Franchising As a Business Concept – Chance for Many in Serbia

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

National Competition Report Q2 2017

NATIONAL COMPETITION QUARTERLY REPORT APRIL– JUNE 2017 BELGIUM basis of their “Best and Final Offer.” Third, Infrabel issued individual calls for specific orders within the This section reviews developments under Book IV of the terms and conditions of the framework agreement. The Belgian Code of Economic Law (“CEL”) on the selected companies had to submit their best offer for Protection of Competition, which is enforced by the each call, and the orders were awarded to the lowest Belgian Competition Authority (“the BCA”). Within the bidder. BCA, the Prosecutor General and its staff of prosecutors (collectively, the “Auditorate”) investigate In 2013, the Auditorate started investigating this public alleged restrictive practices and concentrations, while procurement following ABB’s leniency application. the Competition College (the “College”) functions as The investigation revealed that the bidders had agreed the decision-making body. Prior to September 6, 2013, to allocate the orders placed by Infrabel amongst Belgian competition law was codified in the Act on the themselves. For each call, they exchanged price Protection of Economic Competition of September 15, information and instructions to ensure that the 2006 (“APEC”) and enforced by the Belgian pre-designated participant would present the lowest Competition Authority, then composed of the price and win the tender. The Auditorate found that Directorate General for Competition and the these practices had started in 2010–2011 and continued Competition Council. When relevant, entries in this until June 2016. The Auditorate notified its objections report will refer to the former sub-bodies of the BCA. to the companies in August 2016, and settlement talks began a month later. -

Copy of Censusdata

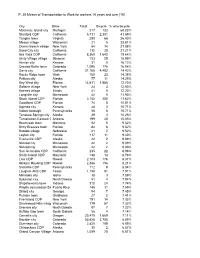

P. 30 Means of Transportation to Work for workers 16 years and over [16] City State Total: Bicycle % who bicycle Mackinac Island city Michigan 217 132 60.83% Stanford CDP California 5,711 2,381 41.69% Tangier town Virginia 250 66 26.40% Mason village Wisconsin 21 5 23.81% Ocean Beach village New York 64 14 21.88% Sand City city California 132 28 21.21% Isla Vista CDP California 8,360 1,642 19.64% Unity Village village Missouri 153 29 18.95% Hunter city Kansas 31 5 16.13% Crested Butte town Colorado 1,096 176 16.06% Davis city California 31,165 4,493 14.42% Rocky Ridge town Utah 160 23 14.38% Pelican city Alaska 77 11 14.29% Key West city Florida 14,611 1,856 12.70% Saltaire village New York 24 3 12.50% Keenes village Illinois 41 5 12.20% Longville city Minnesota 42 5 11.90% Stock Island CDP Florida 2,152 250 11.62% Goodland CDP Florida 74 8 10.81% Agenda city Kansas 28 3 10.71% Volant borough Pennsylvania 56 6 10.71% Tenakee Springs city Alaska 39 4 10.26% Tumacacori-Carmen C Arizona 199 20 10.05% Bearcreek town Montana 52 5 9.62% Briny Breezes town Florida 84 8 9.52% Barada village Nebraska 21 2 9.52% Layton city Florida 117 11 9.40% Evansville CDP Alaska 22 2 9.09% Nimrod city Minnesota 22 2 9.09% Nimrod city Minnesota 22 2 9.09% San Geronimo CDP California 245 22 8.98% Smith Island CDP Maryland 148 13 8.78% Laie CDP Hawaii 2,103 176 8.37% Hickam Housing CDP Hawaii 2,386 196 8.21% Slickville CDP Pennsylvania 112 9 8.04% Laughlin AFB CDP Texas 1,150 91 7.91% Minidoka city Idaho 38 3 7.89% Sykeston city North Dakota 51 4 7.84% Shipshewana town Indiana 310 24 7.74% Playita comunidad (Sa Puerto Rico 145 11 7.59% Dillard city Georgia 94 7 7.45% Putnam town Oklahoma 27 2 7.41% Fire Island CDP New York 191 14 7.33% Shorewood Hills village Wisconsin 779 57 7.32% Grenora city North Dakota 97 7 7.22% Buffalo Gap town South Dakota 56 4 7.14% Corvallis city Oregon 23,475 1,669 7.11% Boulder city Colorado 53,828 3,708 6.89% Gunnison city Colorado 2,825 189 6.69% Chistochina CDP Alaska 30 2 6.67% Grand Canyon Village Arizona 1,059 70 6.61% P. -

SOCIETY SERBIAN FALCON/SERBIAN SOKO/ SREMSKI KARLOVCI from 1904 to 1945Th

Physical education and sport through the centuries www.fiep-serbia.net 2015, 2(1), 54-71 ISSN 2335-0598 Original research article SOCIETY SERBIAN FALCON/SERBIAN SOKO/ SREMSKI KARLOVCI FROM 1904 TO 1945th. Velimir Sesum1 and Bojan Medjedovic1 1 Faculty of Sport and Tourism in Novi Sad, University Edukons Velimir Sesum and Bojan Medjedovic UDK 796.03(497.113)’’1904‐1945 SUMMARY In the introductory part of the paper is a brief history Sokolism the Slavs, as well as what preceded and how to develop ideas Sokolism the Serbs. The influence of Serbian Youth Assembly held in Karlovci in 1903 on the development of Sokolism. Desires and intentions Serbian Youth and the inclusion of Karlovac physics Dr Laza Popovic in establishing the first Sokol Society in Karlovac, 1904. The influence and importance of the first Sokol Society to develop Sokolism the Serbs. The research topic is Sokolsko society "Serbian falcon" from Sremski Karlovci from 1904 to 1945, or its appearance, development and duration, the aim of this research would, therefore, was the finding, gathering and sorting of facts and data on the formation, development and lasting " Serbian falcon "in Sremski Karlovci from 1904 to 1945, that the facts in this regard, using appropriate scientific methods, and above all the historical method, because research by its historical character. The results of the work were presented in the form of final considerations and conclusions, all the results compiled by components of the applied theoretical models, and these are the beginnings, development and duration of this society from 1904 to 1945 . The discussion gives criticism explored and interpretation of historical facts in explaining the establishment, development and duration of the "Serbian falcon" in Karlowitz from 1904 to 1945. -

Yiannis N. Krallis Director General 11/29/2007 1

CHIPITACHIPITA RussiaRussia Yiannis N. Krallis Director General 1 11/29/2007 BACKGROUNDBACKGROUND • Chipita is a Greek origin multinational Company producing and commercializing packed flour based snacks such as: croissants, cakes and bread chips with turnover in excess of 1.5 billion Euro. • Established in 1973, Chipita brands are presented in more than 35 countries with production facilities in Greece, Russia, Poland, Romania, Bulgaria, Mexico, Portugal, Egypt, the leader in all markets where present. • The main international umbrella brand is 7Days. 11/29/2007 2 COMPANYCOMPANY PROFILEPROFILE As of September 1st, 2006, Chipita merged with: ¾ DELTA, Number One in the diary industry ¾ GOODY`S, Number One in the foodservice industry, and ¾ GENERAL FROZEN FOODS “BARBA STATHIS”, Number One in the frozen food industry to establish VIVARTIA - Number One food company in Greece, ranking 35th in Europe with 35 factory units throughout 16 countries, and over 13 000 employees. 11/29/2007 3 BACKGROUNDBACKGROUND • In Russia, Chipita is a Leader of croissants under 7Days brand (with almost 80% market share), presented in main soft cakes segments. • Chipita manufactures 50 SKUs mainly croissants, cakes, pastes and salted snacks; and contracts for TANDER and DANONE. • Chipita Russia employs 750 people • Business activities: all Russia regions, • Commercial companies in: Ukraine, Byelorussia, • Exports activities: Serbia, Czech Republic, Slovakia, Poland, Hungary • Production facilities located in Saint Petersburg. 11/29/2007 4 CHIPITACHIPITALOGISTICS RUSSIARUSSIA Can one explain how a small, by the vast, Russian Geography Standards Company, can survive this Supply Chain and Logistics Marathon? We have been accused of bad service, of low deliveries ratios, we have even been de-listed from KA at times. -

Back from the Wilderness Back from the Wilderness

Back from the Wilderness Back from the Wilderness IBYA HAS struggled to maintain a credible involve Libya militarily in the Arab-Israeli conflict. Building an air force air arm through four turbulent decades. After the young officers, led by Gaddafi, usurped Even prior to the last US and British troops leaving LAfter World War Two, the then Libyan Air the Idris regime, the new rulers had to look for Libya, before March 1970, Gaddafi opened Force (LAF) was just a small organisation, fresh sources of military equipment. Pursuit of negotiations with France for large amounts of although both the United States Air Force and British and US materiel would have been viewed new equipment. Royal Air Force regularly deployed aircraft to the as hypocritical, resulting in domestic and Arab The LAF was subsequently renamed Libyan Arab country. criticism as both nations were regarded as hostile Republic Air Force (LARAF), and then came a deal with After oil was discovered in 1959 Libya, then to Arab interests...and because of their support the French Government for a considerable amount one of the world’s poorest countries, became for Israel. of aircraft, support equipment, spares and weapons extremely wealthy. Generally, the West enjoyed Gaddafi demanded that Wheelus AFB be closed were purchased. The largest and most important of a warm relationship with Libya, with the US and its facilities immediately turned over to the these agreements was the order for approximately pursuing policies to aid its operations from Libyan people. While the US wished to retain 110 Dassault Mirage V fighter-bombers. -

Regional Economic Development in the Balkan Region

Regional Economic Development in the Balkan Region Regional Economic Development in the Balkan Region Edited by Teoman Duman, Merdžana Obralić, Erkan Ilgün and Uğur Ergun Regional Economic Development in the Balkan Region Edited by Teoman Duman, Merdžana Obralić, Erkan Ilgün and Uğur Ergun This book first published 2016 Cambridge Scholars Publishing Lady Stephenson Library, Newcastle upon Tyne, NE6 2PA, UK British Library Cataloguing in Publication Data A catalogue record for this book is available from the British Library Copyright © 2016 by Teoman Duman, Merdžana Obralić, Erkan Ilgün, Uğur Ergun and contributors All rights for this book reserved. No part of this book may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the copyright owner. ISBN (10): 1-4438-8527-4 ISBN (13): 978-1-4438-8527-0 TABLE OF CONTENTS Acknowledgements .................................................................................. viii List of Abbreviations .................................................................................. ix Chapter One ................................................................................................. 1 Introduction Teoman Duman Chapter Two .............................................................................................. 10 Bosnia and Herzegovina, from the Self-Sustainable Economy to Unfinished Transition: What's Next? Sead Kreso, University of Sarajevo, Bosnia and -

NATO Bombing of Yugoslavia

“HENRI COANDA” “GENERAL M.R. STEFANIK” AIR FORCE ACADEMY ARMED FORCES ACADEMY ROMANIA SLOVAK REPUBLIC INTERNATIONAL CONFERENCE of SCIENTIFIC PAPER AFASES 2015 Brasov, 28-30 May 2015 NATO BOMBING IN THE FORMER REPUBLIC OF YUGOSLAVIA Diana Manolache*, Ciprian Chiş* *”Carol I” National Defense University, Bucharest, Romania Abstract: Within this work, we approached the bombing operation in Yugoslavia, named „Allied Force”, that was a part of the War which led to the establishment of Kosovo’s status. The development period of this operation, including bombardment operations, was 78 days, between 24th of March and 10th of June, 1999. In the conducted study, we chose to use the scientifique observation as method of scientifique research as well as we used the comparative-historical method and in terms of the techniques used, we focused mainly on documentary analysis, available with an extensive bibliography. In the conducted study, we have highlighted some dealt less aspects of the subject, and also, items related to the strategy used by combatants during the conflict emphasizing the pros and cons of strategic air power. From these elements can be formulated numerous lessons learned useful in future conflicts, and also, possible research directions. Keywords: Yugoslavia, NATO forces, bombing actions, aircraft. 1. INTRODUCTION The regulations, including the territorial ones, which took place during and after the The bombing operation in Yugoslavia was actions of all kinds from this conflict area, called „Allied Force” and was a part of the were framed within the provisions of United War led to the establishment of Kosovo’s Nations Security Council Resolution no. 1244. -

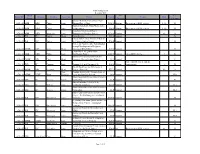

Board Date Bank Group Window Country Loan Type Project Amount

MDB Voting record December 2013 Bank US Env. Board Date Window Country Loan Type Project Amount Reason Code Group Position Category Qinghai Delingha Concentrated Solar 2-Dec-13 ADB ADB China Loan Thermal Power Plant $150.00 Abstain Does not meet BHN criteria. 8, 36 B Yunnan Sustainable Road Maintenance 2-Dec-13 ADB ADB China Loan Sector project $80.00 Abstain Does not meet BHN criteria. 8, 36 B Java–Bali 500-Kilovolt Power 2-Dec-13 ADB ADB Indonesia Loan Transmission Crossing Project $224.00 Support 62 A 2-Dec-13 WB IFC Russia Blend Fuyao Russia $50.00 Support B Chipita Gida Uritim Anonim Sirketi fo 2-Dec-13 WB IFC Turkey Loan the Chipita Turkey Project $14.40 Support B Project for Food Security Consolidation through Development of Irrigation 3-Dec-13 AFDB ADF Mali Blend Farming (PRESA/DCI) $53.98 Support B Urban–Rural Integration Water 3-Dec-13 ADB ADB China Loan Distribution Project $100.00 Support Meets BHN criteria. 7 B Business Climate Improvement and 3-Dec-13 AFDB ADF Chad Blend Economic Diversification Project $8.83 Support C Project includes local content 3-Dec-13 IDB IIC Uruguay Loan Fingano S.A. and Vengano S.A. $10.00 Abstain requirements. 1 B Nacala Road Corridor Development 3-Dec-13 AFDB ADF Regional Blend Project - Phase IV $71.95 Support 62 A Non- Combined 2013-2017 Country Strategy 3-Dec-13 AFDB AFDF Niger Financial Paper and Portfolio Review $0.00 Support N/A Adobe Social Mezzanine Fund I Limited 3-Dec-13 IDB IIC Mexico Equity Partnership $2.50 Support FI Banco Santander (México) S.A., 3-Dec-13 IDB IIC Mexico Loan Institución -

Greece Retail Foods

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 6/27/2018 GAIN Report Number: IT1819 Greece Post: Rome Retail Foods Report Categories: Retail Foods Approved By: Fred Giles Prepared By: Dimosthenis Faniadis Report Highlights: In 2017, value sales of grocery retailers in Greece declined by 2.3 percent to $19.7 billion. The effects of the recession were still evident with low disposable incomes, low consumer confidence and high unemployment; yet the economy seemed to march towards stability. This was mirrored in retailing, as consumption began to pick up gradually. This report overviews the characteristics of Greek retail outlets and how best to place U.S. products in the Greek market. General Information: SECTION I. MARKET SUMMARY Overview Greece is the seventeenth largest economy in EU-28, accounting for 1.2 percent of the EU’s GDP for 2017, the same as Romania and Czech Republic. After a prolonged depression, the economy stabilized in 2017, and Greek GDP is estimated to grow approximately 1.0 percent, and 2.5 percent in 2018. Greece has a capitalist economy with a public sector accounting for about 40 percent of GDP, with tourism providing 18 percent of GDP. Greece is a major beneficiary of EU aid, equal to about 3.3 percent of annual GDP. With a population of 11 million and a gross domestic product (GDP) of approximately $204 billion, Greece is a relatively small country. Greece imports significantly more food and beverages than it exports and is reliant on imports to meet the demands of consumers for food products. -

10-07-2019 Serbia Outlines Orao Modernisation Programme

10-07-2019 Serbia outlines Orao modernisation programme 2019 - 07 - 03 - www.flightglobal.com Serbia’s defence ministry has detailed a Miloradovic says Belgrade has major upgrade programme being purchased Safran’s Sigma 95 inertial performed on its Soko J-22 Orao combat navigation system, which sources aircraft and NJ-22 trainers, which will indicate will be integrated with a mission significantly enhance the type’s computer and multifunctional displays operational capabilities. developed by local manufacturer Teleoptik-Ziroskopi. Speaking at the Partner 2019 exhibition in Belgrade in late June, Nenad The first phase of work will also integrate Miloradovic, the defence ministry’s new weapons. This process will enable assistant for defence technologies, the NJ-22 to be flown with a weapons confirmed that the modernisation activity system officer in the rear cockpit, so that – unofficially dubbed Orao 2.0 – will be the type can serve as a dedicated conducted in two phases. Work to be ground-attack asset. Miloradovic says the completed by the end of this year second phase of modernisation work will includes incorporating new navigation include ―complete digitalisation‖ of the and targeting systems in the rear cockpit aircraft’s cockpit, without revealing... of the two-seat NJ-22. Lire la suite APPELS D’OFFRES A330 Aircraft Spares 2019 - 07 - 10 - www.gebiz.gov.sg Ref: DEFNGPP7119100398 Organisme: MoD Date limite: 22.07.2019 Tel: 68194218 ; Fax: 6273 4823 E-mail: [email protected] Lire la suite Helicopter spare parts (4 years) 2019 - 07 -

The Western Balkans

������� ����������� ������� ������ ������� �������������� ������� ������ �������� The Western Balkans: ������� ������� ������ ����������� ������� ������� �������� Europe’s Next High-Value Location for Manufacturers ������� ����� ���������� ������ ����������� ��� ���������� �������� ��� ������� ��������� ������ r Now is a strategic time to invest in the Western Balkans r A new study of current investors analyzes operating costs and conditions r The European Investor Outreach Program (EIOP) helps investors consider their options and plan site visits ����������������� ���������������� As the EU expands, the focus is on the Western Balkans ������������������������� As the last frontier amid a rapidly integrating continent, the Western Balkans has emerged as Europe’s next high-growth destination for foreign direct investment (FDI). ���������������� ���� ����������������������� The region, now directly adjacent to the EU’s expanding border, has attracted the focus ���������������� of the leadership of the European Commission. It is expected that countries of the Western Balkans will enjoy membership in the EU within five to ten years. As has been demonstrated in the economic booms of recently acceded EU member countries, the period leading up to full EU integration is a strategic time for forward-looking investors to maximize their opportunity. An insiders’ perspective from current investors A recent benchmarking and competitiveness study* conducted by the Multilateral Investment Guarantee Agency (MIGA) of the World Bank Group substantiates -

Serbian Aerospace Industry Content 01 03 Aviation Strategy of the Republic of Serbia

Serbian Aerospace Industry Content 01 03 Aviation Strategy of the Republic of Serbia 04 Overview of Serbia 02 05 General Overview 06 Economic Indicators 07 Foreign Direct Investments 08 Applicable Laws and Regulations 09 Free Trade Agreements 11 Infrastructure 14 History of SerbianAerospace Industry 03 15 Serbian Aviation History 16 Air Transport 18 Aircraft Design and Development 19 Turbulent Years 20 The Renaissance 22 Highly Qualified Workforce 04 23 Labor Availability and Cost 26 Education 05 32 Company Directory 01Aviation Strategy of the Republic of Serbia Serbia has a long and rich history of designing and building commercial and military aircraft and aircraft components. Serbian made aircraft and aircraft components are present in all major markets, and Serbian Serbia has a long and rich aerospace professionals are highly sought after by world’s leading aerospace companies. history of designing and Main strategic objectives for the Serbian aviation industry are: building commercial and Regional leadership in air transport through a strategic partnership between Air Serbia and Etihad; military aircraft and aircraft Expansion of the MRO capability, including both commercial and business jet markets, in line with EASA/ components. FAA Part 145 requirements; Return to the aircraft component manufacturing market at the levels present in 1990, in line with EASA/ FAA Part 21 requirements (POA); Growth of the aircraft development capability, concentrating on aircraft structure, electrical and hydraulic systems and avionics software and hardware in line with EASA/FAA Part 21 requirements (DOA); Modern and market-leading air navigation services provision through the national provider SMATSA; Full membership in EASA; Modernization of the educational programs and facilities (K12 to university level); Return of Serbia’s top aerospace professionals from abroad; Employment of 4,000 additional workers over the next 5 years.