Order 2019 Draft Double Taxation Relief (Cyprus

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

'Political Islam', and the Muslim Brotherhood Review

House of Commons Foreign Affairs Committee ‘Political Islam’, and the Muslim Brotherhood Review Sixth Report of Session 2016–17 Report, together with formal minutes relating to the report Ordered by the House of Commons to be printed 1 November 2016 HC 118 Published on 7 November 2016 by authority of the House of Commons The Foreign Affairs Committee The Foreign Affairs Committee is appointed by the House of Commons to examine the expenditure, administration, and policy of the Foreign and Commonwealth Office and its associated public bodies. Current membership Crispin Blunt MP (Conservative, Reigate) (Chair) Mr John Baron MP (Conservative, Basildon and Billericay) Ann Clwyd MP (Labour, Cynon Valley) Mike Gapes MP (Labour (Co-op), Ilford South) Stephen Gethins MP (Scottish National Party, North East Fife) Mr Mark Hendrick MP (Labour (Co-op), Preston) Adam Holloway MP (Conservative, Gravesham) Daniel Kawczynski MP (Conservative, Shrewsbury and Atcham) Ian Murray MP (Labour, Edinburgh South) Andrew Rosindell MP (Conservative, Romford) Nadhim Zahawi MP (Conservative, Stratford-on-Avon) The following member was also a member of the Committee during this inquiry: Yasmin Qureshi MP (Labour, Bolton South East) Powers The Committee is one of the departmental select committees, the powers of which are set out in House of Commons Standing Orders, principally in SO No 152. These are available on the internet via www.parliament.uk. Publication Committee reports are published on the Committee’s website at www.parliament.uk/facom and in print by Order of the House. Evidence relating to this report is published on the inquiry page of the Committee’s website. -

THE 422 Mps WHO BACKED the MOTION Conservative 1. Bim

THE 422 MPs WHO BACKED THE MOTION Conservative 1. Bim Afolami 2. Peter Aldous 3. Edward Argar 4. Victoria Atkins 5. Harriett Baldwin 6. Steve Barclay 7. Henry Bellingham 8. Guto Bebb 9. Richard Benyon 10. Paul Beresford 11. Peter Bottomley 12. Andrew Bowie 13. Karen Bradley 14. Steve Brine 15. James Brokenshire 16. Robert Buckland 17. Alex Burghart 18. Alistair Burt 19. Alun Cairns 20. James Cartlidge 21. Alex Chalk 22. Jo Churchill 23. Greg Clark 24. Colin Clark 25. Ken Clarke 26. James Cleverly 27. Thérèse Coffey 28. Alberto Costa 29. Glyn Davies 30. Jonathan Djanogly 31. Leo Docherty 32. Oliver Dowden 33. David Duguid 34. Alan Duncan 35. Philip Dunne 36. Michael Ellis 37. Tobias Ellwood 38. Mark Field 39. Vicky Ford 40. Kevin Foster 41. Lucy Frazer 42. George Freeman 43. Mike Freer 44. Mark Garnier 45. David Gauke 46. Nick Gibb 47. John Glen 48. Robert Goodwill 49. Michael Gove 50. Luke Graham 51. Richard Graham 52. Bill Grant 53. Helen Grant 54. Damian Green 55. Justine Greening 56. Dominic Grieve 57. Sam Gyimah 58. Kirstene Hair 59. Luke Hall 60. Philip Hammond 61. Stephen Hammond 62. Matt Hancock 63. Richard Harrington 64. Simon Hart 65. Oliver Heald 66. Peter Heaton-Jones 67. Damian Hinds 68. Simon Hoare 69. George Hollingbery 70. Kevin Hollinrake 71. Nigel Huddleston 72. Jeremy Hunt 73. Nick Hurd 74. Alister Jack (Teller) 75. Margot James 76. Sajid Javid 77. Robert Jenrick 78. Jo Johnson 79. Andrew Jones 80. Gillian Keegan 81. Seema Kennedy 82. Stephen Kerr 83. Mark Lancaster 84. -

Members of the House of Commons December 2019 Diane ABBOTT MP

Members of the House of Commons December 2019 A Labour Conservative Diane ABBOTT MP Adam AFRIYIE MP Hackney North and Stoke Windsor Newington Labour Conservative Debbie ABRAHAMS MP Imran AHMAD-KHAN Oldham East and MP Saddleworth Wakefield Conservative Conservative Nigel ADAMS MP Nickie AIKEN MP Selby and Ainsty Cities of London and Westminster Conservative Conservative Bim AFOLAMI MP Peter ALDOUS MP Hitchin and Harpenden Waveney A Labour Labour Rushanara ALI MP Mike AMESBURY MP Bethnal Green and Bow Weaver Vale Labour Conservative Tahir ALI MP Sir David AMESS MP Birmingham, Hall Green Southend West Conservative Labour Lucy ALLAN MP Fleur ANDERSON MP Telford Putney Labour Conservative Dr Rosena ALLIN-KHAN Lee ANDERSON MP MP Ashfield Tooting Members of the House of Commons December 2019 A Conservative Conservative Stuart ANDERSON MP Edward ARGAR MP Wolverhampton South Charnwood West Conservative Labour Stuart ANDREW MP Jonathan ASHWORTH Pudsey MP Leicester South Conservative Conservative Caroline ANSELL MP Sarah ATHERTON MP Eastbourne Wrexham Labour Conservative Tonia ANTONIAZZI MP Victoria ATKINS MP Gower Louth and Horncastle B Conservative Conservative Gareth BACON MP Siobhan BAILLIE MP Orpington Stroud Conservative Conservative Richard BACON MP Duncan BAKER MP South Norfolk North Norfolk Conservative Conservative Kemi BADENOCH MP Steve BAKER MP Saffron Walden Wycombe Conservative Conservative Shaun BAILEY MP Harriett BALDWIN MP West Bromwich West West Worcestershire Members of the House of Commons December 2019 B Conservative Conservative -

Base Issue 3 - 3Fox International Ltd - 02 Sec01-16Pp - Back - AGFA XL105 CB Middle - JDF (Job Internal) - Blackcyanmagentayellow

−−−−−−−−−−−−−−− 3 −−−−−−−−−−−−−−− 4 −−−−−−−−−−−−−−− 5 −−−−−−−−−−−−−−− 6 −−−−−−−−−−−−−−− 7 −−−−−−−−−−−−−−− 8 −−−−−−−−−−−−−−− 9 −−−−−−−−−−−−−−− 10 −−−−−−−−−−−−−− B = B −−−−−−−−−−−−−− 12 −−−−−−−−−−−−−− C = C −−−−−−−−−−−−−− 14 −−−−−−−−−−−−− M = M −−−−−−−−−−−−− 16 WINTER 2018 WINTER 2018 ISSUE 3 ISSUE Shaping the future £1.7m has been invested in new entrances at Eastgate BASILDON · SOUTH EAST with new investment INVESTMENT AND GROWTH FOR Encompassing more than half of the retail space in the town, and with 1,350 people employed in the centre, Eastgate has consistently invested in Basildon for the benefit of the whole borough. We’ve attracted new destination retailers including Smiggle, Pandora and Accessorize - and are proud to welcome around 12 million shoppers to the centre each year. With exciting new names being lined up for 2019, including a 24-hour PureGym, we’re looking forward to a bright future. INDUSTRY OUT ON THE LESSONS FOR INNOVATIONS: TOWN: GROWTH OF LIFE: LEARNING eastgatecentre.com MODULAR HOUSING THE CENTRES AND LIVING 32 −−−−−−−−−−−−−−− 31 −−−−−−−−−−−−−−− 30 −−−−−−−−−−−−−−− 29 −−−−−−−−−−−−−−− 28 −−−−−−−−−−−−−−− 27 −−−−−−−−−−−−−−− 26 −−−−−−−−−−−−−−− 25 −−−−−−−−−−−−−−− 24 −−−−−−−−−−−−−−− 23 −−−−−−−−−−−−−−− 22 −−−−−−−−−−−−−− Z = Z −−−−−−−−−−−−−− 20 −−−−−−−−−−−−−− X = X −−−−−−−−−−−−−− 18 −−−−−−−−−−−−−− Y = Y −−−−−−−−−−−−−− 16 −−−−−−−−−−−−− M = M −−−−−−−−−−−−− 14 −−−−−−−−−−−−−− C = C −−−−−−−−−−−−−− 12 −−−−−−−−−−−−−− B = B −−−−−−−−−−−−−− 10 −−−−−−−−−−−−−−− 9 −−−−−−−−−−−−−−− 8 −−−−−−−−−−−−−−− 7 −−−−−−−−−−−−−−− 6 −−−−−−−−−−−−−−− -

Questions to the Secretary of State for Defence

Published: Friday 18 October 2019 Questions for oral answer on a future day (Future Day Orals) Questions for oral answer on a future day as of Friday 18 October 2019. T Indicates a topical question. Members are selected by ballot to ask a Topical Question. [R] Indicates that a relevant interest has been declared. Questions for Answer on Monday 21 October Oral Questions to the Secretary of State for Defence 1 Dr David Drew (Stroud): What recent assessment he has made of trends in the number of Army personnel. (900000) 2 Mr John Baron (Basildon and Billericay): What steps his Department is taking to protect UK shipping in the Strait of Hormuz. (900001) 3 Andrew Jones (Harrogate and Knaresborough): What steps his Department is taking to (a) recruit and (b) retain service personnel. (900002) 4 Robert Halfon (Harlow): What steps his Department is taking to (a) recruit and (b) retain service personnel. (900003) 5 Vicky Ford (Chelmsford): What steps his Department is taking to (a) recruit and (b) retain service personnel. (900004) 6 Bambos Charalambous (Enfield, Southgate): What recent assessment he has made of the quality of service provided under contracts outsourced by his Department. (900005) 7 Matt Western (Warwick and Leamington): What steps he is taking to support the UK defence industry. (900007) 8 Stephen Metcalfe (South Basildon and East Thurrock): What steps his Department is taking to maintain the capabilities of UK defence manufacturing. (900008) 9 Mr Steve Baker (Wycombe): What recent assessment he has made of the adequacy of the (a) capabilities and (b) strength of the armed forces. -

Has Your MP Pledged to ACT On

January 2011 Issue 6 Providing information, support and access to established, new or innovative treatments for Atrial Fibrillation Nigel Mills MP Eric Illsley MP John Baron MP David Evennett MP Nick Smith MP Dennis Skinner MP Julie Hilling MP David Tredinnick MP Amber Valley Barnsley Central Basildon and BillericayHHasBexleyheath and CrayfordaBlaenau sGwent Bolsover Bolton West Bosworth Madeleine Moon MP Simon Kirby MP Jonathan Evans MP Alun Michael MP Tom Brake MP Mark Hunter MP Toby Perkins MP Martin Vickers MP Bridgend Brighton, Kemptown Cardiff North Cardiff South and Penarth Carshalton and Wallington Cheadle Chesterfield Cleethorpes Henry Smith MP Edward Timpson MP Grahame Morris MP Stephen Lloyd MP Jo Swinson MP Damian Hinds MP Andy Love MP Andrew Miller MP Crawley Creweyyour and Nantwich oEasington uEastbournerEast Dunbartonshire MMPEast Hampshire PEdmonton Ellesmere Port and Neston Nick de Bois MP David Burrowes MP Mark Durkan MP Willie Bain MP Richard Graham MP Andrew Jones MP Bob Blackman MP Jim Dobbin MP Enfield North Enfield Southgate Foyle Glasgow North East Gloucester Harrogate and Knaresborough Harrow East Heywood and Middleton Andrew Bingham MP Angela Watkinson MP Andrew Turner MP Jeremy Wright MP Joan Ruddock MP Philip Dunne MP Yvonne Fovargue MP John Whittingdale MP High Peak Hornchurchppledged and Upminster lIsle of eWight Kenilworthd and Southam Lewishamg Deptford eLudlow dMakerfield Maldon Annette Brooke MP Glyn Davies MP Andrew Bridgen MP Chloe Smith MP Gordon Banks MP Alistair Carmichael MP Douglas Alexander MP -

Stephen Kinnock MP Aberav

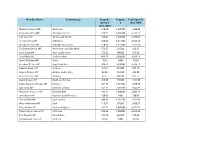

Member Name Constituency Bespoke Postage Total Spend £ Spend £ £ (Incl. VAT) (Incl. VAT) Stephen Kinnock MP Aberavon 318.43 1,220.00 1,538.43 Kirsty Blackman MP Aberdeen North 328.11 6,405.00 6,733.11 Neil Gray MP Airdrie and Shotts 436.97 1,670.00 2,106.97 Leo Docherty MP Aldershot 348.25 3,214.50 3,562.75 Wendy Morton MP Aldridge-Brownhills 220.33 1,535.00 1,755.33 Sir Graham Brady MP Altrincham and Sale West 173.37 225.00 398.37 Mark Tami MP Alyn and Deeside 176.28 700.00 876.28 Nigel Mills MP Amber Valley 489.19 3,050.00 3,539.19 Hywel Williams MP Arfon 18.84 0.00 18.84 Brendan O'Hara MP Argyll and Bute 834.12 5,930.00 6,764.12 Damian Green MP Ashford 32.18 525.00 557.18 Angela Rayner MP Ashton-under-Lyne 82.38 152.50 234.88 Victoria Prentis MP Banbury 67.17 805.00 872.17 David Duguid MP Banff and Buchan 279.65 915.00 1,194.65 Dame Margaret Hodge MP Barking 251.79 1,677.50 1,929.29 Dan Jarvis MP Barnsley Central 542.31 7,102.50 7,644.81 Stephanie Peacock MP Barnsley East 132.14 1,900.00 2,032.14 John Baron MP Basildon and Billericay 130.03 0.00 130.03 Maria Miller MP Basingstoke 209.83 1,187.50 1,397.33 Wera Hobhouse MP Bath 113.57 976.00 1,089.57 Tracy Brabin MP Batley and Spen 262.72 3,050.00 3,312.72 Marsha De Cordova MP Battersea 763.95 7,850.00 8,613.95 Bob Stewart MP Beckenham 157.19 562.50 719.69 Mohammad Yasin MP Bedford 43.34 0.00 43.34 Gavin Robinson MP Belfast East 0.00 0.00 0.00 Paul Maskey MP Belfast West 0.00 0.00 0.00 Neil Coyle MP Bermondsey and Old Southwark 1,114.18 7,622.50 8,736.68 John Lamont MP Berwickshire Roxburgh -

Committees on Arms Export Controls: Unauthorised Disclosures of Draft Report on Use of UK- Manufactured Arms in Yemen

House of Commons Foreign Affairs Committee Committees on Arms Export Controls: unauthorised disclosures of draft Report on Use of UK- manufactured arms in Yemen Seventh Special Report of Session 2016–17 Ordered by the House of Commons to be printed 10 January 2017 HC 935 Published on 18 January 2017 by authority of the House of Commons The Foreign Affairs Committee The Foreign Affairs Committee is appointed by the House of Commons to examine the expenditure, administration, and policy of the Foreign and Commonwealth Office and its associated public bodies. Current membership Crispin Blunt MP (Conservative, Reigate) (Chair) Mr John Baron MP (Conservative, Basildon and Billericay) Ann Clwyd MP (Labour, Cynon Valley) Mike Gapes MP (Labour (Co-op), Ilford South) Stephen Gethins MP (Scottish National Party, North East Fife) Mr Mark Hendrick MP (Labour (Co-op), Preston) Adam Holloway MP (Conservative, Gravesham) Daniel Kawczynski MP (Conservative, Shrewsbury and Atcham) Ian Murray MP (Labour, Edinburgh South) Andrew Rosindell MP (Conservative, Romford) Nadhim Zahawi MP (Conservative, Stratford-on-Avon) Powers The Committee is one of the departmental select committees, the powers of which are set out in House of Commons Standing Orders, principally in SO No 152. These are available on the internet via www.parliament.uk. Publication Committee reports are published on the Committee’s website at www.parliament.uk/facom and in print by Order of the House. Committee staff The current staff of the Committee are Chris Stanton (Clerk), Nick Beech (Second Clerk), Dr Ariella Huff (Senior Committee Specialist), Ashlee Godwin and Nicholas Wade (Committee Specialists), Clare Genis (Senior Committee Assistant), James Hockaday and Su Panchanathan (Committee Assistants), and Estelle Currie (Media Officer). -

Cancer Across the Domains

Cancer across the Domains Cancer priorities for the new NHS 1 The All Party Parliamentary Group on Cancer Contents The All Party Parliamentary Group on Cancer (APPGC) was founded in 1998. The group brings together MPs and Peers from across the political spectrum to campaign together to improve cancer Foreword 4 services and debate key issues affecting cancer patients and their families and carers. Executive summary 6 Currently the Officers of the group are: Cancer priorities for the new NHS 8 John Baron MP – Chairman Stephen Metcalfe MP Baroness Morgan of Drefelin Introduction 12 Grahame Morris MP Baroness Finlay of Llandaff James Clappison MP Domain 1 – Preventing people dying prematurely 15 Baroness Masham of Ilton Rt Hon Paul Burstow MP Domain 2 – Enhancing quality of life for people with long term conditions 20 Domain 3 – Helping people to recover from episodes of ill health or injury 25 The Secretariat to the All Party Parliamentary Domain 4 – Ensuring that people Group on Cancer is provided by have a positive experience of care 28 Domain 5 – Treating and caring for people in a safe environment and protecting them from avoidable harm 33 Conclusion 36 Appendix 1: Acknowledgements 38 The APPGC is also supported by a stakeholder group of organisations including Breakthrough Appendix 2: References 40 Breast Cancer, Cancer Black Care, Cancer Research UK, Prostate Cancer UK, Marie Curie Cancer Care, the Men’s Health Forum, the National Cancer Research Institute (NCRI), the National Cancer Intelligence Network (NCIN), the Teenage Cancer Trust, the Rarer Cancers Foundation and Independent Cancer Patients’ Voice. Five charities formed a Steering Group and contributed funding to the development of this report: Macmillan Cancer Support, Breakthrough Breast Cancer, Cancer Research UK, the Teenage Cancer Trust and Prostate Cancer UK. -

3. Section 13 of the European Union

3. SECTION 13 OF THE EUROPEAN UNION (WITHDRAWAL) ACT 2018 Until 7.00pm (if the Business of the House Motion is agreed to) The Prime Minister That this House, in accordance with the provisions of section 13(6)(a) and 13(11)(b)(i) and 13(13)(b) of the European Union (Withdrawal) Act 2018, has considered the Written Statement titled “Statement under Section 13(4) of the European Union (Withdrawal) Act 2018” and made on 21 January 2019, and the Written Statement titled “Statement under Section 13(11)(a) of the European Union (Withdrawal) Act 2018”and made on 24 January 2019. Amendment (a) Jeremy Corbyn Keir Starmer Emily Thornberry John McDonnell Ms Diane Abbott Mr Nicholas Brown Alex SobelStephen MorganSeema MalhotraHilary BennMatt WesternRachel ReevesHelen GoodmanLiz McInnesPeter KyleStephen DoughtyImran HussainBarry GardinerAnna McMorrinWayne DavidMr Paul SweeneyLloyd Russell- MoyleRushanara AliCatherine McKinnellEmma ReynoldsAndy SlaughterMs Karen BuckMary CreaghStella CreasyLilian GreenwoodWes StreetingBill EstersonHelen HayesStephen TwiggPhil WilsonStephen TimmsIan MurrayPreet Kaur GillGeraint DaviesRuth GeorgeMr David LammyLesley LairdDanielle RowleyDarren JonesKate GreenDaniel ZeichnerKerry McCarthyOwen SmithAnna TurleyMr Clive BettsDr Rupa HuqGed KillenGraham P JonesCatherine WestMartin WhitfieldJoan RyanSiobhain McDonaghRachael MaskellJo StevensMarsha De CordovaMr George HowarthGareth ThomasClive LewisSandy MartinKate OsamorMeg HillierMatt Rodda Line 1, leave out from “House” to end and add “requires ministers to secure sufficient -

The Implications of Cuts to the BBC World Service

House of Commons Foreign Affairs Committee The Implications of Cuts to the BBC World Service Sixth Report of Session 2010–11 Volume I: Report, together with formal minutes, oral and written evidence Additional written evidence is contained in Volume II, available on the Committee website at www.parliament.uk/facom Ordered by the House of Commons to be printed 4 April 2011 HC 849 Published on 13 April 2011 by authority of the House of Commons London: The Stationery Office Limited £14.50 The Foreign Affairs Committee The Foreign Affairs Committee is appointed by the House of Commons to examine the expenditure, administration, and policy of the Foreign and Commonwealth Office and its associated agencies. Current membership Richard Ottaway (Conservative, Croydon South) (Chair) Rt Hon Bob Ainsworth (Labour, Coventry North East) Mr John Baron (Conservative, Basildon and Billericay) Rt Hon Sir Menzies Campbell (Liberal Democrats, North East Fife) Rt Hon Ann Clwyd (Labour, Cynon Valley) Mike Gapes (Labour, Ilford South) Andrew Rosindell (Conservative, Romford) Mr Frank Roy (Labour, Motherwell and Wishaw) Rt Hon Sir John Stanley (Conservative, Tonbridge and Malling) Rory Stewart (Conservative, Penrith and The Border) Mr Dave Watts (Labour, St Helens North) The following Member was also a member of the Committee during the Parliament: Emma Reynolds (Labour, Wolverhampton North East) Powers The Committee is one of the departmental select committees, the powers of which are set out in House of Commons Standing Orders, principally in SO No 152. These are available on the Internet via www.parliament.uk. Publication The Reports and evidence of the Committee are published by The Stationery Office by Order of the House. -

Speech Day 2019

Speech Day 2019 Guest of Honour: John Baron MP Thursday 4th July 2019 Thursday 4th JulyOrder o� Events 10.00 am Speeches and Prizegiving in the Marquee followed by light refreshments in the Sixth Form Centre Guest o� Honour: John Baron MP John Baron was a student at Queen’s from 1975–77 and then studied Law, History and Politics at Cambridge. He joined the Royal Regiment of Fusiliers, serving in Berlin, Northern Ireland and Cyprus. Upon leaving the Army in 1988, he became a Director of Hendersons and then Rothschild Asset Management, specialising as a fund manager in charities and private clients. John was elected MP for Billericay and District in 2001. He resigned as a Shadow Health Minister in 2003 to vote against the Iraq war, and has opposed interventions in Afghanistan, Libya and Syria. John has served as the Chairman of the All-Party Parliamentary Group (APPG) on Cancer, sat on the Foreign Affairs Select Committee, and is presently Chairman of the British Council APPG. John founded the charity ‘The Fun Walk Trust’, which has raised over £1,000,000 for good causes since 2002. Since leaving the City in 2001, John has helped charities monitor their fund managers, regularly writes on investment issues, and has also founded a business reporting on investment trusts. School Prizes 2019 Year 7 – Academic Merit and Contribution to the School Prizes You You Chin Eloise Hill Archie Ledger-Wielkopolski Hugh Pluckwell Rosie Seddon Ben Seddon Greta Siakoufis Year 8 – Academic Merit and Contribution to the School Prizes Emily Davies Rosie East