Silvio Gesell, John Maynard Keynes, Irving Fisher

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Negative Nominal Interest Rates: History and Current Proposals

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Research Papers in Economics econstor www.econstor.eu Der Open-Access-Publikationsserver der ZBW – Leibniz-Informationszentrum Wirtschaft The Open Access Publication Server of the ZBW – Leibniz Information Centre for Economics Ilgmann, Cordelius; Menner, Martin Working Paper Negative nominal interest rates: History and current proposals CAWM discussion paper / Centrum für Angewandte Wirtschaftsforschung Münster, No. 43 Provided in cooperation with: Westfälische Wilhelms-Universität Münster (WWU) Suggested citation: Ilgmann, Cordelius; Menner, Martin (2011) : Negative nominal interest rates: History and current proposals, CAWM discussion paper / Centrum für Angewandte Wirtschaftsforschung Münster, No. 43, http://hdl.handle.net/10419/51360 Nutzungsbedingungen: Terms of use: Die ZBW räumt Ihnen als Nutzerin/Nutzer das unentgeltliche, The ZBW grants you, the user, the non-exclusive right to use räumlich unbeschränkte und zeitlich auf die Dauer des Schutzrechts the selected work free of charge, territorially unrestricted and beschränkte einfache Recht ein, das ausgewählte Werk im Rahmen within the time limit of the term of the property rights according der unter to the terms specified at → http://www.econstor.eu/dspace/Nutzungsbedingungen → http://www.econstor.eu/dspace/Nutzungsbedingungen nachzulesenden vollständigen Nutzungsbedingungen zu By the first use of the selected work the user agrees and vervielfältigen, mit denen die Nutzerin/der Nutzer sich -

Complementary Currencies: Mutual Credit Currency Systems and the Challenge of Globalization

Complementary Currencies: Mutual Credit Currency Systems and the Challenge of Globalization Clare Lascelles1 Abstract Complementary currencies—currencies operating alongside the official currency—have taken many forms throughout the last century or so. While their existence has a rich history, complementary currencies are increasingly viewed as anachronistic in a world where the forces of globalization promote further integration between economies and societies. Even so, towns across the globe have recently witnessed the introduction of complementary currencies in their region, which connotes a renewed emphasis on local identity. This paper explores the rationale behind the modern-day adoption of complementary currencies in a globalized system. I. Introduction Coined money has two sides: heads and tails. ‘Heads’ represents the state authority that issued the coin, while ‘tails’ displays the value of the coin as a medium of exchange. This duality—the “product of social organization both from the top down (‘states’) and from the bottom up (‘markets’)”—reveals the coin as “both a token of authority and a commodity with a price” (Hart, 1986). Yet, even as side ‘heads’ reminds us of the central authority that underwrote the coin, currency can exist outside state control. Indeed, as globalization exerts pressure toward financial integration, complementary currencies—currencies existing alongside the official currency—have become common in small towns and regions. This paper examines the rationale behind complementary currencies, with a focus on mutual credit currency, and concludes that the modern-day adoption of complementary currencies can be attributed to the depersonalizing force of globalization. II. Literature Review Money is certainly not a topic unstudied. -

Markets Not Capitalism Explores the Gap Between Radically Freed Markets and the Capitalist-Controlled Markets That Prevail Today

individualist anarchism against bosses, inequality, corporate power, and structural poverty Edited by Gary Chartier & Charles W. Johnson Individualist anarchists believe in mutual exchange, not economic privilege. They believe in freed markets, not capitalism. They defend a distinctive response to the challenges of ending global capitalism and achieving social justice: eliminate the political privileges that prop up capitalists. Massive concentrations of wealth, rigid economic hierarchies, and unsustainable modes of production are not the results of the market form, but of markets deformed and rigged by a network of state-secured controls and privileges to the business class. Markets Not Capitalism explores the gap between radically freed markets and the capitalist-controlled markets that prevail today. It explains how liberating market exchange from state capitalist privilege can abolish structural poverty, help working people take control over the conditions of their labor, and redistribute wealth and social power. Featuring discussions of socialism, capitalism, markets, ownership, labor struggle, grassroots privatization, intellectual property, health care, racism, sexism, and environmental issues, this unique collection brings together classic essays by Cleyre, and such contemporary innovators as Kevin Carson and Roderick Long. It introduces an eye-opening approach to radical social thought, rooted equally in libertarian socialism and market anarchism. “We on the left need a good shake to get us thinking, and these arguments for market anarchism do the job in lively and thoughtful fashion.” – Alexander Cockburn, editor and publisher, Counterpunch “Anarchy is not chaos; nor is it violence. This rich and provocative gathering of essays by anarchists past and present imagines society unburdened by state, markets un-warped by capitalism. -

Free Money of Wörgl & Complementary Currencies

Summer School for Alternative Economic and Monetary Systems Free Money of Wörgl & Complementary Currencies Vienna, July 24th, 2015 Speaker: Heinz Hafner & Veronika Spielbichler Unterguggenberger Institute, Wörgl is a registered non-profit society, founded in 2003 for the documentation and public education on the WWII free money experiment in Wörgl as well as for contemporary research on complementary currencies nowadays. The Unterguggenberger Institute initiated the „LA21 youth project I-MOTION“ in 2004. The society is a founding member of the initiative „Neues Geld in Österreich 2007“ and addressed a petition onto the Austrian Parliament in 2008. unterguggenberger.org archiv.unterguggenberger.org neuesgeld.com Money for the Freedom of Creation • PART I ~15min impuls from the past Free Money of Wörgl („Wörgler Freigeld“) an historic show case • PART II ~15min impuls from the present complementary currencies today options & experiments (flattering & colourful) • PART III ~60min impuls for the future an interactive approach to currency design classification sheet drafting PART #1 – impuls from the past The monetary experiment in Wörgl – Wörgls Free Money a short outline on a historic show case Initial situation: the historic economic situation in the region of Wörgl The driver: Mayor Michael Unterguggenberger – his life Prearrangements of the Free Money experiment: - foundation of the Free Economic Group of Wörgl - political decisions within the municipality Realization: creation of a demurrage voucher, which represented the worth of labour time – monthly charge in the form of stamps that needed to be bought and sticked onto the voucher – construction programme – facilitation of consumption – fostering municipal taxes – creation of an infinite cycle After life of the experiment: Imitations and copycats in Austria, international attention by the media Between 1900 and 1930 the small town of Wörgl Develops as an industrial and commercial center due to its convenient location mainly based on the railway infrastructure. -

IJCCR 2015 Rosa Stodder

International Journal of Community Currency Research VOLUME 19 (2015) SECTION D 114-127 ON VELOCITY IN SEVERAL COMPLEMENTARY CURRENCIES Josep Lluis De La Rosa* And James Stodder** *TECNIO Centre EASY, University Of Girona, Catalonia ** Rensselaer Polytechnic Institute, USA ABSTRACT We analyse the velocity of several complementary currencies, notably the WIR, RES, Chiem- gauer, Sol, Berkshares dollars, and several other cases. Then we describe the diversity in their velocity of circulation, and seek potential explanations for these differences. For example, WIR velocity is 2.6 while RES velocity is 1.9 despite being similar currencies. The higher speed may be explained by WIR blended loans among other beneIits or by the fact that there are nearly 20.000 unregistered members that contribute with their transactions. Using a comparative method between cases, the article explores a number of possible explanations on the increases in velocity, apart from prevailing demurrage approaches ACKNOWLEDGEMENTS I want to thank the several reviewers of this paper, especially Andreu Honzawa of the STRO foundation. This research is partly funded by the TIN2013-48040-R (QWAVES) Nuevos méto- dos de automatización de la búsqueda social basados en waves de preguntas, the IPT20120482430000 (MIDPOINT) Nuevos enfoques de preservación digital con mejor gestión de costes que garantizan su sostenibilidad, and VISUAL AD Uso de la Red Social para Monetizar el Contenido Visual, RTC-2014-2566-7 and GEPID GamiIicación en la Preservación Digital de- splegada sobre las Redes Sociales, RTC-2014-2576-7, the EU DURAFILE num. 605356, FP7- SME-2013, BSG-SME (Research for SMEs) Innovative Digital Preservation using Social Search in Agent Environments, as well as the AGAUR 2012 FI_B00927 awarded to José Antonio Olvera and the Grup de recerca consolidat CSI-ref. -

Agreements and Disclosures

AGREEMENTS AND DISCLOSURES 1604 Cherry Street, Vicksburg, MS 39180 Ph: 877-457-3654 Fax: 601-634-1707 Lost or Stolen Debit or Credit Cards: 800-682-6075 THESE AGREEMENTS AND DISCLOSURES CONTAIN IMPORTANT MEMBERSHIP INFORMATION, NECESSARY TRUTH-IN-SAVINGS ACCOUNT DISCLOSURES,L ELECTRONIC SERVICES AGREEMENT AND DISCLOSURES, FUNDS AVAILABILITY POLICY, WIRE TRANSFER AGREEMENT, AND PRIVACY POLICY DISCLOSURE. PLEASE BE CERTAIN TO READ THESE AGREEMENTS AND DISCLOSURES CAREFULLY AND NOTIFY US AT ONCE IF ANY PARTS ARE UNCLEAR. Throughout these Agreements and Disclosures, the references to "We," "Us," "Our" and "Credit Union" mean MUTUAL CREDIT UNION. The words "You" and "Your" mean each person applying for and/or using any of the services described herein. "Account" means any account or accounts established for You as set forth in these Agreements and Disclosures. The word "Card" means any ATM Card or VISA Debit Card issued to You by Us and any duplicates or renewals We may issue Our Audio Response System is hereinafter referred to as "Mobile Telephone System," whereas Our Personal Computer Account Access System is hereinafter referred to as "Online Banking," and Our Mobile Internet Account Access System is hereinafter referred to as "Mobile Banking." "E-Check" means any check which You authorize the payee to process electronically. For joint accounts, read singular pronouns in the plural. MUTUAL CREDIT UNION MEMBERSHIP To apply for membership with Mutual Credit Union You must complete, sign and such persons. By signing Your application for membership, You acknowledge return an application for membership. receipt of these Agreements and Disclosures, including the terms and conditions which apply to Your Accounts. -

The Future of Money: from Financial Crisis to Public Resource

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Mellor, Mary Book — Published Version The future of money: From financial crisis to public resource Provided in Cooperation with: Pluto Press Suggested Citation: Mellor, Mary (2010) : The future of money: From financial crisis to public resource, ISBN 978-1-84964-450-1, Pluto Press, London, http://library.oapen.org/handle/20.500.12657/30777 This Version is available at: http://hdl.handle.net/10419/182430 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further -

Complementary Currencies and the Global Economy? Peter Brass

Complementary currencies and deflationary crisis Complementary currencies are alternative currencies to the legal tender. Except from foreign reference currencies which sometimes rule out national currencies in some very small countries or suffering emergency economies, complementary currencies are distinguished from the legal tender by different behaviour. Countless approaches page 1 of 16 are possible to design market exchange by alternative monetary systems but most of them can be roughly subdivided into 1) interest free money (Freigeld) 2) local exchange time systems (LETS) 3) barter trade (electronic market places) Our current monetary system of the legal tender is interest based and interest compound is the most powerful mean to collect money, the so called mass gravity behaviour of interest based money. In a long term consideration led the concentration of money capital to an accelerated concentration of productive capital. Due to this, business cycles have shifted more and more from local to global 1) dimensions and local business cycles disappearing slowly. Complementary currencies are a contrary scheme and mainly used on bounded markets or by delimited social groups or communities. It can be seen as a mean to support local business cycles. But the globalization detracts most of the business and leads subsequently to strong reduction of capabilities for transactions in local business cycles. It is more convenient for market participants to use the legal tender and makes it doubtful that in times of non-crisis globalization can be inverted by the mean of these complementary currencies. The capitalized world of west Europe and North America smile at citizen initiatives which run or try to implement these alternative monetary systems. -

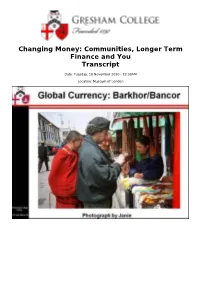

Changing Money: Communities, Longer Term Finance and You Transcript

Changing Money: Communities, Longer Term Finance and You Transcript Date: Tuesday, 16 November 2010 - 12:00AM Location: Museum of London Changing Money: Communities, Longer Term Finance and You Ian Harris, Z/Yen Group 16/11/2010 Good evening Ladies and Gentlemen. I am honoured to have been invited to deliver this third and final guest Gresham Lecture in the "Beyond Crisis" series. This lecture is entitled "Changing Money: Communities, Longer Term Finance & You". Cattle and Pens [SLIDE: OMO VALLEY COMMUNITY SCHOOL] When my partner, Janie, and I travel in the developing world, it has long been our habit to take a healthy supply of basic, ball- point pens with us to give as gifts to children as a small contribution towards their education and therefore development. We are old hands at this now - we learnt many years ago that simply handing pens to children at random is not an educational gift at all, but a gift akin to money. The ball-point pen is a valuable commodity which can be exchanged for other more instantly gratifying items, such as sweets. Or perhaps even cash. In recent years, we have preferred to give the pens through schools, where we are more confident that the teachers will ensure that the children actually use the pens themselves for educational purposes. When we went to Ethiopia a few years ago, we 'struck gold' in a Karo village in the South Omo Valley. The Government had just built the village its first school, which was due to open later that year. But the Government had run out of money for this project before providing consumables for the school. -

A Brief Synopsis of Natural Economic Order by Silvio Gesell

A brief synopsis of Natural Economic Order by Silvio Gesell In spite of the holy promise of all people to banish war, once and for all, in spite of the cry of millions "Never a war again," in spite of all the hopes for a better future, I have this to say: If the present monetary system, based on compound interest, remains in operation, I dare to predict today that it will take less than 25 years before a new and even worse war. I can foresee the coming development clearly. The present degree of technological advancement will quickly result in a record performance of industry. The build-up of capital will be rapid in spite of the enormous war losses, and its over-supply will lower the interest rate. Money will then be hoarded. Economic activity will diminish and an increasing number of unemployed will roam the streets... within the discontented masses, wild, revolutionary ideas will arise, and the poisonous plant called "Super-Nationalism" will proliferate. No country will understand the other, and the end can only be war again. --Silvio Gesell, Letter to Zeitung am Mittag, Berlin 1918 1 Foreword: It is important to keep in mind that no amount of legislature can fix societal ills unless it is directed at the very root of the problem. “Get tough on crime” attitudes never worked exactly because they sought to placate the masses, not eliminate crime. Certainly, it is easy to see that it’s not lenient judges who cause law breaking. Murder, for example, has been illegal since the beginning of our civilization 12,000 years ago, yet they are even more common today than they were in the past. -

Monetary Systems, Sustainable Growth and Inclusive Economic Development

Munich Personal RePEc Archive Monetary systems, sustainable growth and inclusive economic development Omerčević, Edo Finance Department, American School of Economics, American University in Bosnia and Herzegovina, Mije Keroševica Guje 3, 75000 Tuzla, Bosnia and Herzegovina 29 January 2013 Online at https://mpra.ub.uni-muenchen.de/44559/ MPRA Paper No. 44559, posted 23 Mar 2013 08:45 UTC 1 Omerčević, Edo, 2013. Monetary systems, sustainable growth and inclusive economic development. Paper presented at the 2nd International Conference on Islamic Economics and Economies of the Muslim Countries. January 29-30. Available at: <http://mpra.ub.uni-muenchen.de/id/eprint/44559>. Monetary systems, sustainable growth and inclusive economic development Edo Omerčević Finance Department, American School of Economics, American University in Bosnia and Herzegovina, Mije Keroševica Guje 3, 75000 Tuzla, Bosnia and Herzegovina Tel: (387) 35 321 050, Fax: (387) 35 340 100, E-mail: [email protected] Abstract: The main objective of this study is to review the literature on monetary issues and discuss how money and monetary systems contribute to the achievement of sustainable growth and inclusive economic development. The paper is based on an extensive review of literature that deals with monetary issues with the objective of building a case that the achievement of sustainable growth and inclusive economic development requires the right monetary system to be put in place which supports those objectives. The review of literature and theoretical reasoning assert that in order to achieve the stated economic objectives there is a need to develop and implement a different concept of money than the existing one. -

Volume 23 - Issue 2

IJCCR International Journal of Community Currency Research SUMMER 2019 VOLUME 23 - ISSUE 2 www.ijccr.net IJCCR 23 (Summer 2019) – ISSUE 2 Editorial 1 Georgina M. Gómez Transforming or reproducing an unequal economy? Solidarity and inequality 2-16 in a community currency Ester Barinaga Key Factors for the Durability of Community Currencies: An NPO Management 17-34 Perspective Jeremy September Sidechain and volatility of cryptocurrencies based on the blockchain 35-44 technology Olivier Hueber Social representations of money: contrast between citizens and local 45-62 complementary currency members Ariane Tichit INTERNATIONAL JOURNAL OF COMMUNITY CURRENCY RESEARCH 2017 VOLUME 23 (SUMMER) 1 International Journal of Community Currency Research VOLUME 23 (SUMMER) 1 EDITORIAL Georgina M. Gómez (*) Chief Editor International Institute of Social Studies of Erasmus University Rotterdam (*) [email protected] The International Journal of Community Currency Research was founded 23 years ago, when researchers on this topic found a hard time in getting published in other peer reviewed journals. In these two decades the academic publishing industry has exploded and most papers can be published internationally with a minimal peer-review scrutiny, for a fee. Moreover, complementary currency research is not perceived as extravagant as it used to be, so it has now become possible to get published in journals with excellent reputation. In that context, the IJCCR is still the first point of contact of practitioners and new researchers on this topic. It offers open access, free publication, and it is run on a voluntary basis by established scholars in the field. In any of the last five years, it has received about 25000 views.