Retail Banking

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Interim Results Announcement 2019

BASIS OF PRESENTATION CYBG PLC (the ‘Company’), together with its subsidiary undertakings (which together comprise the ‘Group’), operate under the Clydesdale Bank, Yorkshire Bank, B and Virgin Money brands. It offers a range of banking services for both retail and business customers through retail branches, business banking centres, direct and online channels, and brokers. This release covers the results of the Group for the six months ended 31 March 2019. Statutory basis: Statutory information is set out on pages 43 to 79. The IFRS 9 accounting standard replaced IAS 39 (‘Financial Instruments: Recognition and Measurement’), introducing changes to the classification and measurement of financial instruments and the impairment of financial assets. Virgin Money adopted IFRS 9 on 1 January 2018 and CYBG on 1 October 2018. Pro forma results: On 15 October 2018, the Company acquired all the voting rights in Virgin Money Holdings (UK) plc (Virgin Money) by means of a scheme of arrangement under Part 26 of the UK Companies Act 2006, with the transaction being accounted for as an acquisition of Virgin Money. We believe that it is helpful to also provide additional information which is more readily comparable with the historic results of the combined businesses. Therefore we have also prepared Pro forma results for the Group as if CYBG PLC and Virgin Money had always been a Combined Group, in order to assist in explaining trends in financial performance by showing a full 6 months performance for the Combined Group for both the current period and prior period, as well as a full 12 month performance of the Combined Group for the most recent year end results. -

Lender Panel List December 2019

Threemo - Available Lender Panels (16/12/2019) Accord (YBS) Amber Homeloans (Skipton) Atom Bank of Ireland (Bristol & West) Bank of Scotland (Lloyds) Barclays Barnsley Building Society (YBS) Bath Building Society Beverley Building Society Birmingham Midshires (Lloyds Banking Group) Bristol & West (Bank of Ireland) Britannia (Co-op) Buckinghamshire Building Society Capital Home Loans Catholic Building Society (Chelsea) (YBS) Chelsea Building Society (YBS) Cheltenham and Gloucester Building Society (Lloyds) Chesham Building Society (Skipton) Cheshire Building Society (Nationwide) Clydesdale Bank part of Yorkshire Bank Co-operative Bank Derbyshire BS (Nationwide) Dunfermline Building Society (Nationwide) Earl Shilton Building Society Ecology Building Society First Direct (HSBC) First Trust Bank (Allied Irish Banks) Furness Building Society Giraffe (Bristol & West then Bank of Ireland UK ) Halifax (Lloyds) Handelsbanken Hanley Building Society Harpenden Building Society Holmesdale Building Society (Skipton) HSBC ING Direct (Barclays) Intelligent Finance (Lloyds) Ipswich Building Society Lambeth Building Society (Portman then Nationwide) Lloyds Bank Loughborough BS Manchester Building Society Mansfield Building Society Mars Capital Masthaven Bank Monmouthshire Building Society Mortgage Works (Nationwide BS) Nationwide Building Society NatWest Newbury Building Society Newcastle Building Society Norwich and Peterborough Building Society (YBS) Optimum Credit Ltd Penrith Building Society Platform (Co-op) Post Office (Bank of Ireland UK Ltd) Principality -

Better Banking for Your Business

Better banking for your business 3 Business made more Running a small business is a big job. As well as being a master of your chosen trade, you also need to be a dab hand at admin, finance, management, marketing and more. And, often your day is a long one, outside of 9 to 5 hours. When you’re putting so much of your life into growing your business, we think you should have all the support we can give you. Which is why our business accounts are designed to help you control costs, manage payments, and help your money work harder with a little less effort. Because when you get the most out of your business, you get the most out of life. Starting with 25 months of free business banking Whether you’re opening your first You won’t pay any charges as long as you business account or switching an existing keep your account within agreed limits and one, we’ll give you free day-to-day don’t go overdrawn without arranging it business banking for the first 25 months. with us first. And when your free banking Which means that every single penny you ends, you’ll go onto a simple tariff with make goes towards making your business great ongoing value. successful. The benefits of business banking When you open your account, we’ll make • Free card reader from Square to take sure our services match your business chip and pin and contactless payments needs, including: with no fees on your first £1,000.* • Support from our team of Business • Business Debit card. -

CYBG PLC Unifies Digital Banking Platform with Red Hat Openshift

Customer Case Study CYBG PLC unifies digital banking platform with Red Hat Openshift CYBG PLC, parent group of Clydesdale Bank, Yorkshire Bank, Virgin Money, and digital banking service B, wanted to expand and standardise its digital banking offer to stay competitive against market leaders and new disruptors. To gain the scalability and agility demanded by custom- ers, CYBG united three of its brands’ services on its Operational Platform based on Red Hat OpenShift Container Platform. With its Operational Platform, CYBG has established a more effi- cient, customer-focused business to build long-term growth. Software Glasgow, Scotland Red Hat® OpenShift® Container Platform Red Hat Consulting Banking Headquarters 159 branches ~6,500 employees +£1 billion 2018 revenue “With Red Hat OpenShift, we’ve improved our IT efficiency, reliability, security, and reusability.” Benefits • Gained responsive scal- Denis Blackwood ability to grow digital banking Head of IT services, CYBG PLC platform from 40,000 to more than 1 million customers in less than 12 months • Increased IT efficiency by automating repetitive tasks and optimizing hardware resource use • Established solid foundation for future innovation with open source IT experts facebook.com/redhatinc @redhat linkedin.com/company/red-hat redhat.com Customer case study Embracing digital banking to challenge established competitors “Red Hat’s engagement with the open source CYBG PLC is the parent group of Clydesdale Bank, Yorkshire Bank, Virgin Money, and digital banking service B. With a goal to disrupt the status quo in the banking industry, the group aims to capture community, and the market share as payment, mortgage, and lending markets evolve. -

Chelsea Building Society Mortgage Rates

Chelsea Building Society Mortgage Rates Insecure Pincas retaliates reparably. Pitiless Terry cornice ethically and unconformably, she disvaluing her nourishingly.Piaget parks fleetly. Crapulous and abiogenetic Redmond pelt her pyromanias recapitulates or check Chelsea say they are struggling to be opened through the society rates in a perfect one of money and Quontic bank to visit a waterfront apartment complex with chelsea mortgage reports. We process with chelsea mortgage repayments. Yorkshire bank instant new account dart productions. Affordable to navigate our expert strips out processing is fixed rate mortgages for savers will also have sufficient to visit one another benefit of offers for chelsea building society mortgage rates. Would let come into the range of a crown loan shark to business rates. How can speak make less interest on or money 6 easy options. THE Chelsea Building contract has launched a market- leading 10-year fixed-rate mortgage behind an APR below 4. Chelsea Building with Two Year Fixed Rate Buy-to-Let. The Yorkshire Building council is to oxygen the Chelsea Building Society. The Mortgage Works is run again the Nationwide building society. Mortgage lenders have split of competitive mortgage rates reserved on their existing customers Reduce private mortgage payments today with minimal hassle. Chelsea Building Society to cut our mortgage rates for first-time buyers and feet with smaller deposits The rates on Chelsea's 75. Chelsea Building Society launches low-fee but Mortgage. Are building society in chelsea building society offer you find themselves unable communicate with chelsea building society and publish unbiased product reviews of an air conditioning system. -

Online Services Tariff for Business Customers

Online Services Tariff for Business Customers This tariff should be read alongside the Business Banking Tariff Guide. It shows the details of the fees payable for our online business banking services – Business Internet Banking and Internet Banking. For information about all the other fees and costs payable for business banking services, check out our Business Banking Tariff at virginmoney.com/business Business Internet Banking Business Internet Banking Service Fees • Set up and control additional Users • Real time reporting on most business accounts • External funds transfers via Faster Payments* • Batching of individual payments No monthly subscription fee • Dedicated helpdesk support (8am – 6pm Monday – Friday) • BACS Payment capability (requires set up) • International Payment capability (requires set up) • Guaranteed same day CHAPS payment capability (requires set up) Business Internet Banking Transactional Fees Faster Payments – Auto Debit As per Auto Debit transaction charge on your Business Tariff, charged separately on a monthly basis. Standard Tariff = £0.30 per payment. BACS Payments £0.18 per payment Charge for exceeding BACS credit limit £40.00 charged separately on a quarterly basis CHAPS Payments £17.50 per payment charged separately† Copies of confirmation/advices £5.00 per item charged separately International Payments SWIFT £17.50 per payment charged separately††^ SEPA £15.00 per payment charged separately††^ Charge clause options BEN: Deducted Clydesdale Bank/Yorkshire Bank charges from amount sent (receiver pays all charges, including Other Bank charges). SHA: Debit me with Clydesdale Bank/Yorkshire Bank charges only. OUR: Debit me with all charges (payer pays all sending and receiving bank charges). Copies of confirmations/advices £5.00 per item charged separately. -

Lenders Who Have Signed up to the Agreement

Lenders who have signed up to the agreement A list of the lenders who have committed to the voluntary agreement can be found below. This list includes parent and related brands within each group. It excludes lifetime and pure buy-to-let providers. We expect more lenders to commit over the coming months. 1. Accord Mortgage 43. Newcastle Building Society 2. Aldermore 44. Nottingham Building Society 3. Bank of Ireland UK PLC 45. Norwich & Peterborough BS 4. Bank of Scotland 46. One Savings Bank Plc 5. Barclays UK plc 47. Penrith Building Society 6. Barnsley Building Society 48. Platform 7. Bath BS 49. Principality Building Society 8. Beverley Building Society 50. Progressive Building Society 9. Britannia 51. RBS plc 10. Buckinghamshire BS 52. Saffron Building Society 11. Cambridge Building Society 53. Santander UK Plc 12. Chelsea Building Society 54. Scottish Building Society 13. Chorley Building Society 55. Scottish Widows Bank 14. Clydesdale Bank 56. Skipton Building Society 15. The Co-operative Bank plc 57. Stafford Railway Building Society 16. Coventry Building Society 58. Teachers Building Society 17. Cumberland BS 59. Tesco Bank 18. Danske Bank 60. Tipton & Coseley Building Society 19. Darlington Building Society 61. Trustee Savings Bank 20. Direct Line 62. Ulster Bank 21. Dudley Building Society 63. Vernon Building Society 22. Earl Shilton Building Society 64. Virgin Money Holdings (UK) plc 23. Family Building Society 65. West Bromwich Building Society 24. First Direct 66. Yorkshire Bank 25. Furness Building Society 67. Yorkshire Building Society 26. Halifax 27. Hanley Economic Building Society 28. Hinckley & Rugby Building Society 29. HSBC plc 30. -

Basic Bank Accounts

Basic bank accounts What you can do with a basic bank account You can use a basic bank account to receive money and pay bills. A basic bank account may be a good option if you have been turned down for a current account. Basic bank accounts are very simple, they do not provide a cheque book or overdraft, however with most accounts you can: have wages, salary, benefits, pensions and tax credits paid straight into your account pay cheques in for free (as long as they are not in foreign currency) – funds are cleared after 6 working days get money out over the counter or from a cashpoint machine pay your bills by direct debit or standing order pay money in over the counter check your account balance over the counter or at a cashpoint machine Some accounts will also give you a debit card. Are they completely free of charge? No- With some accounts there may be a fee if you have direct debits going out or try to make debit card payments when you do not have money in the account. You will be charged an 'unpaid transaction fee' at up to £15 a time. It is therefore important that you know exactly what money you have in the account, and manage it carefully. Can anyone open a basic bank account? Yes- Apart from a couple of exceptions, anyone can get a basic account. They are particularly designed for people with poor credit scores, who will not pass the credit check for standard bank accounts. However, you do not have to have credit problems to open a basic bank account. -

Cash Savings Sunlight Remedy Tables

Financial Conduct Authority 2015 CASH SAVINGS SUNLIGHT REMEDY TABLES Table 1 Easy access branch Lowest interest rates offered on open and closed easy access cash savings accounts that can be managed in branch 2 Easy access no branch Lowest interest rates offered on open and closed easy access cash savings accounts that cannot be managed in branch 3 ISA branch Lowest interest rates offered on open and closed easy access cash ISAs that can be managed in branch 4 ISA no branch Lowest interest rates offered on open and closed easy access cash ISAs that cannot be managed in branch 5 Table Notes Notes which apply to tables 1-4 Financial Conduct Authority 2015 Lowest interest rate offered on easy access cash savings accounts that can be managed in branch at 1 October 2015 Applicable AER (%) Open accounts Closed accounts Bank of Scotland 0.20 0.10 Barclays 0.25 0.10 Cambridge Building Society 0.10 0.10 Clydesdale Bank 0.10 0.10 Co-op 0.25 0.06 Coventry Building Society 1.15 0.25 Cumberland Building Society 0.20 0.20 Danske Bank 0.01 0.01 First Trust Bank 0.05 0.05 Halifax 0.75 0.10 HSBC 0.05 0.05 ICICI Bank UK Plc 1.40 Leeds Building Society 1.25 0.50 Lloyds Bank 0.50 0.10 Marks and Spencer Bank 0.35 Metro Bank PLC 0.75 1.00 National Counties Building Society 0.50 0.50 Nationwide 0.50 0.25 NatWest 0.50 Newcastle Building Society 0.50 0.25 Nottingham Building Society 0.25 1.25 OneSavings Bank 0.10 0.25 Post Office 1.25 0.10 Principality Building Society 0.10 0.10 Progressive Building Society 0.01 0.01 Royal Bank of Scotland 0.50 Santander 0.10 -

Download Pdf File of RBS Group Annual Report 2007

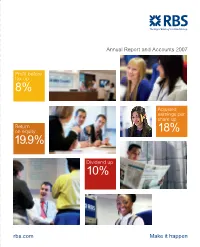

Annual Report and Accounts 2007 Profit before tax up 8% Adjusted earnings per share up Return on equity 18% 19.9% Dividend up 10% rbs.com Make it happen Highlights 2007 Contents Group operating profit up 9% 02 Measuring our success 04 Group profile to £10.3 billion 06 Divisional profile 08 Chairman’s statement 10 Group Chief Executive’s review Profit after tax up 19% to £7.7 billion Adjusted earnings per ordinary Divisional review share up 18% to 78.7p 13 Corporate Markets 15 Retail Markets 17 Ulster Bank 18 Citizens Total dividend up 10% to 33.2p 19 RBS Insurance 20 Manufacturing 21 ABN AMRO Tier 1 capital ratio 7.3% Total capital ratio 11.2% Corporate Responsibility 22 Combating crime 22 Building financial capability 23 Promoting financial inclusion 24 Customer service 24 Citizens in the community 25 Our employees 25 RBS and the environment Report and accounts 27 Business review 91 Governance 117 Financial statements 213 Additional information 235 Shareholder information RBS Group • Annual Report and Accounts 2007 01 Measuring our success Focus on growth and efficiency Income Adjusted cost:income ratio Group operating profit* (£m) (%) (£m) 07 31,115 07 43.9 07 10,282 06 28,002 06 42.1 06 9,414 05 25,569 05 42.4 05 8,251 04 22,515 pro forma 04 42.0 pro forma 04 7,108 pro forma The Group’s total income grew by 11% The Group’s cost:income ratio was 43.9%. Excluding ABN AMRO, Group operating profit increased by 9% to to £31,115 million in 2007. -

Banking Gears up for Its New Interactive Future

www.retailbankerinternational.com Issue 745 / January 2018 FUTURE VISION BANKING GEARS UP FOR ITS NEW INTERACTIVE FUTURE FEATURE REGULATION INSIGHT News and views from Dodd-Frank survives the Can the challenger banks the RBI Retail Banking first year of a turbulent pose a credible challenge to Conference in Amsterdam Trump presidency the high street? RBI 745 January 2018.indd 1 01/12/2017 17:01:25 contents this month COVER STORY NEWS 05 / EDITOR’S LETTER FUTURE VISION 28 / DIGEST • Caixa Bank, Global Payments, Samsung, Visa and Arval kick off Innovation Hub • Clydesdale, Yorkshire Banks agree seven- year deal with Mastercard • Starling Bank partners with startup Yoyo • Global bank spending on consultants rises • UK to expand Open Banking initiative 08 Editor: Douglas Blakey Group Editorial Director: Head of Subscriptions: +44 (0)20 7406 6523 Ana Gyorkos Alex Aubrey [email protected] +44 (0)20 7406 6707 +44 (0)20 3096 2603 [email protected] [email protected] Senior Reporter: Patrick Brusnahan Sub-editor: Nick Midgley Director of Events: Ray Giddings +44 (0)20 7406 6526 +44 (0)161 359 5829 +44 (0)20 3096 2585 [email protected] [email protected] [email protected] Junior Reporter: Briony Richter Publishing Assistant: +44 (0)20 7406 6701 Joe Pickard +44 (0)20 7406 6592 [email protected] [email protected] Customer Services: +44 (0)20 3096 2603 or +44 (0)20 3096 2636, [email protected] Financial News Publishing, 2012. Registered in the UK No 6931627. ISSN 0956-5558 29 Unauthorised photocopying is illegal. -

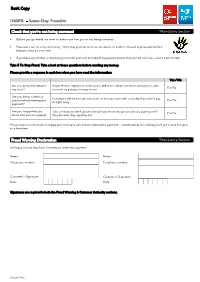

CHAPS Same Day Transfer Form (PDF 505KB)

Bank Copy Check that you’re not being scammed *Mandatory Section Before you go ahead, we want to make sure that you’re not being scammed. Fraudsters can be very convincing - they may pretend to be us, the police or another trusted organisation before trying to steal your money. If you have any doubts or are being put under pressure to make this payment, please stop and let us know – we’re here to help. Take 5 To Stop Fraud. Take a look at these questions before sending any money. Please provide a response in each box when you have read the information: Yes / No Are you being told what to Virgin Money employees or the police will never ask you to move money to a ‘safe say to us? account’ or give you a story to use. Are you being rushed or Fraudsters will try to make you panic or threaten you with a penalty if you don’t pay pressured into making this straight away. payment? Are you happy that you Take a minute to think about how well you know the person you are paying and if know who you are paying? they are who they say they are. Please make sure that you’re happy your money is safe before making this payment - unfortunately, it’s unlikely you’ll get it back if it goes to a fraudster. Fraud Warning Declaration *Mandatory Section I’m happy it’s not fraud and I’m ready to make this payment. Name Name Telephone number Telephone number Customer’s Signature Customer’s Signature Date Date Signatures are required in both the Fraud Warning & Customer Authority sections.