Trading System Development

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Algorithmic Approach to Options Trading

International Research Journal of Engineering and Technology (IRJET) e-ISSN: 2395-0056 Volume: 08 Issue: 05 | May 2021 www.irjet.net p-ISSN: 2395-0072 Algorithmic Approach to Options Trading Shubham Horambe1, Ketan Khanolkar1, Dhairya Dixit1, Huzaifa Shaikh1, Prof. Manasi U. Kulkarni2 1B. Tech Student, Dept of Computer Engineering and IT, VJTI College, Mumbai, Maharashtra, India 2 Assistant Professor, Dept of Computer Engineering and IT, VJTI College, Mumbai, Maharashtra, India ----------------------------------------------------------------------***--------------------------------------------------------------------- Abstract - Majority of the traders lose money whilst trading sitting in front of the screen for hours. Due to this continuous in options owing to market speculation, emotional trading and monitoring requirement, the performance of Manual Trading lack of risk management. The purpose of this research paper is is limited to the amount of time of the day the trader can to introduce an automated way of trading in options in order dedicate to trading. Other than this, Manual Trading also to tackle these problems. To achieve this, we have adopted suffers from time delays, which is the ability to execute some basic option strategies namely Covered Call, Protective trades in a small-time window. Also, for predicting Put and Covered Strangle. These strategies have been tested unprecedented non-random changes that take place in trade over a period of 5 years (2015-2019) for a set of stocks in the prices, a trader must delve into and analyze more and more U.S options market. information which is more powerful than information available on open-sources like news platforms. This is very Key Words: Options, Algorithmic Trading, Call Option, Put difficult to do for humans, as unlike computers, we can Option. -

Front Office Middle Office Back Office

HEDGE FUND TECHNOLOGY Front Office Page 2 Research and Analysis Page 4 Trade Execution and Management Page 8 Portfolio Management Middle Office Page 11 Data Management Page 13 Risk Management Page 15 Cash and Collateral Management Page 16 Securities Pricing and NAV Calculation Page 17 Investor Relations Page 18 Trade Reconciliation and Processing Back Office Page 19 Accounting Page 21 Compliance and Reporting Page 24 Administration Page 25 IT Security and Support HEDGE FUND ALERT: 5 Marine View Plaza, Suite 400, Hoboken NJ 07030. 201-659-1700 To start your FREE trial subscription, return to HFAlert.com and click on “Free Trial”. Or call 201-659-1700. You can also complete the Free Trial Coupon on the last page of this newsletter and fax it to 201-659-4141. Hedge Fund 2 ALERT HEDGE FUND TECHNOLOGY FRONT OFFICE: Research and Analysis FRONT OFFICE: Research and Analysis Vendor Product The Skinny AIM Software GAIN Corporate Actions DM Tracks various corporate events for companies in an investment portfolio, enabling aimsoftware.com the manager to react promptly to announcements. Austrian vendor founded in 1999. Arialytics Aria Aims to reduce the time it takes to identify, design and review trading algorithms. arialytics.com Created with new and emerging managers in mind. Allows users to quickly analyze big-data sets to identify patterns and predictors. Machine-learning component tweaks models in response to real-time activity. Rye, N.Y., vendor founded in 2010 by David Marra, previously a principal at Boston Consulting. Dataminr Dataminr Continually monitors and analyzes publicly available Twitter feeds for information dataminr.com about companies and investments. -

Risk Management & Trading Conference

RiskMathics, aware that the most important factors to develop and consolidate the Financial WHO SHOULD ATTEND? Markets are training and promoting a high level financial culture, will host for the third time in The Risk Management & Trading Conference is aim at Practitioners directly or indirectly involved Mexico: “The Risk Management & Trading Conference”, which will have the participation of in areas of trading, risk management, regulation, technology, and research & development of leading authorities who have key roles in the global financial industry. Stock Exchanges, Brokers, Brokerage Houses, Banks, Institutional Investors (Pension Funds, OBJECTIVES Mutual Funds, Insurance Companies, etc.), Hedge Funds, and Independent Investors. One of the primary objectives of this Conference is to provide through Workshops, Presentations It will be of particular relevance to: and Round Table Discussions the latest advances in Risk Management, Trading, Technology • Chief Executive Officers of financial institutions and intermediaries and Market Regulation, and to transmit all this knowledge by local and international authorities • Traders in the field. • Risk Managers Some other objectives of this Conference are to explain and show in detail the current • Consultants situation and where the Global Financial Industry is heading, advances in Pricing, and how • Regulators intermediaries and direct or indirect participants of markets need to be prepared to remain • Technology managers and staff competitive in spite of the new challenges and paradigms -

2004 to March 2021, the S&P 500 Index’S Annual Return Was 9.85% with a Maximum

RO4 1 Using Machine Learning and Algorithmic Trading to Beat the U.S. Stock Market Index by Chih-yu LEE and Matthew Johann Siy UY RO4 Advised by Prof. David Paul ROSSITER Submitted in partial fulfillment of the requirements for COMP 4981 in the Department of Computer Science and Engineering The Hong Kong University of Science and Technology 2020-2021 Date of submission: April 14, 2021 2 Abstract The project aims to develop investment strategies that can achieve higher returns with lower risks than the S&P 500 Index by applying Machine Learning techniques to traditional investment strategies. In total, we implemented and backtested three Machine Learning-based investing strategies: Harry Browne Permanent Portfolio with LSTM (HBLSTM), Stock Selection with Natural Language Processing (SSNLP), and Pairs Trading with PCA and Clustering (PTPC). From December 2004 to March 2021, the S&P 500 Index's annual return was 9.85% with a Maximum Drawdown (MDD) of 55.1%. On the other hand, two of our Machine Learning-based investment strategies, HBLSTM and SSNLP, were able to achieve both a significantly higher annual return and a lower MDD. HBLSTM had an annual return of 20.4% with an MDD of 18%, while SSNLP had an annual return of 14.8% and an MDD of 33.4%. Although PTPC merely had an annual return of 2.97% with an MDD of 31.6%, we noticed that its role is insurance that generates positive return over time as it performed well during the crises. Finally, our Combined Portfolio had an annual return of 9.99% with an MDD of 7.8%, providing further evidence of the benefits of using Machine Learning techniques in investing strategies. -

Successful Algorithmic Trading

Contents I Introducing Algorithmic Trading 1 1 Introduction to the Book . 3 1.1 Introduction to QuantStart . 3 1.2 What is this Book? . 3 1.3 Who is this Book For? . 3 1.4 What are the Prerequisites? . 3 1.5 Software/Hardware Requirements . 4 1.6 Book Structure . 4 1.7 What the Book does not Cover . 5 1.8 Where to Get Help . 5 2 What Is Algorithmic Trading? . 7 2.1 Overview . 7 2.1.1 Advantages . 7 2.1.2 Disadvantages . 8 2.2 Scientific Method . 9 2.3 Why Python? . 9 2.4 Can Retail Traders Still Compete? . 10 2.4.1 Trading Advantages . 10 2.4.2 Risk Management . 11 2.4.3 Investor Relations . 11 2.4.4 Technology . 11 II Trading Systems 13 3 Successful Backtesting . 15 3.1 Why Backtest Strategies? . 15 3.2 Backtesting Biases . 16 3.2.1 Optimisation Bias . 16 3.2.2 Look-Ahead Bias . 16 3.2.3 Survivorship Bias . 17 3.2.4 Cognitive Bias . 17 3.3 Exchange Issues . 18 3.3.1 Order Types . 18 3.3.2 Price Consolidation . 18 3.3.3 Forex Trading and ECNs . 19 3.3.4 Shorting Constraints . 19 3.4 Transaction Costs . 19 3.4.1 Commission . 19 3.4.2 Slippage . 19 3.4.3 Market Impact . 20 3.5 Backtesting vs Reality . 20 4 Automated Execution . 21 4.1 Backtesting Platforms . 21 1 2 4.1.1 Programming . 22 4.1.2 Research Tools . 22 4.1.3 Event-Driven Backtesting . 23 4.1.4 Latency . -

The Basics of Algorithmic Trading

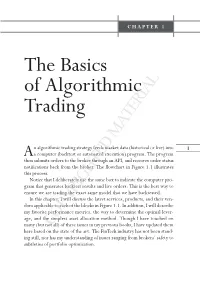

Trim Size: 6in x 9in k Chan c01.tex V2 - 12/11/2016 12:44 A.M. Page 1 CHAPTER 1 The Basics of Algorithmic Trading k n algorithmic trading strategy feeds market data (historical or live) into 1 k Aa computer (backtest or automated execution) program. The program then submits orders to the broker through an API, and receives order status notifications back from the broker. The flowchart in Figure 1.1 illustrates this process. Notice that I deliberately use the same box to indicate the computer pro- gram that generates backtest results and live orders: This is the best way to ensure we are trading the exact same model that we have backtested. In this chapter, I will discuss the latest services, products, and their ven- dors applicable to each of the blocks in Figure 1.1. In addition, I will describe my favorite performance metrics, the way to determine the optimal lever- age, and the simplest asset allocation method. Though I have touched on many (but notCOPYRIGHTED all) of these issues in my previous MATERIAL books, I have updated them here based on the state of the art. The FinTech industry has not been stand- ing still, nor has my understanding of issues ranging from brokers’ safety to subtleties of portfolio optimization. k Trim Size: 6in x 9in k Chan c01.tex V2 - 12/11/2016 12:44 A.M. Page 2 Live market Historical market data data Computer program Order Order status Backtest results Broker API Order Order status Broker’s server k 2 FIGURE 1.1 Algorithmic trading at a glance k ■ Historical Market Data For daily historical data in stocks and futures, I have been using CSI (csidata.com) for a long time. -

Quant Trading Guide

Quant Trading Guide Callum McDougall email [email protected] November 2020 Contents 0 Introduction 2 1 What is quant trading? 3 1.1 Common terminology........................................3 1.2 What does a quant trader do?....................................3 1.3 Quant Trading vs Quant Research.................................4 1.4 Common misconceptions.......................................4 1.4.1 Finance culture is terrible..................................4 1.4.2 The hours in finance are really bad.............................5 1.4.3 You need to be a maths genius...............................5 1.4.4 You need to be a really good coder.............................6 1.4.5 You need lots of finance experience.............................6 1.4.6 You need an amazing CV..................................7 1.4.7 If you make a small mistake in trading, you could lose your job.............7 1.4.8 Working in finance is morally wrong............................8 1.5 Good things about quant trading..................................8 1.6 Bad things about quant trading...................................9 1.7 What to do if you think you might be interested......................... 10 2 Quant Trading Firms & Internships 11 2.1 What is an internship like?..................................... 11 2.2 Internship structure......................................... 12 2.3 Quant trading firms......................................... 13 3 How to prepare for interviews 15 3.1 Solving problems........................................... 15 3.2 Types of interview -

The 'Outsiders'

July 12, 2017 The ‘Outsiders’ - Emerging Ecosystems Equity Research Platforms of Change From Grassroots to Moonshots Rise of the New Robert D. Boroujerdi Year one of a new administration and the (1) DIY Algorithms: Democratizing Finance. (212) 902-9158 [email protected] headlines have kept us busy. Market rotations Dorm rooms to desktops the crowdsourcing of Goldman Sachs & Co. LLC have been swift, the rise of passive unabated and alpha may be the next investment paradigm. the distinction between quant and fundamental (2) Edge Computing. The IT pendulum is once continues to fade. While this construct remains Christopher Wolf, CFA again shifting from centralized (i.e., cloud-based) (212) 934-4221 [email protected] our reality, we pause for a moment to look to decentralized computing in end-devices. Goldman Sachs & Co. LLC beyond the benchmark and peer into seven emerging platforms that exist in the periphery of (3) Big Data & Sports Analytics. From optical our investable universe yet merit close watching. tracking to next-gen wearables, the marriage of science and sport is increasingly ubiquitous. From DIY algorithms broadening the pool of alpha to the multi-billion dollar Dark Net (4) Is Voice the Death of Search? From Siri to economy and the rise of Voice & Digital Cortana, voice search could shake up the $100bn+ Assistants in Search, industries we know are advertising market while also driving its growth. silently reshaping. The blending of science, (5) The Hidden Order of Chaos Theory. What if technology and Sports Analytics is changing the complete disorder is mathematically impossible? nature of engagement between coach, athlete and fan, while the dual forces of AI and the IoT are (6) Alzheimer’s in Focus.