Growth Equity Gains Traction with Lps

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Offering Statement for Fintron LLC (“Fintron”)

Offering Statement for FinTron LLC (“FinTron”) T his document is generated by a website that is operated by Netcapital Systems LLC ("Netcapital"), which is not a registered broker-dealer. Netcapital does not give investment advice, endorsement, analysis or recommendations with respect to any securities. All securities listed here are being offered by, and all information included in this document are the responsibility of, the applicable issuer of such securities. Netcapital has not taken any steps to verify the adequacy, accuracy or completeness of any information. Neither Netcapital nor any of its officers, directors, agents and employees makes any warranty, express or implied, of any kind whatsoever related to the adequacy, accuracy or completeness of any information in this document or the use of information in this document. All Regulation CF offerings are conducted through Netcapital Funding Portal Inc. ("Portal"), an affiliate of Netcapital, and a FINRA/SEC registered funding-portal. For inquiries related to Regulation CF securities activity, contact Netcapital Funding Portal Inc.: Paul Riss: [email protected] Netcapital and Portal do not make investment recommendations and no communication, through this website or in any other medium, should be construed as a recommendation for any security offered on or off this investment platform. Equity crowdfunding investments in private placements, Regulation A, D and CF offerings, and start-up investments in particular are speculative and involve a high degree of risk and those investors who cannot afford to lose their entire investment should not invest in start-ups. Companies seeking startup investments through equity crowdfunding tend to be in earlier stages of development and their business model, products and services may not yet be fully developed, operational or tested in the public marketplace. -

Agenda Are for Discussion and Possible Action by the Board of Directors of the Nevada Capital Investment Corporation (NCIC) Unless Otherwise Noted

Dan Schwartz State Treasurer STATE OF NEVADA OFFICE OF THE STATE TREASURER NOTICE OF PUBLIC MEETING THE NEVADA CAPITAL INVESTMENT CORPORATION BOARD OF DIRECTORS Thursday, May 4, 2017 at 1:30 p.m. Locations: Via videoconference at the following locations: Old Assembly Chambers Capitol Building, Second Floor Grant Sawyer State Office Building 101 N. Carson Street 555 E. Washington Avenue, Suite 5100 Carson City, NV 89701 Las Vegas, NV 89101 Meeting via teleconference available at the: 877.873.8017 Access Code: 5707654# All items listed on this agenda are for discussion and possible action by the Board of Directors of the Nevada Capital Investment Corporation (NCIC) unless otherwise noted. Action may consist of any of the following: approve, deny, condition, hold, or table. NOTE: Public Comment may not be limited based on viewpoint AGENDA 1) Call to Order (Chair Schwartz) 2) Roll Call (Budd Milazzo) 3) Public comment. Comments from the public are invited at this time prior to the commencement of possible action items. The Board reserves the right to limit the amount of time that will be allowed for each individual to speak. The Board is precluded from acting on items raised during Public Comment that are not on the agenda. 4) For possible action: Approval of November 17, 2016 meeting minutes (Budd Milazzo) 5) For possible action: Board review and discuss an investment in an operating agreement with Accion, LLC. to assist the Permanent School Fund in increasing its yield while supporting micro- lending in Nevada. (Greg Henderson, Accion) CARSON CITY OFFICE STATE TREASURER PROGRAMS LAS VEGAS OFFICE State Treasurer Millennium Scholarship Program 555 E. -

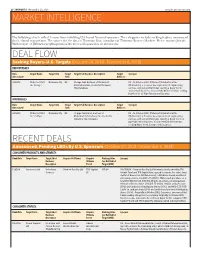

Market Intelligence

26 | BUYOUTS | November 19, 2018 www.buyoutsnews.com MARKET INTELLIGENCE The following charts reflect transactions involving U.S.-based financial sponsors. The categories include seeking buyers, announced deals, closed transactions. The source for the data is Thomson One, a product of Thomson Reuters Markets. Please contact Joseph Weitemeyer at [email protected] with questions or comments. DEAL FLOW Seeking Buyers–U.S. Targets (October 24, 2018 - November 6, 2018) INDUSTRIALS Date Target Name Target City Target Target Full Business Description Target Synopsis Announced State Advisors 10/30/18 Mcdermott Intl Delaware City DE Storage tank business of Mcdermott - US - In October 2018, McDermott International Inc Inc-Storage International Inc, located in Delaware (McDermott), a Houston-based provider of engineering City, Delaware. services, announced that it was seeking a buyer for its storage tank business. Concurrently McDermott was seeking buyer for its US Pipe Fabrication Business. MATERIALS Date Target Name Target City Target Target Full Business Description Target Synopsis Announced State Advisors 10/30/18 Mcdermott Intl Delaware City DE Us pipe fabrication business of - US - In October 2018, McDermott International Inc Inc-US Pipe Mcdermott International Inc, located in (McDermott), a Houston-based provider of engineering Delaware City, Delaware. services, announced that it was seeking a buyer for its us pipe fabrication business. Concurrently McDermott was seeking buyer for its Storage Tank Business. RECENT DEALS Announced, -

Los Angeles County Venture Capital Firms

Los Angeles County Venture Capital Firms Ad-Ventures, LLC. Alcatel Ventures Ambient Capital Arcturus Capital Aurora Capital Group Baroda Ventures, LLC. Bastion Capital Corporation Brentwood Associates California Technology Ventures, LLC Caltius Private Equity Celerity Partners Century Park Capital Partners, L.P. Chanin Capital Partners Clarity Partners, L.P. Clearstone Venture Partners Colony Capital, LLC Digital Coast Ventures Corporation DynaFund Ventures EastWest VentureGroup Entertainment Media Ventures, LLC. Finaventures Freeman Spogli & Co. Fulcrum Capital Group, LLC. Funk Ventures, Inc. GKM Venture Partners GRP Partners Hitachi Corporate Ventures Catalyst Fund Huntington Holdings, Inc. Idealflow Angel Fund LLC. ITU Ventures J.F. Shea Venture Capital Kline Hawkes & Co. Leonard Green & Partners, L.P. Levine Leichtman Capital Partners, Inc. Millennium Hanson Myers Capital Partners, LLC Oaktree Capital Management, LLC Omninet Capital, LLC P & M Investments 1 Pacific Venture Group, L.P. Palomar Ventures PCRS Capital Partners, LLC Putnam Lovell Capital Partners, Inc. Ridgestone Corporation Rolling Oaks Capital Rustic Canyon Ventures Saber Capital, LLC Seidler Equity Partners, LP Shamrock Holdings, Inc. Shelter Capital Partners, LLC Smart Technology Ventures St. Cloud Capital, LLC Steamboat Ventures, LLC Stone Canyon Venture Partners, LP SunAmerica Ventures TCW/Crescent Mezzanine, LLC TI Capital Ad-Ventures, LLC. Description: As both an investor and an entrepreneurial force, adventures seeks to infuse it’s financial and managerial knowledge -

Anderson School of Management University of California Los Angeles

presents mbaMission’s Insider’s Guide Anderson School of Management University of California Los Angeles 2016–2017 mbaMission can help you stand out among the thousands of MBA applicants! World’s Leading MBA Admissions Consulting Firm Our dedicated, full-time Senior Consultants work one-on-one with business school candidates to identify and showcase their strongest attributes in their applications. Free 30-Minute Consultation Visit www.mbamission.com/consult to start getting answers to all your MBA application and admissions questions! mbaMission Resources Check out our blog for essay writing and application tips, MBA news, professor profiles, business school facts, essay analyses, and more! Every candidate has a story to tell. We have the creative experience to help you tell yours best. mbamission.com [email protected] THE ONLY MUST-READ BUSINESS SCHOOL WEBSITE Oering more articles, series and videos on MBA programs and business schools than any other media outlet in the world, Poets&Quants has established a reputation for well-reported and highly-creative stories on the things that matter most to graduate business education prospects, students and alumnus. New and improved responsive website coming soon! MBA Admissions Specialized Master’s preMBA Networking Consultant Directory Directory Festival Poets&Quants’ MBA Admissions For graduate business degree Exclusively for students admitted Consultant Directory offers future seekers looking for a specializa- to a top business school, we applicants the opportunity to find tion along with or apart from an offer Poets&Quants’ preMBA a coach or consultant to assist in MBA, Poets&Quants' Special- Networking Festival. This is a their candidacy into a top ized Master's Directory helps new admit’s chance to get ahead business school. -

Panelist & Moderator Biographies

PANELIST & MODERATOR BIOGRAPHIES TABLE OF CONTENTS Guy Broadbent ...........................................................................................1 Morgan Burns ..............................................................................................2 Andy Cantwell ............................................................................................3 Angie Castille ..............................................................................................4 Michael Clausman ......................................................................................5 Chrisanne Corbett ....................................................................................6 Chad Cornell ...............................................................................................7 Michael Dillahunt .......................................................................................8 Robin Engelson ...........................................................................................9 Bruce Engler ..............................................................................................10 James Frommelt ......................................................................................11 Carl Genberg ............................................................................................12 Pat Goy .......................................................................................................13 Jason Grais .................................................................................................14 -

Supporting Commercial Space Development Part 1

Supporting Commercial Space Development Supporting Commercial Space Development Part 1: Support Alternatives versus Investor Risk Perceptions & Tolerances November 2010 This report, “Supporting Commercial Space Development Part 1: Support Alternatives versus Investor Risk Perceptions & Tolerances” was developed with government funding under Contract Order Number NNH11CD08D awarded by the National Aeronautics and Space Administration and may be released by NASA in whole or in part. The views expressed in this report are those of Near Earth LLC and may not reflect the views of the National Aeronautics and Space Administration or the United States Government. Part 1 1 of 228 Supporting Commercial Space Development “When a new frontier is opened, the new territory always looks vast, empty, hostile, and unrewarding. It is always dangerous to go there, and almost impossible to live there in loneliness and peril. The technological capacities of the time are always taxed to the utmost in dealing with the new environment. The explorations require huge investments of both public and private funds, and the returns are always hazardous at first…The organization, capital, and equipment required for the first exploratory efforts are so large that people tend at first to think only in terms of governmental and military actions; and only later do they conceive the new territory as simply an extension of their present territory and their present economy….an effort of prophetic imagination is what is required of us as citizens, so that we will not…leave the making of the future to others.” - Ralph J. Cordiner, Chairman of General Electric Company, 1961 CONTACT INFORMATION For parties wishing to learn more about the report described herein, additional information can be made available. -

Preqin Private Equity Benchmarks: Venture Capital Benchmark Report

Preqin Private Equity Benchmarks: Venture Capital Benchmark Report As of 31st December 2013 alternative assets. intelligent data. Preqin Private Equity Benchmarks: Venture Capital Benchmark Report As of 31st December 2013 Report Produced on 21st July 2014 This publication is not included in the CLA Licence so you must not copy any portion of it without the permission of the publisher. All rights reserved. The entire contents of the report are the Copyright of Preqin Ltd. No part of this publication or any information contained in it may be copied, transmitted by any electronic means, or stored in any electronic or other data storage medium, or printed or published in any document, report or publication, without the express prior written approval of Preqin Ltd. The information presented in the report is for information purposes only and does not constitute and should not be construed as a solicitation or other offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction, or as advice of any nature whatsoever. If the reader seeks advice rather than information then he should seek an independent fi nancial advisor and hereby agrees that he will not hold Preqin Ltd. responsible in law or equity for any decisions of whatever nature the reader makes or refrains from making following its use of the report. While reasonable efforts have been used to obtain information from sources that are believed to be accurate, and to confi rm the accuracy of such information wherever possible, Preqin Ltd. Does not make any representation or warranty that the information or opinions contained in the report are accurate, reliable, up-to-date or complete. -

University of California Regents' Interest in the Partnership As Determined by the General Partners

The Regents of the University of California Alternative Investments as of September 30, 2005 Since inception in 1979 through September 30, 2005, the Private Equity portfolio has consisted of $3.3 billion in commitments to 141 partnerships. As of September 30, 2005, $2.0 billion of these commitments have been called by the partnerships and $3.4 billion of distributions have been received from the partnerships. Including the Current Net Asset Value of $918 million as of September 30, 2005, the Private Equity portfolio has produced $2.3 billion in profits and a 2.2x multiple on contributed capital. The Private Equity portfolio has generated a total return of 27.6% for the 10-year period ended September 30, 2005. Since the beginning of 2001, Cambridge Associates, LLC (“CA”) has been retained by The Regents of the University of California (“The Regents”) to advise on the Private Equity portfolio and to calculate the Net Internal Rate of Return (“IRR”) for each partnership held in the Private Equity portfolio. Prior to the engagement of CA, the Office of the Treasurer did not calculate IRRs for individual partnerships. The historical returns for all portfolios reported by the Regents and the Office of the Treasurer are based on the annualized Total Returns methodology. Total Return calculations are based on the changing value of a portfolio and any cash flows received during the specified time period. The Private Equity portfolio was historically less than 2% of the total investment portfolio; therefore, The Regents evaluated the portfolio in its entirety and as part of the total equity portfolio. -

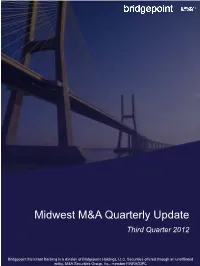

Midwest M&A Quarterly Update

Midwest M&A Quarterly Update Third Quarter 2012 Bridgepoint Merchant Banking is a division of Bridgepoint Holdings, LLC. Securities offered through an unaffiliated entity, M&A Securities Group, Inc., member FINRA/SIPC Third Quarter 2012 Midwest M&A Quarterly Update Bridgepoint Midwest M&A Index Bridgepoint Midwest M&A Index Decreased Slightly in Q3-12 . Index Summary: The Bridgepoint Midwest M&A Index, a measure of corporate merger and acquisition activity in the U.S. Midwest region, decreased 1.6% in Q3-12 after increasing 3.3% and 18.7% in Q2-12 and Q1-12, respectively. On a year- over-year basis, the index increased 18.7% from Q3- 11. The latest decrease put the index at 117.9 (Q3- 06=100), slightly lower from the previous high of 119.5 in Q2-12 . Perspective: Index reflects relatively continued elevated level of Midwest M&A deal volumes in the face of a downward trend in the U.S. M&A environment (according to Pitchbook, U.S. private equity deals decreased 10.0% in Q3). Current index . What the Index Means for You: Deal volumes level of 117.9 continues to reflect the relative remain healthy, with higher median M&A valuations strength of the Midwest deal environment in 2012 as and deal size. The current environment represents the index increased 18.7%, 22.0% and 17.1% on a an attractive opportunity for Midwest companies and year-over-year basis in the first three quarters of the business owners to: year. In addition, median Midwest M&A deal size Evaluate strategic options & your company and valuation (on a TEV/EBITDA basis) also value – Midwest companies are receiving increased from $14.9mm and 8.5x in Q2-12 to strong M&A interest from both sponsors and $17.6mm and 9.7x in Q3-12, respectively other corporates with performing companies garnering premium valuations . -

Venture Benchmark Report

Preqin Private Equity Benchmarks: Venture Benchmark Report As of 30 September 2009 Preqin Private Equity Benchmarks: Venture Benchmark Report As of 30th September 2009 Report Produced on 9th March 2010 This publication is not included in the CLA Licence so you must not copy any portion of it without the permission of the publisher. All rights reserved. The entire contents of the report are the Copyright of Preqin Ltd. No part of this publication or any information contained in it may be copied, transmitted by any electronic means, or stored in any electronic or other data storage medium, or printed or published in any document, report or publication, without the express prior written approval of Preqin Ltd. The information presented in the report is for information purposes only and does not constitute and should not be construed as a solicitation or other offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction, or as advice of any nature whatsoever. If the reader seeks advice rather than information then he should seek an independent fi nancial advisor and hereby agrees that he will not hold Preqin Ltd. responsible in law or equity for any decisions of whatever nature the reader makes or refrains from making following its use of the report. While reasonable efforts have been used to obtain information from sources that are believed to be accurate, and to confi rm the accuracy of such information wherever possible, Preqin Ltd. Does not make any representation or warranty that the information or opinions contained in the report are accurate, reliable, up-to-date or complete. -

Pe Irr 06-30-20.Pdf

The Regents of the University of California Private Equity Investments as of June 30, 2020 (1) Capital Paid‐in Capital Current Market Capital Distributed Total Value Total Value Multiple Description Vintage Year (2) Net IRR (3) Committed (A) Value (B) (C) (B+C) (B+C)/A) Brentwood Associates Private Equity II 1979 3,000,000 3,000,000 ‐ 4,253,768 4,253,768 1.42 5.5% Interwest Partners I 1979 3,000,000 3,000,000 ‐ 6,681,033 6,681,033 2.23 18.6% Alta Co Partners 1980 3,000,000 3,000,000 ‐ 6,655,008 6,655,008 2.22 13.6% Golder, Thoma, Cressey & Rauner Fund 1980 5,000,000 5,000,000 ‐ 59,348,988 59,348,988 11.87 30.5% WCAS Capital Partners II 1980 4,000,000 4,000,000 ‐ 8,669,738 8,669,738 2.17 14.0% KPCB Private Equity (Legacy Funds) (4) Multiple 142,535,631 143,035,469 933,559 1,139,305,336 1,140,238,895 7.97 39.4% Brentwood Associates Private Equity III 1981 3,000,000 3,000,000 ‐ 2,943,142 2,943,142 0.98 ‐0.2% Mayfield IV 1981 5,000,000 5,000,000 ‐ 13,157,658 13,157,658 2.63 26.0% Sequoia Private Equity (Legacy Funds) (4) Multiple 293,200,000 352,355,566 198,038,606 1,055,423,626 1,253,462,231 3.56 30.8% Alta II 1982 3,000,000 3,000,000 ‐ 5,299,578 5,299,578 1.77 7.0% Interwest Partners II 1982 4,008,769 4,008,769 ‐ 6,972,484 6,972,484 1.74 8.4% T V I Fund II 1982 4,000,000 4,000,000 ‐ 6,744,334 6,744,334 1.69 9.3% Brentwood Associates Private Equity IV 1983 5,000,000 5,000,000 ‐ 10,863,119 10,863,119 2.17 10.9% WCAS Capital Partners III 1983 5,000,000 5,000,000 ‐ 9,066,954 9,066,954 1.81 8.5% Golder, Thoma, Cressey & Rauner Fund II 1984 3,000,000