Appendix 1 Draft Statement of Accounts , Item 9. PDF 547 KB

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FOI 114/11 Crimes in Schools September 2010 – February 2011

FOI 114/11 Crimes in Schools September 2010 – February 2011 Incident Premisies Name Town / City Current Offence Group Count Abbeywood Community School Bristol Theft And Handling Stolen Goods 4 Alexandra Park Beechen Cliff School Bath Criminal Damage 1 Alexandra Park Beechen Cliff School Bath Theft And Handling Stolen Goods 4 Alexandra Park Beechen Cliff School Bath Violence Against The Person 1 Allen School House Bristol Theft And Handling Stolen Goods 0 Archbishop Cranmer Community C Of E School Taunton Burglary 1 Ashcombe Cp School Weston-Super-Mare Theft And Handling Stolen Goods 2 Ashcombe Primary School Weston-Super-Mare Violence Against The Person 0 Ashcott Primary School Bridgwater Theft And Handling Stolen Goods 0 Ashill Primary School Ilminster Theft And Handling Stolen Goods 1 Ashley Down Infant School Bristol Theft And Handling Stolen Goods 2 Ashton Park School Bristol Other Offences 1 Ashton Park School Bristol Sexual Offences 1 Ashton Park School Bristol Theft And Handling Stolen Goods 1 Avon Primary School Bristol Burglary 2 Backwell School Bristol Burglary 3 Backwell School Bristol Theft And Handling Stolen Goods 1 Backwell School Bristol Violence Against The Person 1 Badminton School Bristol Violence Against The Person 0 Banwell Primary School Banwell Theft And Handling Stolen Goods 1 Bartletts Elm School Langport Criminal Damage 0 Barton Hill County Infant School & Nursery Bristol Burglary 1 Barton Hill Primary School Bristol Violence Against The Person 0 Barwick Stoford Pre School Yeovil Fraud Forgery 1 Batheaston Primary -

Employers and Contribution Rates 2019

Employer Contribution Rates Participating Employers 2018/19 Employer Year Ended 31 March 2019 2018/19 Employee % of contributions plus contributions pay Deficit / (surplus) amount Scheduled Bodies Principal Councils and Service Providers Avon Fire & Rescue Service £309,067 14.7 £370,700 Bath & North East Somerset Council n.b. includes St Gregory’s £3,795,316 15.2 - City of Bristol Council £11,109,984 15.0 - North Somerset Council £2,498,941 15.2 £4,212,460 South Gloucestershire Council £5,478,268 15.5 - West of England Combined Authority £230,100 13.0 - Further & Higher Education Establishments Bath Spa University £912,596 13.8 £702,700 Bath College £179,576 14.6 £166,600 City of Bristol College £395,295 15.5 £594,700 South Gloucestershire & Stroud College £539,122 13.6 £453,300 St. Brendan's Sixth Form College £97,531 14.9 - University of the West of England £3,886,547 14.2 £2,441,660 Weston College n.b. includes Offender Learning Service £543,923 13.1 £347,240 Academies and Schools Abbeywood Community School £52,431 15.1 £41,900 Abbot Alphege Academy £2,239 20.0 - Ashcombe Primary School £42,761 14.8 £76,800 Ashton Park School £42,454 16.2 £51,675 Ashton Vale Primary School £7,869 17.7 £10,800 Aspire Academy £20,207 12.9 £39,340 Backwell C of E Junior School £8,190 21.7 £13,400 Backwell School £72,980 17.1 £157,100 Badock's Wood E-ACT Academy £9,833 14.0 £11,783 Bannerman Road Community Academy £20,409 13.5 £20,700 Barton Hill Academy £30,900 12.9 £26,200 Bathampton Primary School £9,881 18.9 £12,000 Batheaston Church School £12,462 -

Local Sustainable Transport Fund 15/16 Revenue Application Form

Local Sustainable Transport Fund 15/16 Revenue Application Form Applicant Information Local transport authority name(s): Bath and North East Somerset, Bristol (Lead), North Somerset and South Gloucestershire If the bid is a joint proposal, please enter the names of all participating local transport authorities and specify the lead authority Bid Manager Name and position: Andrew Whitehead, LSTF Programme Manager Contact telephone number: 0117 903 6371 Email address: [email protected] Postal address: Brunel House, St George’s Road, Bristol BS1 5UY Website address for published bid: www.travelwest.info/lstf SECTION A - Project description and funding profile A1. Project name: Travel WEST A2. Headline description: Travel WEST builds on the successful LSTF WEST programme with a package focussed around the Enterprise Areas across the West of England. We will use established partnerships with business and wider stakeholders to continue to transform the travel opportunities for people living and working in our economic centres. We have reviewed what has worked so far in our LSTF programme and listened to voices of businesses to understand what we need to focus on next. The programme ties up with the allocation of further capital from the Strategic Economic Plan focussed on strategic walking, cycling and public transport infrastructure. 2015/16 is an exciting period of change with growth in homes and jobs, and construction of several major capital programmes underway on our networks. The programme within this bid seeks to accommodate this change and, more importantly, to seize on it as an opportunity to change and embed new travel habits. A3. -

Secondaryschoolspendinganaly

www.tutor2u.net Analysis of Resources Spend by School Total Spending Per Pupil Learning Learning ICT Learning Resources (not ICT Learning Resources (not School Resources ICT) Total Resources ICT) Total Pupils (FTE) £000 £000 £000 £/pupil £/pupil £/pupil 000 Swanlea School 651 482 1,133 £599.2 £443.9 £1,043.1 1,086 Staunton Community Sports College 234 192 426 £478.3 £393.6 £871.9 489 The Skinners' Company's School for Girls 143 324 468 £465.0 £1,053.5 £1,518.6 308 The Charter School 482 462 944 £444.6 £425.6 £870.2 1,085 PEMBEC High School 135 341 476 £441.8 £1,117.6 £1,559.4 305 Cumberland School 578 611 1,189 £430.9 £455.1 £885.9 1,342 St John Bosco Arts College 434 230 664 £420.0 £222.2 £642.2 1,034 Deansfield Community School, Specialists In Media Arts 258 430 688 £395.9 £660.4 £1,056.4 651 South Shields Community School 285 253 538 £361.9 £321.7 £683.6 787 Babington Community Technology College 268 290 558 £350.2 £378.9 £729.1 765 Queensbridge School 225 225 450 £344.3 £343.9 £688.2 654 Pent Valley Technology College 452 285 737 £339.2 £214.1 £553.3 1,332 Kemnal Technology College 366 110 477 £330.4 £99.6 £430.0 1,109 The Maplesden Noakes School 337 173 510 £326.5 £167.8 £494.3 1,032 The Folkestone School for Girls 325 309 635 £310.9 £295.4 £606.3 1,047 Abbot Beyne School 260 134 394 £305.9 £157.6 £463.6 851 South Bromsgrove Community High School 403 245 649 £303.8 £184.9 £488.8 1,327 George Green's School 338 757 1,096 £299.7 £670.7 £970.4 1,129 King Edward VI Camp Hill School for Boys 211 309 520 £297.0 £435.7 £732.7 709 Joseph -

Understanding Access in Schools to Mental Health Support 2019

Understanding access to mental health support through school & college June 2019 1 Page Healthwatch North Somerset: Mental Health & Young People Healthwatch North Somerset is a charity (No: 1158487) and a company limited by guarantee (England and Wales No: 08187141). Registered office 3rd Floor, The Sion, Crown Glass Place, Nailsea BS48 1RB About us Healthwatch is a national network of organisations that provide a voice to people who use health and social care. We have significant statutory powers to ensure views and experiences are strengthened and heard by those who commission, plan, deliver and regulate health and care services. Healthwatch North Somerset actively captures the views of the public using various outreach methods. Our mission statement is ‘By offering all people if North Somerset a strong voice, we will improve the quality of local health and social care.’ Our statutory duty and remit is laid out in The Health and Social Care Act 2012 to give people an opportunity to have a say, including those whose voice isn’t usually heard. We take public views to the decision makers locally– including North Somerset’s People and Communities/Health and Wellbeing Board. We also feed issues back to government by sending them to NHS England, Healthwatch England &the Care Quality Commission (CQC). 2 Page Healthwatch North Somerset: Mental Health & Young People Healthwatch North Somerset is a charity (No: 1158487) and a company limited by guarantee (England and Wales No: 08187141). Registered office 3rd Floor, The Sion, Crown Glass Place, Nailsea BS48 1RB Introduction The evaluation was carried out with the sole purpose of exploring the current situation for children and young people (CYP) seeking early intervention mental health help through their schools and colleges, and their access to other services outside school. -

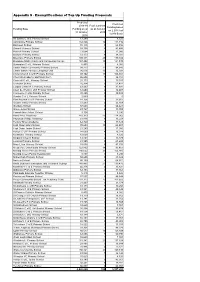

Appendix 5 - Exemplifications of Top up Funding Proposals

Appendix 5 - Exemplifications of Top Up Funding Proposals Predicted Predicted 2018-19 Pupil numbers Funding based Funding Base Funding as at as at Autumn on 2.03% trsf 31 October 2018 to HN Block 2018 All Saints C of E Primary School 13,289 1 8,525 Ashcombe Primary School 132,826 16 114,716 Backwell School 74,118 9 64,856 Banwell Primary School 58,336 8 41,486 Becket Primary School 23,084 3 17,080 Birdwell Primary School 51,173 6 38,031 Bournville Primary School 199,141 28 179,182 Broadoak Mathematics and Computing College 167,492 15 121,538 Burrington C of E Primary School 6,405 1 4,082 Castle Batch Community Primary School 98,272 11 94,640 Castle Batch Primary Language Unit 36,076 15 15,031 Christ Church C of E Primary School 93,462 13 108,464 Churchill Academy and Sixth Form 46,654 7 36,151 Churchill C of E Primary School 25,173 3 19,357 Clevedon School 76,914 9 51,422 Corpus Christi R C Primary School 43,433 6 37,691 Court de Wyck C of E Primary School 12,600 2 12,607 Crockerne C of E Primary School 35,268 5 30,885 Dundry C of E Primary School 2,669 0 0 Flax Bourton C of E Primary School 14,356 2 12,607 Golden Valley Primary School 37,403 4 23,949 Gordano School 57,638 8 56,623 Grove Junior School 43,727 6 35,059 Hannah More Infant School 9,724 1 5,290 Hans Price Academy 210,323 20 174,965 Haywood Village Academy 41,818 6 33,248 Herons' Moor Academy 62,720 7 47,429 High Down Infant School 70,603 10 64,407 High Down Junior School 21,240 2 17,050 Hutton C of E Primary School 24,669 4 16,328 Kewstoke Primary School 10,620 1 8,525 Kingshill -

Employer Contribution Rates

Employer Contribution Rates Participating Employers Contribution Rates Year Ended 31 March 2018 2017/18 2016/17 Active Deficit / Surplus Deficit / Surplus % % membership Amount Amount Scheduled Bodies Principal Councils and Service Providers Avon Fire & Rescue Service 206 14.2 £357,000 13.6 £343,300 Bath & North East Somerset Council 3154 14.7 £15,400,700 14.2 - City of Bristol Council 8902 14.5 £44,183,400 14 - North Somerset Council 2395 14.7 £4,813,930 14.2 £5,412,400 South Gloucestershire Council 5860 15.0 £17,317,600 14.5 - West of England Combined Authority 41 13.0 - - - Further & Higher Education Establishments Bath Spa University 1118 13.8 £646,200 13.7 £589,800 Bath College 218 14.6 £155,700 13.3 £101,700 City of Bristol College 346 15.0 £558,000 14.4 £521,300 South Gloucestershire & Stroud College 519 13.1 £436,600 12.6 £419,900 St. Brendan's Sixth Form College 84 14.3 £122,300 13.8 £39,500 University of the West of England 2149 14.0 £2,286,930 13.5 £2,178,600 Weston College 342 13.1 £308,190 12.6 £275,000 Academies and Schools Abbeywood Community School 56 15.1 £40,400 14.4 £43,500 Abbot Alphege Academy 5 20.0 - - - Ashcombe Primary School 78 14.8 £43,200 - - Aspire Academy 24 12.9 £37,970 14.6 £37,300 Backwell C of E Junior School 10 21.7 £2,133 - - Backwell School 64 16.7 £140,800 16.2 £124,400 Bannerman Road Community Academy 44 13.2 £20,000 12.7 £19,200 Barton Hill Academy 42 12.4 £25,300 11.9 £24,300 Bath Community Academy 17 14.1 £27,500 13.6 £27,000 Bathampton Primary School 31 18.9 £1,000 - - Batheaston Church School -

NSC Minutes Table

People and Communities Strategic Schools Forum Wednesday 25th November 2020 09:30am, Microsoft Teams Member Title P – Present S – Substitute A - Apologies ACADEMY REPRESENTATIVES - vote LOUISE MALIK Chief Financial and Operating Officer, Lighthouse P Schools Partnership ANDREW BERRY Academy Headteacher, Churchill Academy & Sixth P Form (ON BEHALF OF CHRIS HILDREW) WILLIAM HARDING Academy Governor/Trustee of North Somerset P School in Bristol-based Cathedral School Trust TONY SEARLE Academy Headteacher, Hans Price Academy A MARK ANTOINE Academy representative – Chief Operations Officer P ADAM MATTHEWS Academy CEO, Extended Learning Academies P Network JACQUI SCOTT Academy Head Teacher, Worle Community School P - Kaleidoscope STEPHEN WEBBER Academy Headteacher, Clevedon Learning Trust A STEVE DAVIS Academy Governor, Head of Parklands Educate A Together and Chair of PHANS MAINTAINED SCHOOLS HEADTEACHERS - vote SARAH HARDING Primary Headteacher Kewstoke P TRACEY TOWLER Special School Headteacher Westhaven School P EMMA GUNDRY PRU Principal, Voyage Learning Campus P MAINTAINED SCHOOLS GOVERNORS (PRIMARY) - vote WENDY FARRIER Maintained School Representative – Primary A Governor (Churchill Primary) NON-SCHOOLS MEMBERS JOHN SIMPSON Independent Community Representative, Chair P CLLR CATHERINE Executive Member for Children and Young Peoples A GIBBONS Services CLLR WENDY GRIGGS Chair of CYP Policy and Scrutiny Panel P 1 CLAIRE HUDSON Diocese of Bath and Wells A PAUL TRAUBERMAN Early Years – Rainbow Smiles Nursery P KAREN WORTHINGTON 14 – 19 – Weston -

Prospectus for School Leavers 2019/20

PROSPECTUS FOR SCHOOL LEAVERS 2019/20 BRINGING OUT YOUR BEST www.btc.ac.uk PROSPECTUS FOR SCHOOL LEAVERS 2019/20 WELCOME CONTENTS College Life 2 VOCATIONAL COURSES GET IN TOUCH Fantastic Facilities 8 Agriculture 54 Write, email or visit us - we’re always College Academies 16 Animal Care & Management 60 happy to talk to you. University Centre Somerset 19 Applied Science 65 I am delighted to be reading this prospectus at the Choose the Right Course 20 Arboriculture 67 Information, Advice & Guidance Your Educational Journey 24 Art, Design & Media 69 01278 441234 beginning of what is my second year as Principal & Routes to Success 26 Automotive 79 [email protected] Chief Executive at Bridgwater & Taunton College. My BTC Advantage 28 Barbering 87 www.btc.ac.uk Supporting your Learning 30 Beauty & Complementary Therapies 89 The Application Process 32 Business 93 Bridgwater Campus As I read the case studies I was particularly struck by the amazing stories from our Getting Here 34 Children’s Care, Play, Learning Bath Road students, in particular Toby Pitman who said, “I was quite nervous at the start of the A Levels 36 & Development 97 Bridgwater TA6 4PZ course, but as I’ve progressed it has dawned on me that not only am I achieving what A Level Results 45 Computing & Games Technology 101 01278 455464 I thought was impossible, I have the biggest smile on my face”. I think this can be International Baccalaureate Construction 106 said for all of us when we start off at College, whether you’re a new student or a new Diploma Programme 46 Countryside Management 117 Taunton Campus member of staff, it can be quite daunting. -

People and Communities Strategic Schools Forum

People and Communities Strategic Schools Forum 25 November 2020 9:30am via MSTeams Agenda Action Lead Apologies and Declarations of Interest - SSF 1. 9:30 members are reminded that they need to declare an John Simpson interest in any item that is on the agenda 2. 9:35 Minutes of the previous meeting John Simpson Matters arising – not on the agenda 3. 9:40 John Simpson Notification of AOB - Chair’s Business 4. 9:40 John Simpson • None -expected Governance: 5. 9:45 Information Emma Whitehead • None - expected Finance Report, incorporating: 6. 9:45 • Monitoring Report for 2020-21 Decision Emma Whitehead • 2021/22 DSG and Schools Budget 7. 10:30 Education Inclusion Service – Information Wendy Packer 8. 10:45 Evaluation of meeting – Date of next meeting- 20 January 2021 – MSTeams Papers will be issued on Wednesday 13 January 2021 where possible. People and Communities Strategic Schools Forum Wednesday 7th October 2020 09:30am, Microsoft Teams Member Title P – Present S – Substitute A - Apologies ACADEMY REPRESENTATIVES - vote LOUISE MALIK Chief Financial and Operating Officer, Lighthouse P Schools Partnership CHRIS HILDREW Academy Headteacher, Churchill Academy & Sixth P Form WILLIAM HARDING Academy Governor/Trustee of North Somerset P School in Bristol-based Cathedral School Trust TONY SEARLE Academy Headteacher, Hans Price Academy P MARK ANTOINE Academy representative – Secondary Business P Manager/Chief Operations Officer ADAM MATTHEWS Academy CEO, Extended Learning Academies P Network JACQUI SCOTT Academy Head Teacher, Worle Community -

Inside This Issue a Wonderful Job Leading the Upper School and We Are Welcome Messages 3 Studies 20 Always on Hand to Talk to Any Parents / Carers at Any Time

WORLE COMMUNITY SCHOOL THE PRIORY @Wcsa LEARNING TRUST WORLE COMMUNITY SCHOOL MAGAZINE An Academy CHRISTMAS EDITION 2018 PRInCIPAL’s POst I also enjoyed the two celebration evenings that took place in the Autumn Term. We said well done to Dear Parents and Carers, students on The Grand Pier back in October. It was lovely to see so many of our ex Year 11s and hear about the success they are making of their lives. In November, Welcome to the Autumn / we celebrated with our lower school students here at Winter Newsletter 2018. WCSA, which was another lovely evening. I have been As usual, we have packed a lot enjoying my hot chocolate break times with students into the last 15 weeks. The who consistently get a high number of achievement two-week October half term points. Don’t forget, we reset behaviour and achievement seems like a long way away points at the start of each Learning Cycle. We have 4 now. Personally, I made the Learning Cycles in each school year. most of an opportunity to get a way for a few days. I hope that Finally, I do hope that you enjoy reading this newsletter. parents managed to get some cheaper deals and enjoyed We are always aiming to improve our communication the break to the long winter term; the two week break and to take on board ideas from parents and carers. will remain a firm feature of the way we structure our Certainly, some of our best ideas come from you. term dates here at WCSA. -

Eligible If Taken A-Levels at This School (Y/N)

Eligible if taken GCSEs Eligible if taken A-levels School Postcode at this School (Y/N) at this School (Y/N) 16-19 Abingdon 9314127 N/A Yes 3 Dimensions TA20 3AJ No N/A Abacus College OX3 9AX No No Abbey College Cambridge CB1 2JB No No Abbey College in Malvern WR14 4JF No No Abbey College Manchester M2 4WG No No Abbey College, Ramsey PE26 1DG No Yes Abbey Court Foundation Special School ME2 3SP No N/A Abbey Gate College CH3 6EN No No Abbey Grange Church of England Academy LS16 5EA No No Abbey Hill Academy TS19 8BU Yes N/A Abbey Hill School and Performing Arts College ST3 5PR Yes N/A Abbey Park School SN25 2ND Yes N/A Abbey School S61 2RA Yes N/A Abbeyfield School SN15 3XB No Yes Abbeyfield School NN4 8BU Yes Yes Abbeywood Community School BS34 8SF Yes Yes Abbot Beyne School DE15 0JL Yes Yes Abbots Bromley School WS15 3BW No No Abbot's Hill School HP3 8RP No N/A Abbot's Lea School L25 6EE Yes N/A Abbotsfield School UB10 0EX Yes Yes Abbotsholme School ST14 5BS No No Abbs Cross Academy and Arts College RM12 4YB No N/A Abingdon and Witney College OX14 1GG N/A Yes Abingdon School OX14 1DE No No Abraham Darby Academy TF7 5HX Yes Yes Abraham Guest Academy WN5 0DQ Yes N/A Abraham Moss Community School M8 5UF Yes N/A Abrar Academy PR1 1NA No No Abu Bakr Boys School WS2 7AN No N/A Abu Bakr Girls School WS1 4JJ No N/A Academy 360 SR4 9BA Yes N/A Academy@Worden PR25 1QX Yes N/A Access School SY4 3EW No N/A Accrington Academy BB5 4FF Yes Yes Accrington and Rossendale College BB5 2AW N/A Yes Accrington St Christopher's Church of England High School