Canada Research Atlantica Yield

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Timeline of Natural History

Timeline of natural history This timeline of natural history summarizes significant geological and Life timeline Ice Ages biological events from the formation of the 0 — Primates Quater nary Flowers ←Earliest apes Earth to the arrival of modern humans. P Birds h Mammals – Plants Dinosaurs Times are listed in millions of years, or Karo o a n ← Andean Tetrapoda megaanni (Ma). -50 0 — e Arthropods Molluscs r ←Cambrian explosion o ← Cryoge nian Ediacara biota – z ←Earliest animals o ←Earliest plants i Multicellular -1000 — c Contents life ←Sexual reproduction Dating of the Geologic record – P r The earliest Solar System -1500 — o t Precambrian Supereon – e r Eukaryotes Hadean Eon o -2000 — z o Archean Eon i Huron ian – c Eoarchean Era ←Oxygen crisis Paleoarchean Era -2500 — ←Atmospheric oxygen Mesoarchean Era – Photosynthesis Neoarchean Era Pong ola Proterozoic Eon -3000 — A r Paleoproterozoic Era c – h Siderian Period e a Rhyacian Period -3500 — n ←Earliest oxygen Orosirian Period Single-celled – life Statherian Period -4000 — ←Earliest life Mesoproterozoic Era H Calymmian Period a water – d e Ectasian Period a ←Earliest water Stenian Period -4500 — n ←Earth (−4540) (million years ago) Clickable Neoproterozoic Era ( Tonian Period Cryogenian Period Ediacaran Period Phanerozoic Eon Paleozoic Era Cambrian Period Ordovician Period Silurian Period Devonian Period Carboniferous Period Permian Period Mesozoic Era Triassic Period Jurassic Period Cretaceous Period Cenozoic Era Paleogene Period Neogene Period Quaternary Period Etymology of period names References See also External links Dating of the Geologic record The Geologic record is the strata (layers) of rock in the planet's crust and the science of geology is much concerned with the age and origin of all rocks to determine the history and formation of Earth and to understand the forces that have acted upon it. -

EGP Sale Uruguay

Media Relations PRESS T +39 06 8305 5699 RELEASE F +39 06 8305 3771 [email protected] enelgreenpower.com ENEL GREEN POWER STEPS OUT OF URUGUAY THROUGH SALE OF 50 MW WIND FARM FOR 120 MILLION US DOLLARS • EGP closed the sale to Atlantica Yield of Enel Green Power Uruguay S.A., 100% owner of the Melowind plant • The transaction is part of Enel’s active portfolio management strategy, rotating assets to finance growth in strategic areas Rome, December 14th , 2018 – Enel Green Power S.p.A. (“EGP”) closed the sale to power company Atlantica Yield of its fully-owned subsidiary Enel Green Power Uruguay S.A. (“EGP Uruguay”), which owns through its project company Estrellada S.A. the 50 MW Melowind wind farm located in Cerro Largo, around 320 km away from Montevideo. EGP has sold its subsidiary in Uruguay for around 120 million US dollars, equal to the company’s Enterprise Value. The transaction is part of the disposal programme of non-core assets provided for in the Enel Group’s active portfolio management plan. This strategy allows for the reallocation of resources to areas with a greater growth margin and potential for the Group. The Melowind farm sells its electricity output to the state-owned power company UTE (Administración Nacional de Usinas y Trasmisiones Eléctricas), which manages the transmission, distribution and sale of electricity in Uruguay, under a 20-year power purchase agreement (PPA). Atlantica Yield plc owns a diversified portfolio of contracted renewable energy, efficient natural gas, electric transmission and water assets in North and South America, and certain markets in Europe, the Middle East and Africa (EMEA). -

Mafic Dyke Swarm, Brazil: Implications for Archean Supercratons

Michigan Technological University Digital Commons @ Michigan Tech Michigan Tech Publications 12-3-2018 Revisiting the paleomagnetism of the Neoarchean Uauá mafic dyke swarm, Brazil: Implications for Archean supercratons J. Salminen University of Helsinki E. P. Oliveira State University of Campinas, Brazil Elisa J. Piispa Michigan Technological University Aleksey Smirnov Michigan Technological University, [email protected] R. I. F. Trindade Universidade de Sao Paulo Follow this and additional works at: https://digitalcommons.mtu.edu/michigantech-p Part of the Geological Engineering Commons, and the Physics Commons Recommended Citation Salminen, J., Oliveira, E. P., Piispa, E. J., Smirnov, A., & Trindade, R. I. (2018). Revisiting the paleomagnetism of the Neoarchean Uauá mafic dyke swarm, Brazil: Implications for Archean supercratons. Precambrian Research, 329, 108-123. http://dx.doi.org/10.1016/j.precamres.2018.12.001 Retrieved from: https://digitalcommons.mtu.edu/michigantech-p/443 Follow this and additional works at: https://digitalcommons.mtu.edu/michigantech-p Part of the Geological Engineering Commons, and the Physics Commons Precambrian Research 329 (2019) 108–123 Contents lists available at ScienceDirect Precambrian Research journal homepage: www.elsevier.com/locate/precamres Revisiting the paleomagnetism of the Neoarchean Uauá mafic dyke swarm, T Brazil: Implications for Archean supercratons ⁎ J. Salminena,b, , E.P. Oliveirac, E.J. Piispad,e, A.V. Smirnovd,f, R.I.F. Trindadeg a Physics Department, University of Helsinki, P.O. Box -

Dead Sea Pollen Provides New Insights Into the Paleoenvironment of the Southern Levant During MIS 6ᅢ까タᅡモ5

Quaternary Science Reviews 188 (2018) 15e27 Contents lists available at ScienceDirect Quaternary Science Reviews journal homepage: www.elsevier.com/locate/quascirev Dead Sea pollen provides new insights into the paleoenvironment of the southern Levant during MIS 6e5 * Chunzhu Chen a, b, , Thomas Litt b a School of Geographic Science, Nantong University, Tongjingdadao 999, 226007 Nantong, China b Steinmann Institute for Geology, Mineralogy, and Paleontology, University of Bonn, Nussallee 8, 53115 Bonn, Germany article info abstract Article history: The paleoclimate of the southern Levant, especially during the last interglacial (LIG), is still under debate. Received 18 December 2017 Reliable paleovegetation information for this period, as independent evidence to the paleoenvironment, Received in revised form was still missing. In this study, we present a high-resolution pollen record encompassing 147e89 ka from 17 March 2018 the Dead Sea deep drilling core 5017-1A. The sediment profile is marked by alternations of laminated Accepted 18 March 2018 marl deposits and thick massive halite, indicating lake-level fluctuations. The pollen record suggests that steppe and desert components predominated in the Dead Sea surroundings during the whole investi- gated interval. The late penultimate glacial (147.3e130.9 ka) and early last glacial (115.5e89.1 ka) were Keywords: fi Last interglacial cool and relatively dry, with sub-humid conditions con ned to the mountains that sustained moderate Paleovegetation amounts of deciduous oaks. Prior to the LIG optimum, a prevalence of desert components and a Lake level concomitant increase in frost-sensitive pistachio trees demonstrate the occurrence of an arid initial Early modern human migration warming phase (130.9e124.2 ka). -

Precambrian Basement and Late Paleoproterozoic to Mesoproterozoic Tectonic Evolution of the SW Yangtze Block, South China

minerals Article Precambrian Basement and Late Paleoproterozoic to Mesoproterozoic Tectonic Evolution of the SW Yangtze Block, South China: Constraints from Zircon U–Pb Dating and Hf Isotopes Wei Liu 1,2,*, Xiaoyong Yang 1,*, Shengyuan Shu 1, Lei Liu 1 and Sihua Yuan 3 1 CAS Key Laboratory of Crust-Mantle Materials and Environments, University of Science and Technology of China, Hefei 230026, China; [email protected] (S.S.); [email protected] (L.L.) 2 Chengdu Center, China Geological Survey, Chengdu 610081, China 3 Department of Earthquake Science, Institute of Disaster Prevention, Langfang 065201, China; [email protected] * Correspondence: [email protected] (W.L.); [email protected] (X.Y.) Received: 27 May 2018; Accepted: 30 July 2018; Published: 3 August 2018 Abstract: Zircon U–Pb dating and Hf isotopic analyses are performed on clastic rocks, sedimentary tuff of the Dongchuan Group (DCG), and a diabase, which is an intrusive body from the base of DCG in the SW Yangtze Block. The results provide new constraints on the Precambrian basement and the Late Paleoproterozoic to Mesoproterozoic tectonic evolution of the SW Yangtze Block, South China. DCG has been divided into four formations from the bottom to the top: Yinmin, Luoxue, Heishan, and Qinglongshan. The Yinmin Formation, which represents the oldest rock unit of DCG, was intruded by a diabase dyke. The oldest zircon age of the clastic rocks from the Yinmin Formation is 3654 Ma, with "Hf(t) of −3.1 and a two-stage modeled age of 4081 Ma. Another zircon exhibits an age of 2406 Ma, with "Hf(t) of −20.1 and a two-stage modeled age of 4152 Ma. -

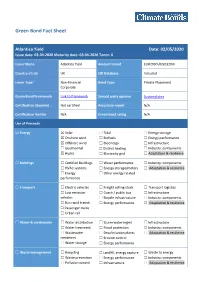

Atlantica Yield Date: 02/05/2020 Issue Date: 03-04-2020 Maturity Date: 03-04-2026 Tenor: 6

Green Bond Fact Sheet Atlantica Yield Date: 02/05/2020 Issue date: 03-04-2020 Maturity date: 03-04-2026 Tenor: 6 Issuer Name Atlantica Yield Amount Issued EUR290m/USD320m Country of risk UK CBI Database Included Issuer Type1 Non-Financial Bond Type Private Placement Corporate Green Bond Framework Link to framework Second party opinion Sustainalytics Certification Standard Not certified Assurance report N/A Certification Verifier N/A Green bond rating N/A Use of Proceeds ☒ Energy ☒ Solar ☐ Tidal ☐ Energy storage ☒ Onshore wind ☐ Biofuels ☐ Energy performance ☒ Offshore wind ☐ Bioenergy ☐ Infrastructure ☐ Geothermal ☐ District heating ☐ Industry: components ☒ Hydro ☐ Electricity grid ☐ Adaptation & resilience ☐ Buildings ☐ Certified Buildings ☐ Water performance ☐ Industry: components ☐ HVAC systems ☐ Energy storage/meters ☐ Adaptation & resilience ☐ Energy ☐ Other energy related performance ☐ Transport ☐ Electric vehicles ☐ Freight rolling stock ☐ Transport logistics ☐ Low emission ☐ Coach / public bus ☐ Infrastructure vehicles ☐ Bicycle infrastructure ☐ Industry: components ☐ Bus rapid transit ☐ Energy performance ☐ Adaptation & resilience ☐ Passenger trains ☐ Urban rail ☐ Water & wastewater ☐ Water distribution ☐ Storm water mgmt ☐ Infrastructure ☐ Water treatment ☐ Flood protection ☐ Industry: components ☐ Wastewater ☐ Desalinisation plants ☐ Adaptation & resilience treatment ☐ Erosion control ☐ Water storage ☐ Energy performance ☐ Waste management ☐ Recycling ☐ Landfill, energy capture ☐ Waste to energy ☐ Waste prevention ☐ Energy -

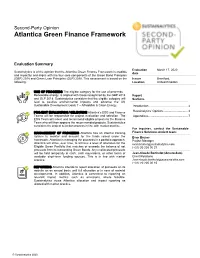

Second Party Opinion on Atlantica's Green Finance Framework

Second-Party Opinion Atlantica Green Finance Framework Evaluation Summary Evaluation March 17, 2020 Sustainalytics is of the opinion that the Atlantica Green Finance Framework is credible date and impactful and aligns with the four core components of the Green Bond Principles (GBP) 2018 and Green Loan Principles (GLP) 2018. This assessment is based on the Issuer Brentford, following: Location United Kingdom The eligible category for the use of proceeds – Renewable energy, is aligned with those recognized by the GBP 2018 Report and GLP 2018. Sustainalytics considers that the eligible category will Sections lead to positive environmental impacts and advance the UN Sustainable Development Goals 7 – Affordable & Clean Energy. Introduction ................................................ 2 Atlantica’s ESG and Finance Sustainalytics’ Opinion .............................. 3 Teams will be responsible for project evaluation and selection. The Appendices ................................................ 7 ESG Team will select and recommend eligible projects to the Finance Team who will then approve the recommended projects. Sustainalytics considers the project selection process in line with market practice. For inquiries, contact the Sustainable Atlantica has an internal tracking Finance Solutions project team: system to monitor and account for the funds raised under the Evan Bruner framework. Atlantica is managing the proceeds in a portfolio approach. Project Manager Atlantica will strive, over time, to achieve a level of allocation for the [email protected] Eligible Green Portfolio that matches or exceeds the balance of net (+31) 20 205 00 27 proceeds from its outstanding Green Bonds. Any unallocated proceeds will be held temporally in cash, cash equivalents, or other forms of Jean-Claude Berthelot (Amsterdam) available short-term funding sources. -

The Americas 2014-2015

The Americas 2014-2015 ALASKA | CANADA & NEW ENGLAND | CARIBBEAN & PANAMA CANAL | SOUTH AMERICA CoNTENTS 2 EXPERIENCE 96 EXPLORE ASHORE Your World. Your Way.® Land Tour Series 16 TaSTE 107 HoTEL PROGRamS The Finest Cuisine at Sea Pre- & Post-Cruise Hotel Programs 28 VaLUE 110 SUITES & STATERoomS Best Value in Upscale Cruising 120 DECK PLANS 32 OCEANIA CLUB Rewarding Membership Privileges 124 AIR PROGRamS & INfoRmaTION 34 DESTINATION SPECIALISTS 126 CRUISE CALENdaR 38 CaRIbbEAN & PaNama CaNAL 128 EXPERIENCE OCEANIACRUISES.Com 60 SoUTH AMERICA 129 GENERAL INfoRmaTION 66 ALASKA 78 CaNada & NEW ENGLAND 86 TRANSOCEANIC VoyaGES Hubbard Glacier Alaskan king crab ON THE COVER Colorful Maine lobster buoys are used to mark the lobster traps of local fishermen. As tradition shows, each fisherman paints a unique color and design onto a buoy to identify its origin of ownership. POINTS OF DISTINCTION n FREE AIRFARE* on every voyage n Mid-size, elegant ships catering to The Americas just 684 or 1,250 guests 2014 - 2015 n Finest cuisine at sea, served in a variety of distinctive open-seating restaurants, at no additional charge NEW WORLD ADVENTURES | European and Asian explorers once risked everything n to discover the New World and tame this rugged frontier. Now you, on board Oceania Gourmet culinary program crafted by world-renowned Master Chef Cruises, can trace the routes of the ages along the New England and Canadian shores, Jacques Pépin transformed by autumn’s embrace, or through the astounding Panama Canal. European and n Spectacular port-intensive itineraries African cultures mixed with native traditions gave birth to the tango, the passionate dance of featuring overnight visits and extended Buenos Aires. -

Welcome to Your CDP Climate Change Questionnaire 2019 C0. Introduction

Atlantica Yield plc CDP Climate Change Questionnaire 2019 31 July 2019 Welcome to your CDP Climate Change Questionnaire 2019 C0. Introduction C0.1 (C0.1) Give a general description and introduction to your organization. Atlantica is a sustainable infrastructure company with the majority of its activities in renewable energy. We own and manage renewable energy, efficient natural gas, transmission and transportation infrastructures and water assets in North America, South America and EMEA. We intend to expand our business, maintaining North America, South America and Europe as our core geographies. Our business operations reduce greenhouse gas emissions contributing to mitigate the impact of climate change. In 2018 Atlantica avoided almost 5 million tons of CO2 in power generation versus the emissions an equivalent fossil fuel fleet would have generated. We intend to maintain 80% of our revenues generated from low-carbon footprint assets including our renewables, transportation and transmission infrastructures and water assets. Approximately 76% of our 2018 revenues were generated by our renewable energy assets including solar and wind. Atlantica is a UK company listed on Nasdaq Global Select Market under the ticker symbol "AY". Our assets generated in 2018 revenues of $1,043 million and Adjusted EBITDA of $858.7 million. Atlantica had 217 employees as of December 31, 2018, 40% of which were women. As of December 31, 2018 Atlantica owns or has interests in 24 assets, comprising 1,496 MW of renewable energy generation, 300 MW of efficient natural gas power generation, 10.5 M ft3 per day of water desalination and 1,152 miles of electric transmission lines. -

Genomic Characterization of Three Marine Fungi, Including Emericellopsis Atlantica Sp

Hagestad et al. IMA Fungus (2021) 12:21 https://doi.org/10.1186/s43008-021-00072-0 IMA Fungus RESEARCH Open Access Genomic characterization of three marine fungi, including Emericellopsis atlantica sp. nov. with signatures of a generalist lifestyle and marine biomass degradation Ole Christian Hagestad1* , Lingwei Hou2, Jeanette H. Andersen1, Espen H. Hansen1, Bjørn Altermark3, Chun Li1, Eric Kuhnert4, Russell J. Cox4, Pedro W. Crous2, Joseph W. Spatafora5, Kathleen Lail6, Mojgan Amirebrahimi6, Anna Lipzen6, Jasmyn Pangilinan6, William Andreopoulos6, Richard D. Hayes6, Vivian Ng6, Igor V. Grigoriev6,7, Stephen A. Jackson8,9, Thomas D. S. Sutton8,10, Alan D. W. Dobson8,9 and Teppo Rämä1 ABSTRACT Marine fungi remain poorly covered in global genome sequencing campaigns; the 1000 fungal genomes (1KFG) project attempts to shed light on the diversity, ecology and potential industrial use of overlooked and poorly resolved fungal taxa. This study characterizes the genomes of three marine fungi: Emericellopsis sp. TS7, wood- associated Amylocarpus encephaloides and algae-associated Calycina marina. These species were genome sequenced to study their genomic features, biosynthetic potential and phylogenetic placement using multilocus data. Amylocarpus encephaloides and C. marina were placed in the Helotiaceae and Pezizellaceae (Helotiales), respectively, based on a 15-gene phylogenetic analysis. These two genomes had fewer biosynthetic gene clusters (BGCs) and carbohydrate active enzymes (CAZymes) than Emericellopsis sp. TS7 isolate. Emericellopsis sp. TS7 (Hypocreales, Ascomycota) was isolated from the sponge Stelletta normani. A six-gene phylogenetic analysis placed the isolate in the marine Emericellopsis clade and morphological examination confirmed that the isolate represents a new species, which is described here as E. -

Cogeneration and Conventional Plants, Being a Pioneer in the O&M of Hybrid Solar-Gas Plants

Services Corporate Presentation R-25062021 Who 1 are we? 2 Abengoa (MCE: ABG.B) is an international company that Who are we? applies innovative technology solutions for sustainable development in the infrastructure, energy and water sectors. Constructing energy infrastructures . Generating conventional and renewable energy. Transporting and distributing energy. Providing solutions for the integrated water cycle . Developing desalination and water treatment processes. Constructing hydraulic infrastructures. Being a reference in the transmission and distribution sector . Developing transmission lines, electric distribution and railway electrification projects. Constructing installations and infrastructures for all types of plants and buildings. Obtaining results in the services area . Providing operation and maintenance services for plants optimization. Managing private assets efficiently. Furthering new horizons for development and innovation . Our 280 accumulated awarded patents since 2008 position us as technological leaders in sectors such as solar thermal technology. Renewable energy storage and our bet for energy efficiency and water consumption (water-energy nexus). 3 Una compañía viable con una base sólida Sólido negocio en ingeniería, La huella global aporta resiliencia al negocio de suministro, construcción, operación y Abengoa y el tamaño de su cartera de proyectos mantenimiento en mercados de alto proporciona visibilidad de los ingresos crecimiento Credibilidad de los Estructura ligera con alta eficiencia stakeholders operativa El desarrollo de tecnología pionera Un modelo de negocio más concentrado y una y comercialmente viable se ha estructura de capital sana y robusta, sumados a un convertido en la ventaja conjunto multidisciplinar de capacidades, sitúan a la competitiva clave de Abengoa compañía en una posición sólida para la creación de valor. Equipo humano, comprometido y capaz, poseedor de un know-how especializado y competitivo. -

Supercontinent Reconstruction the Palaeomagnetically Viable, Long

Geological Society, London, Special Publications The palaeomagnetically viable, long-lived and all-inclusive Rodinia supercontinent reconstruction David A. D. Evans Geological Society, London, Special Publications 2009; v. 327; p. 371-404 doi:10.1144/SP327.16 Email alerting click here to receive free email alerts when new articles cite this service article Permission click here to seek permission to re-use all or part of this article request Subscribe click here to subscribe to Geological Society, London, Special Publications or the Lyell Collection Notes Downloaded by on 21 December 2009 © 2009 Geological Society of London The palaeomagnetically viable, long-lived and all-inclusive Rodinia supercontinent reconstruction DAVID A. D. EVANS Department of Geology & Geophysics, Yale University, New Haven, CT 06520-8109, USA (e-mail: [email protected]) Abstract: Palaeomagnetic apparent polar wander (APW) paths from the world’s cratons at 1300–700 Ma can constrain the palaeogeographic possibilities for a long-lived and all-inclusive Rodinia supercontinent. Laurentia’s APW path is the most complete and forms the basis for super- position by other cratons’ APW paths to identify possible durations of those cratons’ inclusion in Rodinia, and also to generate reconstructions that are constrained both in latitude and longitude relative to Laurentia. Baltica reconstructs adjacent to the SE margin of Greenland, in a standard and geographically ‘upright’ position, between c. 1050 and 600 Ma. Australia reconstructs adja- cent to the pre-Caspian margin of Baltica, geographically ‘inverted’ such that cratonic portions of Queensland are juxtaposed with that margin via collision at c. 1100 Ma. Arctic North America reconstructs opposite to the CONgo þ Sa˜o Francisco craton at its DAmaride–Lufilian margin (the ‘ANACONDA’ fit) throughout the interval 1235–755 Ma according to palaeomag- netic poles of those ages from both cratons, and the reconstruction was probably established during the c.