AWS Sees Growth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tata Sky Channel List

Sr. No. Channel Name HD/SD Genre EPG No. FTA/Pay MRP MRP + Tax NCF Counter 1 DD National SD Hindi Entertainment 114 FTA FTA FTA 0 2 Star Plus HD HD Hindi Entertainment 115 Pay ₹ 19.00 ₹ 22.42 2 3 Star Plus SD Hindi Entertainment 117 Pay ₹ 19.00 ₹ 22.42 1 4 Star Bharat HD HD Hindi Entertainment 121 Pay ₹ 19.00 ₹ 22.42 2 5 Star Bharat SD Hindi Entertainment 122 Pay ₹ 10.00 ₹ 11.80 1 6 SET HD HD Hindi Entertainment 128 Pay ₹ 19.00 ₹ 22.42 2 7 SET SD Hindi Entertainment 130 Pay ₹ 19.00 ₹ 22.42 1 8 Sony SAB HD HD Hindi Entertainment 132 Pay ₹ 19.00 ₹ 22.42 2 9 Sony SAB SD Hindi Entertainment 134 Pay ₹ 19.00 ₹ 22.42 1 10 &TV HD HD Hindi Entertainment 137 Pay ₹ 19.00 ₹ 22.42 2 11 &TV SD Hindi Entertainment 139 Pay ₹ 12.00 ₹ 14.16 1 12 Zee TV HD HD Hindi Entertainment 141 Pay ₹ 19.00 ₹ 22.42 2 13 Zee TV SD Hindi Entertainment 143 Pay ₹ 19.00 ₹ 22.42 1 14 Colors HD HD Hindi Entertainment 147 Pay ₹ 19.00 ₹ 22.42 2 15 Colors SD Hindi Entertainment 149 Pay ₹ 19.00 ₹ 22.42 1 16 UTV Bindass SD Hindi Entertainment 153 Pay ₹ 1.00 ₹ 1.18 1 17 Investigation Discovery SD Hindi Entertainment 155 Pay ₹ 1.00 ₹ 1.18 1 18 Naaptol SD Shopping 156 FTA FTA FTA 0 19 Ezmall SD Others 158 FTA FTA FTA 0 20 Star Utsav SD Hindi Entertainment 171 Pay ₹ 1.00 ₹ 1.18 1 21 Zee Anmol SD Hindi Entertainment 172 Pay ₹ 0.10 ₹ 0.12 1 22 Colors Rishtey SD Hindi Entertainment 173 Pay ₹ 1.00 ₹ 1.18 1 23 Sony Pal SD Hindi Entertainment 174 Pay ₹ 1.00 ₹ 1.18 1 24 The Q India SD Hindi Entertainment 175 FTA FTA FTA 0 25 Big Magic SD Hindi Entertainment 176 Pay ₹ 0.10 ₹ 0.12 1 26 Dangal -

Channel List

Channel List: - Channels, EPG numbers and prices are subject to change. - MRP: Maximum Retail Price, per month. DRP (Distributor Retail Price) of all channels is the same as the MRP. - Pack lock-in duration: 1 day Sr. Channel Name HD/SD Genre EPG No. FTA/Pay MRP MRP + Tax No. 1 DD National SD Hindi Entertainment 114 FTA FTA FTA 2 Star Plus HD HD Hindi Entertainment 115 Pay ₹ 19.00 ₹ 22.42 3 Star Plus SD Hindi Entertainment 117 Pay ₹ 19.00 ₹ 22.42 4 Star Bharat HD HD Hindi Entertainment 121 Pay ₹ 19.00 ₹ 22.42 5 Star Bharat SD Hindi Entertainment 122 Pay ₹ 10.00 ₹ 11.80 6 SET HD HD Hindi Entertainment 128 Pay ₹ 19.00 ₹ 22.42 7 SET SD Hindi Entertainment 130 Pay ₹ 19.00 ₹ 22.42 8 Sony SAB HD HD Hindi Entertainment 132 Pay ₹ 19.00 ₹ 22.42 9 Sony SAB SD Hindi Entertainment 134 Pay ₹ 19.00 ₹ 22.42 10 &TV HD HD Hindi Entertainment 137 Pay ₹ 19.00 ₹ 22.42 11 &TV SD Hindi Entertainment 139 Pay ₹ 12.00 ₹ 14.16 12 Zee TV HD HD Hindi Entertainment 141 Pay ₹ 19.00 ₹ 22.42 13 Zee TV SD Hindi Entertainment 143 Pay ₹ 19.00 ₹ 22.42 14 Colors HD HD Hindi Entertainment 147 Pay ₹ 19.00 ₹ 22.42 15 Colors SD Hindi Entertainment 149 Pay ₹ 19.00 ₹ 22.42 16 UTV Bindass SD Hindi Entertainment 153 Pay ₹ 1.00 ₹ 1.18 17 Investigation Discovery SD Hindi Entertainment 155 Pay ₹ 1.00 ₹ 1.18 18 Naaptol SD Shopping 156 FTA FTA FTA 19 Ezmall SD Others 158 FTA FTA FTA 20 Star Utsav SD Hindi Entertainment 171 Pay ₹ 1.00 ₹ 1.18 21 Zee Anmol SD Hindi Entertainment 172 Pay ₹ 0.10 ₹ 0.12 22 Colors Rishtey SD Hindi Entertainment 173 Pay ₹ 1.00 ₹ 1.18 23 Sony Pal SD Hindi Entertainment -

Zeel – Rio (Mrp) – Version 2/2020

ZEEL – RIO (MRP) – VERSION 2/2020 AMENDMENT AGREEMENT FOR MODIFICATION OF SUBSCRIBED ZEE GROUP CHANNELS AND/OR ZEE BOUQUETS This Amendment Agreement (“Amendment Agreement”) for modification of subscribed Zee Group Channels and/or Zee Bouquets is made on this _______ day of ______, by and between: ZEE ENTERTAINMENT ENTERPRISES LIMITED, a company incorporated under the provisions of the Companies Act, 2013 (as amended) having Corporate Identification Number (CIN): L92132MH1982PLC028767 and having its registered office at 18th Floor, A Wing, Marathon Futurex, N.M. Joshi Marg, Lower Parel (East), Mumbai – 400013 and Delhi office at B-10, Essel House, Lawrence Road, New Delhi- 110035 (hereinafter referred to as “ZEEL” which expression unless repugnant to the context or meaning thereof, shall mean and include its successors and permitted assigns) of the ONE PART, AND MSO/ DTH Operator/ HITS Operator/IPTV Operator (M/s): _______________________________________________________________________ Legal Status: Company Partnership Firm Proprietorship Firm Individual HUF LLP (hereinafter referred to as the “Distribution Platform Operator” or “DPO”) which expression shall unless it be repugnant to the meaning or context thereof, be deemed to include the heirs, executors and administrators in the case of a sole proprietorship; the successors and permitted assigns in the case of a company; the partner or partners for the time being and the heirs, executors and administrators of the last surviving partner in the case of a partnership firm; and Karta and -

A New Vision Is Blooming

A NEW VISION IS BLOOMING ZEE 4.0 - ANNUAL REPORT 2020-21 Zee Entertainment Enterprises Limited Transformation stems from the natural evolution of every living being. Inside each of us lies a distinctive desire to do something more than the norm, out of the ordinary. This nature of existence flows from people to businesses, leading them from old path to new, creating opportunities for themselves and for the rest of the world. Media and Entertainment landscape is not untouched by this phenomenon. From consumer FINANCIAL behaviour to consumer experiences, the industry has evolved in all shapes and forms over STATEMENTS the last few decades. Today, we are seeing a paradigm shift in the consumption and delivery 03 of entertainment. In this new realm, the alchemy of the consumer experience is one that blends content creation, delivery, and monetization in a seamless manner. This hyper- STANDALONE competitive, digitally accelerated environment demands a unique strategic vision. We at ZEE INDEX Independent Auditor’s Report 107 are preparing to step into this future with a sharper and synergised version, transforming into ZEE 4.0 - a future-ready organisation to gain competitive advantage. ZEE 4.0 is Balance Sheet 115 designed around enhanced customer centricity with levers for capitalizing on Statement of Profit and Loss 116 immense growth opportunities and driving higher profitability. COMPANY Statement of Cash Flow 117 OVERVIEW The 5G pillars - Governance, Granularity, Growth, Goodwill and Gusto, form 01 Statement of Changes in Equity 119 the cornerstone of ZEE 4.0, sharpening our abilities to capture the emerging Notes 121 opportunities across markets, to transform ZEE into South Asia’s leading Media & Key Performance Indicators 04 STATUTORY Entertainment Company. -

NXTDIGITAL-HITS LCN (SOUTH)-LCN GENRE.Xlsx

NXTDIGITAL HITS - SOUTH * Please note that channels will be available subject to the model of COPE (Cable Operator Premise Equipment ). SR. NO NAME OF CHANNEL LCN 1UDAYA TV 4 2 STAR SUVARNA HD 5 3SUVARNA 6 4 ZEE KANNADA HD 7 5ZEE KANNADA 8 6 UDAYA MOVIES 11 7 UDAYA COMEDY 12 8 DANGAL KANNADA 13 9 COLORS KANNADA HD 14 10 COLORS KANNADA 15 11 COLORS SUPER 16 12LOCAL 1 21 13LOCAL 2 22 14DD CHANDANA 24 15ALL TIME 25 16AYUSH TV 26 17 SUVARNA PLUS 31 18ZEE PICCHAR 33 19 PUBLIC MOVIES 35 20 COLORS KANNADA CINEMA 36 21LOCAL 3 39 22LOCAL 4 40 23 RAJ NEWS KANNADA 43 24 SUVARNA NEWS 24X7 45 25TV9 KANNADA 47 26 KASTHURI NEWS 24 48 27PRAJA TV 49 28PUBLIC TV 50 29 DIGHVIJAYA 24X7 51 30 NEWS18 KANNADA 53 31BTV NEWS 54 32 NEWSX KANNADA 55 33TV5 KANNADA 56 34POWER TV 58 35UDAYA MUSIC 65 36 PUBLIC MUSIC 67 37 NAAPTOL BLUE 69 38 NAAPTOL KANNADA 71 39SRI SANKARA 74 40SHEKINAH 76 41LOCAL 5 81 42LOCAL 6 82 43LOCAL 7 83 44LOCAL 8 84 45LOCAL 9 85 46LOCAL 10 86 47LOCAL 11 87 48LOCAL 12 88 49LOCAL 13 89 50LOCAL 14 90 51LOCAL 15 91 52LOCAL 16 92 53LOCAL 17 93 54LOCAL 18 94 55LOCAL 19 95 56LOCAL 20 96 57STAR PLUS 100 58 CUSTOMER INFO 101 59NXT TARANG 102 60 SUNFLOWER KIDS 105 61NXT TOONS 106 62NXT RHYMES 107 63 NXT KIDS MOVIES 108 64 NXT STUDIO 1 109 65 NXT STUDIO 2 110 66FILMI GANE 111 67 NXT SONGDEW 112 68 BOLLYWOOD HITZ 113 69NXT K-POP 114 70 NXT K-WORLD 115 71 COMEDY 24X7 116 72 NXT COOKING 117 73HARIOM TV 118 74IBAADAT TV 119 75 NXT HOLLYWOOD ACTION 120 76 NXT HOLLYWOOD MOVIES 121 77 NXT SOUTH ACTION 122 78 NXT MALAYALAM 123 79NXT TAMIL 124 80NXT TELUGU 125 -

Declaration Under Section 4 (4) of the Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No

Declaration Under Section 4 (4) of The Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No. 1 of 2017) 4(4)a: Target Market States/Parts of State covered as "Coverage Area" 1. Karnataka 2.Maharashtra 3.Goa 4(4)b: Total Channel carrying capacity Distribution Network Location Capacity in SD Terms Bengaluru (Karnataka) 476 Hubballi (Karnataka) 462 Belagavi (Karnataka) 524 Solapur (Maharashtra) 525 NashiK (Maharashtra) 491 Goa 462 Kindly Note: 1. Local Channels considered as 1 SD; 2. Consideration in SD Terms is clarified as 1 SD = 1 SD; 1 HD = 2 SD; 3. Number of channels will vary within the area serviced by a distribution network location depending upon available Bandwidth capacity 4(4)c: List of channels available on network List attached below in Annexure I 4(4)d: Number of channels which signals of television channels have been requested by the distributor from broadcasters and the interconnection agreements signed Nil 4(4)e: Spare channels capacity available on the network for the purpose of carrying signals of television channels Distribution Network Location Spare Channel Capacity in SD Terms Bengaluru Nil Hubballi Nil Belagavi 50 Solapur 50 NashiK Nil Goa Nil 4(4)f: List of channels, in chronological order, for which requests have been received from broadcasters for distribution of their channels, the interconnection agreements have been signed and are pending for distribution due to non-availability of the spare channel capacity Nil ANNEXURE I Distribution Network Location: -

Declaration Under Section 4 (4) of the Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No

Version 3/202104 Declaration Under Section 4 (4) of The Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No. 1 of 2017) 4(4)a: Target Market States/Parts of State covered as "Coverage Area" 1. Andhra Pradesh 2. Assam 3. Delhi 4. Haryana 5. Karnataka 6. Madhya Pradesh 7. Maharashtra 8. Odisha 9. Rajasthan 10. Sikkim 11. Telangana 12. Tripura 13. Uttar Pradesh 14. Uttarakhand 15. West Bengal 4(4)b: Total Channel carrying capacity Distribution Network Location Capacity in SD Terms Bangalore 506 Bhopal 358 Delhi 384 Hyderabad 456 Kolkata 472 Mumbai 447 Kindly Note: 1. Local Channels considered as 1 SD; 2. Consideration in SD Terms is clarified as 1 SD = 1 SD; 1 HD = 2 SD; 3. Number of channels will vary within the area serviced by a distribution network location depending upon available Bandwidth capacity. Page 1 of 39 Version 3/202104 4(4)c: List of channels available on network List attached below in Annexure I 4(4)d: Number of channels which signals of television channels have been requested by the distributor from broadcasters and the interconnection agreements signed Nil 4(4)e: Spare channels capacity available on the network for the purpose of carrying signals of television channels Distribution Network Location Spare Channel Capacity in SD Terms Bangalore Nil Bhopal Nil Delhi Nil Hyderabad Nil Kolkata Nil Mumbai Nil 4(4)f: List of channels, in chronological order, for which requests have been received from broadcasters for distribution of their channels, the interconnection -

LCN Home Channel 1 SD 100 Star Plus SD 101 ZEE TV SD 103 &Tv SD 104 Colors SD 105 DANGAL SD 106 Star Bharat SD 107 SET SD 109 Dr

Channel Name SD/HD LCN Home Channel 1 SD 100 Star Plus SD 101 ZEE TV SD 103 &tv SD 104 colors SD 105 DANGAL SD 106 Star Bharat SD 107 SET SD 109 Dr. Shuddhi SD 110 ID SD 111 Big Magic SD 112 SONY SAB SD 113 ABZY Cool SD 114 ZEE ANMOL SD 116 d2h Positive SD 117 EZ MALL SD 118 bindass SD 120 colors rishtey SD 121 Shemaroo TV SD 123 Anjan SD 128 Ayushman Active SD 130 Comedy Active SD 131 Fitness Active SD 132 Thriller Active SD 134 Shorts TV Active SD 135 Korean Drama Active SD 136 Watcho SD 144 Cooking Active SD 146 Zee Zest SD 147 DD NATIONAL SD 149 DD Retro SD 151 STAR UTSAV SD 156 SONY PAL SD 159 TOPPER SD 160 STAR WORLD SD 179 ZEE cafe SD 181 Colors Infinity SD 183 COMEDY CENTRAL SD 185 ZEEPLEX Screen 1 SD 200 SONY MAX SD 201 &pictures SD 202 ZEE CINEMA SD 203 Jyotish Duniya SD 204 Star GOLD SD 205 ABZY MOVIES SD 206 UTV MOVIES SD 207 B4U Kadak SD 210 UTV ACTION SD 211 Box Cinema SD 212 Cine Active SD 213 Rangmanch Active SD 214 Evergreen Classics Active SD 215 Hits Active SD 217 ZEE Bollywood SD 218 EZ MALL SD 219 colors cineplex SD 221 Movies Active SD 222 Housefull Movies SD 223 enterr 10 Movies SD 225 ABZY Dhadkan SD 226 Star Gold 2 SD 227 ZEE Action SD 228 B4U MOVIES SD 229 Star Gold Select SD 231 Star Utsav Movies SD 234 EZ MALL SD 235 Zee Anmol Cinema SD 237 Dr. -

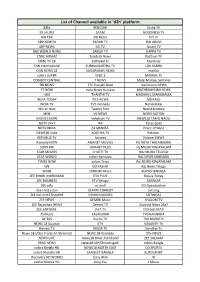

List of Channel Available in 'D2h' Platform

List of Channel available in 'd2h' platform &flix RENGONI Disha TV 9X JALWA SAAM GOODNESS TV AAJ TAK DD Retro hm tv ABP ASMITA SAFARI TV ISAI ARUVI ABP NEWS SAI TV Janam TV BBC WORLD NEWS SAKSHI TV KAPPA TV CNBC AWAAZ Sandesh News Kasthuri TV CNBC TV 18 Sathiyam tv Kaumudy CNN International SUBHAVAARTHA TV LOK SABHA CNN NEWS 18 SUDARSHAN NEWS madha colors SUPER SVBC 2 MAKKAL TV COMEDY CENTRAL T NEWS Malai Murasu Seithikal DD NEWS PTC Punjabi Gold manorama NEWS ET NOW India News Haryana MATHRUBHUMI NEWS HBO THANTHI TV MAZHAVIL MANORAMA INDIA TODAY TV 5 NEWS MURASU INDIA TV TV5 Kannada Nambikkkai Mirror Now Twenty Four News18 Kerala MNX V6 NEWS NEWS NATION MOVIES NOW Velicham TV NEWS18 TAMIL NADU NDTV 24x7 WE Paras Gold NDTV INDIA 24 GHANTA Peace of Mind NEWS18 India ADITHYA TV Polimer REPUBLIC TV Asianet Polimer NEWS Romedy NOW ASIANET MOVIES PUTHIYA THALAIMURAI SONY PIX ASIANET PLUS raj MUSIX MALAYALAM STAR MOVIES CHUTTI TV RAJ MUSIX TELUGU STAR WORLD colors Kannada RAJ NEWS KANNADA TIMES NOW colors Oriya Raj NEWS MALAYALAM WB DD KASHIR Raj News Telugu WION DHOOM Music RUPASI BANGLA ZEE BIHAR JHARKHAND ETV PLUS Russia Today ZEE BUSINESS ETV Telugu SANSKAR ZEE cafe ez mall DD Gyandarshan Zee Hindustan GEMINI COMEDY Satsang ZEE MP CHATTISGARH GEMINI MOVIES SEITHIGAL ZEE NEWS GEMINI Music SHALOM TV ZEE Rajasthan NEWS Gemini TV Suvarna News 24x7 ZEE SARTHAK JAYA TV TV9 GUJARATI 7S Music KALAIGNAR TV9 KANNADA DY 365 Kochu TV TV9 MARATHI NEWS 18 Gujarati KTV VASANTH TV Harvest TV MEGA TV Vendhar Tv News 18 Uttar Pradesh Uttranchal NEWS 18 Kannada -

NXTDIGITAL-HITS LCN (Rest of India) -LCN GENRE.Xlsx

NXTDIGITAL HITS - Rest of India General * Please note that channels will be available subject to the model of COPE (Cable Operator Premise Equipment ). SR. NO NAME OF CHANNEL LCN 1STAR PLUS 100 2 CUSTOMER INFO 101 3 NXT TARANG 102 4 SUNFLOWER KIDS 105 5NXT TOONS 106 6 NXT RHYMES 107 7 NXT KIDS MOVIES 108 8 NXT STUDIO 1 109 9 NXT STUDIO 2 110 10FILMI GANE 111 11 NXT SONGDEW 112 12 BOLLYWOOD HITZ 113 13NXT K-POP 114 14 NXT K-WORLD 115 15 COMEDY 24X7 116 16 NXT COOKING 117 17HARIOM TV 118 18IBAADAT TV 119 19 NXT HOLLYWOOD ACTION 120 20 NXT HOLLYWOOD MOVIES 121 21 NXT SOUTH ACTION 122 22 NXT MALAYALAM 123 23NXT TAMIL 124 24NXT TELUGU 125 25NXT BENGALI 126 26 NXT BHOJPURI 127 27 NXT BHOJPURI SONGS 128 28 NXT HOLLYWOOD BENGALI 129 29LOCAL 1 130 30LOCAL 2 131 31LOCAL 3 132 32LOCAL 4 133 33LOCAL 5 134 34LOCAL 6 135 SR. NO NAME OF CHANNEL LCN 35LOCAL 7 136 36LOCAL 8 137 37LOCAL 9 138 38LOCAL 10 139 39LOCAL 11 140 40LOCAL 12 141 41LOCAL 13 142 42LOCAL 14 143 43LOCAL 15 144 44LOCAL 16 145 45LOCAL 17 146 46LOCAL 18 147 47LOCAL 19 148 48LOCAL 20 149 49 STAR PLUS HD 155 50ZEE TV HD 159 51ZEE TV 160 52 COLORS HD 161 53 COLORS 162 54 SONY HD 163 55 SONY 164 56& TV HD 165 57& TV 166 58 STAR BHARAT HD 167 59 STAR BHARAT 168 60 SONY SAB HD 169 61 SAB TV 170 62BIG MAGIC 171 63 COLORS RISHTEY 172 64ZEE ANMOL 173 65 DANGAL TV 174 66ENTERR10 175 67STAR UTSAV 176 68 SONY PAL 177 69 ENTERR10 178 70BINDASS 181 71E24 182 SR. -

Hathway Recommended Pack

HATHWAY RECOMMENDED PACK KARNATAKA Prices are excluding taxes INFINITY HD MRP : ₹ 668 (142 PAY CHANNELS + KARNATAKA FTA) Total Pay Channels 78 SD + 64 HD (Excluding tax) LANG - GENRE CHANNEL_NAME SD/HD Bengali - Gec SONY AATH SD English - Gec STAR WORLD HD HD English - Gec STAR WORLD PREMIERE HD HD English - Gec ZEE CAFE HD HD English - Infotainment TLC HD HD English - Kids BABY TV HD HD English - Kids NICK JR SD English - Movie &FLIX HD HD English - Movie &PRIVE HD HD English - Movie HBO HD HD English - Movie MN+ HD HD English - Movie MNX HD HD English - Movie MOVIES NOW HD HD English - Movie ROMEDY NOW HD HD English - Movie SONY PIX HD HD English - Movie STAR MOVIES HD HD English - Movie STAR MOVIES SELECT HD HD English - Movie WB SD English - Music VH1 HD HD English - News BBC WORLD NEWS SD English - News CNBC TV18 SD English - News CNN INTERNATIONAL SD English - News CNN NEWS18 SD English - News ET NOW SD English - News INDIA TODAY SD English - News MIRROR NOW SD English - News NDTV 24X7 SD English - News NDTV PROFIT SD English - News TIMES NOW SD English - News TIMES NOW WORLD HD HD English - Sports EUROSPORT HD HD Hindi - Gec &TV HD HD Hindi - Gec BIG MAGIC SD Page 1 of 98 Hindi - Gec COLORS HD HD Hindi - Gec COLORS RISHTEY SD Hindi - Gec INVESTIGATION DISCOVERY HD HD Hindi - Gec SONY HD HD Hindi - Gec SONY PAL SD Hindi - Gec SONY SAB HD HD Hindi - Gec ZEE ANMOL SD Hindi - Gec ZEE TV HD HD Hindi - Infotainment HISTORY TV18 HD HD Hindi - Kids CARTOON NETWORK SD Hindi - Kids NICK SD Hindi - Kids NICK HD+ HD Hindi - Kids POGO SD Hindi -

Zeel – Rio (Mrp) –Version 2/2020

ZEEL – RIO (MRP) –VERSION 2/2020 Application Form [Request for subscription to Zee Group Channels and/or Zee Bouquets under sub-regulation (5) and (6) of Regulation 10 of the Interconnection Regulations by MSO/DTH Operator/HITs Operator/IPTV Operator (“DPO”)] DATE:______________ 1. Name of the DPO: ______________________________________________________________ 2. Platform: _____________________________________________________________________ 3. The name(s) of Owners/Directors/Partners of the DPO:_________________________________ 4. Registered Office address of DPO:_________________________________________________ 5. Complete Address for communication (with pincode): ____________________________________________________________________________ 6. Name of the contact person/ Authorized Representative (letter of authorization/Board Resolution enclosed):____________________________________________________________________ 7. Telephone :___________________________________________________________________ 8. Email address :________________________________________________________________ 9. Details of Head-end, Conditional Access Systems (CAS) and Subscriber Management Systems (SMS) deployed by DPO to be provided in Part A of the Annexure A hereto 10. Valid and authorized Website of the DPO with details set out in Regulation 4 of the Interconnection Regulations:__________________________________________________________________ 11. Documents to be uploaded/Attached along with the Application Form: a) Copy of certificate of registration/ permission/