Designing a New Fiscal Framework: Understanding and Confronting Uncertainty

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Glossary of Treasury Terms

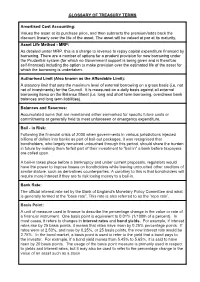

GLOSSARY OF TREASURY TERMS Amortised Cost Accounting: Values the asset at its purchase price, and then subtracts the premium/adds back the discount linearly over the life of the asset. The asset will be valued at par at its maturity. Asset Life Method - MRP: As detailed under MRP, this is a charge to revenue to repay capital expenditure financed by borrowing. There are a number of options for a prudent provision for new borrowing under the Prudential system (for which no Government support is being given and is therefore self-financed) including the option to make provision over the estimated life of the asset for which the borrowing is undertaken. Authorised Limit (Also known as the Affordable Limit): A statutory limit that sets the maximum level of external borrowing on a gross basis (i.e. not net of investments) for the Council. It is measured on a daily basis against all external borrowing items on the Balance Sheet (i.e. long and short term borrowing, overdrawn bank balances and long term liabilities). Balances and Reserves: Accumulated sums that are maintained either earmarked for specific future costs or commitments or generally held to meet unforeseen or emergency expenditure. Bail - in Risk: Following the financial crisis of 2008 when governments in various jurisdictions injected billions of dollars into banks as part of bail-out packages, it was recognised that bondholders, who largely remained untouched through this period, should share the burden in future by making them forfeit part of their investment to "bail in" a bank before taxpayers are called upon. A bail-in takes place before a bankruptcy and under current proposals, regulators would have the power to impose losses on bondholders while leaving untouched other creditors of similar stature, such as derivatives counterparties. -

House of Commons Official Report Parliamentary Debates

Monday Volume 652 7 January 2019 No. 228 HOUSE OF COMMONS OFFICIAL REPORT PARLIAMENTARY DEBATES (HANSARD) Monday 7 January 2019 © Parliamentary Copyright House of Commons 2019 This publication may be reproduced under the terms of the Open Parliament licence, which is published at www.parliament.uk/site-information/copyright/. HER MAJESTY’S GOVERNMENT MEMBERS OF THE CABINET (FORMED BY THE RT HON. THERESA MAY, MP, JUNE 2017) PRIME MINISTER,FIRST LORD OF THE TREASURY AND MINISTER FOR THE CIVIL SERVICE—The Rt Hon. Theresa May, MP CHANCELLOR OF THE DUCHY OF LANCASTER AND MINISTER FOR THE CABINET OFFICE—The Rt Hon. David Lidington, MP CHANCELLOR OF THE EXCHEQUER—The Rt Hon. Philip Hammond, MP SECRETARY OF STATE FOR THE HOME DEPARTMENT—The Rt Hon. Sajid Javid, MP SECRETARY OF STATE FOR FOREIGN AND COMMONWEALTH AFFAIRS—The Rt. Hon Jeremy Hunt, MP SECRETARY OF STATE FOR EXITING THE EUROPEAN UNION—The Rt Hon. Stephen Barclay, MP SECRETARY OF STATE FOR DEFENCE—The Rt Hon. Gavin Williamson, MP LORD CHANCELLOR AND SECRETARY OF STATE FOR JUSTICE—The Rt Hon. David Gauke, MP SECRETARY OF STATE FOR HEALTH AND SOCIAL CARE—The Rt Hon. Matt Hancock, MP SECRETARY OF STATE FOR BUSINESS,ENERGY AND INDUSTRIAL STRATEGY—The Rt Hon. Greg Clark, MP SECRETARY OF STATE FOR INTERNATIONAL TRADE AND PRESIDENT OF THE BOARD OF TRADE—The Rt Hon. Liam Fox, MP SECRETARY OF STATE FOR WORK AND PENSIONS—The Rt Hon. Amber Rudd, MP SECRETARY OF STATE FOR EDUCATION—The Rt Hon. Damian Hinds, MP SECRETARY OF STATE FOR ENVIRONMENT,FOOD AND RURAL AFFAIRS—The Rt Hon. -

A Guide to the Government for BIA Members

A guide to the Government for BIA members Correct as of 26 June 2020 This is a briefing for BIA members on the Government led by Boris Johnson and key ministerial appointments for our sector after the December 2019 General Election and February 2020 Cabinet reshuffle. Following the Conservative Party’s compelling victory, the Government now holds a majority of 80 seats in the House of Commons. The life sciences sector is high on the Government’s agenda and Boris Johnson has pledged to make the UK “the leading global hub for life sciences after Brexit”. With its strong majority, the Government has the power to enact the policies supportive of the sector in the Conservatives 2019 Manifesto. All in all, this indicates a positive outlook for life sciences during this Government’s tenure. Contents: Ministerial and policy maker positions in the new Government relevant to the life sciences sector .......................................................................................... 2 Ministers and policy maker profiles................................................................................................................................................................................................ 7 Ministerial and policy maker positions in the new Government relevant to the life sciences sector* *Please note that this guide only covers ministers and responsibilities relevant to the life sciences and will be updated as further roles and responsibilities are announced. Department Position Holder Relevant responsibility Holder in -

The Tempered Ordered Probit (TOP) Model with an Application to Monetary Policy William H.Greene Max Gillman Mark N.Harris Christopher Spencer WP 2013 – 10

ISSN 1750-4171 ECONOMICS DISCUSSION PAPER SERIES The Tempered Ordered Probit (TOP) Model With An Application To Monetary Policy William H.Greene Max Gillman Mark N.Harris Christopher Spencer WP 2013 – 10 School of Business and Economics Loughborough University Loughborough LE11 3TU United Kingdom Tel: + 44 (0) 1509 222701 Fax: + 44 (0) 1509 223910 http://www.lboro.ac.uk/departments/sbe/economics/ The Tempered Ordered Probit (TOP) model with an application to monetary policy William H. Greeney Max Gillmanz Mark N. Harrisx Christopher Spencer{ September 2013 Abstract We propose a Tempered Ordered Probit (TOP) model. Our contribution lies not only in explicitly accounting for an excessive number of observations in a given choice category - as is the case in the standard literature on in‡ated models; rather, we introduce a new econometric model which nests the recently developed Middle In‡ated Ordered Probit (MIOP) models of Bagozzi and Mukherjee (2012) and Brooks, Harris, and Spencer (2012) as a special case, and further, can be used as a speci…cation test of the MIOP, where the implicit test is described as being one of symmetry versus asymmetry. In our application, which exploits a panel data-set containing the votes of Bank of England Monetary Policy Committee (MPC) members, we show that the TOP model a¤ords the econometrician considerable ‡exibility with respect to modelling the impact of di¤erent forms of uncertainty on interest rate decisions. Our …ndings, we argue, reveal MPC members’ asymmetric attitudes towards uncertainty and the changeability of interest rates. Keywords: Monetary policy committee, voting, discrete data, uncertainty, tempered equations. -

Fit to Work and Play Thanks to Occupational Health!

TALKING POINT April 2017 Fit to work and play thanks to Page 10 occupational health! Talking Important changes to Point is your urgent care magazine NHS South Tees Clinical Commissioning Group has and it is only introduced a number of changes as good as to urgent care after listening to local people at a series of you make it. consultation events… It is produced quarterly in The service will be operated by local January, April, July and October Changes to Redcar Minor doctors and nurses from the South Tees each year. Injury Unit opening times area with access to your patient records. Ideas and stories or suggestions Minor injury units (MIU) can assess and There are a number of ways to make to make Talking Point even better treat: minor burns, scalds, infected an appointment: are always welcome. wounds, sprains, cuts, grazes and • Telephone your own GP surgery which Contact the communication possible broken bones. has access to appointments in the and engagement team on If you have a minor injury you can go extended hours GP centres. 01642 854343, extension 54343, to Redcar Primary Care Hospital. Please James Cook or email note, the opening times have been • Your own surgery will always try [email protected]. changed from 1 April 2017 to reflect to meet your needs first but if you patient demand. require an appointment urgently and they can’t fit you in - or if it is more The new opening times are 8am to convenient for you to be seen in the 9.30pm, 7 days a week and include evening or at the weekend, they will Mailing list – still access to x-ray. -

Assessment of Compliance with the Code of Practice for Official Statistics

Assessment of compliance with the Code of Practice for Official Statistics Statistics on the Public Sector Finances (produced by the Office for National Statistics and HM Treasury) Assessment Report 316 October 2015 © Crown Copyright 2015 The text in this document may be reproduced free of charge in any format or medium providing it is reproduced accurately and not used in a misleading context. The material must be acknowledged as Crown copyright and the title of the document specified. Where we have identified any third party copyright material you will need to obtain permission from the copyright holders concerned. For any other use of this material please write to Office of Public Sector Information, Information Policy Team, Kew, Richmond, Surrey TW9 4DU or email: [email protected] About the UK Statistics Authority The UK Statistics Authority is an independent body operating at arm’s length from government as a non-ministerial department, directly accountable to Parliament. It was established on 1 April 2008 by the Statistics and Registration Service Act 2007. The Authority’s overall objective is to promote and safeguard the production and publication of official statistics that serve the public good. It is also required to promote and safeguard the quality and comprehensiveness of official statistics, and good practice in relation to official statistics. The Statistics Authority has two main functions: 1. oversight of the Office for National Statistics (ONS) – the executive office of the Authority; 2. independent scrutiny (monitoring -

Speech by Martin Weale at the University of Nottingham, Tuesday

Unconventional monetary policy Speech given by Martin Weale, External Member of the Monetary Policy Committee University of Nottingham 8 March 2016 I am grateful to Andrew Blake, Alex Harberis and Richard Harrison for helpful discussions, to Tomasz Wieladek for the work he has done with me on both asset purchases and forward guidance and to Kristin Forbes, Tomas Key, Benjamin Nelson, Minouche Shafik, James Talbot, Matthew Tong, Gertjan Vlieghe and Sebastian Walsh for very helpful comments. 1 All speeches are available online at www.bankofengland.co.uk/publications/Pages/speeches/default.aspx Introduction Thank you for inviting me here today. I would like to talk about unconventional monetary policy. I am speaking to you about this not because I anticipate that the Monetary Policy Committee will have recourse to expand its use of unconventional policy any time soon. As we said in our most recent set of minutes, we collectively believe it more likely than not that the next move in rates will be up. I certainly consider this to be the most likely direction for policy. The UK labour market suggests that medium-term inflationary pressures are building rather than easing; wage growth may have disappointed, but a year of zero inflation does not seem to have depressed pay prospects further. However, I want to discuss unconventional policy options today because the Committee does not want to be a monetary equivalent of King Æthelred the Unready.1 It is as important to consider what we could do in the event of unlikely outcomes as the more likely scenarios. In particular, there is much to be said for reviewing the unconventional policy the MPC has already conducted, especially as the passage of time has given us a clearer insight into its effects. -

Euro Medium Term Note Prospectus

20MAY201112144662 London Stock Exchange Group plc (Registered number 5369106, incorporated with limited liability under the laws of England and Wales) £1,000,000,000 Euro Medium Term Note Programme Under this £1,000,000,000 Euro Medium Term Note Programme (the Programme) London Stock Exchange Group plc (the Issuer) may from time to time issue notes (the Notes) denominated in any currency agreed between the Issuer and the relevant Dealer (as defined on page 1). An investment in Notes issued under the Programme involves certain risks. For a description of these risks, see ‘‘Risk Factors’’ below. Application has been made to the Financial Services Authority (the UK Listing Authority) in its capacity as competent authority under the Financial Services and Markets Act 2000, as amended (the FSMA) for Notes issued during the period of 12 months from the date of this Offering Circular to be admitted to the official list of the UK Listing Authority (the Official List) and to the London Stock Exchange plc (the London Stock Exchange) for such Notes to be admitted to trading on the London Stock Exchange’s regulated market. References in this Offering Circular to Notes being ‘‘listed’’ (and all related references) shall either mean that such Notes have been admitted to trading on the London Stock Exchange’s regulated market and have been admitted to the Official List or shall be construed in a similar manner in respect of any other EEA State Stock Exchange, as applicable. The expression ‘‘EEA State’’ when used in this Offering Circular has the meaning given to such term in the FSMA (as defined above). -

National Institute Economic Review Road, Cambridge CB2 8BS, England for the National Institute of Economic and Social Research

National Volume 255 – February 2021 Nati onal Insti tute Economic Review Economic tute Insti onal Nati Institute Economic Review NIER Volume 255 February 2021 255 February Volume National Institute Economic Review Road, Cambridge CB2 8BS, England for the National Institute of Economic and Social Research. Annual subscription including postage: institutional rate (combined print and electronic) £596/US$1102; Managing Editors individual rate (print only) £166/US$292. Electronic only and print Jagjit Chadha (National Institute of Economic and Social Research) only subscriptions are available for institutions at a discounted rate. Prasanna Gai (University of Auckland) Note VAT is applicable at the appropriate local rate. Abstracts, tables Ana Galvao (University of Warwick) of contents and contents alerts are available online free of charge for Sayantan Ghosal (University of Glasgow) all. Student discounts, single issue rates and advertising details are Colin Jennings (King’s College London) available from Cambridge University Press, One Liberty Plaza, Hande Küçük (National Institute of Economic and Social Research) New York, NY 10006, USA/UPH, Shaftesbury Road, Cambridge CB2 Miguel Leon-Ledesma (University of Kent) 8BS, England. POSTMASTER: Send address changes in the USA and Corrado Macchiarelli (National Institute of Economic and Canada to National Institute Economic Review, Cambridge University Social Research) Press, Journals Ful llment Dept., One Liberty Plaza, New York, Adrian Pabst (National Institute of Economic and Social Research) NY 10006-4020, USA. Send address changes elsewhere to National Institute Economic Review, Cambridge University Press, University Council of Management Printing House, Shaftesbury Road, Cambridge, CB2 8BS, England. Sir Paul Tucker (President) Neil Gaskell Professor Nicholas Crafts (Chair) Professor Sir David Aims and Scope Professor Jagjit S. -

Orme) Wilberforce (Albert) Raymond Blackburn (Alexander Bell

Copyrights sought (Albert) Basil (Orme) Wilberforce (Albert) Raymond Blackburn (Alexander Bell) Filson Young (Alexander) Forbes Hendry (Alexander) Frederick Whyte (Alfred Hubert) Roy Fedden (Alfred) Alistair Cooke (Alfred) Guy Garrod (Alfred) James Hawkey (Archibald) Berkeley Milne (Archibald) David Stirling (Archibald) Havergal Downes-Shaw (Arthur) Berriedale Keith (Arthur) Beverley Baxter (Arthur) Cecil Tyrrell Beck (Arthur) Clive Morrison-Bell (Arthur) Hugh (Elsdale) Molson (Arthur) Mervyn Stockwood (Arthur) Paul Boissier, Harrow Heraldry Committee & Harrow School (Arthur) Trevor Dawson (Arwyn) Lynn Ungoed-Thomas (Basil Arthur) John Peto (Basil) Kingsley Martin (Basil) Kingsley Martin (Basil) Kingsley Martin & New Statesman (Borlasse Elward) Wyndham Childs (Cecil Frederick) Nevil Macready (Cecil George) Graham Hayman (Charles Edward) Howard Vincent (Charles Henry) Collins Baker (Charles) Alexander Harris (Charles) Cyril Clarke (Charles) Edgar Wood (Charles) Edward Troup (Charles) Frederick (Howard) Gough (Charles) Michael Duff (Charles) Philip Fothergill (Charles) Philip Fothergill, Liberal National Organisation, N-E Warwickshire Liberal Association & Rt Hon Charles Albert McCurdy (Charles) Vernon (Oldfield) Bartlett (Charles) Vernon (Oldfield) Bartlett & World Review of Reviews (Claude) Nigel (Byam) Davies (Claude) Nigel (Byam) Davies (Colin) Mark Patrick (Crwfurd) Wilfrid Griffin Eady (Cyril) Berkeley Ormerod (Cyril) Desmond Keeling (Cyril) George Toogood (Cyril) Kenneth Bird (David) Euan Wallace (Davies) Evan Bedford (Denis Duncan) -

Escoe CONFERENCE on ECONOMIC MEASUREMENT 2020

ESCoE CONFERENCE ON ECONOMIC MEASUREMENT 2020 16-18 SEPTEMBER 2020 @ESCoEorg #econstats2020 Welcome Keynote speakers Welcome to the ESCoE Conference on Economic Measurement 2020. Anil Arora (Statistics This year sees a remarkable first for everyone involved, a completely online, digital, annual Canada) conference. As many of you will be aware, we, in partnership with the Office for National Statistics, were ‘Statistics Canada’s Modernization due to return to the excellent facilities of King’s Business School for EM2020. Covid-19, Journey – Responding to the Fast social distancing rules and travel restrictions all of course meant that these plans had to be Evolving Data Needs of the 21st changed. While there is no substitute that could ever completely replicate the experience of a traditional conference and the opportunities they provide for meeting colleagues in Century’ person, we are however very pleased to be able to host you this year on a virtual platform. We’ve done our best to recreate at least something of the experience of physically attending a conference. Our virtual conference space includes lecture rooms where you can access a comprehensive programme of live plenary, panel, contributed, Covid-19 and special sessions. The need for good-quality facts and data, in a society where there are massive changes, has You will also be able to visit our conference poster exhibition and engage directly with other never been greater. At Statistics Canada, a full-fledged modernization initiative is underway attendees and speakers via dedicated direct messaging and topic chatroom functions. to provide even greater value to Canadians and businesses in the form of data, analytics and insights. -

Book Review: Ed: the Milibands and the Making of a Labour Leader

blogs.lse.ac.uk http://blogs.lse.ac.uk/politicsandpolicy/2011/07/16/book-review-ed-the-milibands-and-the-making-of-a-labour-leader/ Book Review: Ed: The Milibands and the Making of a Labour Leader Matthew Partridge reviews the brand new Ed Miliband biography by Mehdi Hasan and James Macintyre, published this weekend. Ed: The Milibands and the Making of a Labour Leader. By Mehdi Hassan and James Macintyre. Biteback Publishing. June 2011. Writing the first major biography of a political figure, which is what Mehdi Hasan and James Macintyre have done with Ed: The Milibands and the Making of a Labour Leader, is always challenging. The first major work looking at Margaret Thatcher did not reach the public until a year after she entered Downing Street and five years after her election as Conservative leader. Even though publishers would be quicker to respond to the rise of John Major, Tony Blair, William Hague and others, they all had relatively substantial parliamentary careers from which their biographers could draw from. Indeed, the only recent party leader with a comparably thin record was David Cameron, the present occupant of Downing Street. The parallels between the career trajectory of Miliband and Cameron, are superficially striking. For instance, both had the advantage of family connections, entered politics as advisors, took mid-career breaks and enjoyed the close patronage of their predecessors. However, while Cameron spent most of his time as a researcher in the Conservative party’s central office, his two stints with Norman Lamont and Michael Howard proved to be short lived.