W Estern Riverside Council of Governm Ents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Stations Monitored

Stations Monitored 10/01/2019 Format Call Letters Market Station Name Adult Contemporary WHBC-FM AKRON, OH MIX 94.1 Adult Contemporary WKDD-FM AKRON, OH 98.1 WKDD Adult Contemporary WRVE-FM ALBANY-SCHENECTADY-TROY, NY 99.5 THE RIVER Adult Contemporary WYJB-FM ALBANY-SCHENECTADY-TROY, NY B95.5 Adult Contemporary KDRF-FM ALBUQUERQUE, NM 103.3 eD FM Adult Contemporary KMGA-FM ALBUQUERQUE, NM 99.5 MAGIC FM Adult Contemporary KPEK-FM ALBUQUERQUE, NM 100.3 THE PEAK Adult Contemporary WLEV-FM ALLENTOWN-BETHLEHEM, PA 100.7 WLEV Adult Contemporary KMVN-FM ANCHORAGE, AK MOViN 105.7 Adult Contemporary KMXS-FM ANCHORAGE, AK MIX 103.1 Adult Contemporary WOXL-FS ASHEVILLE, NC MIX 96.5 Adult Contemporary WSB-FM ATLANTA, GA B98.5 Adult Contemporary WSTR-FM ATLANTA, GA STAR 94.1 Adult Contemporary WFPG-FM ATLANTIC CITY-CAPE MAY, NJ LITE ROCK 96.9 Adult Contemporary WSJO-FM ATLANTIC CITY-CAPE MAY, NJ SOJO 104.9 Adult Contemporary KAMX-FM AUSTIN, TX MIX 94.7 Adult Contemporary KBPA-FM AUSTIN, TX 103.5 BOB FM Adult Contemporary KKMJ-FM AUSTIN, TX MAJIC 95.5 Adult Contemporary WLIF-FM BALTIMORE, MD TODAY'S 101.9 Adult Contemporary WQSR-FM BALTIMORE, MD 102.7 JACK FM Adult Contemporary WWMX-FM BALTIMORE, MD MIX 106.5 Adult Contemporary KRVE-FM BATON ROUGE, LA 96.1 THE RIVER Adult Contemporary WMJY-FS BILOXI-GULFPORT-PASCAGOULA, MS MAGIC 93.7 Adult Contemporary WMJJ-FM BIRMINGHAM, AL MAGIC 96 Adult Contemporary KCIX-FM BOISE, ID MIX 106 Adult Contemporary KXLT-FM BOISE, ID LITE 107.9 Adult Contemporary WMJX-FM BOSTON, MA MAGIC 106.7 Adult Contemporary WWBX-FM -

The Southern California Radio Reference Guide 4/29/2020

The Southern California Radio Reference Guide 4/29/2020 Call letters Branding Dial position Ownership Nielsen Market Format Phone Website KATY 101.3fm The Mix 101.3 FM All Pro Broadcasting Riverside/San Bernardino Adult Contemporary (951) 506-1222 http://www.1013themix.com/ KHTI Hot 103.9 103.9 FM All Pro Broadcasting Riverside/San Bernardino Hot AC (909) 890-5904 http://www.x1039.com/ KKBB Groove 99-3 99.3 FM Alpha Media USA Bakersfield Rhythmic Oldies (661) 393-1900 https://www.groove993.com/ KLLY Energy 95.3 95.3 FM Alpha Media USA Bakersfield Hot AC (661) 393-1900 https://www.energy953.com/ KNZR 1560 & 97.7 FM KNZR 1560 AM Alpha Media USA Bakersfield News Talk (661) 393-1900 https://www.knzr.com/ KCLB 93.7 KCLB 93.7 FM Alphamedia Palm Springs Rock (760) 322-7890 https://www.937kclb.com/ KDES 98.5 The Bull 98.5 FM Alphamedia Palm Springs Country (760) 322-7891 https://www.985thebull.com/ KDGL The Eagle 106.9 106.9 FM Alphamedia Palm Springs Classic Rock (760) 322-7890 https://www.theeagle1069.com/ U-92.7 The Desert's KKUU 92.7 FM Alphamedia Palm Springs Dance CHR (760) 322-7890 https://www.u927.com/ Hottest Music KNWH / KNWQ / KNWZ K-News, The Voice of 1250 AM/1140 AM/970 Alphamedia Palm Springs Talk (760) 322-7890 https://www.knewsradio.com/ AM & FM The Valley AM/94.3 FM Mix 100.5 The Desert's KPSI FM 100.5 Alphamedia Palm Springs Hot AC (760) 322-7890 https://www.mix1005.fm/ Best Mix KCAL 96.7 K-CAL Rocks 96.7 FM Anaheim Broadcasting Corporation Riverside/San Bernardino Rock (909) 793-3554 https://www.kcalfm.com/ KOLA KOLA 99.9 99.9 FM Anaheim Broadcasting Corporation Riverside/San Bernardino Oldies (909) 793-3554 https://www.kolafm.com/ KCWR Real Country 107.1 FM Buck Owens Broadcasting Bakersfield Country (661) 326-1011 N/A KRJK 97.3 The Bull 97.3 FM Buck Owens Broadcasting Bakersfield Adult HIts (661) 326-1011 https://www.bull973.com/ KUZZ AM/FM (simulcast) KUZZ AM 55 ▪ FM 107.9 550 AM/107.9 FM Buck Owens Broadcasting Bakersfield Country (661) 326-1011 http://www.kuzzradio.com/ KWVE FM K-Wave 107.9 FM Calvary Chapel Church, Inc. -

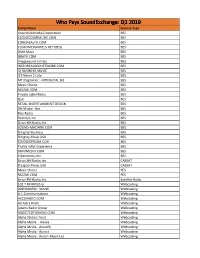

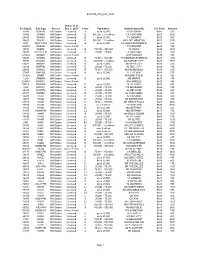

Licensee Count Q1 2019.Xlsx

Who Pays SoundExchange: Q1 2019 Entity Name License Type Aura Multimedia Corporation BES CLOUDCOVERMUSIC.COM BES COROHEALTH.COM BES CUSTOMCHANNELS.NET (BES) BES DMX Music BES GRAYV.COM BES Imagesound Limited BES INSTOREAUDIONETWORK.COM BES IO BUSINESS MUSIC BES It'S Never 2 Late BES MTI Digital Inc - MTIDIGITAL.BIZ BES Music Choice BES MUZAK.COM BES Private Label Radio BES Qsic BES RETAIL ENTERTAINMENT DESIGN BES Rfc Media - Bes BES Rise Radio BES Rockbot, Inc. BES Sirius XM Radio, Inc BES SOUND-MACHINE.COM BES Stingray Business BES Stingray Music USA BES STUDIOSTREAM.COM BES Thales Inflyt Experience BES UMIXMEDIA.COM BES Vibenomics, Inc. BES Sirius XM Radio, Inc CABSAT Stingray Music USA CABSAT Music Choice PES MUZAK.COM PES Sirius XM Radio, Inc Satellite Radio 102.7 FM KPGZ-lp Webcasting 999HANKFM - WANK Webcasting A-1 Communications Webcasting ACCURADIO.COM Webcasting Ad Astra Radio Webcasting Adams Radio Group Webcasting ADDICTEDTORADIO.COM Webcasting Aloha Station Trust Webcasting Alpha Media - Alaska Webcasting Alpha Media - Amarillo Webcasting Alpha Media - Aurora Webcasting Alpha Media - Austin-Albert Lea Webcasting Alpha Media - Bakersfield Webcasting Alpha Media - Biloxi - Gulfport, MS Webcasting Alpha Media - Brookings Webcasting Alpha Media - Cameron - Bethany Webcasting Alpha Media - Canton Webcasting Alpha Media - Columbia, SC Webcasting Alpha Media - Columbus Webcasting Alpha Media - Dayton, Oh Webcasting Alpha Media - East Texas Webcasting Alpha Media - Fairfield Webcasting Alpha Media - Far East Bay Webcasting Alpha Media -

Federal Communications Commission FCC 96-372 in Re Applications Of

Federal Communications Commission FCC 96-372 Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C 20554 In re Applications of ) KOLA, INC., ) File No. BALH-940513EC Assignor, ) and ) RAY M STANFIELD, RECEIVER, ) Assignee. ) RAY M. STANFIELD, RECEIVER, ) File No. BAL-940706GP Assignor, ) and ) INLAND EMPIRE BROADCASTING ) CORPORATION, ) Assignee. ) ) For Assignment of the License of ) Radio Station KOLA(FM), ) San Bemardino, California ) MEMORANDUM OPINION AND ORDER Adopted: September 5, 1996 Released: October 25, 1996 By the Commission: 1. The Commission has under consideration the Letter of the Chief. Mass Media Bureau, to Joseph D. Jones, et al. dated June 29, 1995 (hereafter the "Letter Decision"), denying a Petition for Reconsideration filed by Joseph D. Jones ("Jones") of the grant of a pro forma assignment of the license of Station KOLA(FM), San Bemardino, California, from KOLA. Inc. ("KOLAI"), to Ray M. Stanfield, Receiver ("Stanfield"). The Letter Decision also denied a Petition to Deny filed by Jones with respect to a subsequent application to assign the KOLA(FM) license from Stanfield to Inland Empire Broadcasting Corporation ("Inland"), and granted the Inland assignment application. Now before the Commission are a "Petition for Administrative 14297 Federal Communications Commission FCC 96-372 Review" 1 filed by Jones on August 7, 1995, with respect to that portion of the Letter Decision denying his Petition for Reconsideration of the grant of ^& pro forma assignment of KOLA(FM) from KOLAI to Stanfield,2 and a separate -

Southern California Edison

Southern California Edison Public Safety Power Shutoff Protocol (PSPS) Post-Event Reporting in Compliance with Resolution ESRB-8 and Decision 19-05-042 September 21 to October 1, 2019 Submitted to: California Public Utilities Commission Director of the Safety and Enforcement Division October 15, 2019 SCE PSPS Post Event Report September 21 to October 1, 2019 Executive Summary On September 21, 2019, Southern California Edison (SCE) activated its Emergency Operations Center and PSPS Incident Management Team to perform response operations associated with a weather event where forecasted high winds and low relative humidity levels were expected to create the potential for execution of SCE’s Public Safety Power Shutoff (PSPS) protocol. Over the course of the event, potentially impacted customers were identified in Inyo, Kern, Los Angeles, Mono, Riverside, San Bernardino, Santa Barbara, Tulare and Tuolumne counties. The PSPS notifications team completed all required notifications to potentially impacted customers, emergency management agencies (county and state), and elected officials in areas which could be and/or were impacted. Pro-active de-energization was ultimately required for a portion of the Riverside County area and affected 85 customers. SCE submits the following report to the California Public Utilities Commission’s (CPUC) Director of the Safety and Enforcement Division (SED) pursuant to Resolution ESRB-8 and Decision (D.) 19-05-042. In separate sections of this report, SCE sets forth the reasons for its decision to notify customers of the potential for and execution of de-energization and includes an event summary and responses to the questions as required in post-event reporting. -

Exhibit 2181

Exhibit 2181 Case 1:18-cv-04420-LLS Document 131 Filed 03/23/20 Page 1 of 4 Electronically Filed Docket: 19-CRB-0005-WR (2021-2025) Filing Date: 08/24/2020 10:54:36 AM EDT NAB Trial Ex. 2181.1 Exhibit 2181 Case 1:18-cv-04420-LLS Document 131 Filed 03/23/20 Page 2 of 4 NAB Trial Ex. 2181.2 Exhibit 2181 Case 1:18-cv-04420-LLS Document 131 Filed 03/23/20 Page 3 of 4 NAB Trial Ex. 2181.3 Exhibit 2181 Case 1:18-cv-04420-LLS Document 131 Filed 03/23/20 Page 4 of 4 NAB Trial Ex. 2181.4 Exhibit 2181 Case 1:18-cv-04420-LLS Document 132 Filed 03/23/20 Page 1 of 1 NAB Trial Ex. 2181.5 Exhibit 2181 Case 1:18-cv-04420-LLS Document 133 Filed 04/15/20 Page 1 of 4 ATARA MILLER Partner 55 Hudson Yards | New York, NY 10001-2163 T: 212.530.5421 [email protected] | milbank.com April 15, 2020 VIA ECF Honorable Louis L. Stanton Daniel Patrick Moynihan United States Courthouse 500 Pearl St. New York, NY 10007-1312 Re: Radio Music License Comm., Inc. v. Broad. Music, Inc., 18 Civ. 4420 (LLS) Dear Judge Stanton: We write on behalf of Respondent Broadcast Music, Inc. (“BMI”) to update the Court on the status of BMI’s efforts to implement its agreement with the Radio Music License Committee, Inc. (“RMLC”) and to request that the Court unseal the Exhibits attached to the Order (see Dkt. -

Morning Mania Contest, Clubs, Am Fm Programs Gorly's Cafe & Russian Brewery

Guide MORNING MANIA CONTEST, CLUBS, AM FM PROGRAMS GORLY'S CAFE & RUSSIAN BREWERY DOWNTOWN 536 EAST 8TH STREET [213] 627 -4060 HOLLYWOOD: 1716 NORTH CAHUENGA [213] 463 -4060 OPEN 24 HOURS - LIVE MUSIC CONTENTS RADIO GUIDE Published by Radio Waves Publications Vol.1 No. 10 April 21 -May 11 1989 Local Listings Features For April 21 -May 11 11 Mon -Fri. Daily Dependables 28 Weekend Dependables AO DEPARTMENTS LETTERS TO THE EDITOR 4 CLUB LIFE 4 L.A. RADIO AT A GLANCE 6 RADIO BUZZ 8 CROSS -A -IRON 14 MORNING MANIA BALLOT 15 WAR OF THE WAVES 26 SEXIEST VOICE WINNERS! 38 HOT AND FRESH TRACKS 48 FRAZE AT THE FLICKS 49 RADIO GUIDE Staff in repose: L -R LAST WORDS: TRAVELS WITH DAD 50 (from bottom) Tommi Lewis, Diane Moca, Phil Marino, Linda Valentine and Jodl Fuchs Cover: KQLZ'S (Michael) Scott Shannon by Mark Engbrecht Morning Mania Ballot -p. 15 And The Winners Are... -p.38 XTC Moves Up In Hot Tracks -p. 48 PUBLISHER ADVERTISING SALES Philip J. Marino Lourl Brogdon, Patricia Diggs EDITORIAL DIRECTOR CONTRIBUTING WRITERS Tommi Lewis Ruth Drizen, Tracey Goldberg, Bob King, Gary Moskowi z, Craig Rosen, Mark Rowland, Ilene Segalove, Jeff Silberman ART DIRECTOR Paul Bob CONTRIBUTING PHOTOGRAPHERS Mark Engbrecht, ASSISTANT EDITOR Michael Quarterman, Diane Moca Rubble 'RF' Taylor EDITORIAL ASSISTANT BUSINESS MANAGER Jodi Fuchs Jeffrey Lewis; Anna Tenaglia, Assistant RADIO GUIDE Magazine Is published by RADIO WAVES PUBLICATIONS, Inc., 3307 -A Plco Blvd., Santa Monica, CA. 90405. (213) 828 -2268 FAX (213) 453 -0865 Subscription price; $16 for one year. For display advertising, call (213) 828 -2268 Submissions are welcomed. -

Postcard Data Web Clean Status As of Facility ID. Call Sign Service Oct. 1, 2005 Class Population State/Community Fee Code Amoun

postcard_data_web_clean Status as of Facility ID. Call Sign Service Oct. 1, 2005 Class Population State/Community Fee Code Amount 33080 DDKVIK FM Station Licensed A up to 25,000 IA DECORAH 0641 575 13550 DKABN AM Station Licensed B 500,001 - 1.2 million CA CONCORD 0627 3100 60843 DKHOS AM Station Licensed B up to 25,000 TX SONORA 0623 500 35480 DKKSL AM Station Licensed B 500,001 - 1.2 million OR LAKE OSWEGO 0627 3100 2891 DKLPL-FM FM Station Licensed A up to 25,000 LA LAKE PROVIDENCE 0641 575 128875 DKPOE AM Station Const. Permit TX MIDLAND 0615 395 35580 DKQRL AM Station Licensed B 150,001 - 500,000 TX WACO 0626 2025 30308 DKTRY-FM FM Station Licensed A 25,001 - 75,000 LA BASTROP 0642 1150 129602 DKUUX AM Station Const. Permit WA PULLMAN 0615 395 50028 DKZRA AM Station Licensed B 75,001 - 150,000 TX DENISON-SHERMAN 0625 1200 70700 DWAGY AM Station Licensed B 1,200,001 - 3 million NC FOREST CITY 0628 4750 63423 DWDEE AM Station Licensed D up to 25,000 MI REED CITY 0635 475 62109 DWFHK AM Station Licensed D 25,001 - 75,000 AL PELL CITY 0636 725 20452 DWKLZ AM Station Licensed B 75,001 - 150,000 MI KALAMAZOO 0625 1200 37060 DWLVO FM Station Licensed A up to 25,000 FL LIVE OAK 0641 575 135829 DWMII AM Station Const. Permit MI MANISTIQUE 0615 395 1219 DWQMA AM Station Licensed D up to 25,000 MS MARKS 0635 475 129615 DWQSY AM Station Const. -

FM-1949-07.Pdf

MM partl DIRECTORY BY OPL, SYSTEMS COUNTY U POLICE 1S1pP,TE FIRE FORESTRYOpSp `p` O COMPANIES TO REVISED LISTINGS 1, 1949 4/ka feeZ means IessJnterference ... AT HEADQUARTERS THE NEW RCA STATION RECEIVER Type CR -9A (152 -174 Mc) ON THE ROAD THE NEW RCA CARFONE Mobile 2 -way FM radio, 152 -174 Mc ...you get the greatest selectivity with RCA's All -New Communication Equipment You're going to hear a lot about selectivity from potentially useful channels for mobile radio communi- now on. In communication systems, receiver selectiv- cation systems. ity, more than any other single factor, determines the For degree of freedom from interference. complete details on the new RCA Station Re- This is impor- ceiver type CR -9A, tant both for today and for the future. and the new RCA CARFONE for mobile use, write today. RCA engineers are at your Recognizing this fact, RCA has taken the necessary service for consultation on prob- steps to make its all -new communication equipment lems of coverage, usage, or com- the most selective of any on the market today. To the plex systems installations. Write user, this means reliable operation substantially free Dept. 38 C. from interference. In addition, this greater selectivity Free literature on RCA's All -New now rhakes adjacent -channel operation a practical Communication Equipment -yours possibility - thereby greatly increasing the number of for the asking. COMMUN /CAT/ON SECT/ON RADIO CORPORATION of AMERICA ENGINEERING PRODUCTS DEPARTMENT, CAMDEN, N.J. In Canada: R C A VICTOR Company limited, Montreal Á#ofher s with 8(11(011' DlNews ERIE'S FIRST TV STATION Says EDWARD LAMB, publisher of "The Erie Dis- telecasting economics. -

For Public Inspection Comprehensive

REDACTED – FOR PUBLIC INSPECTION COMPREHENSIVE EXHIBIT I. Introduction and Summary .............................................................................................. 3 II. Description of the Transaction ......................................................................................... 4 III. Public Interest Benefits of the Transaction ..................................................................... 6 IV. Pending Applications and Cut-Off Rules ........................................................................ 9 V. Parties to the Application ................................................................................................ 11 A. ForgeLight ..................................................................................................................... 11 B. Searchlight .................................................................................................................... 14 C. Televisa .......................................................................................................................... 18 VI. Transaction Documents ................................................................................................... 26 VII. National Television Ownership Compliance ................................................................. 28 VIII. Local Television Ownership Compliance ...................................................................... 29 A. Rule Compliant Markets ............................................................................................ -

(Unedited) April 9, 2019 College of Arts and Letters

College/Unit Highlights (unedited) April 9, 2019 College of Arts and Letters Student Success ENG: The English club held a study hall/social event on Friday 3/15 from 4:00-8:00 in UH 053. ENG: Professor Jason Perez will be taking several English students (staff members of Pacific Review enrolled in ENG 543 Literary Production) to the annual AWP (American Writers Project) conference in Portland (March 27-30). ENG: Senior Misael Osorio (Creative Writing) has been admitted to the MFA program at the University of Notre Dame, with a fellowship. PHIL: On March 13, Jenny Brown, founder of Woodstock Farm Animal Sanctuary and author of The Lucky Ones: My Passionate Fight for Farm Animals, gave a talk to about 50 students enrolled in various PHIL courses. Brown's presentation challenged students to take a closer look at our food system and the uncomfortable truths behind it, forcing them to think about our consumption habits and the ethics of our everyday choices. COYOTE RADIO & ADVERTISING: Ten of the 11 entries submitted by the Coyote Advertising student design team won at the March 15 American Advertising Federation - Inland Chapter’s ADDY Awards banquet at the Mission Inn in Riverside. Four student designers (CAL grads!) - Maelani Balane, Robert Klimper, Nicole Rodriguez and Bliss Gray, were recognized for their work in graphic design, videography and written campaigns. Most impressive was that all won in the “Professional Category.” This team picked up 4 Silver and 6 Bronze ADDYs! Read more: https://inside.csusb.edu/node/21581 COYOTE R & A: Radio student, Collin Pacillo (seen above on right at ADDYs), was hired as a board operator at Inland Empire country music station, K-FROG, 95.1 FM. -

FY 2004 AM and FM Radio Station Regulatory Fees

FY 2004 AM and FM Radio Station Regulatory Fees Call Sign Fac. ID. # Service Class Community State Fee Code Fee Population KA2XRA 91078 AM D ALBUQUERQUE NM 0435$ 425 up to 25,000 KAAA 55492 AM C KINGMAN AZ 0430$ 525 25,001 to 75,000 KAAB 39607 AM D BATESVILLE AR 0436$ 625 25,001 to 75,000 KAAK 63872 FM C1 GREAT FALLS MT 0449$ 2,200 75,001 to 150,000 KAAM 17303 AM B GARLAND TX 0480$ 5,400 above 3 million KAAN 31004 AM D BETHANY MO 0435$ 425 up to 25,000 KAAN-FM 31005 FM C2 BETHANY MO 0447$ 675 up to 25,000 KAAP 63882 FM A ROCK ISLAND WA 0442$ 1,050 25,001 to 75,000 KAAQ 18090 FM C1 ALLIANCE NE 0447$ 675 up to 25,000 KAAR 63877 FM C1 BUTTE MT 0448$ 1,175 25,001 to 75,000 KAAT 8341 FM B1 OAKHURST CA 0442$ 1,050 25,001 to 75,000 KAAY 33253 AM A LITTLE ROCK AR 0421$ 3,900 500,000 to 1.2 million KABC 33254 AM B LOS ANGELES CA 0480$ 5,400 above 3 million KABF 2772 FM C1 LITTLE ROCK AR 0451$ 4,225 500,000 to 1.2 million KABG 44000 FM C LOS ALAMOS NM 0450$ 2,875 150,001 to 500,000 KABI 18054 AM D ABILENE KS 0435$ 425 up to 25,000 KABK-FM 26390 FM C2 AUGUSTA AR 0448$ 1,175 25,001 to 75,000 KABL 59957 AM B OAKLAND CA 0480$ 5,400 above 3 million KABN 13550 AM B CONCORD CA 0427$ 2,925 500,000 to 1.2 million KABQ 65394 AM B ALBUQUERQUE NM 0427$ 2,925 500,000 to 1.2 million KABR 65389 AM D ALAMO COMMUNITY NM 0435$ 425 up to 25,000 KABU 15265 FM A FORT TOTTEN ND 0441$ 525 up to 25,000 KABX-FM 41173 FM B MERCED CA 0449$ 2,200 75,001 to 150,000 KABZ 60134 FM C LITTLE ROCK AR 0451$ 4,225 500,000 to 1.2 million KACC 1205 FM A ALVIN TX 0443$ 1,450 75,001