FIAT CHRYSLER AUTOMOBILES N.V. (Translation of Registrant’S Name Into English)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2018 Annual Report

2018 ANNUAL REPORT 2018 ANNUAL REPORT AND FORM 20-F 2 2018 | ANNUAL REPORT 2018 | ANNUAL REPORT 3 Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes No Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes No Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and emerging growth company” in Rule 12b-2 of the Exchange Act. Large accelerated filer Accelerated filer Non-accelerated filer Emerging growth company If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing: U.S. -

Qualitas 2016 Annual Strategy Meeting and Supplier Awards

QUALITAS 2016 ANNUAL STRATEGY MEETING & SUPPLIER AWARDS CEREMONY Confidential Information – ©2016 FCA US LLC WELCOME Scott Thiele Chief Purchasing Officer, FCA – Global Head of Purchasing & Supplier Quality, FCA – North America Confidential Information – ©2016 FCA US LLC Theme of the Event QUALITY MAKERS: Aligning for Excellence Confidential Information – ©2016 FCA US LLC Agenda Corporate and Global Update Scott Thiele Supplier of the Year Awards 3rd Party Perspective from JD Power Jacob George Corporate Quality Update Scott Garberding Intermission North America Update Scott Thiele Industrialization Plan Steve Beahm Supplier of the Year Awards Product Design Ralph Gilles Supplier of the Year Award My Background Manager Director Global Commodity Buyer Supply Base Commodity Analyst Management Management General Manager Director Director Director Global Raw Purchasing Product Cost & Global Technology Materials (2 Positions) Standardization = Whirlpool Director Vice President Vice President Finance Global Product Global P&SQ (2 Positions) Finance = FCA Confidential Information – ©2016 FCA US LLC CORPORATE UPDATE Confidential Information – ©2016 FCA US LLC “Being a supplier to this Group is not a walk in the park, and never will be, because our commitment to the customer is not negotiable.” SERGIO MARCHIONNE Chief Executive Officer - FCA Confidential Information – ©2016 FCA US LLC 2015 Key Figures 15 150 4.6M €110.6B €5.3B COMMERCIAL MARKETS VEHICLES NET ADJUSTED BRANDS SHIPPED REVENUE EBIT 164 40 238,162 84 €4.1B* PLANTS COUNTRIES EMPLOYEES R&D CENTERS INVESTMENT OF OPERATION IN R&D * Includes Ferrari, Capitalized R&D and R&D Charged Directly to the Income Statement Confidential Information – ©2016 FCA US LLC Key Actions for Success: Meeting Business Plan Targets LATAM APAC NAFTA EMEA . -

Car 71.0.0 Обновление По Idc5 Car 70.0.0

Обновление IDC5 CAR 71.0.0 ОБНОВЛЕНИЕ ПО IDC5 CAR 70.0.0 Новая версия ПО IDC5 CAR 71 включает в IDC5 CAR 71 включает более 20000 новых себя только самые лучшие возможности потенциальных вариантов выбора для основных диагностики TEXA для целого ряда брендов марок, присутствующих на мировом рынке, легковых и легких коммерческих автомобилей. среди которых: ALFA ROMEO, AUDI, BENTLEY, Применение этого ПО обеспечивает боль- BMW, BUGATTI, CADILLAC, CHEVROLET, шое число диагностических разработок, спе- CHRYSLER, CITROËN, DAIHATSU, DODGE, DS, циальных функций и технических сведений, FERRARI, FIAT, FORD, GMC, HONDA, HYUNDAI, играющих важную роль для профессионального JAGUAR, JEEP, KIA, LAMBORGHINI, LAND ROVER, выполнения даже самых сложных работ на СТО. LEXUS, LINCOLN, MASERATI, MAZDA, MERCEDES- В этом выпуске было обновлено 63 марки. BENZ, MITSUBISHI, NISSAN, OPEL, PEUGEOT, Кроме того, для 51 из них разработаны новые PORSCHE, RENAULT, ROLLSROYCE, SEAT, SKODA, диагностические системы, которые затраги- SUZUKI, TOYOTA, VOLKSWAGEN, VOLVO. Помимо вают более 900 моделей. Кроме того, транспортных средств на рынках Европы, разработано более 1100 диагностических Северной Америки, Южной Америки и Брази- систем, предназначенных более чем для 250 лии, также предлагается и охват индийского систем. Специалисты TEXA обращали особое рынка. внимание на дальнейшее совершенствование работы с активными системами безопасности ПРИМЕЧАНИЕ: программное обеспечение IDC5 (ADAS), число которых на современных недоступно для приборов старого поколения: автомобилях неуклонно -

Lista De Precios 1/7/2021 O Resumen De Aplicaciones R Este Resumen No Da Información Completa Y Precio ($) WIX MANN-FILTER I N Clasificación Unit

Lista de Precios 1/7/2021 O Resumen de Aplicaciones r Este resumen no da información completa y Precio ($) WIX MANN-FILTER i n Clasificación unit. sin IVA g no puede reemplazar nuestra tabla de e aplicaciones Special order gasket used with base 24759 - this gasket USA Accesories 15661 comes packed with the base $ 68,93 Cabezav Filtros hidráulicos sistemas CATERPILLAR 24759 USA generico 51632, 51746, 51758, 51759, 51846, 51847, $ 4.426,87 Accesories 51849, 51860, 51861 WA10108 C 29 022 USA JCB, Case, New Holland - Secundario WA10188 $ 10.924,00 Accesories WA10188 CF 16 022 USA JCB, Case/New Holland Equipment - Primario WA10108 $ 8.223,74 Accesories Vaso plastico para los codigos 33231 - WF10012 Ford/Volvo USA Accesories WF10136 Trucks $ 2.213,64 Vaso plastico para los codigos 33630 - 33812 - 33813 - USA Accesories WF10137 33774 - 33969 $ 2.493,72 Plastic Bowl Assessory - used w/ these filters: WF10013 - USA Accesories WS10003 WF10014 $ 5.046,64 24888 C 16 140 USA Caterpillar Máquinas Viales $ 4.672,57 Air Filter Sullair Compressors and Various HD Housings (Outer used USA Air Filter 42018 w/42019) $ 20.030,94 42019 USA Various Sullair Compressors (Inner used w/42018 outer) $ 11.738,15 Air Filter Caterpillar (Outer used w/42046 or 46629) Radial Seal USA Air Filter 42045 C 28 848 Version 46607 $ 4.651,36 Caterpillar (Outer used w/42048 or 46511 inner) Radial Seal C 24 165/3 USA Air Filter 42047 Version 46474 - for NanoPro Version use 42047NP $ 2.938,83 GM Family of Cars and Trucks (69-96) - A separate wrap is USA Air Filter 42088 available (part # is 24706) $ 1.357,92 42110 C 1839 USA TOWNMOTOR V-Serie 30, 40, 50 $ 807,54 Air Filter 42114 USA Vortox Housing Applications $ 5.895,29 Air Filter New Holland 1180-1380 motor Fiat, 1580-1880 motor Fiat, USA Air Filter 42119 C 24 719 1380 motor Fiat, 160.90- 180.90 motor Fiat 8365.25 $ 6.263,82 Clark, Cummins, Euclid, Ford H.D. -

CAPEMI BUJES ALFABETICA.Pdf

CAPEMI, Centro Capemi s.r.l. http://localhost/suspension/index.php/capemi-m-1 INICIO » Catálogo » CAPEMI CAPEMI Viendo del 1 al 1844 (de 1844 productos) Páginas de resultado: 1 Modelo Fabricante Nombre de Producto+ ACOPLADOS FRUEHAUF BUJE BALANCIN INTERIOR METALICO CAP3369 CAPEMI (DI 50,8/DE 88,9/LI 111/P 661 GR) ACOPLADOS FRUEHAUF/HUTCHENS BUJE CAP3371 CAPEMI BARRA TORSION (DI 31,75/DE 55,56/LI 60,33/P 164 GR) ACOPLADOS HELVETICA BUJE ELASTICO ELASTICO TRASERO CAP1601 CAPEMI (22,3 INT/49,3 EXT/80 L) 90389-14004 ACOPLADOS HELVETICA BUJE ELASTICO ELASTICO TRASERO CAP1601/1 CAPEMI (22,3 INT/49,8 EXT/64,8 L) 90389-14004 ACOPLADOS HELVETICA BUJE CAP1733 CAPEMI LANZA (50 INT/74 EXT/127 L) ACOPLADOS HELVETICA BUJE CAP3441 CAPEMI TENSOR BRAZO (DI 22,6/DE 47,5/LL 78,4) ACOPLADOS MALDONADO BUJE CAP1754 CAPEMI LANZA (DI 38,3/DE 77,3/LI 83,8/P 610 GR) ACOPLADOS MONTENEGRO/HERMANN BUJE CAP3535 CAPEMI TENSOR (DI 22,5/DE 47/L 78)(1110A0586A) ACOPLADOS MONTENEGRO/MALDONADO BUJE CAP1475 CAPEMI TENSOR (DI 22,3/DE 46,57/LE 70/LI 79/P 365 GR) ACOPLADOS RANDON BUJE CAP3380 CAPEMI BARRA TORSION (DI 30/DE 53,5/LI 62,5/P 133 GR) ACOPLADOS RANDON BUJE TENSOR (DI 40,5/DE 152,5/L CAP3532 CAPEMI 132,5) SUSPENSION NEUMATICA (100000133571/03AXIOS2611) 1 de 124 04/08/2021 06:50 p. m. CAPEMI, Centro Capemi s.r.l. http://localhost/suspension/index.php/capemi-m-1 ACOPLADOS RANDON BUJE TENSOR KIT BUJE CENTRADOR CAP3532/1 CAPEMI SUSPENSION NEUMATICA(DI 30,6)(100000133571/03AXIOS2611) ACOPLADOS RANDON/HELVETICA CAP1773 CAPEMI BUJE TENSOR ACOPLADO (30,4 INT/84,7 EXT/118,8 -

2015 Annual Report

2015 ANNUAL REPORT 2015 | ANNUAL REPORT 3 Table of contents Table of contents Board of Directors and Auditors .................. 5 Consolidated Financial Statements at December 31, 2015 ............................... 133 Letter from the Chairman and the CEO ....... 7 Consolidated Income Statement ....................... 134 Certain Defined Terms .................................. 9 Consolidated Statement of Comprehensive Income/(Loss) ..................... 135 Selected Financial Data .............................. 10 Consolidated Statement of Financial Position .... 136 Creating Value for Our Shareholders ......... 13 Consolidated Statement of Cash Flows ............ 137 Risk Factors ................................................ 14 Consolidated Statement of Changes in Equity .. 138 Overview ..................................................... 31 Notes to the Consolidated Financial Statements .... 139 Our Business Plan ...................................... 34 Company Financial Statements ............... 239 Industry Overview ....................................... 35 Income Statement ............................................ 240 Overview of Our Business .......................... 37 Statement of Financial Position ......................... 241 Operating Results ....................................... 50 Notes to the Company Financial Statements .... 242 Other Information ............................................. 256 Subsequent Events and 2016 Guidance .... 82 Major Shareholders .................................... 84 Appendix -

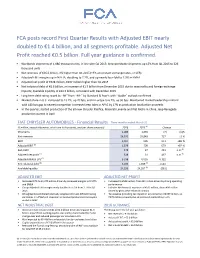

FCA Posts Record First Quarter Results with Adjusted EBIT Nearly Doubled to €1.4 Billion, and All Segments Profitable

FCA posts record First Quarter Results with Adjusted EBIT nearly doubled to €1.4 billion, and all segments profitable. Adjusted Net Profit reached €0.5 billion. Full year guidance is confirmed. • Worldwide shipments of 1,086 thousand units, in line with Q1 2015; Jeep worldwide shipments up 15% from Q1 2015 to 326 thousand units • Net revenues of €26.6 billion, 3% higher than Q1 2015 (+4% at constant exchange rates, or CER) • Adjusted EBIT margins up in NAFTA, doubling to 7.2%, and up nearly four-fold to 1.9% in EMEA • Adjusted net profit of €528 million, €497 million higher than Q1 2015 • Net industrial debt of €6.6 billion, an increase of €1.5 billion from December 2015 due to seasonality and foreign exchange impacts; Available liquidity of €24.3 billion, consistent with December 2015 • Long-term debt rating raised to “BB” from “BB-” by Standard & Poor's with “Stable” outlook confirmed • Market share in U.S. increased to 13.2%, up 70 bps, and in Europe to 6.7%, up 50 bps. Maintained market leadership in Brazil with 180 bps gap to nearest competitor. Increased Jeep sales in APAC by 17% as production localization proceeds • In the quarter, started production of the all-new Chrysler Pacifica, Maserati Levante and Fiat Mobi; in China, Jeep Renegade production started in April FIAT CHRYSLER AUTOMOBILES - Financial Results Three months ended March 31 (€ million, except shipments, which are in thousands, and per share amounts) 2016 2015 (1) Change Shipments 1,086 1,093 (7 ) (1 )% Net revenues 26,570 25,843 727 +3 % EBIT 1,307 696 611 +88 % -

Toyota Will Invest in Expansion in Rio Grande Do Sul

Edition Weekly Brazilian automotive industry news | 7.9 to 7.14.2018 Year XII 838 The step by step of the 19th AutoData Award It is already causing a stir. One day after the announcement of the finalist companies, products and executives of the nineteenth edition of the AutoData Award – The Best of the Automotive Sector, we received many questions about the next steps of this which is the most relevant of the awards of the national automotive industry. More on pg. 4 Toyota will invest in expansion in Rio Grande do Sul São Paulo - Toyota will invest in the expansion of the distribution center in Rio Grande do Sul. On Tuesday, 10, the president Rafael Chang signed an agreement with the state government. The value of the investment remains undefined – even so the executive’s expectation is to increase the unit’s staff and attract new suppliers: More on pg. 2 Company Toyota will invest in expansion in Rio Grande do Sul Karine Viana/Palácio Piratini. Bruno de Oliveira | [email protected] ão Paulo - Toyota will invest in the America. Vehicles produced in Argentina, Sexpansion of the distribution center such as the Hillux pickup truck and the SW4 in Rio Grande do Sul. On Tuesday, 10, the SUV, for example, are received in the place president Rafael Chang signed an agreement before entering the national market. The with the state government. The value of the same happens with the models produced investment remains undefined – even so the here, which pass through the facility before executive’s expectation is to increase the unit’s being exported - a procedure similar to what staff and attract new suppliers: happens with auto parts and components that the Brazilian operation receives from other “We signed a commitment to increase our intercompany units. -

2017 Annual Report

2017 ANNUAL REPORT 2017 | ANNUAL REPORT 3 Table of contents Table of contents Board of Directors and Auditor ...................... 5 Consolidated Financial Statements at December 31, 2017 ................................ 135 Letter from the Chairman and the CEO ......... 7 Consolidated Income Statement ...................... 136 Consolidated Statement Board Report ................................................ 11 of Comprehensive Income/(Loss) ..................... 137 Certain Defined Terms ....................................... 12 Consolidated Statement of Financial Position ... 138 Selected Financial Data ..................................... 13 Consolidated Statement of Cash Flows ............ 139 Risk Factors ...................................................... 16 Consolidated Statement of Changes in Equity .. 140 Overview ........................................................... 32 Notes to the Consolidated Financial Statements .. 141 Our Business Plan ............................................. 34 Company Financial Statements ................ 233 Overview of Our Business .................................. 35 Income Statement ............................................ 234 Operating Results .............................................. 44 Statement of Financial Position ......................... 235 Subsequent Events and 2018 Guidance ............ 76 Notes to the Company Financial Statements .... 236 Other Information ............................................. 246 Major Shareholders .......................................... -

TABELA-IPVA-2020.Pdf

COORDENADORIA DE ARRECADAÇÃO - COART TABELA DE VALORES A RECOLHER REFERENTE AO IPVA EXERCICIO 2020 - ANO FABRICAÇÃO 2005 A 2019 - VALORES EXPRESSOS EM REAIS (R$) ANEXO I A QUE SE REFERE A INSTRUÇÃO NORMATIVA N.º 87 , DE 16 DE DEZEMBRO DE 2019 TIPO MARCA ALIQ DENAT DESCRIÇÃO POT CIL COMB 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 AUTOMÓVEL AMERICAR 3.0% 160901 AMERICAR/CLASSIC XK 120 179 2850 G 891,54 855,66 824,94 695,37 683,73 625,23 578,67 543,96 459,57 ASA 2.5% 161000 ASA/CAUYPE SPORT 97 1800 G 543,53 494,65 455,65 388,60 346,33 319,80 309,58 303,28 243,83 221,53 203,70 162,83 ASTON MARTIN 3.5% 105006 I/ASTON MARTIN V8VANTAGE 420 4735 G 15.961,44 12.555,34 9.743,23 9.302,93 8.807,47 AUDI 3.0% 106026 I/AUDI A3 1.6 102 1595 G 902,16 822,54 106035 I/AUDI A4 1.8T 150 1781 G 2.416,32 1.013,94 805,68 744,53 106074 I/AUDI A3 SPB 1.6 102 1595 G 1.211,25 1.083,96 1.039,41 906,42 811,20 106093 I/AUDI A4 2.0T 180HP 180 1984 G 1.557,81 1.376,73 1.280,37 1.160,13 106095 I/AUDI A4 AV 2.0T 180HP 180 1984 G 1.757,55 1.430,13 1.307,64 1.156,59 106101 AUDI/A3 1.8 125 1781 G 568,17 528,42 106102 AUDI/A3 1.8T 150 1781 G 577,74 559,24 106103 AUDI/A3 1.6 101 0 G 565,32 543,00 106148 I/AUDI A1 1.4TFSI 122 1390 G 1.714,83 1.638,72 1.480,98 1.445,19 1.320,00 106168 I/AUDI A5 SPB 2.0TFSI AT 180 1984 G 2.929,11 2.647,15 2.524,32 106169 I/AUDI A4 2.0TFSI 180 1984 G 4.335,72 4.033,14 3.732,36 3.393,60 2.447,97 2.110,59 1.867,20 1.660,26 106175 I/AUDI A1 SPB 1.4TFSI 122 1390 G 2.733,81 1.931,55 1.896,81 1.646,55 1.602,21 106187 I/AUDI -

Fiat Chrysler Automobiles N.V. Fiat Chrysler Finance Europe

Base Prospectus Supplement dated March 23, 2020 to the Base Prospectus dated March 28, 2019 Fiat Chrysler Automobiles N.V. (Incorporated as a public limited liability company (naamloze vennootschap) under the laws of the Netherlands No. 60372958) as Issuer and as Guarantor, in respect of Notes issued by Fiat Chrysler Finance Europe société en nom collectif and Fiat Chrysler Finance Europe société en nom collectif (Incorporated with limited liability under the laws of the Grand-Duchy of Luxembourg; Registre de Commerce et des Sociétés de Luxembourg No. B-59500) as Issuer €20,000,000,000 Euro Medium Term Note Programme This base prospectus supplement (the Supplement) is supplemental to and should be read in conjunction with the Base Prospectus dated March 28, 2019 (the Base Prospectus), the Base Prospectus supplement dated June 7, 2019, the Base Prospectus supplement dated August 12, 2019 and the Base Prospectus supplement dated November 25, 2019 in relation to the €20,000,000,000 Euro Medium Term Note Programme (the Programme) of Fiat Chrysler Automobiles N.V. (FCA) and Fiat Chrysler Finance Europe société en nom collectif (FCFE) (each an Issuer and together the Issuers). The payments of all amounts due in respect of Notes issued by FCFE will be unconditionally and irrevocably guaranteed by FCA (in such capacity, the Guarantor). This Supplement constitutes a base prospectus supplement for the purposes of Article 16 of Directive 2003/71/EC, as amended (the Prospectus Directive) and is prepared in connection with the Programme. This Supplement has been approved by the Central Bank of Ireland (the Central Bank), as competent authority under the Prospectus Directive. -

2016 Annual Report

2016 ANNUAL REPORT 2016 | ANNUAL REPORT 3 Table of contents Table of contents Board of Directors and Auditor .................... 5 Consolidated Financial Statements at December 31, 2016 ............................... 135 Letter from the Chairman and the CEO ....... 7 Consolidated Income Statement ....................... 136 Board Report .............................................. 11 Consolidated Statement of Comprehensive Income/(Loss) ..................... 137 Certain Defined Terms ........................................ 12 Consolidated Statement of Financial Position .... 138 Selected Financial Data ...................................... 13 Consolidated Statement of Cash Flows ............ 139 Sustainable Value for Our Shareholders .............. 16 Consolidated Statement of Changes in Equity .. 140 Risk Factors ....................................................... 17 Notes to the Consolidated Financial Statements .... 141 Overview ............................................................ 34 Our Business Plan .............................................. 36 Company Financial Statements ............... 245 Industry Overview ............................................... 37 Income Statement ............................................ 246 Overview of Our Business ................................... 39 Statement of Financial Position ......................... 247 Operating Results ............................................... 53 Notes to the Company Financial Statements .... 248 Subsequent Events and 2017 Guidance ............