Federal Register/Vol. 85, No. 202/Monday, October 19, 2020/Rules and Regulations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Early Dance Division Calendar 17-18

Early Dance Division 2017-2018 Session 1 September 9 – November 3 Monday Classes Tuesday Classes September 11 Class September 12 Class September 18 Class September 19 Class September 25 Class September 26 Class October 2 Class October 3 Class October 9 Class October 10 Class October 16 Class October 17 Class October 23 Class October 24 Class October 30 Last Class October 31 Last Class Wednesday Classes Thursday Classes September 13 Class September 14 Class September 20 Class September 21* Class September 27 Class September 28 Class October 4 Class October 5 Class October 11 Class October 12 Class October 18 Class October 19 Class October 25 Class October 26 Class November 1 Last Class November 2 Last Class Saturday Classes Sunday Classes September 9 Class September 10 Class September 16 Class September 17 Class September 23 Class September 24 Class September 30* Class October 1 Class October 7 Class October 8 Class October 14 Class October 15 Class October 21 Class October 22 Class October 28 Last Class October 29 Last Class *Absences due to the holiday will be granted an additional make-up class. Early Dance Division 2017-2018 Session 2 November 4 – January 22 Monday Classes Tuesday Classes November 6 Class November 7 Class November 13 Class November 14 Class November 20 No Class November 21 No Class November 27 Class November 28 Class December 4 Class December 5 Class December 11 Class December 12 Class December 18 Class December 19 Class December 25 No Class December 26 No Class January 1 No Class January 2 No Class January 8 Class -

2021 7 Day Working Days Calendar

2021 7 Day Working Days Calendar The Working Day Calendar is used to compute the estimated completion date of a contract. To use the calendar, find the start date of the contract, add the working days to the number of the calendar date (a number from 1 to 1000), and subtract 1, find that calculated number in the calendar and that will be the completion date of the contract Date Number of the Calendar Date Friday, January 1, 2021 133 Saturday, January 2, 2021 134 Sunday, January 3, 2021 135 Monday, January 4, 2021 136 Tuesday, January 5, 2021 137 Wednesday, January 6, 2021 138 Thursday, January 7, 2021 139 Friday, January 8, 2021 140 Saturday, January 9, 2021 141 Sunday, January 10, 2021 142 Monday, January 11, 2021 143 Tuesday, January 12, 2021 144 Wednesday, January 13, 2021 145 Thursday, January 14, 2021 146 Friday, January 15, 2021 147 Saturday, January 16, 2021 148 Sunday, January 17, 2021 149 Monday, January 18, 2021 150 Tuesday, January 19, 2021 151 Wednesday, January 20, 2021 152 Thursday, January 21, 2021 153 Friday, January 22, 2021 154 Saturday, January 23, 2021 155 Sunday, January 24, 2021 156 Monday, January 25, 2021 157 Tuesday, January 26, 2021 158 Wednesday, January 27, 2021 159 Thursday, January 28, 2021 160 Friday, January 29, 2021 161 Saturday, January 30, 2021 162 Sunday, January 31, 2021 163 Monday, February 1, 2021 164 Tuesday, February 2, 2021 165 Wednesday, February 3, 2021 166 Thursday, February 4, 2021 167 Date Number of the Calendar Date Friday, February 5, 2021 168 Saturday, February 6, 2021 169 Sunday, February -

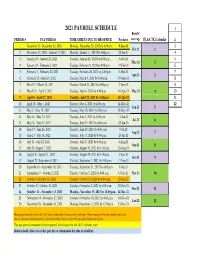

Payroll Calendar 2021

2021 PAYROLL SCHEDULE 1 Benefit PERIOD # PAY PERIOD TIME SHEETS DUE TO HR OFFICE Paydates coverage FLSA 7K Calendar 2 1 December 13- December 26, 2020 Monday, December 28, 2020 by 4:00 p.m. 8-Jan-21 3 Feb-21 1 2 December 27, 2020 - Janurary 9, 2021 Monday, January 11, 2021 by 4:00 p.m. 22-Jan-21 4 3 January 10 - January 23, 2021 Tuesday, January 26, 2021 by 4:00 p.m. 5-Feb-21 5 Mar-21 2 4 January 24 - February 6, 2021 Tuesday, February 9, 2021 by 4:00 p.m. 19-Feb-21 6 5 February 7 - February 20, 2021 Tuesday, February 26, 2021 by 4:00 p.m. 5-Mar-21 7 Apr-21 3 6 February 21 - March 6, 2021 Tuesday, March 9, 2021 by 4:00 p.m. 19-Mar-21 8 7 March 7 - March 20, 2021 Tuesday, March 23, 2021 by 4:00 p.m. 2-Apr-21 9 8 March 21 - April 3, 2021 Tuesday, April 6, 2021 by 4:00 p.m. 16-Apr-21 May-21 4 10 9 April 4 - April 17, 2021 Tuesday, April 20, 2021 by 4:00 p.m. 30-Apr-21 11 10 April 18 - May 1, 2021 Tuesday, May 4, 2021 by 4:00 p.m. 14-May-21 12 Jun-21 5 11 May 2 - May 15, 2021 Tuesday, May 18, 2021 by 4:00 p.m. 28-May-21 12 May 16 - May 29, 2021 Tuesday, June 1, 2021 by 4:00 p.m. 11-Jun-21 Jul-21 6 13 May 30 - June 12, 2021 Tuesday, June 15, 2021 by 4:00 p.m. -

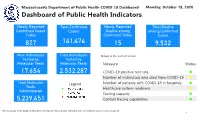

COVID-19 Dashboard- Monday, October 19, 2020 Dashboard of Public Health Indicators

10/19/2020 Public Health Indicators Massachusetts Department of Public Health COVID-19 Dashboard- Monday, October 19, 2020 Dashboard of Public Health Indicators Newly Reported Total Confirmed Newly Reported Total Deaths Confirmed Cases Cases Deaths among among Confirmed Today Confirmed Today Cases 827 141,474 15 9,532 New Individuals Total Individuals Below is the current status: Tested by Tested by Molecular Tests Molecular Tests Measure Status 17,654 2,532,287 COVID-19 positive test rate ⚫ Number of individuals who died from COVID-19 ⚫ Total Molecular Legend Number of patients with COVID-19 in hospitals ⚫ Tests Healthcare system readiness ⚫ Administered Testing capacity ⚫ 5,239,651 Contact tracing capabilities ⚫ The front page of the dashboard has been reformatted. Antibody tests (individual and total numbers) can be found on page 18. 1 1/1 10/19/2020 Public Health Indicators2 Massachusetts Department of Public Health COVID-19 Dashboard- Monday, October 19, 2020 Percent or Count of Change Since Dashboard of Public Health Indicators Lowest Observed Value (LOV) 1.4% 7 Day Weighted 1.2% 1.2% 1.2% 1.1% 1.1% 1.1% 1.1% 1.2% 1.1% 1.1% 1.1% Average of Positive 1.2% 1.1% 1.3% 1.3% 1.2% 0.9% 1.0% 1.2% 1.3% 1.3% 1.2% 1.0% 0.9% 0.9% 1.1% 59 % Molecular Test Rate* 0.8% 0.8% 0.8% 0.8% 1.1% 0.8% 0.6% 0.8% 19 20 21 22 23 24 25 26 27 28 29 30 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 September October LOV =0.8% 3 Day Average of 494 498 500 499 Number of COVID- 500 468 439 442 514 514 423 433 432 425 505 509 505 505 505 505 494 19 Patients in 393 -

BILLING CYCLE SCHEDULE Department of Procurement, Disbursements & Contract Services 1135 Old Main 600 Lincoln Avenue Charleston, IL 61920

Eastern Illinois University BILLING CYCLE SCHEDULE Department of Procurement, Disbursements & Contract Services 1135 Old Main 600 Lincoln Avenue Charleston, IL 61920 Billing Cycle Beginning Date Billing Cycle Ending Date June 26, 2018 July 25, 2018 Tuesday Wednesday July 26, 2018 August 24, 2018 Thursday Friday August 26, 2018 September 25, 2018 Sunday Tuesday September 26, 2018 October 25, 2018 Wednesday Thursday October 26, 2018 November 26, 2018 Friday Monday November 27, 2018 December 26, 2018 Tuesday Wednesday December 27, 2018 January 25, 2019 Thursday Friday January 26, 2019 February 25, 2019 Saturday Monday February 26, 2019 March 25, 2019 Tuesday Monday March 26, 2019 April 25, 2019 Tuesday Thursday April 26, 2019 May 24, 2019 Friday Friday May 26, 2019 June 25, 2019 Sunday Tuesday June 26, 2019 July 25, 2019 Wednesday Thursday Revised 2/2/18 1 Transactions with a Post Date of: Must be Reviewed Upload to Banner & Approved by: July 1, 2018 – July 6, 2018 July 12, 2018 July 13, 2018 Thursday Friday July 7, 2018 – July 13, 2018 July 19, 2018 July 20, 2018 Thursday Friday July 14, 2018 – July 20, 2018 July 26, 2018 July 27, 2018 Thursday Friday July 21, 2018 – July 27, 2018 August 2, 2018 August 3, 2018 Thursday Friday July 28, 2018 – August 3, 2018 August 9, 2018 August 10, 2018 Thursday Friday August 4, 2018 – August 10, 2018 August 16, 2018 August 17, 2018 Thursday Friday August 11, 2018 – August 17, 2018 August 23, 2018 August 24, 2018 Thursday Friday August 18, 2018 – August 24, 2018 August 30, 2018 August 31, 2018 Thursday -

2020-2021 Academic Calendar Revised 9.18.20

FRANCISCAN UNIVERSITY OF STEUBENVILLE 2020-2021 ACADEMIC CALENDAR REVISED 9.18.20 FALL 2020 SEMESTER SPRING 2021 SEMESTER August 24 25-December 11 January 11-May 5 New Student Orientation August 20-23 (Thurs-Sun) January 7-10 (Thurs-Sun) Convocation & Opening of School Mass August 24 (Mon) (4 pm; 3 pm classes January 11 (Mon) (mass only, 10:30 am) shortened & 4:30 pm classes cancelled) Classes begin August 24 (Mon) January 11 (Mon) (10 a.m. classes shortened) Last day for late registration August 28 (Fri) January 15 (Fri) Last day for adding/dropping courses September 2 (Wed) January 20 (Wed) Labor Day (class day) September 7 (Mon) (class day) N/A March for Life N/A January 29 (no day classes) Last day for audit changes September 11 (Fri) January 22 (Fri) Incomplete grades due to registrar September 25 (Fri) February 12 (Fri) Feast of St. Francis October 4 (Sun) N/A Homecoming weekend October 2-4 (Fri-Sun) N/A Midterm deficiencies due to registrar October 14 (Wed) March 5 (Fri) Spring Break N/A March 8-12 (Mon-Fri) (classes resume Mon, March 15) Last day for course withdrawal November 2 (Mon) March 26 (Fri) Tentative Class Make-up Days November 14, 21 (Sat) Thanksgiving vacation November 25-29 (Wed-Sun) N/A (classes resume Mon, Nov 30) Holy Thursday April 1 (no evening classes) Easter recess (Friday & Monday day classes N/A April 2-April 5 (day) canceled; *Monday evening classes do meet) (classes resume Mon evening, April 5, Tuesday day, April 6) Classes Resume Evening: Mon, April 5; Day: Tues, April 6 Last day of classes December 1 (Tues) -

Julian Date Cheat Sheet for Regular Years

Date Code Cheat Sheet For Regular Years Day of Year Calendar Date 1 January 1 2 January 2 3 January 3 4 January 4 5 January 5 6 January 6 7 January 7 8 January 8 9 January 9 10 January 10 11 January 11 12 January 12 13 January 13 14 January 14 15 January 15 16 January 16 17 January 17 18 January 18 19 January 19 20 January 20 21 January 21 22 January 22 23 January 23 24 January 24 25 January 25 26 January 26 27 January 27 28 January 28 29 January 29 30 January 30 31 January 31 32 February 1 33 February 2 34 February 3 35 February 4 36 February 5 37 February 6 38 February 7 39 February 8 40 February 9 41 February 10 42 February 11 43 February 12 44 February 13 45 February 14 46 February 15 47 February 16 48 February 17 49 February 18 50 February 19 51 February 20 52 February 21 53 February 22 54 February 23 55 February 24 56 February 25 57 February 26 58 February 27 59 February 28 60 March 1 61 March 2 62 March 3 63 March 4 64 March 5 65 March 6 66 March 7 67 March 8 68 March 9 69 March 10 70 March 11 71 March 12 72 March 13 73 March 14 74 March 15 75 March 16 76 March 17 77 March 18 78 March 19 79 March 20 80 March 21 81 March 22 82 March 23 83 March 24 84 March 25 85 March 26 86 March 27 87 March 28 88 March 29 89 March 30 90 March 31 91 April 1 92 April 2 93 April 3 94 April 4 95 April 5 96 April 6 97 April 7 98 April 8 99 April 9 100 April 10 101 April 11 102 April 12 103 April 13 104 April 14 105 April 15 106 April 16 107 April 17 108 April 18 109 April 19 110 April 20 111 April 21 112 April 22 113 April 23 114 April 24 115 April -

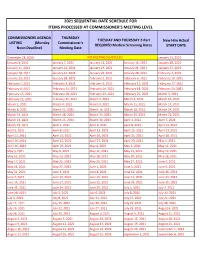

2021 Sequential Date List

2021 SEQUENTIAL DATE SCHEDULE FOR ITEMS PROCESSED AT COMMISSIONER'S MEETING LEVEL COMMISSIONERS AGENDA THURSDAY TUESDAY AND THURSDAY 2-Part New Hire Actual LISTING (Monday Commissioner's REQUIRED Medical Screening Dates START DATE Noon Deadline) Meeting Date December 28, 2020 NO MEETING SCHEDULED January 13, 2021 January 4, 2021 January 7, 2021 January 12, 2021 January 14, 2021 January 20, 2021 January 11, 2021 January 14, 2021 January 19, 2021 January 21, 2021 January 27, 2021 January 18, 2021 January 21, 2021 January 26, 2021 January 28, 2021 February 3, 2021 January 25, 2021 January 28, 2021 February 2, 2021 February 4, 2021 February 10, 2021 February 1, 2021 February 4, 2021 February 9, 2021 February 11, 2021 February 17, 2021 February 8, 2021 February 11, 2021 February 16, 2021 February 18, 2021 February 24, 2021 February 15, 2021 February 18, 2021 February 23, 2021 February 25, 2021 March 3, 2021 February 22, 2021 February 25, 2021 March 2, 2021 March 4, 2021 March 10, 2021 March 1, 2021 March 4, 2021 March 9, 2021 March 11, 2021 March 17, 2021 March 8, 2021 March 11, 2021 March 16, 2021 March 18, 2021 March 24, 2021 March 15, 2021 March 18, 2021 March 23, 2021 March 25, 2021 March 31, 2021 March 22, 2021 March 25, 2021 March 30, 2021 April 1, 2021 April 7, 2021 March 29, 2021 April 1, 2021 April 6, 2021 April 8, 2021 April 14, 2021 April 5, 2021 April 8, 2021 April 13, 2021 April 15, 2021 April 21, 2021 April 12, 2021 April 15, 2021 April 20, 2021 April 22, 2021 April 28, 2021 April 19, 2021 April 22, 2021 April 27, 2021 April -

Due Date Chart 201803281304173331.Xlsx

Special Event Permit Application Due Date Chart for Events from January 1, 2019 - June 30, 2020 If due date lands on a Saturday or Sunday, the due date is moved to the next business day Event Date 30 Calendar days 90 Calendar Days Tuesday, January 01, 2019 Sunday, December 02, 2018 Wednesday, October 03, 2018 Wednesday, January 02, 2019 Monday, December 03, 2018 Thursday, October 04, 2018 Thursday, January 03, 2019 Tuesday, December 04, 2018 Friday, October 05, 2018 Friday, January 04, 2019 Wednesday, December 05, 2018 Saturday, October 06, 2018 Saturday, January 05, 2019 Thursday, December 06, 2018 Sunday, October 07, 2018 Sunday, January 06, 2019 Friday, December 07, 2018 Monday, October 08, 2018 Monday, January 07, 2019 Saturday, December 08, 2018 Tuesday, October 09, 2018 Tuesday, January 08, 2019 Sunday, December 09, 2018 Wednesday, October 10, 2018 Wednesday, January 09, 2019 Monday, December 10, 2018 Thursday, October 11, 2018 Thursday, January 10, 2019 Tuesday, December 11, 2018 Friday, October 12, 2018 Friday, January 11, 2019 Wednesday, December 12, 2018 Saturday, October 13, 2018 Saturday, January 12, 2019 Thursday, December 13, 2018 Sunday, October 14, 2018 Sunday, January 13, 2019 Friday, December 14, 2018 Monday, October 15, 2018 Monday, January 14, 2019 Saturday, December 15, 2018 Tuesday, October 16, 2018 2019 Tuesday, January 15, 2019 Sunday, December 16, 2018 Wednesday, October 17, 2018 Wednesday, January 16, 2019 Monday, December 17, 2018 Thursday, October 18, 2018 Thursday, January 17, 2019 Tuesday, December 18, 2018 -

August '19 September '19 October '19 November '19 December '19

2019-2020 August '19 September '19 October '19 Su M Tu W Th F Sa Su M Tu W Th F Sa Su M Tu W Th F Sa 1 2 3 1 2 3 4 5 6 7 1 2 3 4 5 Date Description Marking Period End Dates and Parent Conferences 4 5 6 7 8 9 10 8 9 10 11 12 13 14 6 7 8 9 10 11 12 Aug. 14-15 Professional Staff Development Marking Period End Dates (Gr. K-12): Transition Day - Grades K, 3-6, 9 and New Students 11 12 13 14 15 16 17 15 16 17 18 19 20 21 13 14 15 16 17 18 19 Aug. 19 Oct 24 (1) Jan 13 (2) March 20 (3) May 27 (4) at High School and Middle School will Report 18 19 20 21 22 23 24 22 23 24 25 26 27 28 20 21 22 23 24 25 26 Aug. 20 First Day of School - All Students Report 25 26 27 28 29 30 31 29 30 27 28 29 30 31 Sept. 2 Labor Day (School Closed) Parent/Teacher Conferences: [42] Sept. 30 Parent/Teacher Conferences (No School for Students) 5:00 pm - 8:00 pm Oct. 14 School Closed Oct 2 - Grades K-2 Oct 3 - Middle School Early Dismissal for Students: Prof Staff Development November '19 December '19 January '20 Oct. 25 12:10 PM for Secondary & 12:45 PM for Elementary Oct 8 - Grades 3-5 Oct 10 - High School Professional Staff Development (Act 80) Su M Tu W Th F Sa Su M Tu W Th F Sa Su M Tu W Th F Sa Nov. -

TENTATIVE SCHOOL CALENDAR 2020-2021 July '20 August '20 September '20 October '20 November '20 December '20 for up T

TENTATIVE SCHOOL CALENDAR 2020-2021 August 31 .................Building In-Service/Staff Work Days July ‘20 January ‘21 S M T W T F S S M T W T F S September 1-3 ..........Building In-Service/Staff 1 2 3 4 1 2 Work Days 5 6 7 8 9 10 11 3 4 5 6 7 8 9 September 7 .............No School/Labor Day September 8 .............First Day (1-8) 12 13 14 15 16 17 18 10 11 12 13 14 15 16 September 8 & 9 .......PS & K Orientation 19 20 21 22 23 24 25 17 18 19 20 21 22 23 September 10 ...........First Day (PS & K) 2 2 26 27 28 29 30 31 24 25 26 27 8 8 29 30 September 14-30 ......NWEA Testing 31 October 1-2...............NWEA Testing August ‘20 October 14 & 15 ........No School/Staff In-Service S M T W T F S February ‘21 October 16 ................No School October 19 ................No School/Staff In-Service 1 S M T W T F S October 20 ................Parent Conferences 2 3 4 5 6 7 8 1 2 3 4 5 6 (PS-8) 3:00 p.m.-7:00 p.m. 9 10 11 12 13 14 15 7 8 9 10 11 12 13 October 22 ................Parent Conferences 16 17 18 19 20 21 22 (PS-8) 3:00 p.m.-7:00 p.m. 14 15 16 17 18 19 20 23 24 25 26 27 28 29 21 22 23 24 25 26 27 November 12 ............Parent PM Pick Up/ 30 31 28 .................................Full Day November 12 ............End of 1st Quarter November 13 ............No School/Staff Work Day September ‘20 March ‘21 November 25-27 .......No School/Thanksgiving S M T W T F S S M T W T F S Break 1 2 3 4 5 1 2 3 4 5 6 6 7 8 9 10 11 12 December 23-31 .......No School/Winter Break 7 8 9 10 11 12 13 13 14 15 16 17 18 19 14 15 16 17 18 19 20 January 1 ..................No -

Caltrans Construction 5-Workday Calendar 2028

CONSTRUCTION 5-WORKDAY CALENDAR Year 2028 JANUARY JULY Sund Mond Tuesd Wedn Thurs Friday Satur Sund Mond Tuesd Wedn Thurs Friday Satur 1 1 678 679 680 681 682 804 805 806 807 2 3 4 5 6 7 8 2 3 4 5 6 7 8 683 684 685 686 687 808 809 810 811 812 9 10 11 12 13 14 15 9 10 11 12 13 14 15 688 689 690 691 813 814 815 816 817 16 17 18 19 20 21 22 16 17 18 19 20 21 22 692 693 694 695 696 818 819 820 821 822 23 24 25 26 27 28 29 23 24 25 26 27 28 29 697 823 30 31 30 31 FEBRUARY AUGUST Sund Mond Tuesd Wedn Thurs Friday Satur Sund Mond Tuesd Wedn Thurs Friday Satur 698 699 700 701 824 825 826 827 1 2 3 4 5 1 2 3 4 5 702 703 704 705 706 828 829 830 831 832 6 7 8 9 10 11 12 6 7 8 9 10 11 12 707 708 709 710 711 833 834 835 836 837 13 14 15 16 17 18 19 13 14 15 16 17 18 19 712 713 714 715 838 839 840 841 842 20 21 22 23 24 25 26 20 21 22 23 24 25 26 716 717 843 844 845 846 27 28 29 27 28 29 30 31 MARCH SEPTEMBER Sund Mond Tuesd Wedn Thurs Friday Satur Sund Mond Tuesd Wedn Thurs Friday Satur 718 719 720 847 1 2 3 4 1 2 721 722 723 724 725 848 849 850 851 5 6 7 8 9 10 11 3 4 5 6 7 8 9 726 727 728 729 730 852 853 854 855 856 12 13 14 15 16 17 18 10 11 12 13 14 15 16 731 732 733 734 735 857 858 859 860 861 19 20 21 22 23 24 25 17 18 19 20 21 22 23 736 737 738 739 862 863 864 865 866 26 27 28 29 30 31 24 25 26 27 28 29 30 APRIL OCTOBER Sund Mond Tuesd Wedn Thurs Friday Satur Sund Mond Tuesd Wedn Thurs Friday Satur 867 868 869 870 871 1 1 2 3 4 5 6 7 740 741 742 743 744 872 873 874 875 2 3 4 5 6 7 8 8 9 10 11 12 13 14 745 746 747 748 749 876 877 878 879 880