Report Contains Important Disclosures, Analyst Certifications, Legal Entity Disclosure and the Status of Non-Us Analysts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

GPU Developments 2018

GPU Developments 2018 2018 GPU Developments 2018 © Copyright Jon Peddie Research 2019. All rights reserved. Reproduction in whole or in part is prohibited without written permission from Jon Peddie Research. This report is the property of Jon Peddie Research (JPR) and made available to a restricted number of clients only upon these terms and conditions. Agreement not to copy or disclose. This report and all future reports or other materials provided by JPR pursuant to this subscription (collectively, “Reports”) are protected by: (i) federal copyright, pursuant to the Copyright Act of 1976; and (ii) the nondisclosure provisions set forth immediately following. License, exclusive use, and agreement not to disclose. Reports are the trade secret property exclusively of JPR and are made available to a restricted number of clients, for their exclusive use and only upon the following terms and conditions. JPR grants site-wide license to read and utilize the information in the Reports, exclusively to the initial subscriber to the Reports, its subsidiaries, divisions, and employees (collectively, “Subscriber”). The Reports shall, at all times, be treated by Subscriber as proprietary and confidential documents, for internal use only. Subscriber agrees that it will not reproduce for or share any of the material in the Reports (“Material”) with any entity or individual other than Subscriber (“Shared Third Party”) (collectively, “Share” or “Sharing”), without the advance written permission of JPR. Subscriber shall be liable for any breach of this agreement and shall be subject to cancellation of its subscription to Reports. Without limiting this liability, Subscriber shall be liable for any damages suffered by JPR as a result of any Sharing of any Material, without advance written permission of JPR. -

China Equity Strategy

June 5, 2019 09:40 AM GMT MORGAN STANLEY ASIA LIMITED+ China Equity Strategy | Asia Pacific Jonathan F Garner EQUITY STRATEGIST [email protected] +852 2848-7288 The Rubio "Equitable Act" - Our Laura Wang EQUITY STRATEGIST [email protected] +852 2848-6853 First Thoughts Corey Ng, CFA EQUITY STRATEGIST [email protected] +852 2848-5523 Fran Chen, CFA A new bill sponsored by US Senator Marco Rubio has the EQUITY STRATEGIST potential to cause significant change in the listing domains of [email protected] +852 2848-7135 Chinese firms. After the market close in the US yesterday 4th June the Wall Street Journal published an Op-Ed by US Senator Marco Rubio in which he announced that he intends to sponsor the “Equitable Act” – an acronym for Ensuring Quality Information and Transparency for Abroad-Based Listings on our Exchanges. At this time the text of the bill has not been published and we are seeking additional information about its contents and likelihood of passing. However, our early reaction is that this has the potential to cause significant changes in the domain for listings of Chinese firms going forward with the potential for de- listing of Chinese firms on US exchanges and re-listing elsewhere (most likely Hong Kong). More generally we see this development as part of an increased escalation of tensions between China and the US on multiple fronts which should cap the valuation multiple for China equities, in particular in the offshore index constituents and US-listed parts of the universe. We provide a list of the potentially impacted China / HK names with either primary or secondary listings on Amex, NYSE or Nasdaq. -

Leading Chinese Cross-Border Brands – the Top 50

Leading Chinese cross-border brands The Top 50 kpmg.com/cn © 2018 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Contents Foreword: KPMG & Facebook 2 Executive summary 4 Methodology 6 Top 50 Chinese global brands 8 Survey commentary 10 Chinese brands going global – business opportunities for SMEs 32 • Thought leader: Yan Zhu, Head, Institute of Internet Industry, Tsinghua University 34 Going global and ensuring market diversification 36 Customer centricity 44 Thought leaders 58 • Kaitian Zeng, Co-founder, 37 Interactive Entertainment 58 • Yue Leng, General Manager, Tmall Global, Alibaba Group 59 • Scott Thiel, Partner, DLA Piper 60 • Gu He, Vice President, Shenzhen Globalegrow E-Commerce Co., Ltd. 62 • Chibo Tang, Managing Director, Gobi Partners 63 • Ethan Wang, Vice President, NetEase 64 • Scott Kronick, Chief Executive, Public Relations & Influence, Asia, Ogilvy 65 • Alen Wu, Vice President, OPPO Mobile; Head of Business, Overseas Markets 66 • Beehong Hong, General Manager, Brand Management Centre, TRANSSION Holdings 67 Acknowledgements 68 About us 69 Contact us 70 Leading Chinese cross-border brands: The Top 50 1 © 2018 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. © 2018 KPMG, a Hong Kong partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Foreword Global trade has long been a hallmark of Chinese business culture. -

QI Wireless Compatible Device List Apple Asus Blackberry CASIO

QI Wireless Compatible Device List Apple • iPhone 8 • iPhone 8 Plus • iPhone X • iPhone Xs • iPhone Xs Max • iPhone Xr Asus • Asus PadFone S BlackBerry • BlackBerry Passport • BlackBerry PRIV • BlackBerry Z30 CASIO • CASIO G'z One Commando Caterpillar • Cat S50 • Cat S50C DeWalt • Dewalt MD501 • Dewalt MIL810G Energy Sistem • Energy Phone Pro Qi Fujitsu • Fujitsu Arrows F-09D • Fujitsu Arrows Kiss F-03D • Fujitsu Arrows Kiss F-03E • Fujitsu Arrows X F-10D Google • Google Nexus 4 • Google Nexus 5 • Google Nexus 6 • Google Pixel 3 • Google Pixel 3 XL HP • HP Elite X3 HTC • HTC Droid DNA • HTC Windows Phone 8X Huawei • Huawei Mate20 Pro • Huawei Mate RS Porsche Design • Huawei P30 Pro Kyocera • Kyocera Brigadier • Kyocera DuraForce • Kyocera Hydro Elite • Kyocera Torque G02 • Kyocera Torque KC-S701 • Kyocera Urbano L01 • Kyocera Urbano L03 LG • LG G2 • LG G3 • LG G6 ¹ • LG G6 Plus ¹ • LG G7 • LG G7 ThinQ • LG Lucid 2 • LG Lucid 3 • LG Optimus F5 • LG Optimus G Pro • LG Optimus It L-05E • LG Spectrum 2 • LG Vu 2 • LG Vu 3 • LG V30 • LG V30 Plus • LG V40 ThinQ M.T.T. • M.T.T. Master 4G Meizu • Meizu Zero Microsoft • Microsoft Lumia 950 • Microsoft Lumia 950 Dual Sim • Microsoft Lumia 950 XL • Microsoft Lumia 950 XL Dual Sim Mlais • Mlais MX69W Motorola • Motorola Droid Maxx • Motorola Droid Mini • Motorola Droid Turbo • Motorola Droid Turbo 2 • Motorola Moto Maxx • Motorola Moto X Force mPhone • mPhone 8 NEC • NEC Medias PP N-01D • NEC Medias X N-04E Noa • Noa F10 Pro Nokia • Nokia Lumia 1520 • Nokia Lumia 735 • Nokia Lumia 830 • Nokia Lumia -

Site List Fashion, Food & Home

SITE LIST FASHION, FOOD & HOME MARCH 2020 The John Lewis Partnership’s relationships with its suppliers are based on honesty, fairness, courtesy and promptness. In return, the Partnership expects its suppliers to obey the law and to respond the wellbeing of their employees, local communities and the environment. The sites featured in the list below are John Lewis & Partners suppliers’ production sites which represent 100% of John Lewis & Partners’ branded product. Region Number of Sites Africa 23 Americas 14 Arab States 1 Asia Pacific 1195 Europe & Central Asia 526 United Kingdom 548 Total 2307 Active Union or Product No. of Female Male Site Name Address Country Worker Category Workers Worker % Worker % Committee Afa 3 Calzatura Sh.P.K. Velabisht, Beral, Albania Fashion 221 73% 27% Yes Weingut Rabl Weraingraben 10, Langenlois Austria Food 20 25% 75% No Weingut Markus Hurber Cmbh & Cokg Rechersdorf An Der Traisen, Weinriedenweg 13 Austria Food * No Akh Fashions 133-134 Hemayetpur, Savar, Dhaka, Dhaka 1340 Bangladesh Fashion 1222 65% 35% Yes Aman Graphics & Designs Ltd Najim Nagar, Dhaka, Savar Bangladesh Fashion 3804 60% 40% Yes Aman Knittings Ltd Kulashur, Hemayetpur, Dhaka, Savar Bangladesh Fashion 1715 46% 54% Yes Bando Eco Apparels Ld. Plot #188/2, Block G-A, Chanpur, Amin Bazar, Savar, Dhaka, Dhaka, Dhaka Bangladesh Fashion 1200 53% 47% Yes Basic Shirts Ltd Plot # 341, Majukhan, Po: Harbaid, Ps Gazipur Sadar, Gazipur Bangladesh Fashion 2410 70% 30% Yes Direct Sports & Leisurewear (Bd) Limited Plot No. S.A. 07, 08, R.S. 11, 12, 13 Karamtola Pubail Gazipur, Dhaka, Bangladesh Fashion 374 65% 35% No Energypac Fashion Ltd. -

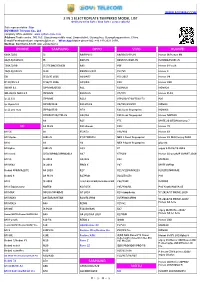

2 in 1 Electroplate Tempered Model List Iphone Samsung

WWW.BOYIMAX.COM 2 IN 1 ELECTROPLATE TEMPERED MODEL LIST Ordinary white light / blue light / aurora colorful Sale representative :Star BOYIMAX® Telecom Co., Ltd company office website: www.i-phonecase.com Address:Trade centra , NO.163, Qiaozhong middle road, Liwan distirct, Guangzhou, Guangdong province, China. E-mail/Facebook/skype: [email protected] ,WhatsApp/Mobile phone NO.:+86 189 2621 0199, WeChat: BOYIMAX-STAR ,QQ: 2233234410 IPHONE SAMSUNG OPPO VIVO HUAWEI 6G(4.7)/6S J2 R9/FIPLUS X9/X9S/V5PLUS Honor 9I/Honor 9N 6G(5.5)/6SPLUS J5 R9PLUS X9SPLUS/X9PLUS P20PRO/P20PLUS 7G(4.7)/8G J7/J7CORE/J7NEO R9S Y66 Honor 9 Youth 7G(5.5)/8PLUS J120 R9SPLUS/F3P Y67/V5 Honor 9 5G J510/J5 2016 A39/A57 Y53 2017 Honor V9 IP 8X/XS 5.8 J710/J7 2016 A59/FIS X20 Honor V10 9G/XR 6.1 J2PRIME/G530 R11 X20PLUS NOVA2S 9PLUS/XS MAX 6.5 J5PRIME R11PLUS V7/Y75 Honor PLAY ip 11 6.1 J7PRIME R11S V7PLUS/Y79/Y75S/Y73 P20 ip 11pro 5.8 J3PRO/J330 R11SPLUS V9/Y85/Z1\Z3X NOVA3 ip 11 pro max J5PRO/J530 A79 X21 back fingerprint NOVA3I J7PRO/J730/J7PLUS A83/A1 X21 front fingerprint Honor NOTE10 A8 R15 Y71 MATE 20 LITE/Maimang 7 MI A8 PLUS R15 dream X21I Honor 7X MI 5X S8 F5/A73 Y83/Y81 Honor 8X MI 5Splus S8PLUS F7/F7YOUTH NEX S front fingerprint Honor 8X MAX/enjoy MAX MI 6 S9 A3 NEX A back fingerprint play 8C MI 6plus S9PLUS A33 X7 enjoy 9 PLUS/Y9 2019 MI note3 J250/J2PRO/J2PRO2018 A37 X7PLUS Honor 10 youth/P SMART 2019 MI 5S J4 2018 A5/A3S X23 MATE20 MI MIX2 J6 2018 FIND X Y97 MATE20PRO Redmi 6PRO/A2LITE A6 2018 R17 V11/V11PRO/X21S P20LITE/NOVA3E Redmi 6 A6 PLUS R17PRO V11I/Z3I/Z3 -

Electronic 3D Models Catalogue (On July 26, 2019)

Electronic 3D models Catalogue (on July 26, 2019) Acer 001 Acer Iconia Tab A510 002 Acer Liquid Z5 003 Acer Liquid S2 Red 004 Acer Liquid S2 Black 005 Acer Iconia Tab A3 White 006 Acer Iconia Tab A1-810 White 007 Acer Iconia W4 008 Acer Liquid E3 Black 009 Acer Liquid E3 Silver 010 Acer Iconia B1-720 Iron Gray 011 Acer Iconia B1-720 Red 012 Acer Iconia B1-720 White 013 Acer Liquid Z3 Rock Black 014 Acer Liquid Z3 Classic White 015 Acer Iconia One 7 B1-730 Black 016 Acer Iconia One 7 B1-730 Red 017 Acer Iconia One 7 B1-730 Yellow 018 Acer Iconia One 7 B1-730 Green 019 Acer Iconia One 7 B1-730 Pink 020 Acer Iconia One 7 B1-730 Orange 021 Acer Iconia One 7 B1-730 Purple 022 Acer Iconia One 7 B1-730 White 023 Acer Iconia One 7 B1-730 Blue 024 Acer Iconia One 7 B1-730 Cyan 025 Acer Aspire Switch 10 026 Acer Iconia Tab A1-810 Red 027 Acer Iconia Tab A1-810 Black 028 Acer Iconia A1-830 White 029 Acer Liquid Z4 White 030 Acer Liquid Z4 Black 031 Acer Liquid Z200 Essential White 032 Acer Liquid Z200 Titanium Black 033 Acer Liquid Z200 Fragrant Pink 034 Acer Liquid Z200 Sky Blue 035 Acer Liquid Z200 Sunshine Yellow 036 Acer Liquid Jade Black 037 Acer Liquid Jade Green 038 Acer Liquid Jade White 039 Acer Liquid Z500 Sandy Silver 040 Acer Liquid Z500 Aquamarine Green 041 Acer Liquid Z500 Titanium Black 042 Acer Iconia Tab 7 (A1-713) 043 Acer Iconia Tab 7 (A1-713HD) 044 Acer Liquid E700 Burgundy Red 045 Acer Liquid E700 Titan Black 046 Acer Iconia Tab 8 047 Acer Liquid X1 Graphite Black 048 Acer Liquid X1 Wine Red 049 Acer Iconia Tab 8 W 050 Acer -

Sensors and Data Encryption, Two Aspects of Electronics That Used to Be Two Worlds Apart and That Are Now Often Tightly Integrated, One Relying on the Other

www.eenewseurope.com January 2019 electronics europe News News e-skin beats human touch Swedish startup beats e-Ink on low-power Special Focus: Power Sources european business press November 2011 Electronic Engineering Times Europe1 181231_8-3_Mill_EENE_EU_Snipe.indd 1 12/14/18 3:59 PM 181231_QualR_EENE_EU.indd 1 12/14/18 3:53 PM CONTENTS JANUARY 2019 Dear readers, www.eenewseurope.com January 2019 The Consumer Electronics Show has just closed its doors in Las Vegas, yet the show has opened the mind of many designers, some returning home with new electronics europe News News ideas and possibly new companies to be founded. All the electronic devices unveiled at CES share in common the need for a cheap power source and a lot of research goes into making power sources more sus- tainable. While lithium-ion batteries are commercially mature, their long-term viability is often questioned and new battery chemistries are being investigated for their simpler material sourcing, lower cost and sometime increased energy density. Energy harvesting is another feature that is more and more often inte- e-skin beats human touch grated into wearables but also at grid-level. Our Power Sources feature will give you a market insight and reviews some of the latest findings. Other topics covered in our January edition are Sensors and Data Encryption, two aspects of electronics that used to be two worlds apart and that are now often tightly integrated, one relying on the other. Swedish startup beats e-Ink on low-power With this first edition of 2019, let me wish you all an excellent year and plenty Special Focus: Power Sources of new business opportunities, whether you are designing the future for a european business press startup or working for a well-established company. -

Presentación De Powerpoint

Modelos compatibles de Imóvil No. Marca Modelo Teléfono Versión del sistema operativo 1 360 1501_M02 1501_M02 Android 5.1 2 100+ 100B 100B Android 4.1.2 3 Acer Iconia Tab A500 Android 4.0.3 4 ALPS (Golden Master) MR6012H1C2W1 MR6012H1C2W1 Android 4.2.2 5 ALPS (Golden Master) PMID705GTV PMID705GTV Android 4.2.2 6 Amazon Fire HD 6 Fire HD 6 Fire OS 4.5.2 / Android 4.4.3 7 Amazon Fire Phone 32GB Fire Phone 32GB Fire OS 3.6.8 / Android 4.2.2 8 Amoi A862W A862W Android 4.1.2 9 amzn KFFOWI KFFOWI Android 5.1.1 10 Apple iPad 2 (2nd generation) MC979ZP iOS 7.1 11 Apple iPad 4 MD513ZP/A iOS 7.1 12 Apple iPad 4 MD513ZP/A iOS 8.0 13 Apple iPad Air MD785ZP/A iOS 7.1 14 Apple iPad Air 2 MGLW2J/A iOS 8.1 15 Apple iPad Mini MD531ZP iOS 7.1 16 Apple iPad Mini 2 FE276ZP/A iOS 8.1 17 Apple iPad Mini 3 MGNV2J/A iOS 8.1 18 Apple iPhone 3Gs MC132ZP iOS 6.1.3 19 Apple iPhone 4 MC676LL iOS 7.1.2 20 Apple iPhone 4 MC603ZP iOS 7.1.2 21 Apple iPhone 4 MC604ZP iOS 5.1.1 22 Apple iPhone 4s MD245ZP iOS 8.1 23 Apple iPhone 4s MD245ZP iOS 8.4.1 24 Apple iPhone 4s MD245ZP iOS 6.1.2 25 Apple iPhone 5 MD297ZP iOS 6.0 26 Apple iPhone 5 MD298ZP/A iOS 8.1 27 Apple iPhone 5 MD298ZP/A iOS 7.1.1 28 Apple iPhone 5c MF321ZP/A iOS 7.1.2 29 Apple iPhone 5c MF321ZP/A iOS 8.1 30 Apple iPhone 5s MF353ZP/A iOS 8.0 31 Apple iPhone 5s MF353ZP/A iOS 8.4.1 32 Apple iPhone 5s MF352ZP/A iOS 7.1.1 33 Apple iPhone 6 MG492ZP/A iOS 8.1 34 Apple iPhone 6 MG492ZP/A iOS 9.1 35 Apple iPhone 6 Plus MGA92ZP/A iOS 9.0 36 Apple iPhone 6 Plus MGAK2ZP/A iOS 8.0.2 37 Apple iPhone 6 Plus MGAK2ZP/A iOS 8.1 -

Hardware-Assisted Rootkits: Abusing Performance Counters on the ARM and X86 Architectures

Hardware-Assisted Rootkits: Abusing Performance Counters on the ARM and x86 Architectures Matt Spisak Endgame, Inc. [email protected] Abstract the OS. With KPP in place, attackers are often forced to move malicious code to less privileged user-mode, to ele- In this paper, a novel hardware-assisted rootkit is intro- vate privileges enabling a hypervisor or TrustZone based duced, which leverages the performance monitoring unit rootkit, or to become more creative in their approach to (PMU) of a CPU. By configuring hardware performance achieving a kernel mode rootkit. counters to count specific architectural events, this re- Early advances in rootkit design focused on low-level search effort proves it is possible to transparently trap hooks to system calls and interrupts within the kernel. system calls and other interrupts driven entirely by the With the introduction of hardware virtualization exten- PMU. This offers an attacker the opportunity to redirect sions, hypervisor based rootkits became a popular area control flow to malicious code without requiring modifi- of study allowing malicious code to run underneath a cations to a kernel image. guest operating system [4, 5]. Another class of OS ag- The approach is demonstrated as a kernel-mode nostic rootkits also emerged that run in System Manage- rootkit on both the ARM and Intel x86-64 architectures ment Mode (SMM) on x86 [6] or within ARM Trust- that is capable of intercepting system calls while evad- Zone [7]. The latter two categories, which leverage vir- ing current kernel patch protection implementations such tualization extensions, SMM on x86, and security exten- as PatchGuard. -

HR Kompatibilitätsübersicht

Kompatibilitätsübersicht HR-imotion HR-imotion Kompatibilität/Compatibility 2017 / 03 Gerätetyp Telefon 22410001 23010201 22110001 23010001 23010101 22010401 22010501 22010301 22010201 22110101 22010701 22011101 22010101 22210101 22210001 23510101 23010501 23010601 23010701 23510320 22610001 23510420 Smartphone Acer Liquid Zest Plus Smartphone AEG Voxtel M250 Smartphone Alcatel A3 Smartphone Alcatel A3 XL Smartphone Alcatel A5 LED Smartphone Alcatel Idol 4S Smartphone Alcatel U5 Smartphone Allview X3 Soul Smartphone Apple iPhone Smartphone Apple iPhone 3G / 3GS Smartphone Apple iPhone 4 / 4S Smartphone Apple iPhone 5 / 5S Smartphone Apple iPhone 5C Smartphone Apple iPhone 6 / 6S Smartphone Apple iPhone 6 Plus / 6S Plus Smartphone Apple iPhone 7 Smartphone Apple iPhone 7 Plus Smartphone Apple iPhone SE Smartphone Archos 50 Saphir Smartphone Archos Diamond 2 Plus Smartphone Asus ZenFone 3 Smartphone Asus ZenFone 3 Deluxe Smartphone Asus ZenFone 3 Zoom Smartphone Asus ZenFone AR Smartphone BlackBerry Classic Smartphone Blackberry DTEK 50 Smartphone Blackberry KEYOne Smartphone BlackBerry Passport Smartphone BlackBerry Priv Smartphone BlackBerry Z30 Smartphone BQ Aquaris X5 Smartphone BQ Aquaris X5 Plus Smartphone CAT B15 Smartphone Cubot P11 Smartphone Cubot S500 Smartphone Elephone P8000 Smartphone Emporia Pure Smartphone Gigaset GS160 Smartphone Gigaset ME Smartphone Gigaset ME Pro Smartphone Gigaset ME Pure Smartphone Google Nexus 5 Smartphone Google Nexus 5X Smartphone Google Nexus 6 Smartphone Google Nexus 6P Smartphone Google Pixel -

![Arxiv:1910.06663V1 [Cs.PF] 15 Oct 2019](https://docslib.b-cdn.net/cover/5599/arxiv-1910-06663v1-cs-pf-15-oct-2019-1465599.webp)

Arxiv:1910.06663V1 [Cs.PF] 15 Oct 2019

AI Benchmark: All About Deep Learning on Smartphones in 2019 Andrey Ignatov Radu Timofte Andrei Kulik ETH Zurich ETH Zurich Google Research [email protected] [email protected] [email protected] Seungsoo Yang Ke Wang Felix Baum Max Wu Samsung, Inc. Huawei, Inc. Qualcomm, Inc. MediaTek, Inc. [email protected] [email protected] [email protected] [email protected] Lirong Xu Luc Van Gool∗ Unisoc, Inc. ETH Zurich [email protected] [email protected] Abstract compact models as they were running at best on devices with a single-core 600 MHz Arm CPU and 8-128 MB of The performance of mobile AI accelerators has been evolv- RAM. The situation changed after 2010, when mobile de- ing rapidly in the past two years, nearly doubling with each vices started to get multi-core processors, as well as power- new generation of SoCs. The current 4th generation of mo- ful GPUs, DSPs and NPUs, well suitable for machine and bile NPUs is already approaching the results of CUDA- deep learning tasks. At the same time, there was a fast de- compatible Nvidia graphics cards presented not long ago, velopment of the deep learning field, with numerous novel which together with the increased capabilities of mobile approaches and models that were achieving a fundamentally deep learning frameworks makes it possible to run com- new level of performance for many practical tasks, such as plex and deep AI models on mobile devices. In this pa- image classification, photo and speech processing, neural per, we evaluate the performance and compare the results of language understanding, etc.