CDL | Investor Relations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SAVOURING SINGAPORE This Urbane Island-State Is All About Its Sophisticated Fusion of Diverse Cuisines, Vibrant Cultures and Architectural Gems

TRAVEL TRAVEL SAVOURING SINGAPORE This urbane island-state is all about its sophisticated fusion of diverse cuisines, vibrant cultures and architectural gems. By Doug Wallace ity, state and country, all rolled into one Tamil — but you will also hear many other It’s also worth noting that, for a country that — Singapore, the chameleon nation of tongues, including the colloquial “Singlish.” has been evolving for centuries, Singapore boasts Southeast Asia, is many things all at once. This island nation is also an architect’s paradise, a surprising number of green spaces where Its colourful history as a trading settlement with cutting-edge skyscrapers coexisting with visitors and locals alike can saunter through influences all facets of modern life, colonial-era buildings meticulously revived and and relax. One of these is the Botanic Gardens, C harmoniously, in innovative ways. infused with modern elements. Streets are awash which showcases the world’s largest collection The population of 5.8 million is a vibrant in colour, thanks to the lively façades of the of orchids. Gardens by the Bay, a futuristic eco- mix of Chinese, Indian and Malay cultures iconic mixed-use traditional shophouses, where architectural park, features two biomes and a — Peranakans (locally born Singaporeans) retail stores are on the main floor and, above “forest” of tree-like towers covered with tropical The glittering Marina Bay skyline at descended from people who began immigrating them, one or two storeys of apartments. Well- flowers and ferns. In addition to running tracks sundown is an irresistable magnet for to the Malay Archipelago 400 years ago — preserved places of worship anchor almost every and dog-walking parks, as well as yoga and tai Instagram aficionados, whether they’re and more than 145 years of British rule left an neighbourhood, such as the Sri Mariamman, the chi class venues, these urban oases also offer a locals or first-time visitors to Singapore. -

Download 1919 E-Brochure

SEXY, EDGY, SHARPLY SOPHISTICATED AND MINIMALIST IN BLACK AND WHITE ARE THE DEFINING A WAY THAT FEELS HARMONIOUS AND COMPOSED, SHADES OF THE NEW MILLENNIUM. 2 SIMPLY TIMELESS Artist’s impression 3 INTRODUCING 1919 An inspired collection of seventy-five black & white apartments, 1919 recalls the charmed lives of ease and elegance associated with Singapore’s colonial era. Set amidst the stylish yet in sophisticated interior tranquil Mount Sophia design. 1919 offers you a neighbourhood, 1919 contemporary yet classic combines the distinctiveness home that will remain of Singapore’s iconic timeless in its beauty, architecture with the latest form and function. 4 5 A PIECE OF HISTORY 19191919 isis lolocateded in ththe illuillustrioustrious Mountount SopSophia neigeighboubourhood,hood, anan areaea entnthusused withwith a ricich hihistoryry datingting backck to 18231823. Originally called Seligi Hill, the Holy Infant Jesus western slopes of Mount (now CHIJMES), Sophia which lead down to home to Chinese St.Margaret’s Primary Handy Road. Singaporean merchants and School and Nan Hwa Girls’ their families who sought to High School, making it Strolling around the area move away from the one of the earliest middle today one can still get a increasingly over-populated class districts in Singapore Chinatown in the late - thereby setting the impressive heritage, and 1800’s, venturing to higher architectural and social tone whilst some of the iconic grounds and bringing of the area. architecture still remains, with them the archetypal it is now fused with Singapore shophouses, Over the years, this enclave modern structures such as those that occupy of Singapore has boasted - a mark of a true the current site at 1919. -

JUL 07 a Quarterly Publication by City Developments Limited

JUL 07 A Quarterly Publication by City Developments Limited CDL WON HIGHEST BCA GREEN MARK AWARDS WELCOME TO THE NEW HAUTE LIVING LANDMARK From your vantage point, the world revolves 360° around you at Cliveden at Grange. The epitome of prestige and refinement, revel in the generous and ingenious spaces. Apartments range from 2,100 square feet to 6,000 square feet. ENTER A WORLD OF TIMELESS SOPHISTICATION, WITH ELEGANCE AND REFINEMENT AT EVERY TURN, ONLY AT CLIVEDEN AT GRANGE. YOUR SENSES WILL BE HEIGHTENED TO A NEW LEVEL OF LUXURY – WHERE NOTHING ELSE COMPARES. WELCOME TO THE NEW HAUTE LIVING LANDMARK Artist’s Impression At Cliveden at Grange, luxuriate in absolute privacy with only Designed by world-renowned architect Carlos Ott, the same one residence per floor. Stepping into your own private lift man behind the immensely successful One Shenton and The lobby, be swept away by grandeur as you enter the stylish and Solitaire, Cliveden at Grange comprises four elegant glass generously-sized apartment, complete with only the finest towers set amidst regally manicured gardens of paradise. designer fittings and fixtures. The artful landscaping re-creates a beautiful and captivating Be enthralled by virtually 360° spectacular panoramas of Garden of Eden experience – a delight for the senses. Viewing the surrounding views and beyond. Located at the doorstep of the show suite is by appointment only. of the pulsating Orchard Road vicinity, this freehold iconic residence is destined for prominence as possibly the finest For the pleasure of ownership, please contact (65) 6732 1211. – and most exclusive – residential project in the prestigious District 10 residential enclave. -

097 Lasalle Prospectus

LASALLE PROSPECTUS 097 001 LASALLE PROSPECTUS CONTENT 005/ABOUT LASALLE 009/WHY LASALLE 011/INTEGRATED ARTS CAMPUS 013/BEST OF BOTH WORLDS 015/THE WIN-WIN FACTOR 016/A-LUMINARIES 019/WHY SINGAPORE? 021/HOW TO GET TO LASALLE DIPLOMA PROGRAMMES 024/DESIGN COMMUNICATION 025/FASHION 026/INTERIOR DESIGN 027/PRODUCT DESIGN 028/FINE ARTS 029/ANIMATION 030/BROADCAST MEDIA 031/AUDIO PRODUCTION 032/DANCE 033/MUSIC 034/PERFORMANCE 035/TECHNICAL AND PRODUCTION MANAGEMENT BACHELOR OF ARTS (HONS) PROGRAMMES 039/DESIGN COMMUNICATION 041/FASHION DESIGN AND TEXTILES 043/FASHION MEDIA AND INDUSTRIES 045/INTERIOR DESIGN 047/PRODUCT DESIGN 049/FINE ARTS 051/ANIMATION ART 053/FILM 055/ACTING 057/DANCE 059/MUSIC 061/MUSICAL THEATRE 063/ARTS MANAGEMENT CERTIFICATE PROGRAMMES 067/FOUNDATION CERTIFICATE IN VISUAL ARTS 069/ENGLISH LANGUAGE FOR THE CREATIVE ARTS ADMISSIONS 072/HOW TO APPLY 073/APPLICATION FEES 074/ACADEMIC REQUIREMENTS 077/CREATIVE PORTFOLIO/AUDITION REQUIREMENTS & WRITTEN ASSIGNMENTS 086/TUITION FEES 088/SCHOLARSHIPS 090/FINANCIAL ASSISTANCE 092/PRIVATE EDUCATION ACT 093/REFUND POLICY 094/SUPPORTING DOCUMENT CHECKLIST 095/ACKNOWLEDGEMENT 096/FIND OUT MORE LASALLE PROSPECTUS 00303 “A Renaissance City Plan was conceptualised to enable Singapore to become a global arts city with strong inter-cultural bonds and a distinct national identity. Today, a decade later, there have indeed been dramatic changes in our skyline and there is a vast array of arts and cultural activities. This year, London-based magazine, Monocle, ranks Singapore as 15th most liveable -

APR 08 a Quarterly Publication by City Developments Limited

APR 08 A Quarterly Publication by City Developments Limited The Legendary St. Regis Opens its Doors in Singapore Record Profit in 2007 It was truly a grand affair. A party of glitz and glamour, at the official opening of the six-star St. Regis Singapore on 20 April 2008. The event was attended by over 700 GLITZ AND GLAMOUR distinguished guests, comprising foreign dignitaries, government leaders, members AT ST. REGIS SINGAPORE of the business and arts community as well as society’s who’s who. “Singapore is excited to be the home of the first St. Regis Hotel in South-East Asia. I commend the owners of the hotel for their vision in bringing this fine name in hospitality to Singapore, a name that has been synonymous with the hospitality industry for over a century.” A red-carpet evening of refinement and grandeur, guests were treated to the renowned and exclusive Krug Mr Mah Bow Tan, champagne, mouth-watering gourmet treats and not Minister for National Development forgetting, world-class entertainment. Bob Valentine and his jazz ensemble breathed exhilaration and exuberance into the majestic ballroom by serenading the “For the past ten years or night away with familiar favourites, while dynamic tap dancers so, no other internationally injected an energetic up-tempo beat to the evening with their branded six-star hotel snazzy footwork. development has been launched in Singapore. Today, I present to you, the latest remarkable property in the St Regis luxury collection... the flagship of the St Regis brand in Southeast Asia!” Guests toured the hotel’s exquisitely-appointed suites and Mr Kwek Leng Beng, mingled freely amongst the impressive world-class artworks Executive Chairman, from Botero, Miro, Chagall, among others. -

Green Sustainable

Inside this issue: XILINX ASIA PACIFIC PARC EMILY CONDOMINIUM CONSTRUCTION WASTE 2 HEADQUARTERS 7 This project makes use of the natural 10 RECYCLING TECHNOLOGIES A key design for this project is elements to maximise natural daylight Recycling of the different types of sustainability and the aim to create and ventilation waste materials for construction a ‘green’ space applications Going and moregreen sustainable When the inaugural edition of PREFAB increasingly focused on being green Mark Platinum Award winner and the Architecture was issued in 2003, its and sustainable. More developers Parc Emily Condominium, one of the aim was to promote and upgrade the and designers are incorporating best pioneer projects that was awarded the design and construction techniques of practices in environmental design and BCA Green Mark Gold Award in 2005. prefabricated architectures in Singapore. construction, and adopting green building In addition, construction waste recycling The intention was to feature outstanding technologies. These measures will technologies and the application of such prefabricated solutions used in various reap many long term benefits for the recycled products are highlighted in local and overseas buildings. building owners, such as reduced energy another article. and utility bills, and improved indoor Over the years, the team has highlighted environmental quality for healthy living I would like to thank SIA for its strong various prefabricated systems successfully and reduced environmental impact. support and making this newsletter a adopted by local designers and builders. successful private-public collaboration. I PREFAB Architecture has been well- It is therefore time for PREFAB architecture am confident that Sustainable Architecture received locally and overseas. -

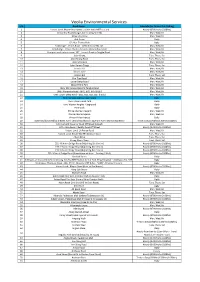

Veolia Environmental Services

Veolia Environmental Services S/N Road Name Schedule (Inc Drain Litter Picking) 1 Vacant Land: Mayne Road (next to Little India MRT station) Hourly (0700hrs to 0100hrs) 2 Alexandra Road (Ganges Ave to Leng Kee Rd) Mon, Wed, Fri 3 Alexandra View Mon, Wed, Fri 4 Ash Grove Daily 5 CP: Mar Thoma Park Daily 6 Footbridge - Jervois Road behind house No. 40 Mon, Wed, Fri 7 Footbridge - Prince Charles Crescent (Alexandra canal) Mon, Wed, Fri 8 Footpath and staircase near 107 Jervois Road to Tanglin Road Mon, Wed, Fri 9 Jalan Kilang Tues, Thurs, Sat 10 Jalan Kilang Barat Tues, Thurs, Sat 11 Jalan Membina Mon, Wed, Fri 12 Jalan Rumah Tinggi Tues, Thurs, Sat 13 Jervois Hill Mon, Wed, Fri 14 Jervois Lane Mon, Wed, Fri 15 Keppel Hill Tues, Thurs, Sat 16 Kim Tian Road Mon, Wed, Fri 17 Lower Delta Road Mon, Wed, Fri 18 Mount Echo Park Mon, Wed, Fri 19 Near 107 Jervois Road to Tanglin Road Mon, Wed, Fri 20 OHB: Alexandra Road - (B01, B03, B05 & B07) Mon, Wed, Fri 21 OHB: Lower Delta Road - (B01, B03, B05, B07 & B10) Mon, Wed, Fri 22 Park: Ganges Avenue Open Space Daily 23 Park: Kheam Hock Park Daily 24 Park: Watten Heights Playground Daily 25 Pine Walk Daily 26 Prince Charles Crescent Mon, Wed, Fri 27 Prince Charles Square Mon, Wed, Fri 28 Prince Philip Avenue Daily 29 State land bounded by sheares Ave / Central Boulevard / Bayfront Ave / Marina Boulevard Thrice a day (0700hrs/1100hrs/1500hrs) 30 URA Carpark: Spooner Road Off Street Carpark Mon, Wed, Fri 31 URA: Jalan Besar / Beatty Road Off Street Hourly (0700hrs to 0100hrs) 32 Vacant Land: 1A Peirce -

Haus-On-Handy-Brochure.Pdf

ILLSIDE LIVING MEETS ELEVATED LUXURY WELCOME TO THE HOOD. HISTORY PAINTS A PRETTY BACKDROP. HOW YOUR FUTURE IS SHAPED IS UP TO YOU. HAVING A HOME IN THE BEST PART OF THE CITY IS JUST THE START. HOME IN ON WHAT YOU SEEK. HANG AROUND AND TAKE IN THE VIEW. AUS ON HANDY. Artist’s Impression OW YOU LIVE IS AS IMPORTANT AS WHERE YOU LIVE Designed to complement the scale and architecture of the iconic Tower House and to optimise the unique hillside, the two towers of Haus on Handy feature functional balconies, terraces and a Sky Garden. A perfect balance of form and function, the façade is draped in warm colour tones, resembling timber and terracotta. Lushly landscaped paths and gardens link the Club Haus on top of Mount Sophia to your home. Artist’s Impression BT TIMAH RD Little India Interchange (NE7/DT12) BT TIMAH RD EMERALD HILL RD Istana Tekka Market SERANGOON RD MACKENZIE RD MACKENZIE RD LOCATION E Rochor D I (DT13) N C B E U N R T ROCHOR CANAL RD G MOUNT EMILY RD R H A WILKIE RD L R D UPPER WILKIE RD Mt Emily E X P SOPHIA RD Park Village R E Hotel S Tang BIDEFORD RD S Plaza W A CAVENAGH RD Y St Margaret’s Lucky Pri Sch Plaza CAIRNHILL RD The ORCHARD RD Paragon HULLET RD ION Orchard CinemasRex Mackenzie Rd Sungei Rd Orchard (NS22) Grand Park Chatsworth Intl Sch Mount Emily Park (Interchange Wisma Orchard (Orchard Campus) Mount Emily Rd Atria Village Hotel U/C) Ngee Ann Albert Court City LaSalle College Upper Wilkie Rd Selegie Rd of The Arts NIVEN RD SELEGIE RD ORCHARD TURN Sophia Rd (McNally Campus) The WILKIE RD Saunders Rd Heeren Wilkie -

Download Walking and Cycling Design Guide

SINGAPORE WALKING AND CYCLING DESIGN GUIDE Public Version 1.0 Contributing Agencies Co-led by: With valuable input from: This Guide is an inter-agency in-house production. All rights reserved. Content updated as of November 018. Copyright © 018 xian Contents 1 INTRODUCTION 2.6 Green Buffer. 30 2.7 Roadside Drain . 31 1.1 Vision . 6 .7.1 Types of Roadside Drain. 1.2 Purpose . 6 2.8 Bus Stop. 33 1.3 Pedestrians & Cyclists' Needs. 7 .8.1 Typical Bus Shelter . 1..1 Pedestrian. 7 .8. High-roof Bus Shelter . 4 1.. Cyclist . 8 .8. Bus Stop Features. 4 1.4 Fundamentals of Active Mobility Design 9 2.9 Taxi Stand . 35 1.4.1 Safe. 9 1.4. Direct. 9 2.10 Lighting . 36 .10.1 General Lighting Illuminance. 6 1.4. Comfortable. 10 .10. Placement of Lamp Post for Active Mobility 6 1.5 Walking and Cycling Network Principles 10 .10. Design of Street Lighting. 7 1.6 Universal Design Principles in Active .10.4 Cycling Path Lighting Design. 7 Mobility Designs . 12 .10.5 Cycling Path Lighting Within Covered Linkway 7 1.7 Active Mobility Programmes . 13 1.7.1 National Cycling Plan . 1 1.7. Covered Linkway Programme. 14 3 ROADSIDE TYPOLOGIES 3.1 Standard Typologies. 40 .1.1 Footpath . 4 2 ROADSIDE ELEMENTS .1. Footpath & Cycling Path . 44 2.1 Footpath. 16 .1. Covered Linkway. 46 .1.1 Standalone Footpath. 16 .1.4 Covered Linkway & Cycling Path . 48 .1. Footpath Next To Cycling Path . 17 .1.5 Bus Stop & Footpath. 50 .1. Materials . -

Illside Living Meets Elevated Luxury Welcome to the Hood

ILLSIDE LIVING MEETS ELEVATED LUXURY WELCOME TO THE HOOD. HISTORY PAINTS A PRETTY BACKDROP. HOW YOUR FUTURE IS SHAPED IS UP TO YOU. HAVING A HOME IN THE BEST PART OF THE CITY IS JUST THE START. HOME IN ON WHAT YOU SEEK. HANG AROUND AND TAKE IN THE VIEW. AUS ON HANDY. Artist’s Impression OW YOU LIVE IS AS IMPORTANT AS WHERE YOU LIVE Designed to complement the scale and architecture of the iconic Tower House and to optimise the unique hillside, the two towers of Haus on Handy feature functional balconies, terraces and a Sky Garden. A perfect balance of form and function, the façade is draped in warm colour tones, resembling timber and terracotta. Lushly landscaped paths and gardens link the Club Haus on top of Mount Sophia to your home. Artist’s Impression BT TIMAH RD Little India Interchange (NE7/DT12) BT TIMAH RD EMERALD HILL RD Istana Tekka Market SERANGOON RD MACKENZIE RD MACKENZIE RD LOCATION E Rochor D I (DT13) N C B E U N R T ROCHOR CANAL RD G MOUNT EMILY RD R H A WILKIE RD L R D UPPER WILKIE RD Mt Emily E X P SOPHIA RD Park Village R E Hotel S Tang BIDEFORD RD S Plaza W A CAVENAGH RD Y St Margaret’s Lucky Pri Sch Plaza CAIRNHILL RD The ORCHARD RD Paragon HULLET RD ION Orchard CinemasRex Mackenzie Rd Sungei Rd Orchard (NS22) Grand Park Chatsworth Intl Sch Mount Emily Park (Interchange Wisma Orchard (Orchard Campus) Mount Emily Rd Atria Village Hotel U/C) Ngee Ann Albert Court City LaSalle College Upper Wilkie Rd Selegie Rd of The Arts NIVEN RD SELEGIE RD ORCHARD TURN Sophia Rd (McNally Campus) The WILKIE RD Saunders Rd Heeren Wilkie -

Integrated Public Cleaning Central South

Integrated Public Cleaning Central South Subject: Park Schedule Dear residents, Below is the summary of park types within Central South region maintained by Sembcorp: INTEGRATED PUBLIC CLEANING CENTRAL SOUTH – PARKS Park Connectors, PCN Community Parks Arts and Heritage Parks Southern Ridges URA Marina Bay Waterfront Promenade & Central Lawn You may click on the above link for each park type or refer to the full list on these subsequent pages. If you have any enquires on our cleaning schedules, please feel free to contact us at our hotline 1800 898 1920 or email us at [email protected]. Page 1 of 7 Integrated Public Cleaning Central South Subject: Park Schedule (Park Connectors, PCN) Dear residents, The PCN parks within Central South region will be cleaned as per the schedule below: S/N Name of Park Connector Schedule 1 Alexandra Canal Linear Park Daily / Thrice on Sat, Sun, PH 2 Alexandra Park Connector Daily / Thrice on Sat, Sun, PH 3 Alexandra-Queensway Park Connector Daily / Thrice on Sat, Sun, PH 4 Henderson Park Connector Daily / Thrice on Sat, Sun, PH 5 Kallang Park Connector Daily / Thrice on Sat, Sun, PH 6 Pelton Canal Park Connector (New) Daily / Thrice on Sat, Sun, PH 7 Whampoa Park Connector Daily / Thrice on Sat, Sun, PH If you have any enquires on our cleaning schedules, please feel free to contact us at our hotline 1800 898 1920 or email us at [email protected]. Page 2 of 7 Integrated Public Cleaning Central South Subject: Park Schedule (Community Park) Dear residents, The community parks -

BOOKBOON.COM KEINE REGISTRIERUNG NOTWENDIG Download Free Books at Bookboon.Com Singapore © 2008 Stig Albeck & Ventus Publishing Aps Translation: Claus Jensen

STIG ALBECK SINGAPORE GRATIS REISEFÜHRER FÜR DEN URLAUB BOOKBOON.COM KEINE REGISTRIERUNG NOTWENDIG Download free books at BookBooN.com Singapore © 2008 Stig Albeck & Ventus Publishing ApS Translation: Claus Jensen All rights and copyright relating to the content of this book are the property of Ventus Publishing ApS, and/or its suppliers. Content from ths book, may not be reproduced in any shape or form without prior written permission from Ventus Publishing ApS. Quoting this book is allowed when clear references are made, in relation to reviews are allowed. ISBN 978-87-7061-299-9 1st edition Pictures and illustrations in this book are reproduced according to agreement with the following copyright owners : Stig Albeck, Flemming Skovlund & Brian McMorrow. The stated prices and opening hours are indicative and may have been subject to change after this book was published. Download free books at BookBooN.com Singapore Kapiteloverskrift ONLIBRI Download free books at BookBooN.com 4 Singapore A visit to Singapore A visit to Singapore www.visitsingapore.com The city-state of Singapore is a wonderful place Singapore is very modern, with splendid where many of Asia’s cultures, new and old, as well architecture and lots of shopping opportunities and as tropical beaches and pristine rainforest, can all be other attractions. Everything is held together via an experienced within a very small area. The official efficient public transportation system. Singapore is language is English, but Singapore’s many ethnic only 60 kilometres from the Equator, and it is a groups, such as Malay, Indian, Arab and the Chinese good starting point for trips to the nearby put their own unique mark on the city, each with Indonesian islands, or to Malaysia’s second largest their own city quarters, shops, restaurants and city, Johor Bahru, which borders Singapore.