Table of Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mound Road Industrial Corridor Technology And

Mound Road Industrial Corridor Technology and Innovation Project Partners: Macomb County, City of Sterling Heights, and City of Warren, MI Contact: John Crumm, Director of Planning, Macomb County Department of Roads (586) 469-5285; [email protected] www.innovatemound.org/INFRA Project Name Mound Road Industrial Corridor Technology and Innovation Project Was an INFRA application for this project submitted No previously? If yes, what was the name of the project in the previous N/a application? Previously Incurred Project Cost $67,797 Future Eligible Project Cost $216,860,000 Total Project Cost $216,927,797 INFRA Request $130,116,000 Total Federal Funding (including INFRA) $130,116,000 (60% of total cost) Are matching funds restricted to a specific project No component? If so, which one? Is the project or a portion of the project currently Yes located on a National Highway Freight Network? Is the project or a portion of the project located on the Yes National Highway System? • Does the project add capacity to the Interstate No system? • Is the project in a national scenic area? No Do the project components include a railway-highway No grade crossing or grade separation project? o If so, please include the grade crossing ID N/a Do the project components include an intermodal or No freight rail project, or freight project within the boundaries of a public or private freight rail, water (including ports) or intermodal facility? If answered yes to either of the two component questions N/a above, how much of requested INFRA funds will be spent -

LARGEST RETAIL Centersranked by Gross Leasable Area

CRAIN'S LIST: LARGEST RETAIL CENTERS Ranked by gross leasable area Shopping center name Leasing agent Address Gross leasable area Company Number of Rank Phone; website Top executive(s) (square footage) Center type Phone stores Anchors Lakeside Mall Ed Kubes 1,550,450 Super-regional Rob Michaels 180 Macy's, Macy's Men & Home, Sears, JCPenney, Lord 14000 Lakeside Circle, Sterling Heights 48313 general manager General Growth Properties Inc. & Taylor 1. (586) 247-1590; www.shop-lakesidemall.com (312) 960-5270 Twelve Oaks Mall Daniel Jones 1,513,000 Super-regional Margaux Levy-Keusch 200 Nordstrom, Macy's, Lord & Taylor, JCPenney, Sears 27500 Novi Road, Novi 48377 general manager The Taubman Co. 2. (248) 348-9400; www.shoptwelveoaks.com (248) 258-6800 Oakland Mall Peter Light 1,500,000 Super-regional Jennifer Jones 127 Macy's, Sears, JCPenney 412 W. 14 Mile Road, Troy 48083 general manager Urban Retail Properties LLC 3. (248) 585-6000; www.oaklandmall.com (248) 585-4114 Northland Center Brent Reetz 1,464,434 Super-regional Amanda Royalty 122 Macy's, Target 21500 Northwestern Hwy., Southfield 48075 general manager AAC Realty 4. (248) 569-6272; www.shopatnorthland.com (317) 590-7913 Somerset Collection John Myszak 1,440,000 Super-regional The Forbes Co. 180 Macy's, Neiman Marcus, Nordstrom, Saks Fifth 2800 W. Big Beaver Road, Troy 48084 general manager (248) 827-4600 Avenue 5. (248) 643-6360; www.thesomersetcollection.com Eastland Center Brent Reetz 1,393,222 Super-regional Casey Conley 105 Target, Macy's, Lowe's, Burlington Coat Factory, 18000 Vernier Road, Harper Woods 48225 general manager (313) 371-1500 K & G Fashions 6. -

Preliminary Design of Bus Rapid Transit in the Southfield/Jefferies C

GM Tlansportation Systems 4.0 INTERMEDIATE SERVICE IN THE SOUTHFIELD-GREENFIELD CORRIDOR The potential transit demand in the Southfield-Greenfield corridor, as estimated in Stage I, is not sufficient to support the non-stop (or one-stop) BRT service envisioned for the Southfield-Jeffries corridor, An intermediate stopping service is therefore proposed to provide improved transit service in the corridor, This section of the final report presents the analyses which led to the design of the Intermediate Service, Following an over view of the system, the evaluation of alternative routes and implementations is described. Then a summary of the corridor demand analysis, including consideration of potential demand for Fairlane, is presented, Finally, system cost estimates are presented. 4.1 Overview of Greenfield Intermediate Service The objective of the Intermediate Service is to provide a higher level of service in the Southfield-Greenfield corridor than is currently being provided by local buses with a system that can be deployed quiGkly and with low capital investment. The system which is proposed to satisfy this objective is an intermediate level bus service operating on Greenfield Road between Southfield and Dearborn, The system is designed to provide improved travel time for relatively long transit trips (two miles or more) by stopping only at major cross-streets and by operating with traffic signal pre-emption. The proposed system operates at constant 12-minute headway throughout the day from 7:00a.m. to 9:00p.m. During periods of peak work trip demand (7:00 to 10:00 a.m. and 3:00 to 6:00p.m.), the route is configured so that direct distribution service is provided to employment sites in Dearborn and in Southfield along Northwestern Highway. -

Demographic Analysis

Appendix 1.1 Waterford Regional Destination Recommended Indoor Amenities Facilities Sq. Ft. Phase I - Waterford Township PDA Driving Range; Golf Simulator 40,000 Basketball, Volleyball Courts 40,000 Tennis, Handball, Racquet Ball Courts 15,000 Community Ice Arena (relocation) 15,000 Amusement Arcade, Go-Karts 15,000 Conference Space; Banquet Hall 15,000 Fitness and Weight Training Facility 10,000 Indoor Race / Running Track 5,000 Rock Wall Climbing / Training Facility 5,000 Modern Skate Park 5,000 Subtotal 165,000 Phase II - Waterford Township PDA Sports Arena - Two Sheets, Flat Surface Arena 40,000 Olympic Size Swimming Pool 15,000 Subtotal 55,000 Total Project Build-Out 220,000 Recommended Outdoor Amenities Tennis Courts nc Bike and Fitness Path nc Baseball / Softball Park nc Bandstand, Festival Market nc nc indicates not comparable. The square footage totals exclude ballfields, parks, boulevards, pavilions, bandstands, paths, and other green space. Appendix 1.2 Recommended Retail Mix Waterford Township Planned Destination Area Replace Lost Retailers, Like… Sq. Ft. Recruit Family Fitness, Like… Sq. Ft. Recruit New Eateries, Like… Sq. Ft. Bath and Body Works (closed) 2,000 Fitness USA 15,000 Boston Market 1,000 Coffee Beanery (closed) 1,000 Powerhouse Gym 15,000 Buffalo Wild Wings 3,500 DOC Eyeworld (closed) 2,000 Subtotal 30,000 Culver's 3,500 Radio Shack (closed) 2,000 Famous Dave's 3,500 Suncoast Motion Picture Co. (closed) 2,000 Recruit Craft Stores, Like… Sq. Ft. Jimmy John's 2,000 Sunglass Hut (closed) 1,000 Michael's Crafts 25,000 Knock Out Bar & Grill 3,000 Subtotal 10,000 Party City 10,000 Longhorn Steakhouse 3,500 JoAnn Fabric 10,000 Max & Erma's 3,500 Retain Existing Anchors, Like… Sq. -

US-60/Grand Avenue Corridor Optimization, Access Management, and System Study (COMPASS)

US-60/Grand Avenue COMPASS Loop 303 to Interstate 10 TM 3 – National Case Study Review US-60/Grand Avenue Corridor Optimization, Access Management, and System Study (COMPASS) Loop 303 to Interstate 10 Technical Memorandum 3 National Case Study Review Prepared for: Prepared by: Wilson & Company, Inc. In Association With: Burgess & Niple, Inc. Partners for Strategic Action, Inc. Philip B. Demosthenes, LLC March 2013 3/25/2013 US-60/Grand Avenue COMPASS Loop 303 to Interstate 10 TM 3 – National Case Study Review Table of Contents List of Abbreviations 1.0 Introduction ............................................................................................................................................................................................. 1 1.1. Purpose of this Paper ................................................................................................................................................................ 1 1.2. Study Area ..................................................................................................................................................................................... 2 2.0 Michigan 1 (M-1)/Woodward Avenue – Detroit, Michigan ................................................................................................... 4 2.1. Access to Urban/Suburban Areas ......................................................................................................................................... 4 2.2. Corridor Access Control ........................................................................................................................................................... -

Rocket Fiber's Launch Includes Second Stage

20150302-NEWS--0001-NAT-CCI-CD_-- 2/27/2015 5:29 PM Page 1 ® www.crainsdetroit.com Vol. 31, No. 9 MARCH 2 – 8, 2015 $2 a copy; $59 a year ©Entire contents copyright 2015 by Crain Communications Inc. All rights reserved Page 3 ROCKET FIBER:PHASE 1 COVERAGE AREA Panasonic unit plays ‘Taps’ ‘To chase for apps, rethinks strategy According to figures provided by Rocket the animal’ Fiber, the download times for ... “Star Wars” movie on Blu-ray: about seven hours at a typical residential Internet speed of Packard Plant owner eyes bids 10 megabits per second but about 4½ minutes at gigabit speed. for historic downtown buildings An album on iTunes: About one minute on LOOKING BACK: ’80s office residential Internet and less than a second BY KIRK PINHO at gigabit speed boom still rumbles in ’burbs CRAIN’S DETROIT BUSINESS Over breakfast at the Inn on Ferry Street in Lions invite Midtown, Fernando Palazuelo slides salt and fans to pepper shakers across the table like chess pieces. They are a representation of his Detroit take a hike real estate strategy. Yes, he says, he’s getting at new Rocket Fiber’s launch ready to make a series of big moves. The new owner of the 3.5 million-square-foot fantasy football camp Packard Plant on the city’s east side has much broader ambitions for his portfolio in the city, which first took notice of him in 2013 when he Retirement Communities bought the shuttered plant — all 47 buildings, all 40 acres — for a mere $405,000 at a Wayne includes second stage County tax foreclosure auction. -

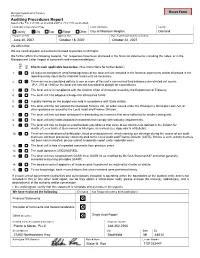

Form 496, Auditing Procedures Report

Michigan Department of Treasury 496 (02/06) Auditing Procedures Report Issued under P.A. 2 of 1968, as amended and P.A. 71 of 1919, as amended. Local Unit of Government Type Local Unit Name County County City Twp Village Other Fiscal Year End Opinion Date Date Audit Report Submitted to State We affirm that: We are certified public accountants licensed to practice in Michigan. We further affirm the following material, “no” responses have been disclosed in the financial statements, including the notes, or in the Management Letter (report of comments and recommendations). Check each applicable box below. (See instructions for further detail.) YES YES NO 1. All required component units/funds/agencies of the local unit are included in the financial statements and/or disclosed in the reporting entity notes to the financial statements as necessary. 2. There are no accumulated deficits in one or more of this unit’s unreserved fund balances/unrestricted net assets (P.A. 275 of 1980) or the local unit has not exceeded its budget for expenditures. 3. The local unit is in compliance with the Uniform Chart of Accounts issued by the Department of Treasury. 4. The local unit has adopted a budget for all required funds. 5. A public hearing on the budget was held in accordance with State statute. 6. The local unit has not violated the Municipal Finance Act, an order issued under the Emergency Municipal Loan Act, or other guidance as issued by the Local Audit and Finance Division. 7. The local unit has not been delinquent in distributing tax revenues that were collected for another taxing unit. -

Issue: Shopping Malls Shopping Malls

Issue: Shopping Malls Shopping Malls By: Sharon O’Malley Pub. Date: August 29, 2016 Access Date: October 1, 2021 DOI: 10.1177/237455680217.n1 Source URL: http://businessresearcher.sagepub.com/sbr-1775-100682-2747282/20160829/shopping-malls ©2021 SAGE Publishing, Inc. All Rights Reserved. ©2021 SAGE Publishing, Inc. All Rights Reserved. Can they survive in the 21st century? Executive Summary For one analyst, the opening of a new enclosed mall is akin to watching a dinosaur traversing the landscape: It’s something not seen anymore. Dozens of malls have closed since 2011, and one study predicts at least 15 percent of the country’s largest 1,052 malls could cease operations over the next decade. Retail analysts say threats to the mall range from the rise of e-commerce to the demise of the “anchor” department store. What’s more, traditional malls do not hold the same allure for today’s teens as they did for Baby Boomers in the 1960s and ’70s. For malls to remain relevant, developers are repositioning them into must-visit destinations that feature not only shopping but also attractions such as amusement parks or trendy restaurants. Many are experimenting with open-air town centers that create the feel of an urban experience by positioning upscale retailers alongside apartments, offices, parks and restaurants. Among the questions under debate: Can the traditional shopping mall survive? Is e-commerce killing the shopping mall? Do mall closures hurt the economy? Overview Minnesota’s Mall of America, largest in the U.S., includes a theme park, wedding chapel and other nonretail attractions in an attempt to draw patrons. -

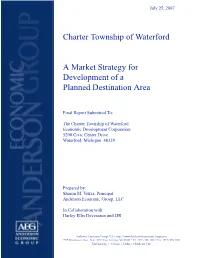

PDA Market Strategy

July 25, 2007 Charter Township of Waterford A Market Strategy for Development of a Planned Destination Area Final Report Submitted To: The Charter Township of Waterford Economic Development Corporation 5200 Civic Center Drive Waterford, Michigan 48329 Prepared by: Sharon M. Vokes, Principal Anderson Economic Group, LLC In Collaboration with: Harley Ellis Devereaux and JJR Anderson Economic Group LLC • http://www.AndersonEconomicGroup.com 1555 Watertower Place, Suite 100 • East Lansing, MI 48823 • Tel: (517) 333-6984 • Fax: (517) 333-7058 East Lansing | Chicago | Dallas | Oklahoma City Waterford Township - Planned Destination Area Final Report Table of Contents 1.0 EXECUTIVE SUMMARY 1 2.0 THE SHOPPING AREA - A BRIEF HISTORY 6 3.0 PROJECT PARAMETERS 10 4.0 A REGIONAL DESTINATION 18 5.0 SPORTS COMPARABLES 22 6.0 MUSIC VENUES 31 7.0 RETAIL ANALYSIS 33 8.0 RETAIL COMPARABLES 36 9.0 RESIDENTIAL ANALYSIS 44 Anderson Economic Group, LLC 0 Waterford Township - Planned Destination Area Final Report 1.0 EXECUTIVE SUMMARY 1.1 Introduction We appreciate this opportunity to contribute to this important project for Waterford Township, and are hopeful that its property owners and other Community Stakeholders are able to share your vision for a mixed-use project that creates a regional destination and refuels economic growth. If this project is planned, designed, implemented and developed carefully, then it has high potential for success, and will enhance the quality of life for your residents, working families and visitors. This document reports our preliminary findings regarding the economic feasibility of redeveloping Waterford Township’s Planned Destination Area (PDA). In short, our findings are favorable for the project, with the following summary of recommenda- tions: 1. -

The Afterlife of Malls

The Afterlife of Malls John Drain INTRODUCTION teenage embarrassments and rejection, along with fonder It seems like it was yesterday: Grandpa imagined the search memories – from visiting Mall Santa to getting fitted for my for some new music would distract him from an illness prom tux. that was reaching its terminal stage. This meant a trip to the Rolling Acres Mall at Akron’s western fringe; probably Some spectators interpret the decline of malls as a signal the destination was a Sam Goody, which in 1996 was as that auto-oriented suburban sprawl is finally unwinding. synonymous with record store as iTunes is with music today. Iconoclasts might attribute their abrupt collapse to a Grandpa bought a couple tapes and then happily strolled conspiracy of “planned obsolescence,” or even declare this the mall concourse. But his relief quickly faded; he slowed a symptom of a decadent society. Some will fault today’s his clip and sidled into a composite bench-planter on a politics or the Great Recession (anachronistically, in most carpeted oasis, confessing, “I am so tired.” cases). Some attribute the decline to a compromised sense of safety among crowds of people who aren’t exposed Grandpa and his cohort – the rubber workers – have mostly to an intensive security screening (certainly the violent vanished from Akron. The Rolling Acres Mall is abandoned. incidents in Ward Parkway Mall in Kansas City2 or the City The so-called “shadow retail” that gradually built up around Center in Columbus3 lend some credence to this view that the mall is today the shadow of a ghost. -

Data Driven Approach to Characterize and Forecast the Impact of Freeway Work Zones on Mobility Using Probe Vehicle Data

Wayne State University Wayne State University Dissertations January 2019 Data Driven Approach To Characterize And Forecast The Impact Of Freeway Work Zones On Mobility Using Probe Vehicle Data Mohsen Kamyab Wayne State University Follow this and additional works at: https://digitalcommons.wayne.edu/oa_dissertations Part of the Computer Sciences Commons, and the Urban Studies and Planning Commons Recommended Citation Kamyab, Mohsen, "Data Driven Approach To Characterize And Forecast The Impact Of Freeway Work Zones On Mobility Using Probe Vehicle Data" (2019). Wayne State University Dissertations. 2358. https://digitalcommons.wayne.edu/oa_dissertations/2358 This Open Access Dissertation is brought to you for free and open access by DigitalCommons@WayneState. It has been accepted for inclusion in Wayne State University Dissertations by an authorized administrator of DigitalCommons@WayneState. DATA DRIVEN APPROACH TO CHARACTERIZE AND FORECAST THE IMPACT OF FREEWAY WORK ZONES ON MOBILITY USING PROBE VEHICLE DATA by MOHSEN KAMYAB DISSERTATION Submitted to the Graduate School of Wayne State University Detroit, Michigan in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY 2019 MAJOR: CIVIL ENGINEERING (Transportation) Approved By: Advisor Date DEDICATION To my beloved family and all my well-wishers. i ACKNOWLEDGMENT I am grateful to many people for their support as I wrote this dissertation. I would like to extend my deepest gratitude to my committee chair Dr. Stephen Remias for his excellent guidance and insight at each step of this process. I am extremely grateful for his continuous support, encouragement and patience. Special thanks to all my committee members whom provided me with their generous guidance and support. -

TAPPER's DIAMONDS & FINE JEWELRY 22Nd ANNUAL COAT

Contact: Kathleen Kennedy Ferris Kennedy Ferris Communications 313.418.4898 [email protected] TAPPER’S DIAMONDS & FINE JEWELRY 22nd ANNUAL COAT DRIVE WILL TAKE PLACE NOW THROUGH NOV. 18 Collection Bins for Warm Winter Items Staged at Tapper’s, Marlee’s, Tapper’s Gold Exchange and Morgan Stanley Locations Throughout Metro Area – New Online Component Will Help Collect Cash for New Coats WEST BLOOMFIELD, MI (October 16, 2013) – Chilly fall days and cold evenings have arrived in southeastern Michigan. For those who are challenged to meet basic needs, a winter coat is an unaffordable luxury. Tapper’s Diamonds & Fine Jewelry seeks to help local residents stay warm this winter by hosting its 22nd annual Coat Drive now through Nov. 18. Tapper’s, in affiliation with Morgan Stanley, will accept gently used or new coats, hats, mittens and blankets, as well as, cash donations for new coats at locations throughout the metro area. “We’re excited to team up with Morgan Stanley this year and together expect to provide more than 2,500 coats for those in need,” says Steven Tapper, custom designer and vice president of Tapper’s Diamonds & Fine Jewelry. “The gift of warmth and comfort has more meaning and value than we can imagine. We urge everyone to join us in this community effort that will change lives.” Tapper’s will also collect funds online at http://www.gofundme.com/tapperscoatdrive. Cash donations raised here and at all Tapper’s, Marlee’s, Tapper’s Gold Exchange and Morgan Stanley locations will go toward the purchase of brand-new coats.