SURVEY of DOWNTOWN OFFICE SPACE, June 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

City of Rochester Name: Raul Salinas Downtown Name: Center City District County: Monroe

Rochester, NY Submission to the Downtown Revitalization Initiative 6/10/2016 Executive Summary The revitalization of downtown Rochester must engage and retain young adults as residents who want to live and work in cities. A recent Urban Land Institute and National League of Cities supported a study of downtown Rochester, NY identified an immediate need to re-activate the Genesee Riverfront and Main Street to target diverse young adults and bring vibrancy to the fronts of downtown buildings. Critical to re-activating Rochester’s downtown is giving the job to rebuild it to the people who need the work the most. Thanks to the efforts of the Governor’s Rochester Anti-Poverty Task Force and the local Rochester Monroe Anti-Poverty Initiative (RMAPI), the anti-poverty program pilot area is adjacent to Rochester’s downtown district. The program will provide employment supports (e.g. daycare and transportation) to stabilize families and connect them to Rochester’s downtown success. Rochester’s downtown district, the Center City District (CCD), is experiencing dramatic residential growth. Developers partnered with government to create new living spaces within iconic buildings. Despite the 1.7 million people visiting the district annually and record investment in downtown growing high tech firms, retail and walkable amenities do not support 18 hours of activity. Foot traffic by young adults connecting downtown living and work will bridge the gap between living and work that exists in downtown Rochester, NY. Young adults are drawn to an iconic city and will create the demand for first floor retail that will give jobs and stabilize neighborhoods. -

Rochester I D CHARLES F

ETERAN HE IS independent and prond, yet democratic fortunate people in the world, and the U. S. the and friendly. He is the envy of the rest of the world, greatest nation on earth. and its hope. He is generous and tolerant and peace In the plants of the General Electric Company, loving-and withal the most powerful man in the working with General Electric scientists and engi world. He is the American workman. neers, this man, the American workman, has made His hands, accustomed to the feel of wrench and giant generators to light whole cities, X-ray tubes lever and gauge, may never have held a gun; his to penetrate the mysteries of human flesh and metal mind, trained to think in terms of tolerances as fine castings, radio and television apparatus to project as 1/10,000 of an inch, may never have wrestled with man's voice and image through space over the a problem of military strategy; and yet he is the mysterious waves of the ether. veteran of a thousand campaigns. Today, in the gravest hour of world histOry, he is His campaigns began in the laboratories, and his engaged in the greatest campaign of all. But there is prowess was proved in the test pits of American serenity and confidence in his face, and the experience industry. His battles were waged on the factory of a thousand campaigns behind him. He is sure of floor and in the field. His victories have helped to his own abilities, certain of his country's future. -

Historic Erie Canal Aqueduct & Broad Street Corridor

HISTORIC ERIE CANAL AQUEDUCT & BROAD STREET CORRIDOR MASTER PLAN MAY 2009 PREPARED FOR THE CITY OF ROCHESTER Copyright May 2009 Cooper Carry All rights reserved. Design: Cooper Carry 2 Historic Erie Canal AQUedUct & Broad Street Corridor Master Plan HISTORIC ERIE CANAL AQUEDUCT & BROAD STREET CORRIDOR 1.0 MASTER PLAN TABLE OF CONTENTS 5 1.1 EXECUTIVE SUMMARY 23 1.2 INTRODUCTION 27 1.3 PARTICIPANTS 33 2.1 SITE ANALYSIS/ RESEARCH 53 2.2 DESIGN PROCESS 57 2.3 HISTORIC PRECEDENT 59 2.4 MARKET CONDITIONS 67 2.5 DESIGN ALTERNATIVES 75 2.6 RECOMMENDATIONS 93 2.7 PHASING 101 2.8 INFRASTRUCTURE & UTILITIES 113 3.1 RESOURCES 115 3.2 ACKNOWLEDGEMENTS Historic Erie Canal AQUedUct & Broad Street Corridor Master Plan 3 A city... is the pulsating product of the human hand and mind, reflecting man’s history, his struggle for freedom, creativity and genius. - Charles Abrams VISION STATEMENT: “Celebrating the Genesee River and Erie Canal, create a vibrant, walkable mixed-use neighborhood as an international destination grounded in Rochester history connecting to greater city assets and neighborhoods and promoting flexible mass transit alternatives.” 4 Historic Erie Canal AQUedUct & Broad Street Corridor Master Plan 1.1 EXECUTIVE SUMMARY CREATING A NEW CANAL DISTRICT Recognizing the unrealized potential of the area, the City of the historic experience with open space and streetscape initiatives Rochester undertook a planning process to develop a master plan which coordinate with the milestones of the trail. for the Historic Erie Canal Aqueduct and adjoining Broad Street Corridor. The resulting Master Plan for the Historic Erie Canal Following the pathway of the original canal, this linear water Aqueduct and Broad Street Corridor represents a strategic new amenity creates a signature urban place drawing visitors, residents, beginning for this underutilized quarter of downtown Rochester. -

FINGER LAKES 2019 Progress Report FINGER LAKES REGIONAL ECONOMIC DEVELOPMENT COUNCIL MEMBERS LIST: Table of Contents CO-CHAIRS

New York: FINGER LAKES 2019 Progress Report FINGER LAKES REGIONAL ECONOMIC DEVELOPMENT COUNCIL MEMBERS LIST: Table of Contents CO-CHAIRS Anne Kress List of Council Members ...................................................................................... 2 Monroe Community College Message from the Co-Chairs ............................................................................ 4 Bob Duffy I. EXECUTIVE SUMMARY ................................................................. 6 Greater Rochester Chamber of Commerce II. PROGRESS ..................................................................................... 10 APPOINTED MEMBERS General Progress in the Region ......................................................................12 Status of Past Priority Projects .........................................................................15 Ginny Clark Wade Norwood A. Douglas Berwanger Leverage of State Investment Past Priority Projects .................................15 Wild Star Partners Foundation Common Ground Health Wyoming County Board of Supervisors Chair Status of All Projects Awarded CFA Funding .............................................16 Matt Cole Peter Robinson Aggregated Status of All CFA Projects .........................................................16 Commodity Resource Corp. University of Rochester Cheryl Dinolfo Leverage of State Investment in All CFA Projects ......................................17 Monroe County Executive Job Creation .........................................................................................................17 -

Gilbert Mccurdy and Max Farash Theodore E

CLASS NOTES Eva Hess McNett ’53, IN MEMORIAM February 2010 Virginia Hall Meyer ’53, March 2010 Charles L. Werner ’53, March 2010 Manuela Crespo Bryant ’54, November 2009 Charles G. Graham ’54, March 2010 Esther Gerber Landreth ’54, February 2010 Alan M. Lazerson ’54, January 2010 Richard E. Maxwell ’54, February 2010 Erwin H. Sapiro ’54E, ’55E (MM), adVISORS: Businessman and Interfaith Chapel benefactor Gilbert McCurdy (left) and February 2010 real estate developer Max Farash served as trustees over the course of three decades. James D. Sharps ’54, February 2010 TribuE T Mary Watson ’54E, ’56E (MM), March 2010 Leaders and Benefactors: Alexander F. Kowalski ’55, February 2010 Gilbert McCurdy and Max Farash Theodore E. Guglin ’56W (Mas), t wo longtime members of the University f or more than half a century, Mccurdy and March 2010 family—former trustees Gilbert Mccurdy his family have been generous supporters of Dorothy Payne ’56E, ’74E (DMA), and Max farash—died in february. the University. the River campus Interfaith March 2010 Mccurdy, the grandson of the founder of chapel was a gift of the family in the 1960s, Donna Renton ’57E, the family’s downtown department store, and Mccurdy and his wife, katherine August 2009 served as a trustee from 1971 to 1993 babcock Mccurdy, made many gifts to the Edward J. Shaughnessy ’57W (Mas), and was elected a life trustee in 1997. He Memorial Art Gallery, the Eastman school, November 2009 died february 16 at the age of 87. A noted and to Arts, sciences, and Engineering. Joyce Burlingame Shwabe ’58N, leader in the business and philanthropic f arash, the founder of farash corp., one February 2010 communities of Rochester, he served as of the largest real estate development com- Joan Korn Starkweather ’58, chairman and cEO of Mccurdy’s from 1962 panies in western New york, died february January 2009 to 1992. -

URMC/Strong Memorial Hospital COVID-19 Vaccination Progress

URMC/Strong Memorial Hospital COVID-19 Vaccination Progress The University of Rochester Medical Center/Strong Memorial Hospital has followed all guidance and requirements issued by New York State Department of Health related to Covid19 vaccine eligibility, and has been active in our community to assure equity in vaccine administration, with particular outreach to underserved urban populations. Vaccination Statistics as of Tuesday 1/26/2021: Activity Numbers Notes First doses received as of 18,030 1/25/2021 Includes 688 doses provided to our employees First doses given to SMH 18,718 through allocations from Rochester Regional, employees as of 1/26/2021 Highland and Unity hospitals SMH/URMC employees fully 8,993 Includes first and second doses vaccinated as of 1/27/21 Eligible healthcare workers in the community, Individuals vaccinated not residents/employees of congregate living and 5,552 employed by URMC care homes, eligible persons 65 and over, and persons in eligible 1b occupational groups. December 14-January 11 • Employee Vaccination Program: Initially, URMC/SMH followed the December NYSDOH guidance for being considered in the 1A eligibility category. Given the limited vaccine supply, employees at highest risk for Covid19 exposure (Critical Care, Units with Covid19 patients, Emergency Department, Perioperative units, etc.) were invited to be vaccinated in the first weeks of vaccine availability through SMH Employee Health department. Subsequently, all other healthcare workers who met the NYS 1A eligibility guidelines, including community-based healthcare workers who had an affiliation with our healthcare system, were invited to be vaccinated. We also included medical, nursing and other allied health students who were beginning rotations in our clinic areas. -

2020 Sales Tax Exemption Package (As Sent) (COMIDA Li Cycle Inc.)

HARRIS BEACH ATTORNEYS AT LAW October 5, 2020 99 GARNSEY ROAD PITTSFORD, NY 14534 (585) 419-8800 RACHEL C. BARANELLO, ESQ. DIRECT: (585) 419-8769 VIA E-MAIL ONLY FAX: (585) 419-8816 [email protected] Bruce Maclnnis, CFO Li-Cycle Inc. 2351 Royal Windsor Drive, Unit 10 Mississauga, ON L5J 4S7 Re: County of Monroe Industrial Development Agency ("COMIDA") Li-Cycle Inc. Project located at Building 350 in the Eastman Business Park on Mt. Read Boulevard in the Town of Greece, NY Dear Mr. MacInnis: Pursuant to your request, enclosed herewith please find documentation which provides for sales tax exemption for your ongoing project referenced above until the date of December 31, 2021. Please review the enclosed package carefully to ensure full compliance with State sales tax requirements so you do not jeopardize your Company's benefits. If you have any questions regarding the enclosed or otherwise, please feel free to contact me or my paralegal, Lori Palmer at 419-8681. Very truly yours. e Rachel C. Baranello RCB/lap Enc. 31263641834-6108-5389\v1 NOTICE Please be advised NYS has now required IDAs to recapture from the approved project applicant, excess sales tax savings over and above the amount stated in the original sales tax package. Therefore, please examine the amount of sales tax savings carefully because you (as the approved project applicant) will be required to reimburse NYS for any amount received over and above what was stated on the Form ST-60. If you anticipate that your project sales tax amount will exceed the amount initially anticipated, please contact the Executive Director at COMIDA immediately [(585) 753- 2000] whereupon the IDA will consider if a revised Form ST-60 can be issued. -

Light Rail Potential in Rochester, New York

TRB Special Report 195 73 Light Rail Potential in Rochester, New York SIGURD GRAVA, Parsons Brinckerhoff Quade & Douglas, Inc. The development of public transit in the United States is farebox revenues exceeded operating expenses in only one again at a crossroads. The administration in Washington year (1943). Patronage peaked at 5 million in 1949, but slid has made policy statements and begun to implement pro- to about a million in the mid-1950s. By then the line was grammatic changes that significantly differ or diametri- becoming dilapidated because of deferred maintenance; cally oppose trends that dominated the recent past. What after disputes between the city and the corporation as to the future holds, or what adjustments will be required to financial responsibility, service was discontinued in 1956 existing transit services and to plans for system expansion, (the year of the Interstate Highway Act). is uncertain. it is clear, however, that a turning point has For several decades thereafter, the "ditch" in been reached. Light rail is regarded differently than heavy Rochester stayed in the memories of transit specialists and rail or buses. Heavy rail is in considerable disfavor planners: "Shouldn't the service be reactivated?" "What because of high capital costs; buses are in favor because are they going to do with it?" A partial, although negative, they are simple and responsive; light rail is left somewhere answer was provided in the context of the highway building in the middle. A recently "discovered' mode, light rail boom that swept the nation in the 1960s. Rochester is one does not have the documented use in North America to of the few cities in the United States that actually built a allow nondebatable forecasts and estimates of its merits. -

Southeast Rochester Catholic Community

Blessed Southeast Sacrament Rochester SaintCatholic Boniface Community Saint Mary’s www.southeastrochestercatholics.org Southeast Rochester Catholic Community www.southeastrochestercatholics.org January 12, 2020 June 7, 2020 The Baptism of the Lord The Most Holy Trinity WELCOME EVERYONE: No matter who you are, no matter where you've been, no matter what you've done, you are invited, accepted and most welcome in our parish communities. We hope Christ will bring fullness into your life, and that we can provide you with the spiritual support and information you need. Mass Schedule Blessed Sacrament Saint Boniface Saint Mary’s 534 Oxford Street 330 Gregory Street 15 St. Mary’s Place Rochester, New York 14607 Rochester, New York 14620 Rochester, New York 14607 259 Rutgers Street (mailing) 259 Rutgers Street (mailing) 259 Rutgers Street (mailing) Rochester, New York 14607 Rochester, New York 14607 Rochester, New York 14607 (585) 271-7240 (585) 271-7240 (585) 271-7240 (585) 442-7517 Fax “All public Masses in the Diocese of Rochester have been suspended until further notice.” “Those seeking to celebrate the Sacrament of Penance in individual confessions, please contact one of our parish priests to schedule a time.” Parish Offices are located in the Rectory of Blessed Sacrament Church Hours are Monday through Friday 8:30am-4:30pm Parish Office is closed and will remain closed due to the NYS COVID19 Mandate Low gluten Nursery available at hosts Download our app! Find Blessed Sacrament & St. available it on iTunes or Google Mary’s at both Masses. Check in the southeastrochestercatholics.org Click on Ways You Can Give Play! Ask the Ushers to direct Sacristy you. -

Rochester's Landmark Buildings

Rochester’s Landmark Buildings (and their stories) by Tom Fortunato A presentation for the Rochester Philatelic Association, 2020 The City of Rochester, NY has a rich architectural history seen through its buildings of today and images of the past. Iconic companies and wealthy businessmen often built skyscrapers downtown that took their name, including Kodak, Xerox and Bausch & Lomb. The buildings are still here while their original occupants are gone. Here are seven classic structures still on the city skyline you may not be so familiar with. Next time you drive by you’ll know more about them. This brief presentation uses advertising covers, postcards and photos to make the reader aware of what was and still is in the Flower City. Enjoy! Let’s start out with an easy quiz… How many of these Rochester sites can you identify from 1937? Look at Answers each appear letter on the and next identify slide. the They are landmark all still shown. around! How did you do? R Eastman S Cumberland Theater Post Office O U of R T Driving Park Library Bridge C Highland E Charlotte Park Bath House H Public R Auditorium Library Theater E Veteran’s Memorial Bridge Buildings in this presentation include: West Main St Area • Duffy-Powers Building • Powers Building/Hotel • German Insurance Company Building • Ellwanger and Barry Building East Main St Area • Wilder Building • Granite Building • Sibley Triangle Building These classic buildings are all in central downtown, most around the “Four Corners” intersection of Main and State streets. 100 Acre Plot Tour Look for web links like this throughout the presentation to learn more about the buildings. -

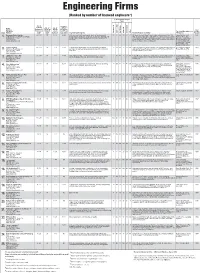

Engineering Firms (Ranked by Number of Licensed Engineers*) % of Total Work Project Types

Engineering Firms (Ranked by number of licensed engineers*) % of Total Work Project Types No. of Total Area Licensed Name 1 No. of No. of Office Address Engineers / Technical Offices Billings for Year Telephone Total Local Support Local / Last Fiscal Top Local Executive(s) or 2 3 4 5 6 Locally Rank Website Staff Staff National Year ($000) Engineering Disciplines Commercial Construction Gov't/Munic. Industrial Institutional Other Notable Projects or Clients Principal(s) Founded Bergmann Associates Inc. 63 / 215 170 1 / 10 36,000 Civil, structural, traffic, mechanical, electrical, environmental, 25 0 30 25 20 0 Mt. Hope Avenue/College Town Corridor redevelopment; New York James Buckley, chief 1980 1. 28 E. Main St., 200 First Federal Plaza transportation, architecture, landscape architecture, planning, 3-D State Canal movable dam rehab and flood-control enhancement; City financial officer, Pete Rochester, N.Y. 14614 design, interior design, geographical information systems and of Rochester Intermodal Transportation Center; I-390 / I-490 Western Giovenco, vice president, (585) 232-5135 surveying Crossroads project; El Camino “Rail to Trail” conversion; University of Robert McCubbin, vice www.bergmannpc.com Rochester Warner School of Education president, William Miles, vice president, Thomas Mitchell, CEO, John Murray, vice president Erdman Anthony 36 / 113 49 1 / 7 14,126 Transportation engineering; facilities engineering and design 16 30 36 2 16 NA Radio City Music Hall laser scanning; Lake Champlain bridge erection Curt Helman, president, 1954 2. 145 Culver Road, Suite 200 services; civil engineering; geospatial services and construction engineering; Dorsey Road reconstruction and Broome Community Russell Bullock, CEO Rochester, N.Y. -

ROCHESTER CITY COUNCIL REGULAR MEETING May 12, 2020

ROCHESTER CITY COUNCIL REGULAR MEETING May 12, 2020 Due to the social distancing and other health and safety measures necessary to slow the progress of the COVID-19 pandemic and in accordance with emergency Executive Orders issued by the Governor and Local Emergency Orders issued by the Mayor, the meeting was conducted via video conferencing on Zoom and streamed live for public viewing on the Internet via the Council's Facebook and YouTube pages and on City 12, the City's government access channel that is available to Spectrum Cable subscribers – Channel 1303. Present –President Scott, Councilmembers Evans, Gruber, Harris, Lightfoot, Lupien, Ortiz, Patterson, Peo – 9. President Scott requested the Council to pause for a Moment of Silence. Pledge of Allegiance to the Flag of the United States of America. Retirement: DES: *John Caraballo *Barr Miesch DHRM: *Choyce Bush NBD: *Lawrence Fedick RFD: *Daniel Caufield *Ricardo Cortez *James Hydock *Joseph O’Gorman *Jerry Randise RPD: *Lloyd Cuyler *Kevin Riley *Thomas Rodriguez *Walter Sanders *Mark E. Simmons *Brett Sobieraski *Not attending meeting May 12, 2020 APPROVAL OF THE MINUTES By Vice President Lightfoot RESOLVED, that the minutes of the Regular Meeting on April 14, 2020 be approved as published in the official sheets of the Proceedings. Adopted unanimously. COMMUNICATIONS FROM THE MAYOR, COUNCIL PRESIDENT, CORPORATE OFFICERS AND OTHERS. THE CITY CLERK---THE FOLLOWING DOCUMENTS ARE HEREBY DIRECTED TO BE RECEIVED AND FILED: The Mayor submits the following: Quarterly Report NBD Grants Report – March 31, 2020 Quarterly Report PSA costs of less than $10,000 – March 31, 2020 The Council submits Disclosure of Interest Form from Councilmember Harris on Int.