7 Principles of Earned Value Management Tier 2 System Implementation Intent Guide

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Earned Value Management (EVM) System Description

NASA/SP-2019-3704 Earned Value Management (EVM) System Description National Aeronautics and Space Administration November 1, 2019 Electronic copies are available from: NASA STI Program: https://wwww.sti.nasa.gov NASA STI Information Desk: [email protected]/ (757) 864-9658 Write to: NASA STI Information Desk Mail Stop 148 NASA Langley Research Center Hampton, VA 23681-2199 NASA Engineering Network (NEN) at https://nen.nasa.gov/web/pm/ (inside the NASA firewall only). OCFO-SID EVM Homepage at https://community.max.gov/dis- play/NASA/Earned+Value+Management+HOMEPAGE (inside the NASA firewall only) RECORD OF REVISIONS R E DESCRIPTION DATE V Basic Issue November 2013 1 Incorporate IPMR, ANSI/EIA-748 reference change March 2016 2 Added EVM reciprocity, scalability and new EVM $250M threshold January 2018 Added SMD Class-D EVMS Deviation, revised Intra-Agency Work Agree- ment EVM requirements, updated links, updated NASA EVMS requirements 3 September 2019 thresholds chart, deleted special publication numbers from references, cor- rected Data Requirements Description acronym, minor edits, etc. NASA EVM System Description ii ii TABLE OF CONTENTS P.1 Purpose ............................................................................................................ vi P.2 Applicability ..................................................................................................... vii P.3 Authority .......................................................................................................... vii P.4 References ..................................................................................................... -

Earned Value Management Best Practices

WHITE PAPER Earned Value Management Best Practices CONTENTS BACKGROUND BEST PRACTICES FOR EVMS USE Earned Value Management (EVM), a mainstay of When it comes to using an EVMS, most Best Practices for EVMS Use ..............................1 major government project management, has organizations follow a learning curve. The now caught the imagination of government IT purpose of this paper is to help organizations Use an EVMS Description professionals as well as those in the private flatten the curve, arming them with EVMS best and Keep it Up to sector. This has happened because EVM offers, practices. These best practices are broken down Date ...................................1 for the first time, an “apples to apples” into five guideline areas: Use EVMS on Every methodology for understanding how projects Project ..............................2 are progressing in relation to the original • EVMS description When to Use EVMS on funding and scope. It is a systematic approach a Program .................3 to planning, measuring, and forecasting a • EVMS use Building a Work project and a tool in the project manager’s Breakdown Structure toolbox for successfully completing an assigned • Work Breakdown Structure (WBS) and (WBS) ..............................3 project. Control Account WBS and Control Account Earned Value Management Systems (EVMS) are • Cost and schedule integration Guidelines ................3 required by the Office of Management and Budget for federal agencies and by contract on • Earned Value calculation Defining a Control Account ....................4 major systems acquistions done by the U.S. Government and some foreign governments. USE AN EVMS DESCRIPTION AND KEEP IT Cost and Schedule They are also part of the Project Management UP TO DATE Integration Institute’s Project Management Body of The system description provides an Guidelines ........................4 Knowledge (PMI PMBOK) and are used by many understanding of each activity required to meet Earned Value Calculation civilian organizations. -

Earned Value Management: What Is It? Who Needs

Franklin Training Group EARNED VALUE MANAGEMENT: WHAT IS IT? WHO NEEDS IT? Capturing Opportunities for Performance Excellence Earned Value Management 1 Chet Franklin ASQ 711 July 2008 What is EVM? Franklin Training Group • EVM; Earned Value Management • For the management of projects • It is called: – A concept – A discipline – An approach – A program • A set of tools Capturing Opportunities for Performance Excellence Earned Value Management 2 Chet Franklin ASQ 711 July 2008 Who needs it? Franklin Training Group • No one NEEDS it • Who can use it? – Program Managers – Project Managers – Project Teams – Budget Analysts – Planners Capturing Opportunities for Performance Excellence Earned Value Management 3 Chet Franklin ASQ 711 July 2008 Project Managers Need Franklin Training Group • Plan – What is to be done? – When is it to be done? – What will it cost? • Tracking – What has been done? – When was it done? – What did it cost? Capturing Opportunities for Performance Excellence Earned Value Management 4 Chet Franklin ASQ 711 July 2008 What will EVM do? Franklin Training Group • Provide Project Status – Financial performance – Schedule performance • Provide information – Identify risks – Predict future performance • Financial – Cost-to-Complete • Schedule – Variance from plan Capturing Opportunities for Performance Excellence Earned Value Management 5 Chet Franklin ASQ 711 July 2008 Is EVM New? Franklin Training Group • NO! • The basic concepts? – They’ve been around for a 100 years, or so – PVA (Planned Value of Work Accomplished) – BCWP -

Control Account Manger (CAM)/ Earned Value Management System (EVMS) Training 1

Control Account Manger (CAM)/ Earned Value Management System (EVMS) Training 1 Introduction to EVM Organization, Planning, Scheduling, Budgeting, and Accounting Considerations Steve Langish Overview Covering The Basics – Introduction to EVMS Web Page/Contents – What Is Earned Value Management (EVM) – Why Use EVM – The EVM Process & How It AliApplies To You Heavy Detail On The Front – Organization – Planning, Scheduling, & Budgeting – Accounting Considerations Light Detail On The End (For This Session) – Analysis & Management Reports – Revisions Summary & What ‘s Up Next Time At The End For Questions & Throughout 2 PPPL’s EVMS Web Page http://www‐local. pppl. gov/EVMS/ 3 What Is EVM? Definition – Earned Value Management (EVM) Is A Project Management Technique For Measuring Project Progress In An Objective Manner – A Systematic Approach To The Integration & Measurement Of Cost, Schedule, & Technical (Scope) Accomplishments On A Project Application – Work Is Planned, Budgeted, & Scheduled In Time‐Phased Increments To Achieve This – Takes Into Consideration Risk, Uncertainties, & Assumptions – Involves Project Managers, Control Account Managers, Contractors, Customers, etc Objective – Encourage The Use Of Effective Internal Cost & Schedule Management Controls – Allow Timely Data For Determining Product‐Oriented Status 4 Why Use EVM? Who Wants To Babysit Every Line In A Schedule Of This Size? – Management By Exception ‐ Provides Early Warning Of Performance Problems – Trip Wires Via Thresholds – Using All Views Instead Of Driving -

Critical Analysis on Earned Value Management (EVM) Technique in Building Construction

Critical Analysis on Earned Value Management (EVM) Technique in Building Construction CRITICAL ANALYSIS ON EARNED VALUE MANAGEMENT (EVM) TECHNIQUE IN BUILDING CONSTRUCTION Luis Felipe Cândido1, Luiz Fernando Mählmann Heineck2 José de Paula Barros Neto3 ABSTRACT Earned Value Management (EVM) is a technique of performance measurement focused on project physical, financial and time progress, indicating planned and actual performance, variations of them and forecasts on final project duration and cost. It takes a step further traditional measurement tools like PERT/Cost and C/SCSC. EVM is strongly supported by Project Management Community gather around the Project Management Institute, but recently the technique is being criticized in respect to its conceptual problems and implementation difficulties. This paper aims to explore in greater depth this debate through a case study on a construction project that applied EVM as a planning and control tool. Four major problems are analyzed in the search for an enlarged list of topics the EVM approach fails to support lean construction applications. Among them are the disregard for the mobilization of resources phase and the lack of consideration of construction indirect costs. Finally, the authors concluded that EVM is just an extension of the traditional approach of measuring physical and financial advances over time. This narrow approach is insufficient to provide a comprehensive managerial tool, as became clear through the analyses of the building project under consideration. KEYWORDS EVM (Earned Value Management), Control of Building Projects, Lean Construction and Project Management. INTRODUCTION Uncertainty and complexity typical of constructions projects led building companies to adopt more sophisticated techniques and tools to effectively plan and control building developments. -

Earned Value Management Best Practices Report

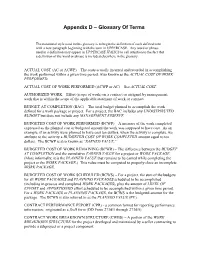

Appendix D – Glossary Of Terms The notational style used in this glossary is to begin the definition of each defined term with a new paragraph beginning with the term in UPPERCASE. Any word or phrase used in a definition may appear in UPPERCASE ITALICS to call attention to the fact that a definition of the word or phrase is included elsewhere in the glossary. ACTUAL COST (AC or ACWP) – The costs actually incurred and recorded in accomplishing the work performed within a given time period. Also known as the ACTUAL COST OF WORK PERFORMED. ACTUAL COST OF WORK PERFORMED (ACWP or AC) – See ACTUAL COST. AUTHORIZED WORK – Effort (scope of work) on a contract or assigned by management; work that is within the scope of the applicable statement of work or contract. BUDGET AT COMPLETION (BAC) – The total budget planned to accomplish the work defined for a work package or project. For a project, the BAC includes any UNDISTRIBUTED BUDGET but does not include any MANAGEMENT RESERVE. BUDGETED COST OF WORK PERFORMED (BCWP) – A measure of the work completed expressed as the planned cost or budgeted amount the work was supposed to have cost. As an example, if an activity were planned to have cost ten dollars, when the activity is complete, we attribute to the activity a BUDGETED COST OF WORK COMPLETED amount equal to ten dollars. The BCWP is also known as “EARNED VALUE.” BUDGETED COST OF WORK REMAINING (BCWR) – The difference between the BUDGET AT COMPLETION and the cumulative EARNED VALUE for a project or WORK PACKAGE. -

Evolution of EVM and the Future

Evolution of EVM and the Future NSF Large Facilities Workshop Baton Rouge, LA May 1, 2017 Wayne Abba President, CPM [email protected] Agenda • College of Performance Management (CPM) • Earned Value Management (EVM) – the Foundation of Integrated Program Management (IPM) • Evolution of IPM – Past (Cost/Schedule Control Systems Criteria) – Present (Earned Value Management) – Future (Integrated Program Management) • War Story – A Tale of Two Aircraft • Summary and Q&A 2 THE COLLEGE OF PERFORMANCE MANAGEMENT (CPM) WWW.MYCPM.ORG/ 3 About CPM • The College of Performance Management (CPM) is a global, non-profit, professional organization dedicated to developing and disseminating the principles and practices of earned value management and other project performance management techniques. • We assist the project control professional and project manager in professional growth and promote the application of earned value management. We are a growing body of professionals dedicated to managing projects on time and on budget. 4 2017 CPM Events • EVM World 2017 • IPM Workshop – May 31 – June 2, 2017 – Oct 30 – Nov 1, 2017 – New Orleans, Louisiana – Bethesda, Maryland – Hyatt Regency New – Bethesda North Marriott Orleans Hotel & Conference – Science & PM Track Center 50 www.mycpm.org/news-events/events/ 5 EARNED VALUE MANAGEMENT (EVM) 6 What is EVM? • Earned Value Management (EVM) is a project management technique for measuring project performance and progress. In a single integrated system, Earned Value Management (EVM) is able to provide accurate -

Earned Value Management Tutorial Module 5: EVMS Concepts and Methods

Earned Value Management Tutorial Module 5: EVMS Concepts and Methods Prepared by: Module 5: EVMS Concepts and Methods Welcome to Module 5. The objective of this module is to introduce you to Basic Earned Value concepts and methods. The Topics that will be addressed in this Module include: • Earned Valve Management System (EVMS) Criteria • The definitions and illustrations of the basic EVMS terminology • The definition and illustrations of the EV methods Module 5 – EVMS Concepts and Methods 1 Prepared by: Booz Allen Hamilton Review of Previous Modules In the previous four modules, we discussed the framework needed to perform Earned Value and develop an Earned Value Management System (EVMS). • In Module 1 we introduced you to earned value and the requirements for properly implementing an earned value management system (EVMS) • In Module 2 we discussed the development of the work breakdown structure (WBS), organizational breakdown structure (OBS) and the integration of WBS and OBS in creating the responsibility assignment matrix (RAM) • In Module 3 we discussed the development of the project schedule and the schedule baseline • In Module 4 we discussed the development of the project budget and the cost baseline Now let’s discuss the basic Earned Value concepts and methods. Module 5 – EVMS Concepts and Methods 2 Prepared by: Booz Allen Hamilton EVMS Criteria Before we start discussing the Earned Value concepts and methods, let’s look at an overview of the criteria needed for EVMS. There are numerous EVMS guidelines that have been developed in both the government and commercial industry. On the next page, we will look at the Industry Standard Earned Value Management Department of System guideline published in DoD 5000.2-R. -

Earned Value Management and Its Applications: a Case of an Oil & Gas Project in Kazakhstan1

PM World Journal Earned Value Management and its Application: A Case of Vol. VII, Issue V – May 2018 an Oil & Gas Project in Kazakhstan www.pmworldjournal.net Student Paper by Assylkhan Ziyash Earned Value Management and its Applications: A Case of an Oil & Gas Project in Kazakhstan1 Assylkhan Ziyash Abstract This research is performed in the study of issues in project control and progress performance evaluation. Particularly, it focuses on the progress measurement by applying the Earned Value Management (EVM). EVM is one of the widely used approaches for project monitoring and control which allows one to assess project progress through scope, schedule, and cost measurements. In order to track the progress effectively the measurements data should be provided systematically. According to the previous research studies on this subject, there are a lot of benefits that have been associated with the use of EVM in Project Management (PM). The main purpose of this research is to assess how EVM, when applied to a real project, helps a project manager to be successful in terms of budget utilization and adherence to schedule. This study is aimed to well understanding of the actual cost expenditures versus planned costs and potential usage of EVM to compare and analyze the available data. For the purpose of data collection, this research evaluates a project that has recently been delivered in the oil and gas industry in Kazakhstan. The study compares actual spending against planned values. It should be noted that the current project did not apply the EVM methodology while being executed. The project had significant cost increase from original budget. -

Dod Earned Value Management Interpretation Guide

FOREWORD Earned Value Management (EVM) is one of the DoD’s and industry's most powerful program management tools. Government and industry program managers utilize EVM to assess cost, schedule, and technical progress on programs to support joint situational awareness and informed decision-making. To be effective, EVM practices and competencies must integrate into the program manager’s acquisition decision-making process. The data provided by the EVM System (EVMS) must be timely, accurate, reliable, and auditable. Industry must implement the EVMS in a disciplined manner consistent with the 32 Guidelines contained in the Electronic Industries Alliance Standard-748 EVMS (EIA-748) (Reference (a)), hereinafter referred to as “the 32 Guidelines.” The Office of Performance Assessments and Root Cause Analyses (PARCA) is accountable for EVM policy, oversight, and governance across the DoD. PARCA’s objective for the DoD EVMS Interpretation Guide (EVMSIG) is to improve the effectiveness of EVM across the Department. The DoD EVMSIG is used as the basis for the DoD to assess EVMS compliance with the 32 Guidelines. This first revision, as with the original document dated February 2015, was developed in collaboration with DoD EVMS experts from the Office of the Secretary of Defense and the organizations responsible for conducting EVMS compliance reviews (i.e., the Defense Contract Management Agency, Intelligence Community, and Navy Shipbuilding). The following strategies underlie the content of this policy: • Reduce the implementation burden associated with demonstrating compliance with the 32 Guidelines by promoting consistent application of EVMS compliance assessments across DoD. • Emphasize the need to establish clear and measurable technical objectives for baseline planning, performance measurement, and management. -

Earned Value Management System Cost Estimating Procedure

LCLS Project Management Project Document # 1.1-021 Management Revision 0.0 Earned Value Management System Cost Estimating Procedure Patricia Mast (LCLS Project Controls Signature Date Manager) Mark Reichanadter (LCLS Deputy Project Director) Signature Date John Galayda (LCLS Project Director) Signature Date Change History Log Rev Revision Sections Affected Description of Change Number Date 0.0 03/22/2006 All Initial version released. Cost Estimating Procedure Table of Contents 1.0 PURPOSE ...........................................................................................................1 2.0 SCOPE ................................................................................................................1 3.0 REFERENCES ....................................................................................................1 4.0 DESCRIPTION ....................................................................................................1 5.0 PROCEDURE DETAILS ......................................................................................2 5.1 Developing a Detailed Cost Estimate .......................................................2 5.2 Basis of Estimate Criteria .........................................................................5 5.3 Design Maturity and Judgment Factors ....................................................6 LIST OF FIGURES Figure 1. Developing a Detailed Cost Estimate.............................................................. 2 i LCLS Earned Value Management System ii Cost Estimating Procedure -

Earned Value Management (EVM)

Earned value management Earned value management Contents Section Subject Page 1 Introduction 1 2 Why EVM? 1 2.1 A brick wall 1 3 What is EVM? 2 4 Wider use of EVM 4 5 Banana skins 4 6 Long-term accounting 5 7 Summary 5 8 Collinson Grant 6 Earned value management 1 Introduction Many projects, particularly those with a component of information technology, have been recognised as too costly, too late, and failing to achieve their initial objectives. Few people would make a journey without knowing how far they have travelled, or how far they must still travel, looking at the journey in stages. Yet many project managers do just that. Every project or programme manager must be able to answer the question ‘How are we doing?’ It is essential for effective control that the performance of a project should be measured while there is still time for corrective action. This document: • examines the reasons for using earned value management (EVM) • provides an overview of the approach to EVM • discusses some of the wider situations, including business units, in which EVM can be deployed. 2 Why EVM? 2.1 A brick wall A bricklayer is building a wall 30m long and 3m high, over flat and consistent ground. The project allows for five days to complete the wall. All the bricks were purchased before work started. When 12 metres have been built, all of which is 3m high, the project is 40% completed. However, the picture becomes more complicated when we learn that the bricklayer is paid a daily rate, the budgeted labour cost allows for five days’ work, and the bricklayer has worked for three days, which is 60% of the time available to complete the work.