SOUTHERN COMPANY 2015 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

20 Management's Report on Internal Control Over Financial Reporting 21 Report of Independent Registered Public Accounting Fi

FINANCIAL REVIEW SOUTHERN COMPANY AND SUBSIDIARY COMPANIES 2004 ANNUAL REPORT 20 Management’s report on internal control over 42 Consolidated statements of income financial reporting 43 Consolidated statements of cash flows 21 Report of Independent Registered Public Accounting 44 Consolidated balance sheets Firm–Internal Control over Financial Reporting 46 Consolidated statements of capitalization 22 Report of Independent Registered Public Accounting 48 Consolidated statements of common stockholders’ equity Firm–Consolidated Financial Statements 48 Consolidated statements of comprehensive income 23 Management’s discussion and analysis of results 49 Notes to financial statements of operations and financial condition 74 Selected consolidated financial and operating data 2000-2004 MANAGEMENT’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING Southern Company’s management is responsible for establishing financial reporting as of December 31, 2004. Deloitte & Touche and maintaining an adequate system of internal control over finan- LLP’s report, which expresses unqualified opinions on management’s cial reporting as required by the Sarbanes-Oxley Act of 2002 and assessment and on the effectiveness of Southern Company’s internal as defined in Exchange Act Rule 13a-15(f). A control system can control over financial reporting, is included herein. provide only reasonable, not absolute, assurance that the objectives of the control system are met. Under management’s supervision, an evaluation of the design and effectiveness of Southern Company’s internal control over financial reporting was conducted based on the framework in Internal David M. Ratcliffe Control–Integrated Framework issued by the Committee of Sponsor- Chairman, President, and Chief Executive Officer ing Organizations of the Treadway Commission (COSO). -

Investing in Failure How Large Power Companies Are Undermining Their Decarbonization Targets

Investing in Failure How Large Power Companies Are Undermining their Decarbonization Targets Prepared for Majority Action, March 9, 2020 Authors: Bruce Biewald, Devi Glick, Jamie Hall, Caitlin Odom, Cheryl Roberto, Rachel Wilson CONTENTS EXECUTIVE SUMMARY ............................................................................................... II 1. PURPOSE OF THE REPORT .................................................................................... 1 2. THE THREE COMPANIES PRODUCE 4 PERCENT OF ECONOMY-WIDE U.S. CO2 EMISSIONS ...... 1 3. THE COMPANIES HAVE AMBITIOUS DECARBONIZATION GOALS FOR 2030 AND 2050 .......... 7 4. DESPITE COMMITMENTS, THERE IS LITTLE PROGRESS .................................................. 8 4.1. The companies’ Status Quo Planning processes are not adequate .....................................9 4.2. The companies are not retiring aging and uneconomic coal plants fast enough ................ 11 4.3. The companies are unduly focused on traditional fossil generation to replace the coal assets they are retiring ................................................................................................... 20 4.4. The companies are underutilizing and underinvesting in renewables and distributed alternatives ................................................................................................................... 25 4.5. The companies’ grid modernization efforts are not equal to the task............................... 36 4.6. The companies’ corporate engagement is not aligned with decarbonization -

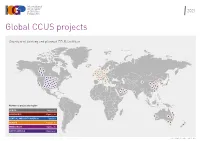

Global CCUS Projects

2021 Global CCUS projects Overview of existing and planned CCUS facilities 19 10 11 20 1 18 23 2 24 22 3 25 28 6 4 9 27 26 13 17 29 14 5 21 30 2 15 16 34 12 20 8 1 4 18 28 7 3 5 32 6 9 19 10 13 29 12 21 16 16 14 25 27 19 23 8 15 20 10 26 25 33 14 11 26 22 7 24 36 11 31 21 17 35 9 12 15 30 17 22 18 1 2 1 5 13 3 4 23 Number of projects by region 24 AFRICA 2 projects 4 ASIA PACIFIC 27 projects 1 5 1 7 3 8 CENTRAL AND SOUTH AMERICA 1 project 2 2 EUROPE 30 projects 6 27 MIDDLE EAST 5 projects NORTH AMERICA 36 projects Source: Global CCS Institute and IOGP data 19 10 11 20 1 18 23 2 24 22 3 25 28 6 4 9 27 26 13 17 29 14 5 21 30 2 15 16 34 12 20 8 1 4 LOCATION PROJECT NAME PROJECT TYPE INDUSTRY DESCRIPTION CO2 CAPTURED/ STARTING DATE STATUS OF PARTICIPANTS IOGP MEMBERS 18 28 7 3 5 32 6 9 19 YEAR (OPERATION) THE PROJECT INVOLVED 10 13 29 12 21 16 16 14 25 27 19 23 8 15 20 10 26 25 33 14 11 Australia Gorgon Carbon Industrial capture Natural gas Reservoir carbon dioxide vented from the Acid 3.4-4 Mtpa 2019 Operational Chevron (The Gorgon Project is Chevron, Shell, 26 22 7 24 36 11 31 21 17 35 9 12 Western Australia Dioxide Injection processing Gas Removal Units at the Gorgon gas processing operated by Chevron Australia and ExxonMobil 15 30 17 22 18 1 2 1 plant on Barrow Island are captured, compressed, is a joint venture of the Australian 5 13 3 4 23 transported by pipeline and injected over 2km below subsidiaries of Chevron (47.3%), the earth’s surface into the Dupuy Formation ExxonMobil (25%), Shell (25%), Osaka Gas (1.25%), Tokyo Gas (1%) and -

Policy Outlook for Carbon Capture in the 2020S

Policy Outlook for Carbon Capture in the 2020s NARUC Subcommittee on Clean Coal and Carbon Management / NARUC-DOE Carbon Capture, Utilization, and Storage Partnership JUNE 9, 2021| 2 – 3 PM (ET) WELCOME Commissioner Ellen Nowak Wisconsin Public Service Commission Vice Chair of the NARUC-DOE Carbon Capture, Utilization, and Storage Partnership and NARUC Subcommittee on Clean Coal and Carbon Management 2 SPEAKERS • Madelyn Morrison, External Affairs Manager, Carbon Capture Coalition • Emeka Richard Ochu, Research Associate, Center on Global Energy Policy, Columbia University • Angelos Kokkinos, Associate Deputy Assistant Secretary, Office of Clean Coal and Carbon Management, Office of Fossil Energy and Carbon Management, U.S. Department of Energy 3 Policy Outlook for Carbon Capture in the 2020s NARUC Subcommittee on Clean Coal and Carbon Management / NARUC-DOE Carbon Capture, Utilization, and Storage Partnership Wednesday, June 9, 2021 Madelyn Morrison External Affairs Manager Carbon Capture Coalition Unprecedented National Coalition in U.S. Energy & Climate Policy Goal: Economywide deployment of the full suite of carbon management options— carbon capture, removal, transport, utilization and storage—to reduce emissions, foster domestic energy and industrial production, and support high-wage jobs. Climate, jobs and energy/industrial benefits unite diverse interests in a common purpose Over 80 members, including companies, unions and environmental To learn more and view our NGOs complete membership list, visit www.carboncapturecoalition.org -

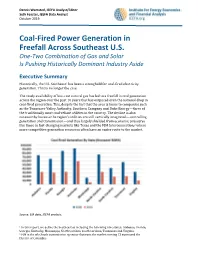

Coal-Fired Power Generation in Freefall Across Southeast U.S. One-Two Combination of Gas and Solar Is Pushing Historically Dominant Industry Aside

Dennis Wamsted, IEEFA Analyst/Editor 1 Seth Feaster, IEEFA Data Analyst October 2019 Coal-Fired Power Generation in Freefall Across Southeast U.S. One-Two Combination of Gas and Solar Is Pushing Historically Dominant Industry Aside Executive Summary Historically, the U.S. Southeast1 has been a stronghold for coal-fired electricity generation. That is no longer the case. The ready availability of low-cost natural gas has led to a freefall in coal generation across the region over the past 10 years that has outpaced even the national drop in coal-fired generation. This, despite the fact that the area is home to companies such as the Tennessee Valley Authority, Southern Company and Duke Energy—three of the traditionally most coal-reliant utilities in the country. The decline is also noteworthy because the region’s utilities are still vertically integrated—controlling generation and transmission—and thus largely shielded from economic pressures like those in fast-changing markets like Texas and the PJM Interconnection,2 where more competitive generation resources often have an easier route to the market. Source: EIA data, IEEFA analysis. 1 In this report, we define the Southeast as including the following nine states: Alabama, Florida, Georgia, Kentucky, Mississippi, North Carolina, South Carolina, Tennessee and Virginia. 2 PJM is the wholesale transmission operator that runs the market serving 13 states and the District of Columbia. Coal-Fired Power Generation in Freefall Across Southeast U.S. 2 The scope of the collapse is evident in the following graphic, which shows significant decline in each of the nine Southeastern states examined in this report. -

Energy for Life 2018 Annual Report Southern Companyreport 2018 Annual

Energy for Life 2018 Annual Report Southern Company 2018 Annual Report SouthernCompany.com Contents Shareholder Information 1 Chairman’s Message Transfer Agent Investor Information 3 Financial Highlights EQ Shareowner Services is Southern Company’s transfer agent, For information about earnings and dividends, stock 4 A Culture of Innovation dividend-paying agent, investment plan administrator and registrar. quotes and current news releases, please visit us at If you have questions concerning your registered Southern Company investor.southerncompany.com. 6 Focused on Fundamentals shareowner account, please contact: Leadership 8 Institutional Investor Inquiries EQ Shareowner Services 10 Financial Review Southern Company maintains an investor relations office in 1110 Centre Pointe Curve, Suite 101 Atlanta, Georgia, 404.506.0901, to meet the information needs Mendota Heights, Minnesota 55120 of institutional investors and securities analysts. Telephone: 1.800.554.7626 Website: shareowneronline.com Electronic Delivery of Proxy Materials Any stockholder may enroll for electronic delivery of proxy Southern Company Shareholder Relations materials by logging on at www.icsdelivery.com/so. Telephone: 404.506.0965 Email: [email protected] Environmental Information Southern Company publishes information on its activities to meet Southern Investment Plan environmental commitments at www.southerncompany.com/ The Southern Investment Plan is a convenient way to become corporate-responsibility. Sandy Alexander a Southern Company shareholder. Participants in the Plan can To request printed materials, write to: Printing: purchase additional shares in Southern Company through optional cash purchases and reinvestment of dividends. The Southern Director, Environmental Affairs Investment Plan prospectus can be found at Research and Environmental Affairs Walter Kirk Walter www.southerncompany.com. 600 North 18th St. -

William P. Cox Senior Attorney Florida Power & Light Company 700

William P. Cox Senior Attorney Florida Power & Light Company 700 Universe Boulevard Juno Beach, FL 33408-0420 (561) 304-5662 (561) 691-7135 (Facsimile) Email: [email protected] April 1, 2021 -VIA ELECTRONIC FILING- Adam Teitzman Commission Clerk Florida Public Service Commission 2540 Shumard Oak Blvd. Tallahassee, FL 32399-0850 RE: Docket No. 20200000-OT Florida Power & Light Company and Gulf Power Company’s 2021-2030 Ten Year Power Plant Site Plan Dear Mr. Teitzman: Please find enclosed for electronic filing Florida Power & Light Company and Gulf Power Company’s 2021-2030 Ten Year Power Plant Site Plan. If there are any questions regarding this transmittal, please contact me at (561)304-5662. Sincerely, /s/ William P. Cox William P. Cox Senior Attorney Fla. Bar No. 00093531 Enclosures cc: Donald Phillips, Division of Engineering Damien Kistner, Division of Engineering Florida Power & Light Company 700 Universe Boulevard, Juno Beach, FL 33408 Ten Year Power Plant Site Plan 2021 – 2030 (This page is intentionally left blank.) Ten Year Power Plant Site Plan 2021-2030 Submitted To: Florida Public Service Commission April 2021 (This page is intentionally left blank.) Table of Contents List of Figures, Tables, and Maps ............................................................................................... iv List of Schedules .......................................................................................................................... vi Overview of the Document .......................................................................................................... -

Glamorous? Nope. 2003 ANNUAL REPORT 2003 GLOSSARY

SOUTHERN COMPANY 2003 ANNUAL REPORT SOUTHERN COMPANY SOUTHERN COMPANY Glamorous? Nope. 2003 REPORT ANNUAL GLOSSARY Book value – a company’s common stockholders’ equity as Payout ratio – the percentage of earnings that is paid to share- it appears on the balance sheet, divided by the number of holders in the form of dividends. common stock shares outstanding. Regulated business – the part of our business that generates, Competitive generation business – our wholesale market-based transmits, and distributes electricity to commercial, industrial, electricity supply business that, primarily through long-term and residential customers in most of Alabama and Georgia, the contracts, serves customers who can choose their suppliers based Florida panhandle, and southeastern Mississippi. on price, reliability, capacity, and other market needs. Retail markets – markets in which energy is sold and delivered Distribution lines – power lines, like those in neighborhoods, directly to the ultimate end-users of that energy. which carry moderate-voltage electricity to customer service areas. Super Southeast – the vibrant region and energy market that includes the four states of our traditional service territory as well Dividend yield – the annual dividend income per share received as surrounding Southeastern states. The geographic focus of our from a company divided by its current stock price. business. Earnings per share – net income divided by the average number Total shareholder return – return on investment, including stock of shares of common stock outstanding. price appreciation plus reinvested dividends. The distribution of shares of Mirant Corporation stock to Southern Company share- Federal Energy Regulatory Commission (FERC) – an independent holders in 2001 is treated as a special dividend for purposes of Lithographix, Los Angeles, CA. -

Gulf Power Company's Environmental Compliance Program Update

Rhonda J. Alexander One Energy Place ~ Gulf Power Manager Pensacola. FL 32520-0780 Regulatory Forecastmg & Pmmg 850 444 6743 tel 850 444 6026 fax rJalexad@southernco <Om April 2, 2018 Ms. Carlotta Stauffer, Commission Clerk Florida Public Service Commission 2540 Shumard Oak Boulevard Tallahassee, FL 32399-0850 Re: Docket No. 20180007-EI Dear Ms. Stauffer: Attached for official filing in the above-referenced docket is Gulf Power Company's Environmental Compliance Program Update. Sincerely, i<.~ ~ Rhonda J. Alexander Regulatory, Forecasting and Pricing Manager md Attachments cc : Gulf Power Company Jeffrey A. Stone, Esq., General Counsel Beggs & Lane Russell Badders, Esq. GULF POWER COMPANY ENVIRONMENTAL COMPLIANCE PROGRAM UPDATE April 2, 2018 CONTENTS I. EXECUTIVE SUMMARY .......................................................................................... 1 II. REGULATORY AND LEGISLATIVE UPDATE .................................................... 3 A. EFFLUENT LIMITATIONS GUIDELINES .................................................................. 3 B. COAL COMBUSTION RESIDUALS (CCR) REGULATION ...................................... 3 C. 316(B) INTAKE STRUCTURE REGULATION............................................................ 4 D. NATIONAL AMBIENT AIR QUALITY STANDARDS (NAAQS) ............................. 4 E. REGIONAL HAZE RULE .............................................................................................. 5 F. EPA’S EXCESS EMISSION STATE IMPLEMENTATION PLANS ........................... 5 G. CLEAN POWER PLAN