 36 St. Vincent-St. Mary High School 21324 7 Amherst Steele High School 42462 37 Massillon Washington High School 20248 8 Grove City High School 39073 38 Hiland High School 19582 9 Lakota West High School 38647 39 Wauseon High School 19342 10 Strongsville High School 38561 40 Willoughby South High School 18677 11 New Albany High School 36506 41 Boardman High School 18631 12 Padua Franciscan High School 35874 42 Bay High School 18557 13 Centerville High School 35080 43 North Royalton High School 18295 14 Big Walnut High School 33406 44 West Jefferson High School 17623 15 Lakota East High School 31891 45 Rittman High School 17063 16 Clyde High School 31594 46 Cuyahoga Falls High School 16874 17 Mineral Ridge High School 30505 47 Saint Joseph Academy 16083 18 Beavercreek High School 30075 48 Highland High School 15672 19 North Olmsted 29779 49 Fairmont High School 15327 20 Miamisburg High School 29641 50 Fairfield Senior High School 15275 21 Vermilion High School 27992 51 Greenville Senior High School 14967 22 Westlake High School 27851 52 Olentangy High School 14828 23 Coldwater High School 26879 53 Olmsted Falls High School 14597 24 Avon Lake High School -

Ohio Contract User List 2016-2017

Ohio Contract Usage 2016-2017 MHEC CONTRACTS leverage the potential volume of the region’s purchasing power, while saving entities time and money by simplifying the procurement process and negating the need to conduct a competitive sourcing event. By offering a turnkey solution with the ability to tailor the already negotiated contract to match the entity’s specific needs and2 requirements,0162017 MHEC contracts shift some of the negotiating power back to the entities. Additionally, because of MHEC’s statutory status, many of these contracts can also be adopted for use by K-12 districts and schools, as well as cities, states and local governments. Smaller institutions benefit from these contracts as they allow these institutions to receive some pricing and terms normally reserved for larger institutions. Committee members participate in the negotiations, sharing strategies, and tactics on dealing with specific contractual issues and vendors. ANNUAL HARDWARE CONTRACTS Tiffin University Bridgeport Exempted Village Cuyahoga Valley Christian School District Academy Higher Education Union Institute and University REPORT Bristol Local School District Dover City School District Antioch University University of Cincinnati Brookville Local School East Palestine City School Ashland University University of Dayton to the Member States District District Bluffton University University of Findlay Brown Local School District Eaton Community Schools Capital University University of Mount Union Buckeye Joint Vocational Fenwick High School Case Western Reserve University of Rio Grande School Field Local Schools University University of Toledo Canfield Local School District Franklin Local School District Cedarville University Walsh University Centerville City Schools Fuchs Mizrachi School Cleveland State University Zane State College Central Junior High School Gallia-Jackson-Vinton Joint College of Wooster Central Primary School Village School District God’s Bible School and HARDWARE CONTRACTS Child Focus, Inc.