Performance Appraisal of Agricultural Market Committees in India–Data Envelopment Analysis Approach

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Telangana Government Notification Rabi 2017-18

GOVERNMENT OF TELANGANA ABSTRACT Agriculture and Cooperation Department – Pradhan Manthri Fasal Bhima Yojana (PMFBY)– Rabi 2017 -18 - Implementation of “Village as Insurance Unit Scheme” and “Mandal as Insurance Unit Scheme under PMFBY -Notification - Orders – Issued. AGRICULTURE & CO-OPERATION (Agri.II.) DEPARTMENT G.O.Rt.No. 1182 Dated: 01-11-2017 Read the following: 1. From the Joint Secretary to Govt. of India, Ministry of Agriculture, DAC, New Delhi Lr.No. 13015/03/2016-Credit-II, Dated.23.02.2016. 2. From the Commissioner of Agriculture, Telangana, Hyderabad Lr.No.Crop.Ins.(2)/175/2017,Dated:12-10-2017. -oOo- O R D E R: The following Notification shall be published in the Telangana State Gazette: N O T I F I C A T I O N The Government of Telangana hereby notify the Crops and Areas (District wise) to implement the “Village as Insurance Unit Scheme” with one predominant crop of each District and other crops under Mandal Insurance Unit scheme under Pradhan Mantri Fasal Bhima Yojana (PMFBY) during Rabi 2017 -18 season vide Annexure I to VIII and Annexure I and II and Statements 1-30 and Proforma A&B of 30 Districts for Village as Insurance Unit Statements 1 to 30 for Mandal Insurance Unit and Appended to this order. 2. Further, settlement of the claims “As per the Pradhan Mantri Fasal Bhima Yojana (PMFBY) Guidelines and administrative approval of Government of India for Kharif 2016 season issued vide letter 13015/03/2016-Credit-II, Dated.23.02.2016 the condition that, the indemnity claims will be settled on the basis of yield data furnished by the State Government based on requisite number of Crop Cutting Experiments (CCEs) under General Crop Estimation Survey (GCES) conducted and not any other basis like Annavari / Paisawari Certificate / Declaration of drought / flood, Gazette Notification etc., by any other Department / Authority. -

A Study in Telangana State

Research Reports Series - 106 Research Study on Agrarian Distress, Coping Mechanisms and Ramifications of Debt Waiver Scheme (A Study in Telangana State) Dr. Ch. Radhika Rani Dr. Siddayya Dr. V. Prabhakar Shri V. Rammohan Rao Dr. K. Sailaja Centre for Agrarian Studies National Institute of Rural Development & Panchayati Raj Rajendranagar, Hyderabad - 500030 India © National Institute of Rural Development and Panchayati Raj ISBN: 978-84503-80-2 May, 2017 Disclaimer It is hereby confirmed and placed on record that the information in this study report is furnished by the study team and the articles, opinions and content published in this book, need not necessarily be the opinions or policies of NABARD and NABARD does not accept any liability for any omissions or errors thereof. Published by: National Institute of Rural Development and Panchayati Raj Ministry of Rural Development, Government of India Rajendranagar, Hyderabad - 500 030, India Telephone : 040 - 24008473 www.nird.org.in Printed at M/s Vaishnavi Laser Graphics Barkathpura, Hyderabad - 500 027. Tel : 040-2755 2178 Acknowledgements We profoundly thank the Department of Economic Analysis and Research (DEAR) Team of NABARD for their institutional support in awarding the study to NIRD&PR. In particular, we are grateful to Dr. Harsh Kumar Bhanwala, Chairman, NABARD, Shri V.V Satyanarayana, CGM, NABARD,Telangana, Dr. K.J. Satyasai, DGM, NABARD and Shri B.V. Prasad, DGM, NABARD for reposing faith in NIRD&PR to conduct this study. We thank Ms. Suparna Tandon of DEAR Team, Ms. Tulika and other team members at NABARD, Hyderabad for their support, advice and inputs at various stages of this work. -

District Census Handbook, Karimnagar, Part XII-A & B, Series-2

CENSUS OF INDIA 1991 SERIES 2 ANDHRA PRADESH DISTRICT CENSUS HANDBOOK KARIMNAGAR PART XII - A &. B VILLAGE &. TOWN DIRECTORY VILLAGE &. TOWNWISE PRIMARY CENSUS ABSTRACT R.P.SINGH OF THE INDIAN ADMINISTRATIVE SERVICE DIRECTOR OF CENSUS OPERATIONS ANDHRA PRADESH PUlLISHED BY THE: G:)VERNMt:NT OF ANDHRA PRADESH 1995 FOREWORD Publication of the District Census Handbooks (DCHs) was initiated after the 1951 Census and is continuing since then with some innovations/modifications after each decennial Census. This is the most valuable district level publication brought out by the Census Organisation on behalf of each State Govt./ Uni~n Territory a?ministratio~. It Inte.r alia Provides data/information on some of the basIc demographic and socia-economic characteristics and on the availability of certain important civic amenities/facilities in each village and town of the respective districts. This publication has thus proved to be of immense utility to the planners., ~dministrators, academicians and researchers. The scope of the DCH was initially confined to qertain important census tables on population, economic and socio-cultural aspects as also the Primary Census Abstract (PCA) of each village and town (ward wise) of the district. The DCHs published after the 1961 Census contained a descriptive account of the district, administrative statistics, census tables and Village and Town Directories including PCA. After the 1971 Census, two parts of the District Census Handbooks (Part-A comprising Village and Town Directories and Part-B comprising Village and Town PCA) were released in all the States and Union Territories. The third Part (C) of the District Census Handbooks comprising administrative statistics and district census tables, which was also to be brought out, could not be published in many StatesjUTs due to considerable delay in compilation of relevant materia1. -

Pincode Officename Districtname Statename

pincode officename districtname statename 500001 Hyderabad G.P.O. Hyderabad TELANGANA 500001 State Bank Of Hyderabad S.O Hyderabad TELANGANA 500001 Seetharampet S.O Hyderabad TELANGANA 500001 Gandhi Bhawan S.O (Hyderabad) Hyderabad TELANGANA 500001 Moazzampura S.O Hyderabad TELANGANA 500002 Hyderabad Jubilee H.O Hyderabad TELANGANA 500002 Moghalpura S.O Hyderabad TELANGANA 500003 Secunderabad H.O Hyderabad TELANGANA 500003 Kingsway S.O Hyderabad TELANGANA 500004 Khairatabad H.O Hyderabad TELANGANA 500004 Vidhan Sabha S.O (Hyderabad) Hyderabad TELANGANA 500004 A.Gs Office S.O Hyderabad TELANGANA 500004 Anandnagar S.O (Hyderabad) Hyderabad TELANGANA 500004 Bazarghat S.O (Hyderabad) Hyderabad TELANGANA 500004 Parishram Bhawan S.O Hyderabad TELANGANA 500005 Balapur B.O K.V.Rangareddy TELANGANA 500005 Jalapally B.O Hyderabad TELANGANA 500005 Pahadishareef B.O K.V.Rangareddy TELANGANA 500005 Crp Camp S.O (Hyderabad) Hyderabad TELANGANA 500005 Keshogiri S.O Hyderabad TELANGANA 500006 Karwan Sahu S.O Hyderabad TELANGANA 500006 Kulsumpura S.O Hyderabad TELANGANA 500006 Mangalhat S.O Hyderabad TELANGANA 500007 IICT S.O Hyderabad TELANGANA 500007 Ngri S.O Hyderabad TELANGANA 500007 Tarnaka S.O Hyderabad TELANGANA 500007 Jama I Osmania S.O Hyderabad TELANGANA 500008 Nanakramguda B.O Hyderabad TELANGANA 500008 Toli Chowki S.O Hyderabad TELANGANA 500008 Sakkubai Nagar S.O Hyderabad TELANGANA 500008 Kakatiya Nagar S.O Hyderabad TELANGANA 500008 Lunger House S.O Hyderabad TELANGANA 500008 Golconda S.O Hyderabad TELANGANA 500009 Manovikasnagar S.O Hyderabad -

GOVERNMENT of TELANGANA ABSTRACT Municipal

GOVERNMENT OF TELANGANA ABSTRACT Municipal Administration & Urban Development Department - Telangana Regularization of Unapproved and Illegal Layout Rules, 2019 for the Grampanchayat areas falling in 4 newly constituted UDAs namely Satavahana Urban Development Authority, Kareemnagar ; Nizamabad Urban Development Authority, Nizamabad; Stambadri Urban Development Authority, Khammam and Siddipet Urban Development Authority, Siddipet newly constituted Municipalities - Orders – Issued. MUNICIPAL ADMINISTRATION & URBAN DEVELOPMENT (Plg.III) DEPARTMENT G.O.Ms. No.265 Dated:08.11.2019 Read the following:- (1) G.O.Ms.No.151 MA Dated: 02.11.2015 (2) G.O.Ms.No.251 MA Dated: 14.10.2019 (3) G.O.Ms.No.261 MA Dated: 29.10.2019 ****** ORDER In the G.O 1stread above “Telangana Regularization of unapproved and illegal layout Rules, 2015 “ were issued for regularization of plots in unauthorized layouts where the plots have been sold by registered sale deed on or before 28.10.2015. These Rules were applicable to Hyderabad Metropolitan Development Authority, Kakatiya Urban Development Authority and Basara Urban Development Authority, Municipal Corporations, Municipalities and Gram Panchayats falling in the Master Plan limits in the State of Telangana. In pursuance of the said rules large number of applications were received by the HMDA / UDAs, / Municipal Corporations / Municipalities and same were considered for regularization by following the norms prescribed in the said rules. 2. And whereas, after issue of above orders, Government have constituted 4 new Urban Development Authorities viz., Satavahana Urban Development Authority, Kareemnagar ; Nizamadabad Urban Development Authority, Nizamabad ; Stambadri Urban Development Authority, Khammam and Siddipet Urban Development Authority, Siddipet and there have been requests from general public and these new UDAs to extend the above Rules to the Grampanchayat areas falling in these UDAs. -

Mgl-Di520- Unpaid Shareholders List As On

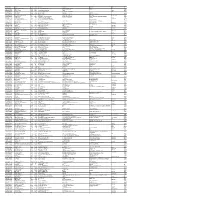

FOLIO_DEMAT ID NAME NETDIV DWNO MICR AD1 AD2 AD3 AD4 CITY PINCOD JH1 JH2 000642 JNANAPRAKASH P.S. 2200.00 205000030 257148 POZHEKKADAVIL HOUSE P.O.KARAYAVATTAM TRICHUR DIST. KERALA STATE 68056 MRS. LATHA M.V. 000691 BHARGAVI V.R. 2200.00 205000031 257149 C/O K.C.VISHWAMBARAN,P.B.NO.63 ADV.KAYCEE & KAYCEE AYYANTHOLE TRICHUR DISTRICT KERALA STATE 001004 KARTHIKEYAN P.K. 2200.00 205000033 257151 PANIKKASSERY HOUSE, THRIPRAYAR POST NATTIKA TRICHUR DIST. KERALA STATE 002769 RAMLATH V E 2200.00 205000037 257155 ELLATHPARAMBIL HOUSE NATTIKA BEACH P O THRISSUR KERALA 003539 RAJAN K C 2200.00 205000038 257107 C/O MODAPPILAI HOUSE PO.KANIMANGALAM THRISSUR NISHA RAJAN 002809 GIREESH C T 2200.00 205000039 257156 CHERIYA THOTTUNGAL H ICE ROAD VATAKARA-3 000000 003124 VENUGOPAL M R 2200.00 205000041 257158 MOOTHEDATH (H) SAWMILL ROAD KOORVENCHERY THRISSUR GEETHADEVI M V 000000 RISHI M.V. 003292 SURENDARAN K K 2068.00 205000043 257160 KOOTTALA (H) PO KOOKKENCHERY THRISSUR 000000 003442 POOKOOYA THANGAL 2068.00 205000045 257162 MECHITHODATHIL HOUSE VELLORE PO POOKOTTOR MALAPPURAM 000000 003445 CHINNAN P P 2200.00 205000046 257163 PARAVALLAPPIL HOUSE KUNNAMKULAM THRISSUR PETER P C 000000 1208160000261446 ALKABEN SHETH 1996.50 205000063 257180 B 202 PUSHKAR RESIDENCY NARAYA OPP SHANKAR ASHRAM PALDI AHMAD AHMEDABAD 380007 AXANSH MUKUNDKUMAR SHETH IN30047640417487 TARUN MADAN 2200.00 205000077 257194 228 PARSHVA SADAN 3RD FLOOR FLAT NO 9 DR A B ROAD WORLI MUMBAI 400004 IN30307710579840 KAVITA VINAY NANGALIA 2475.00 205000078 257195 114 SATNAM APARTMENTS 93 -

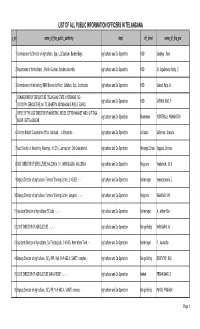

LIST of ALL PUBLIC INFORMATION OFFICERS in TELANGANA S No Name of the Public Authority Dept Off Level Name of the Pio

LIST OF ALL PUBLIC INFORMATION OFFICERS IN TELANGANA s_no name_of_the_public_authority dept off_level name_of_the_pio 1 Commissioner & Director of Agriculture, Opp. L.B.Stadium, BasheerBagh, - Agriculture and Co-Operation HOD Sandhya , Rani 2 Department of Horticulture, , Public Gurdens, Besides Assembly Agriculture and Co-Operation HOD Sri Jagadeswar Reddy, S 3 Commissioner of Marketing, BRKR Bhavan 1st floor, Saifabad, Opp. Secretariat Agriculture and Co-Operation HOD Samuel Raju, M COMMISSIONER OF SERICULTURE, TELANGANA STATE, HYDERABAD, 8-2- 4 Agriculture and Co-Operation HOD JAYAPAL RAO, P 293/82/PN/SERICULTURE, No. 72, BHARTIYA VIDYABHAVANS PUBLIC SCHOOL OFFICE OF THE ASST DIRECTOR OF MARKETING, BESIDE COTTON MARKET YARD, GUTTALA 5 Agriculture and Co-Operation Khammam VUDUTHALA, PADMAVATHI BAZAR, GUTTALA BAZAR 6 O/o the District Cooperative Office, Adilabad , , Collectorate , Agriculture and Co-Operation Adilabad Gaherwar, Sharada 7 Asst.Director of Marketing, Warangal, 4.1.234, Laxmipuram, Old Grain Market Agriculture and Co-Operation Warangal Urban Vuppala, Srinivas 8 ASST DIRECTOR OF SERICULTURE,NALGONDA, 1-1, MIRIYALGUDA, NALGONDA Agriculture and Co-Operation Nalgonda Venkatesh, Sri B 9 Deputy Director of Agriculture, Farmers Training Centre, 2-10-283, -, - Agriculture and Co-Operation Karimnagar Venkateswarlu, S. 10 Deputy Director of Agriculture, Farmers Training Centre, Suryapet, -, -, - Agriculture and Co-Operation Nalgonda RAMARAJU, KV 11 Assistant Director of Agriculture (BC Lab), -, -, - Agriculture and Co-Operation Karimnagar -

Mgl-Di121- Unpaid Shareholders List As On

FOLIO_DEMAIT NAME NETDIV DWNO ADDRESS1 ADDRESS2 ADDRESS3 City PIN 1201090700169075 BHARATKUMAR A SARODE 7.50 4304 HOUSE NO. 348S-01/14/01/02, SWAMI VIVEKANAND NAGAR, CIDCO NASIK 422009 IN30177413890850 SIMA GUPTA 57.00 4627 9 MARHATTA DITCH LANE KOLKATA 700003 1208180017071766 SAKSHAM TANEJA 30.00 8882 H NO 166 2 GODARA GALI RISHI NAGAR HISAR 125001 1208180024440701 DHEERAJ . 79.50 8907 H NO 367C 8 DHANNI GHATI MOHALLA HANSI HISARHANSI HISAR 125033 IN30047642266792 ASHIM GHOSH 15.00 16366 C/15 O N G C NAGAR PALAVASNA MEHSANA 384003 IN30154917163587 SMITA SINGH 450.00 19233 302 MAGIC CARPET JUHU VERSOVA LINK ROAD ANDHERI WESTMUMBAI 400053 1304140001763171 YOGESH RAJENDRA DESHMUKH 7.50 4319 4 HAYNES APRT GANDHI NAGAR BANSILAL NAGAR AREA AURANGABAD 431001 IN30051318370145 MAHESH RAWAT 9.75 5990 26 C DB BLOCK LIG FLATS HARI NAGAR G 8 AREA RAJOURI GARDEN NR HARI NAGAR CLOCK TOWERNEW DELHI DELHI 110027 1208870033232279 ARYAN BATHLA 3.75 8944 SO VIJAY BATHLA 8 SADHBHAWNA MARG C BLOCK SIRSA SIRSA HARYANA SIRSA 125055 1208160063131398 ANAND SINGH SHISHODIA 14.25 11914 133K/2J New Basti Beniganj Ayodhyapuri ALLAHABAD 211016 IN30051385676265 MAULIKKUMAR RAMESHBHAI PATEL 16.50 16370 GANESHPARU KAHODA KAHODA MAHESANA MAHESANA GUJARAT 384130 IN30154915888084 RAVI CHANDRA V 37.50 20437 NO 502 POOJA APTS HAPPY HOME SOC Y S MARG DAHISAR WESTMUMBAI 400068 1304140001392505 GOPAL KRISHNA M S 0.75 4436 184 FLR GF BLDG OM KARNAGAR 6 7 CRS ARAKERE BANGALORE BANGALORE 560076 1208160001238023 RAJKUMAR . 150.00 4510 OLD NO 1 NEW NO 64 BLK 1 WEST ST ATHIKKOTTAI PATTUKKOTTAI THANJAVUR 613001 IN30115127998777 KAUSHAL KUMAR 52.50 7716 D 358 D BLOCK GANESH NAGAR PANDAV NAGAR COMPLEX IIND FLOORNEW DELHI 110092 1208160000404165 S TOMER 0.75 7808 E 5/83 RAJIV GALI DAYAL PUR DELHI NEW DELHI 110094 1203600005786359 SAJAN KHETAN 75.00 8488 F 3 GREENWOOD CITY SECTOR 46 JHARSA GURGAON GURUGRAM 122003 1208160054886793 SOHAN LAL 412.50 12198 , Lonha kanpur road Lonha sarojini nagar LUCKNOW 226008 IN30097411153721 GULATUNBIBI M. -

Mid Day Meal Programme Was Introduced in 1925 for Disadvantaged Children in Madras Municipal Corporation, Where the Children Are Not Going to the School

1. INTRODUCTION: Mid Day Meal Programme was introduced in 1925 for disadvantaged children in Madras Municipal Corporation, where the children are not going to the school. By the mid 1980’s Kerala, Gujarat, Tamilnadu and Pondicherry States have universalized a cooked Mid Day Meal Program for children studying at primary level and in 1990-91 twelve States also started implementing the Mid Day Meal Programme for primary level children with their own resources. The National Program of Nutritional Support to Primary Education (NP-NSPE) was launched as a centrally sponsored scheme on 15th August 1995 in 2408 blocks in the country for enhancement of enrolment, retention, improvement of attendance and quality of education and improving of nutritional levels among children. By the year 1997-98 the NP- NSPE was introduced in all districts of the country. The Hon’ble Supreme Court of India in its direction in 2001 has linked the feeding Programme of the children to quality education Programme of Government. This was done to ensure that lesser number of children go to school hungry. This resulted in encouraging poor families to enroll their children in Government schools and thereby enable them to guarantee at least one square meal a day, called as Mid Day Meal. All State Governments in the country have to ensure that every child coming to a Government school gets one wholesome meal for lunch on school days. Logistically, the problem was tackled through government schools that educate 60 per cent of the country’s children, most of them being from below poverty-line. With parents (often single) going for wage labour early in the morning, the children usually come to school hungry because kitchen fires at home are only late in the evenings after the father or the mother brings home the daily wage. -

1 GOVERNMENTOF TELANGANA OFFICE of the DIRECTOR of PUBLIC HEALTH and FAMILY WELFARE MEDIA BULLETIN- COVID-19 Dated: 07/08/2020

GOVERNMENTOF TELANGANA OFFICE OF THE DIRECTOR OF PUBLIC HEALTH AND FAMILY WELFARE MEDIA BULLETIN- COVID-19 Dated: 07/08/2020 As of:06/08/2020 (8PM) STATUS OF COVID-19 CASES S. NO DETAILS NUMBER 1. NO. OF POSITIVE CASES TODAY (CUMULATIVE) 2,207 (75,257) 2. NO. OF RECOVERED CASES TODAY (CUMULATIVE) 1,136 (53,239) 3. NO. OF DEATHS TODAY (CUMULATIVE) 12 (601) 4. CASE FATALITY RATE (INDIA) 0.79% (2.07%) 5. RECOVERY RATE (INDIA) 70.7% (67.62%) 6. TOTAL NUMBER OF ACTIVE CASES 21,417 7. NO. OF INDIVIDUALS IN HOME/INSTITUTIONAL ISOLATION 14,837 8. NUMBER OF ASYMPTOMATIC CASES (OF THOSE UNDER HOME ISOLATION) ~ 84% STATUS OF TESTS S. NO DETAILS NUMBER 1 NO. OF SAMPLES TESTED TODAY (CUMULATIVE) AGAINST DAILY TESTING 23,495 TARGET FOR TELANGANA AS PER W.H.O. BENCHMARK @ 140 PER MILLION (5,66,984) PER DAY, I.E., 5,600 TESTS PER DAY 2 SAMPLES TESTED PER MILLION POPULALATION 15271.7 3 NO. OF REPORTS AWAITED 1,539 1 AGE AND GENDER WISE COVID POSITIVE DETAILS S.NO. AGE GROUP AGE WISE POSITIVE CASES (%) TOTAL MALE FEMALE 1 UPTO 10 YEARS 3.4 1.9 1.5 2 11 - 20 YEARS 5.3 2.8 2.4 3 21 - 30 YEARS 22.1 14.1 7.9 4 31 - 40 YEARS 25.0 17.7 7.3 5 41 - 50 YEARS 18.6 12.5 6.2 6 51 - 60 YEARS 14.7 9.5 5.2 7 61 - 70 YEARS 7.7 5.0 2.7 8 71 - 80 YEARS 2.6 1.7 0.9 9 81 & ABOVE 0.6 0.4 0.2 TOTAL 100% 65.6% 34.4% COMORBIDITIES STATUS AMONG DEATHS PERCENTAGE OF DEATHS DUE TO COVID-19 46.13 % PERCENTAGE OF DEATHS DUE TO COMORBIDITIES 53.87 % DETAILS OF INFRASTRUCTURE/BED OCCUPANCY UNDER GOVERNMENT S.