China Internet Report 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CYAD JP Morgan Itinerary

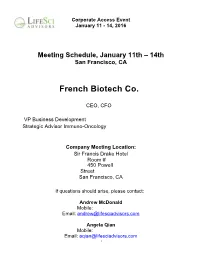

Corporate Access Event January 11 - 14, 2016 Meeting Schedule, January 11th – 14th San Francisco, CA French Biotech Co. CEO, CFO VP Business Development Strategic Advisor Immuno-Oncology Company Meeting Location: Sir Francis Drake Hotel Room # 450 P owell Street San Franc isco, CA If questions should arise, please contact: Andrew McDonald Mobile: Email: [email protected] Angela Qian Mobile: Email: [email protected] -1 Corporate Access Event January 11 - 14, 2016 MEETINGS Note: (*) indicates that this meeting time is double-booked. Meeting Time Room Meeting With Note Type Monday, January 11, 2016 08:00-09:00 am Sir Francis Drake (450 1x1 Aquilo Capital Powell St), Room 530 Patrick Rivers 09:00-10:00 am Sir Francis Drake (450 1x1 Auriga Capital Powell St), Room 530 Glen Losev 10:00-11:00 am Hotel Nikko (222 Mason 1x1 Takeda St), 25th Floor, Bay Kiran Philip View Room 11:00-12:00 pm Sir Francis Drake (450 1x1 Granite Investment Partners LAST MINUTE Powell St), Room 530 Jeffrey Hoo CANCELLATION 12:00-1:00 pm Marriott Marquis (780 1x1 AbbVie Onsite Contact: Mission St), Salon 14 Niels Emmerich Tiffany Cincotta-Janzen, (847) 393-5723 01:30-02:00 pm Sir Francis Drake (450 1x1 Alpine BioVentures, GP LLC Powell St), Room 530 David Miller 03:00-03:30 pm Sir Francis Drake (450 1x1 Tara Capital Grp Powell St), Room 530 Dhesh Govender 04:00-05:00 pm Sir Francis Drake (450 1x1 EVOLUTION Life Science Partners Powell St), Room 530 Anton Gueth Tuesday, January 12, 2016 07:00-08:30 am* Breakfast Fierce Biotech Big Data Breakfast CEO will attend. -

PUBLIC NOTICE FEDERAL COMMUNICATIONS COMMISSION 445 12Th STREET S.W

PUBLIC NOTICE FEDERAL COMMUNICATIONS COMMISSION 445 12th STREET S.W. WASHINGTON D.C. 20554 News media information 202-418-0500 Internet: http://www.fcc.gov (or ftp.fcc.gov) TTY (202) 418-2555 DA No. 09-2218 Report No. TEL-01391 Thursday October 15, 2009 INTERNATIONAL AUTHORIZATIONS GRANTED Section 214 Applications (47 C.F.R. § 63.18); Section 310(b)(4) Requests The following applications have been granted pursuant to the Commission’s streamlined processing procedures set forth in Section 63.12 of the Commission’s rules, 47 C.F.R. § 63.12, other provisions of the Commission’s rules, or procedures set forth in an earlier public notice listing applications accepted for filing. Unless otherwise noted, these grants authorize the applicants (1) to become a facilities-based international common carrier subject to 47 C.F.R. § 63.22; and/or (2) to become a resale-based international common carrier subject to 47 C.F.R. § 63.23; or (3) to exceed the 25 percent foreign ownership benchmark applicable to common carrier radio licensees under 47 U.S.C. § 310(b)(4). THIS PUBLIC NOTICE SERVES AS EACH NEWLY AUTHORIZED CARRIER'S SECTION 214 CERTIFICATE. It contains general and specific conditions, which are set forth below. Newly authorized carriers should carefully review the terms and conditions of their authorizations. Failure to comply with general or specific conditions of an authorization, or with other relevant Commission rules and policies, could result in fines and forfeitures. Petitions for reconsideration under Section 1.106 or applications for review under Section 1.115 of the Commission's rules in regard to the grant of any of these applications may be filed within thirty days of this public notice (see Section 1.4(b)(2)). -

Kraneshares CICC China Leaders 100 Index ETF*

Contact us: +(1) 855 8KRANE8 [email protected] KFYP KraneShares CICC China Leaders 100 Index ETF* Investment Strategy: Fund Details Data as of 01/31/2021 KFYP tracks the CSI CICC Select 100 Index, which takes a smart-beta1 approach to systematically invest in companies listed in Mainland China. The strategy is based on Primary Exchange NYSE China International Capital Corporation (CICC)’s latest research on China’s capital markets. This quantitative approach reflects CICC’s top down and bottom up CUSIP 500767207 research process, seeking to deliver the 100 leading companies in Mainland China. ISIN US5007672075 KFYP Features: Total Annual Fund Operating Expense 0.69% 2 Smart beta strategy which seeks to deliver cost effective alpha . Inception Date 7/22/2013 Exposure to the top 100 industry leaders within China’s Mainland A-share market Distribution Frequency Annual identified through the CICC Research team’s quantitative methodology. Seeks to provide exposure to performance leaders through a Return on Equity Index Name CSI CICC Select 100 Index (ROE)3 filter which is further refined through bottom-line growth and valuation criteria. Number of Holdings 96 About CICC & CICC Research: CICC is a leading, publicly traded, Chinese financial services company with expertise in research, asset management, investment banking, private equity and Top 10 Holdings as of 01/31/2021 Ticker % wealth management. Holdings are subject to change. In 2019, the CICC Research Team ranked #1 in Institutional Investor’s All-China Research Category for the eighth year in a row.4 MIDEA GROUP CO LTD-A 000333 6.25 CICC has over 200 branches across Mainland China, with offices in Hong Kong, INNER MONG YIL-A 600887 6.05 Singapore, New York, San Francisco, and London. -

FTSE Publications

2 FTSE Russell Publications 01 October 2020 FTSE Value Stocks China A Share Indicative Index Weight Data as at Closing on 30 September 2020 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) Agricultural Bank of China (A) 4.01 CHINA Fuyao Glass Group Industries (A) 1.43 CHINA Seazen Holdings (A) 0.81 CHINA Aisino Corporation (A) 0.52 CHINA Gemdale (A) 1.37 CHINA Shanghai Fosun Pharmaceutical Group (A) 1.63 CHINA Anhui Conch Cement (A) 3.15 CHINA GoerTek (A) 2.12 CHINA Shenwan Hongyuan Group (A) 1.11 CHINA AVIC Investment Holdings (A) 0.61 CHINA Gree Electric Appliances Inc of Zhuhai (A) 7.48 CHINA Shenzhen Overseas Chinese Town Holdings 0.66 CHINA Bank of China (A) 2.23 CHINA Guangdong Haid Group (A) 1.24 CHINA (A) Bank Of Nanjing (A) 1.32 CHINA Guotai Junan Securities (A) 1.99 CHINA Sichuan Chuantou Energy (A) 0.71 CHINA Bank of Ningbo (A) 2 CHINA Hangzhou Hikvision Digital Technology (A) 3.56 CHINA Tbea (A) 0.86 CHINA Beijing Dabeinong Technology Group (A) 0.56 CHINA Henan Shuanghui Investment & Development 1.49 CHINA Tonghua Dongbao Medicines(A) 0.59 CHINA China Construction Bank (A) 1.83 CHINA (A) Weichai Power (A) 2.09 CHINA China Life Insurance (A) 2.14 CHINA Hengtong Optic-Electric (A) 0.59 CHINA Wuliangye Yibin (A) 9.84 CHINA China Merchants Shekou Industrial Zone 1.03 CHINA Industrial and Commercial Bank of China (A) 3.5 CHINA XCMG Construction Machinery (A) 0.73 CHINA Holdings (A) Inner Mongolia Yili Industrial(A) 6.32 CHINA Xinjiang Goldwind Science&Technology (A) 0.74 -

21143 5G in China Report V2.Indd

5G in China: the enterprise story More than another G of speed? Copyright © 2018 GSM Association 5G IN CHINA: THE ENTERPRISE STORY GSMA Intelligence The GSMA represents the interests of mobile GSMA Intelligence is the definitive source of global operators worldwide, uniting nearly 800 operators mobile operator data, analysis and forecasts, and with more than 300 companies in the broader publisher of authoritative industry reports and mobile ecosystem, including handset and device research. makers, software companies, equipment providers Our data covers every operator group, network and internet companies, as well as organisations in and MVNO in every country worldwide – from adjacent industry sectors. The GSMA also produces Afghanistan to Zimbabwe. It is the most accurate industry-leading events such as Mobile World and complete set of industry metrics available, Congress, Mobile World Congress Shanghai, Mobile comprising tens of millions of individual data points, World Congress Americas and the Mobile 360 Series updated daily. of conferences. GSMA Intelligence is relied on by leading operators, For more information, please visit the GSMA vendors, regulators, financial institutions and corporate website at www.gsma.com third-party industry players, to support strategic Follow the GSMA on Twitter: @GSMA decision-making and long-term investment planning. The data is used as an industry reference point and is frequently cited by the media and by the industry itself. Our team of analysts and experts produce regular thought-leading research reports across a range of industry topics. GTI (Global TD-LTE Initiative), founded in 2011, has been dedicated to constructing a robust ecosystem www.gsmaintelligence.com of TD-LTE and promoting the convergence of [email protected] LTE TDD and FDD. -

RRP Sector Assessment

OrbiMed Asia Partners III, LP Fund (RRP REG 51072) OWNERSHIP, MANAGEMENT, AND GOVERNANCE A. The Fund Structure 1. The Asian Development Bank (ADB) proposes to invest in OrbiMed Asia Partners III, LP Fund (OAP III), which is a Cayman Islands exempted limited partnership seeking to raise up to $500 million in capital commitments. It is managed by OrbiMed Asia GP III, LP (the general partner), a Cayman Islands exempted limited partnership. The sole limited partner of the general partner is OrbiMed Advisors III Limited, a Cayman Islands exempted company. OrbiMed Advisors LLC (the investment advisor), a registered investment advisor with the United States (US) Securities and Exchange Commission, will provide investment advisory services to OAP III. This structure is illustrated in the figure below. Table 1 shows the ultimate beneficial owners (UBOs) of the general partner and the investment advisor. Table 1: Ultimate Beneficial Owners of the General Partner and the Investment Advisor (ownership stake, %) Name Investment Advisor General Partner Sven H. Borho (~10–25%) (~8%) Alexander M. Cooper (~8%) Carl L. Gordon (~10–25%) (~8%) (also Director) Geoffrey C. Hsu (<5%) (~8%) Samuel D. Isaly (~50–75%) (~8%) W. Carter Neild (<5%) (~8%) (also Director) Jonathan T. Silverstein (~5–10%) (~8%) (also Director) Sunny Sharma (~8%) (also Officer) Evan D. Sotiriou (~8%) David G. Wang (~8%) (also Officer) Jonathan Wang (~8%) (also Officer) Sam Block III (~8%) Source: OrbiMed Group. 2 2. Investors. The fund held a first closing of approximately $233.5 million on 1 March 2017, and a second closing of approximately $137.6 million on 26 April 2017. -

Tencent and China Mobile's Dilemma

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by AIS Electronic Library (AISeL) Association for Information Systems AIS Electronic Library (AISeL) Pacific Asia Conference on Information Systems PACIS 2014 Proceedings (PACIS) 2014 FROM WECHAT TO WE FIGHT: TENCENT AND CHINA MOBILE’S DILEMMA Jun Wu School of Economics and Management, Beijing University of Posts and Telecommunications, [email protected] Qingqing Wan School of Economics and Management, Beijing University of Posts and Telecommunications, [email protected] Follow this and additional works at: http://aisel.aisnet.org/pacis2014 Recommended Citation Wu, Jun and Wan, Qingqing, "FROM WECHAT TO WE FIGHT: TENCENT AND CHINA MOBILE’S DILEMMA" (2014). PACIS 2014 Proceedings. 265. http://aisel.aisnet.org/pacis2014/265 This material is brought to you by the Pacific Asia Conference on Information Systems (PACIS) at AIS Electronic Library (AISeL). It has been accepted for inclusion in PACIS 2014 Proceedings by an authorized administrator of AIS Electronic Library (AISeL). For more information, please contact [email protected]. FROM WECHAT TO WE FIGHT: TENCENT AND CHINA MOBILE’S DILEMMA Jun Wu, School of Economics and Management, Beijing University of Posts and Telecommunications, Beijing, China, [email protected] Qingqing Wan, School of Economics and Management, Beijing University of Posts and Telecommunications, Beijing, China, [email protected] Abstract With the coming of mobile internet era, Giants in the different industry begin to compete face by face. This teaching case presents the event of charging for WeChat in China context to delineate the new challenges that Online Service Provider and Mobile Network Operator will face. -

Japanese Companies' Links to Forced Labor in Xinjiang Uyghur

8 April 2021 [original Japanese text] 6 May 2021 [English translation] Japanese Companies’ Links to Forced Labor in Xinjiang Uyghur Autonomous Region and Corporate Responsibility1 Human Rights Now Japan Uyghur Association We are greatly concerned that Japanese companies have not yet taken sufficient measures to completely eliminate the possibility that they are involved through their supply chains in the Chinese government's mass detention, abuse, forced labor, and destruction of Muslim culture in Xinjiang Uyghur Autonomous Region. It has also been revealed that under the Chinese government's "Strike Hard Campaign against Violent Extremism," there are serious and widespread abuses and violations of basic human rights such as freedom of expression, association and privacy and freedom from torture and inhumane treatment, forced labor, unfair trial, discrimination, and violations of minority rights. In the report "Japanese Companies’ Links to Forced Labor in Xinjiang Uyghur Autonomous Region" dated 28 August 2020,2 we proposed that companies should fulfill their responsibilities in accordance with The UN Guiding Principles on Business and Human Rights ("Guiding Principles")3 in response to forced labor, which is a serious human rights violation, referred to in the report, “Uyghurs for sale: ‘Re-education’, forced labour and surveillance beyond Xinjiang” by the Australian Strategic Policy Institute (ASPI).4 Based on the Guiding Principles, Japanese companies are required to conduct human rights due diligence covering their supply chains and value chains, not only in cases where their business activities cause human rights violations, but also in cases where they may be involved in or contribute to human rights violations, or where their business, products or services directly link to business partners which violate human rights. -

Understanding Private Equity. What Is Private Equity? EXAMPLES of PRIVATELY HELD COMPANIES

Understanding private equity. What is private equity? EXAMPLES OF PRIVATELY HELD COMPANIES: A private equity investor is an individual or entity that invests capital into a private company (i.e. firms not traded on a public exchange) in exchange for equity interest in that business. In the US, there are approximately 18,000 publicly traded companies, and more than 300,000 privately held companies. WHO MIGHT SEEK A PRIVATE EQUITY INVESTOR AS A SOURCE OF CAPITAL? • Companies looking to fund a capital need that is beyond traditional bank financing • Owners considering a partial or complete sale of their business • Managers looking to buy a business Private equity strategies. EXAMPLES OF PRIVATE EQUITY FIRMS: MOST PRIVATE EQUITY INVESTORS WILL LIMIT THEIR INVESTMENTS TO ONE OR TWO OF THE FOLLOWING STRATEGIES: • Angel investing • Growth capital • Venture capital • Distressed investments • Leveraged buyouts (LBO) • Mezzanine capital Sources of capital for PE funds. THERE ARE TWO TYPES OF PRIVATE EQUITY FIRMS: • Firms with a dedicated fund, with the majority of the capital sourced from institutional investors (i.e. pension funds, banks, endowments, etc.) and accredited investors (i.e. high net worth individual investors) • Firms that raise capital from investors on a per-deal basis (pledge funds) INVESTMENT DURATION AND RETURNS. • Typical investment period is 3−10 years, after which capital is distributed to investors • Rates of return are higher than public market returns, typically 15−30%, depending on the strategy HISTORICAL S&P 500 RETURNS S&P 500 Returns Average Source: Standard & Poor’s LCD Private equity fund structure. PRIVATE EQUITY FIRM LIMITED PARTNERS (Investors) (Public pension funds, corporate pension funds, insurance companies, high net worth individuals, family offices, endowments, banks, foundations, funds-of-funds, etc.) Management Company General Partner Fund Ownership Fund Investment Management PRIVATE EQUITY FUND (Limited Partnership) Fund’s Ownership of Portfolio Investments Etc. -

Corporate Venturing Report 2019

Corporate Venturing 2019 Report SUMMIT@RSM All Rights Reserved. Copyright © 2019. Created by Joshua Eckblad, Academic Researcher at TiSEM in The Netherlands. 2 TABLE OF CONTENTS LEAD AUTHORS 03 Forewords Joshua G. Eckblad 06 All Investors In External Startups [email protected] 21 Corporate VC Investors https://www.corporateventuringresearch.org/ 38 Accelerator Investors CentER PhD Candidate, Department of Management 43 2018 Global Startup Fundraising Survey (Our Results) Tilburg School of Economics and Management (TiSEM) Tilburg University, The Netherlands 56 2019 Global Startup Fundraising Survey (Please Distribute) Dr. Tobias Gutmann [email protected] https://www.corporateventuringresearch.org/ LEGAL DISCLAIMER Post-Doctoral Researcher Dr. Ing. h.c. F. Porsche AG Chair of Strategic Management and Digital Entrepreneurship The information contained herein is for the prospects of specific companies. While HHL Leipzig Graduate School of Management, Germany general guidance on matters of interest, and every attempt has been made to ensure that intended for the personal use of the reader the information contained in this report has only. The analyses and conclusions are been obtained and arranged with due care, Christian Lindener based on publicly available information, Wayra is not responsible for any Pitchbook, CBInsights and information inaccuracies, errors or omissions contained [email protected] provided in the course of recent surveys in or relating to, this information. No Managing Director with a sample of startups and corporate information herein may be replicated Wayra Germany firms. without prior consent by Wayra. Wayra Germany GmbH (“Wayra”) accepts no Wayra Germany GmbH liability for any actions taken as response Kaufingerstraße 15 hereto. -

China's Rise in Artificial Intelligence

EQUITY RESEARCH | August 31, 2017 Piyush Mubayi +852-2978-1677 [email protected] Goldman Sachs (Asia) L.L.C. Elsie Cheng +852-2978-0820 [email protected] China's Rise in Goldman Sachs (Asia) L.L.C. Heath P. Terry, CFA +1-212-357-1849 [email protected] Artificial Intelligence Goldman Sachs & Co. LLC The New New China Andrew Tilton For the exclusive use of [email protected] +852-2978-1802 China has emerged as a major global contender in the field of AI, the apex [email protected] technology of the information era. In this report, we set out China’s Goldman Sachs (Asia) L.L.C. ambitious top-down plans, the factors (talent, data and infrastructure) Tina Hou that make China unique and the companies (Baidu, Alibaba and Tencent) +86(21)2401-8694 that are making it happen. We believe the development of an ‘intelligent [email protected] economy’ and ‘intelligent society’ by 2030 in China has the potential to Beijing Gao Hua Securities drive productivity improvement and GDP growth in the next two decades. Company Limited Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. -

U.S. Investors Are Funding Malign PRC Companies on Major Indices

U.S. DEPARTMENT OF STATE Office of the Spokesperson For Immediate Release FACT SHEET December 8, 2020 U.S. Investors Are Funding Malign PRC Companies on Major Indices “Under Xi Jinping, the CCP has prioritized something called ‘military-civil fusion.’ … Chinese companies and researchers must… under penalty of law – share technology with the Chinese military. The goal is to ensure that the People’s Liberation Army has military dominance. And the PLA’s core mission is to sustain the Chinese Communist Party’s grip on power.” – Secretary of State Michael R. Pompeo, January 13, 2020 The Chinese Communist Party’s (CCP) threat to American national security extends into our financial markets and impacts American investors. Many major stock and bond indices developed by index providers like MSCI and FTSE include malign People’s Republic of China (PRC) companies that are listed on the Department of Commerce’s Entity List and/or the Department of Defense’s List of “Communist Chinese military companies” (CCMCs). The money flowing into these index funds – often passively, from U.S. retail investors – supports Chinese companies involved in both civilian and military production. Some of these companies produce technologies for the surveillance of civilians and repression of human rights, as is the case with Uyghurs and other Muslim minority groups in Xinjiang, China, as well as in other repressive regimes, such as Iran and Venezuela. As of December 2020, at least 24 of the 35 parent-level CCMCs had affiliates’ securities included on a major securities index. This includes at least 71 distinct affiliate-level securities issuers.