Nber Working Paper Series Us Monetary Policy and The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Jyske Bank H1 2014 Agenda

Jyske Bank H1 2014 Agenda • Jyske Bank in brief • Jyske Banks Performance 1968-2013 • Merger with BRFkredit • Focus in H1 2014 • H1 2014 in figures • Capital Structure • Liquidity • Credit Quality • Strategic Issues • Macro Economy & Danish Banking 2013-2015 • Danish FSA • Fact Book 2 Jyske Bank in brief 3 Jyske Bank in brief Jyske Bank focuses on core business Description Branch Network • Established and listed in 1967 • 2nd largest Danish bank by lending • Total lending of DKK 344bn • 149 domestic branches • Approx. 900,000 customers • Business focus is on Danish private individuals, SMEs and international private and institutional investment clients • International units in Hamburg, Zürich, Gibraltar, Cannes and Weert • A de-centralised organisation • 4,352 employees (end of H1 2013) • Full-scale bank with core operations within retail and commercial banking, mortgage financing, customer driven trading, asset management and private banking • Flexible business model using strategic partnerships within life insurance (PFA), mortgage products (DLR), credit cards (SEB), IT operations (JN Data) and IT R&D (Bankdata) 4 Jyske Bank in brief Jyske Bank has a differentiation strategy “Jyske Differences” • Jyske Bank wants to be Denmark’s most customer-oriented bank by providing high standard personal financial advice and taking a genuine interest in customers • The strategy is to position Jyske Bank as a visible and distinct alternative to more traditional providers of financial services, with regard to distribution channels, products, branches, layout and communication forms • Equal treatment and long term relationships with stakeholders • Core values driven by common sense • Strategic initiatives: Valuebased management Differentiation Risk management Efficiency improvement Acquisitions 5 1990 1996 2002 2006 (Q4) 2011/2012 Jyske Bank performance 1968-2013 6 ROE on opening equity – 1968-2013 Pre-tax profit Average: (ROE on open. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Beholdningsoversigt 31.03.2021 Jyske Bank.Xlsx

INSTRUMENT_TYPE ISIN ISSUER_NAME Formue Københavns Kommune i kr. 4.069.081.439,62 Equity GB00B0SWJX34 London Stock Exchange Group PLC 1.701.893,31 Equity GB00B24CGK77 Reckitt Benckiser Group PLC 3.564.881,56 Equity AU000000SYD9 Sydney Airport 1.337.059,47 Equity JP3435000009 Sony Corp 6.910.276,86 Equity US0091581068 Air Products and Chemicals Inc 3.520.243,74 Equity US87918A1051 Teladoc Health Inc 1.795.360,11 Equity NL0012169213 QIAGEN NV 1.219.259,56 Equity US12504L1098 CBRE Group Inc 1.615.018,42 Equity FR0013154002 Sartorius Stedim Biotech 1.136.250,30 Equity CH0432492467 Alcon Inc 1.661.975,62 Equity FR0000121667 EssilorLuxottica SA 2.339.599,76 Equity CH0010645932 Givaudan SA 2.497.439,42 Equity CH0013841017 Lonza Group AG 2.547.489,13 Equity FR0010533075 Getlink SE 1.081.032,87 Equity AU0000030678 Coles Group Ltd 1.716.338,55 Equity NO0003054108 Mowi ASA 988.624,03 Equity GB00BHJYC057 InterContinental Hotels Group PLC 1.324.892,92 Equity NL0013267909 Akzo Nobel NV 2.081.864,14 Equity CA12532H1047 CGI Inc 1.974.562,46 Equity SE0012455673 Boliden AB 1.168.396,04 Equity BMG475671050 IHS Markit Ltd 1.720.814,54 Equity CA82509L1076 Shopify Inc 5.815.734,65 Equity CA7677441056 Ritchie Bros Auctioneers Inc 1.079.486,62 Equity JP3198900007 Oriental Land Co Ltd/Japan 2.377.930,50 Equity US6516391066 Newmont Corp 3.214.940,55 Equity IE00BK9ZQ967 Trane Technologies PLC 1.962.517,98 Equity GB00B39J2M42 United Utilities Group PLC 1.586.616,23 Equity US0036541003 ABIOMED Inc 1.469.304,62 Equity US9553061055 West Pharmaceutical Services Inc 1.484.522,98 -

EMTN-2020-Prospectus.Pdf

Prospectus JYSKE BANK A/S (incorporated as a public limited company in Denmark) U.S.$8,000,000,000 Euro Medium Term Note Programme On 22 December 1997, the Issuer (as defined below) entered into a U.S.$1,000,000,000 Euro Medium Term Note Programme (the “Programme”). This document supersedes the Prospectus dated 11 June 2019 and any previous Prospectus and/or Offering Circular. Any Notes (as defined below) issued under the Programme on or after the date of this Prospectus are issued subject to the provisions described herein. This Prospectus does not affect any Notes issued before the date of this Prospectus. Under the Programme, Jyske Bank A/S (the “Issuer”, “Jyske Bank” or the “Bank”) may from time to time issue notes (the ”Notes”), which may be (i) preferred senior notes (“Preferred Senior Notes”), (ii) non-preferred senior notes (“Non-Preferred Senior Notes”), (iii) subordinated and, on issue, constituting Tier 2 Capital (as defined in the Terms and Conditions of the Notes) (“Subordinated Notes”) or (iv) subordinated and, on issue, constituting Additional Tier 1 Capital (as defined in the Terms and Conditions of the Notes) (“Additional Tier 1 Capital Notes”) as indicated in the applicable Final Terms (as defined below). Notes may be denominated in any currency (including euro) agreed between the Issuer and the relevant Dealer (as defined below). The maximum aggregate principal amount of all Notes from time to time outstanding under the Programme will not exceed U.S.$8,000,000,000 (or its equivalent in other currencies calculated as described herein), subject to any increase as described herein. -

Jyske Bank Q4 2020

Jyske Bank Q4 2020 23 February 2021 2020 in brief Clients experienced Negative rates – for better or worse All Progress Counts A changing organisation • More online meetings. • More clients began to invest • Own wind turbine to offset CO2 • An organisational change in the instead of having cash deposits. emission from direct and development organisation with • More specialists. indirect power consumption a view to becoming even more • To an increasing degree, the covered by means of own agile. • Fewer branches to visit. negative interest rate renewable energy production. environment was reflected in • Organisational changes in • A brand new mobile banking deposit rates for personal • First estimate of CO e emission Personal Clients to become platform. 2 clients. from business volumes. more focused and specialized. • Increased flexibility with Jyske • Targets for sustainability in all Frihed. • Advantageous interest rates • Many employees experienced and remortgaging opportunities material business areas. changed working conditions due for home owners remained. to COVID-19. • Energy loans and CO2 calculator facilitating energy retrofitting. • The sale of Jyske Bank Gibraltar • A new equity fund offering more was finalized. sustainable investment solutions. • New VISA card without Dankort. COVID-19 • Lockdown and restrictions affected Danish society in 2020. • Clients received individual advice and guidance about the COVID-19 situation. • Jyske Bank's employees were most flexible and adaptive, and the bank remained accessible. • A COVID-19 -

Remuneration for Bank Executives

Remuneration for bank execu- tives A study on the impacts of corporate governance codes on executive re- muneration in Sweden, Denmark and the United Kingdom between 2004 and 2010 Degree Project within Business Administration Author: Andreas Klang and Niclas Kristoferson Tutor: Assoc. Prof. Dr. Dr. Petra Inwinkl Jönköping May 2011 Acknowledgements The process of this degree project, would not have been what it is without a number of people whom have contributed and played a part in shaping it to what it is today We would like to thank our tutor Assoc. Prof. Dr. Dr. Petra Inwinkl for herr advice and guidance throughout the process of the whole thesis. This thesis would not have been the same without her influential ideas and constructive criticism. We would also like to thank our seminare partners for their constructive feedback dur- ing all seminars. At last we would like to thank our families and girlfriends whom have endure us during the past six months with constant support and love. Andreas Klang Niclas Kristoferson Division of work The authors of the Remuneration for bank executives, a study on the impacts of corporate go- vernance codes on executive remuneration in Sweden, Denmark and the United Kingdom be- tween 2004 and 2010 are Andreas Klang and Niclas Kristoferson. Andreas Klang have done fif- ty per cent and Niclas Kristoferson have done fifty per cent. Degree Project within Business Administration Title: Remuneration for Bank Executive- A study on the impacts of corporate governance on executive remuneration Author: Andreas Klang and Niclas Kristoferson Tutor: Assoc. Prof. Dr. Dr. -

Can the Business Model of Handelsbanken Be an Archetype

The Journal of Applied Business Research – May/June 2014 Volume 30, Number 3 Can The Business Model Of Handelsbanken Be An Archetype For Small And Medium Sized Banks? A Comparative Case Study Morten Kousgaard Larsen, Aarhus University, Denmark Jacob Lange Nissen, Aarhus University, Denmark Rainer Lueg, Aarhus University, Denmark Christian Schmaltz, Aarhus University, Denmark & True North Institute, United Kingdom Joachim Røjkjær Thorhauge, Aarhus University, Denmark ABSTRACT The Danish Banking sector faces increasing requirements regarding regulation and profitability, which especially threatens small and medium sized banks. This study analyzes whether the successful business model of Handelsbanken (‘The Handelsbanken Way’) can serve as a blueprint for small and medium sized banks. We conduct a comparative case study by interviewing Handelsbanken and the disguised ‘Danish Local Bank’ (DLB). The DLB is a representative example of small and medium sized Danish banks. This study is structured according to the frameworks from business model implementations and from implied organizational structures. Using the notion of Osterwalder and Pigneur (2010), this study reveals only minor differences in the business models of Handelsbanken and DLB. Despite the supposedly obvious advantages of ‘The Handelsbanken Way,’ this study suggests that the financially troubled small and medium sized banks in Denmark will not necessarily benefit from the tactical choice of decentralization unless they incorporate specific adjustments. This study contributes to the existing theory if Handelsbanken’s approach to banking can improve the situation of financially troubled small and medium sized banks. Keywords: Business Model; Decentralization; Handelsbanken; Banking; Organizational Structure; Financial Crisis 1. INTRODUCTION ompared to other banking sectors in the EU, the Danish sector is marked by particularly fierce competition, leading to very low achievable profit margins (The Danish Bankers Association, 2007; C Weill, 2013). -

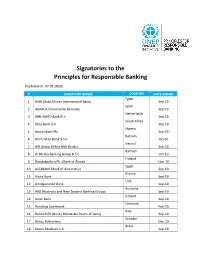

Signatories to the Principles for Responsible Banking

Signatories to the Principles for Responsible Banking (Updated on: 07.09.2020) # SIGNATORY BANKS COUNTRY DATE SIGNED Egypt 1 AAIB (Arab African International Bank) Sep-19 Spain 2 ABANCA Corporación Bancaria Sep-19 Netherlands 3 ABN AMRO Bank N.V. Sep-19 South Africa 4 Absa Bank Ltd. Sep-19 Nigeria 5 Access Bank Plc Sep-19 Bahrain 6 Ahli United Bank B.S.C Jan-20 Ireland 7 AIB Group (Allied Irish Banks) Sep-19 Bahrain 8 Al Baraka Banking Group B.S.C. Oct-19 Finland 9 Ålandsbanken Plc. (Bank of Åland) Nov-19 Egypt 10 ALEXBANK (Bank of Alexandria) Sep-19 Greece 11 Alpha Bank Sep-19 USA 12 Amalgamated Bank Sep-19 Australia 13 ANZ (Australia and New Zealand Banking Group) Sep-19 Iceland 14 Arion Bank Sep-19 Denmark 15 Aurskorg Sparebank Feb-20 Italy 16 Banca MPS (Banca Monte dei Paschi di Siena) Sep-19 Ecuador 17 Banco Bolivariano Dec-19 Brazil 18 Banco Bradesco S.A. Sep-19 Brazil 19 Banco da Amazônia Jan-20 Argentina 20 Banco de Galicia y Buenos Aires SA Sep-19 Ecuador 21 Banco de la Produccion S.A Produbanco Sep-19 Ecuador 22 Banco de Machala S.A. Sep-19 Mexico 23 Banco del Bajio, S.A. Aug-20 Ecuador 24 Banco Diners Club del Ecuador S.A. Nov-19 Nicaragua 25 Banco Grupo Promerica Nicaragua Sep-19 Ecuador 26 Banco Guayaquil Sep-19 El Salvador 27 Banco Hipotecario de El Salvador S.A. Sep-19 Ecuador 28 Banco Pichincha Sep-19 Dominican Republic 29 Banco Popular Dominicano Sep-19 Costa Rica 30 Banco Promerica Costa Rica Sep-19 Paraguay 31 Banco Regional Jul-20 Spain 32 Banco Sabadell Sep-19 Ecuador 33 Banco Solidario Nov-19 Colombia 34 Bancolombia -

Lazard Capital Fi PVC

Juli 2021 Lazard Capital FI SRI - PVC EUR Internationale Schuldverschreibungen und Forderungspapiere ISIN-Kennung * NIW in € Nettovermögen (in Mio. €) Nettogesamtvermögen (in Mio. €) PVC EUR-Anteile FR0010952788 2 181,19 328,16 1 019,50 * Nicht alle Anteilsklassen des jeweiligen Teilfonds sind registriert VERWALTUNG Overall Ziele und Anlagepolitik Der Fonds strebt eine Wertentwicklung nach Kosten an, die über dem Index Barclays Global Contingent Capital Hedged EUR Index für PVC EUR, PVD EUR, RVC EUR, RVD EUR, SC EUR und TVD EUR-Anteilen liegt, dem Barclays Global Contingent Capital Hedged USD Index für den PVC H-USD und dem Barclays Global Contingent Capital Hedged CHF Index für PVC H-CHF-Anteile durch eine aktive Verwaltung des Zins-, Kredit- und Wechselkursrisikos. Um dieses Verwaltungsziel zu erreichen, basiert die Strategie auf einer aktiven Verwaltung des Portfolios, das im Wesentlichen in nachrangigen Schuldtiteln angelegt ist (diese Schuldtitel sind risikoreicher als Senior-Schulden oder gesicherte Schuldtitel), sowie in von europäischen Finanzinstituten begebenen Titeln, der nicht als Stammaktien gelten. Das Verwaltungsverfahren verknüpft einen Top-down-Ansatz (strategisches und geografisches Allokationskonzept unter Berücksichtigung des makroökonomischen und sektoriellen Umfelds) mit einem Bottom-up-Ansatz (Auswahl von Anlageinstrumenten auf fundamentaler Basis nach Analyse der Bonität der Emittenten und der Wertpapiermerkmale), um so das regulatorische Umfeld, in dem sich diese Anlagekategorie entwickelt, zu integrieren. Die Zinssensitivität wird von 0 bis 8 verwaltet. Der Fonds investiert ausschließlich in Anleihen oder Wertpapiere, die von Emittenten begeben werden, deren Sitz sich in einem Mitgliedstaat der OECD befindet, und/oder in Emissionen oder Wertpapiere, die an einer Börse in einem dieser Länder notiert sind. Der OGA investiert ausschließlich in Anleihen, die in Euro, US-Dollar oder Pfund Sterling gehandelt werden. -

Dexia – Rise & Fall of a Banking Giant ______

DEXIA – RISE & FALL OF A BANKING GIANT __________________________________________________ LES ETUDES DU CLUB N° 100 DECEMBRE 2013 DEXIA – RISE & FALL OF A BANKING GIANT __________________________________________________ LES ETUDES DU CLUB N° 100 DECEMBRE 2013 Etude réalisée par Monsieur Nicholas Whitbeck (HEC 2013) sous la direction de Monsieur Ulrich Hege Professeur à HEC Paris Introduction .................................................................................................................................................... 3 I. How Dexia conquered the world ............................................................................................................ 4 A. Marriage of convenience ............................................................................................................................................... 4 B. Consolidation .................................................................................................................................................................. 6 C. Expansion in all directions ........................................................................................................................................... 8 D. Kempen & Labouchère – Dexia’s first warnings ................................................................................................... 10 E. Short-term liabilities fuelled the expansion of Dexia’s balance sheet ................................................................. 11 F. Under the leadership of Axel Miller, Dexia continued -

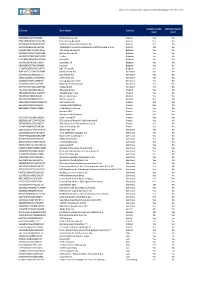

EBA List of Institutions for the Purpose of Supervisory Benchmarking (2021

EBA list of institutions for supervisory benchmarking as of 31 Dec 2020 Submits Credit Submits Market LEI Code Bank Name Country Risk? Risk? 529900S9YO2JHTIIDG38 BAWAG Group AG Austria Yes No PQOH26KWDF7CG10L6792 Erste Group Bank AG Austria Yes Yes 9ZHRYM6F437SQJ6OUG95 Raiffeisen Bank International AG Austria Yes Yes 529900IQMS1E10HN8V33 Volkskredit Verwaltungsgenossenschaft reg.Gen.m.b.H. Austria Yes No LSGM84136ACA92XCN876 AXA Bank Europe SA Belgium Yes No A5GWLFH3KM7YV2SFQL84 Belfius Banque SA Belgium Yes Yes 549300DYPOFMXOR7XM56 Crelan Belgium Yes No D3K6HXMBBB6SK9OXH394 Dexia NV Belgium No Yes 549300CBNW05DILT6870 Euroclear SA Belgium Yes No 5493008QOCP58OLEN998 Investar Belgium Yes No 213800X3Q9LSAKRUWY91 KBC Group NV Belgium Yes Yes MAES062Z21O4RZ2U7M96 Danske Bank A/S Denmark Yes Yes 529900PR2ELW8QI1B775 DLR Kredit A/S Denmark Yes No 3M5E1GQGKL17HI6CPN30 Jyske Bank A/S Denmark Yes No 213800UYAHIRLZ4NSN67 Lån og Spar Bank A/S Denmark Yes No LIU16F6VZJSD6UKHD557 Nykredit Realkredit A/S Denmark Yes Yes GP5DT10VX1QRQUKVBK64 Sydbank A/S Denmark Yes No 743700GC62JLHFBUND16 Aktia Bank Abp Finland Yes No 7437006WYM821IJ3MN73 Ålandsbanken Abp Finland Yes No 529900ODI3047E2LIV03 Nordea Bank Abp Finland Yes Yes 7437003B5WFBOIEFY714 OP Osuuskunta Finland Yes No R0MUWSFPU8MPRO8K5P83 BNP Paribas SA France Yes Yes 969500GVS02SJYG9S632 CARREFOUR BANQUE France Yes No 9695000CG7B84NLR5984 Crédit Mutuel Group France Yes No Groupe BPCE France Yes Yes Groupe Credit Agricole France Yes Yes F0HUI1NY1AZMJMD8LP67 HSBC France (*) France Yes Yes 96950001WI712W7PQG45 -

As of 10/31/2020

Annual Report | October 31, 2020 Vanguard Total International Bond Index Fund See the inside front cover for important information about access to your fund’s annual and semiannual shareholder reports. Important information about access to shareholder reports Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of your fund’s annual and semiannual shareholder reports will no longer be sent to you by mail, unless you specifically request them. Instead, you will be notified by mail each time a report is posted on the website and will be provided with a link to access the report. If you have already elected to receive shareholder reports electronically, you will not be affected by this change and do not need to take any action. You may elect to receive shareholder reports and other communications from the fund electronically by contacting your financial intermediary (such as a broker-dealer or bank) or, if you invest directly with the fund, by calling Vanguard at one of the phone numbers on the back cover of this report or by logging on to vanguard.com. You may elect to receive paper copies of all future shareholder reports free of charge. If you invest through a financial intermediary, you can contact the intermediary to request that you continue to receive paper copies. If you invest directly with the fund, you can call Vanguard at one of the phone numbers on the back cover of this report or log on to vanguard.com. Your election to receive paper copies will apply to all the funds you hold through an intermediary or directly with Vanguard.