A Study in Telangana State

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Telangana Government Notification Rabi 2017-18

GOVERNMENT OF TELANGANA ABSTRACT Agriculture and Cooperation Department – Pradhan Manthri Fasal Bhima Yojana (PMFBY)– Rabi 2017 -18 - Implementation of “Village as Insurance Unit Scheme” and “Mandal as Insurance Unit Scheme under PMFBY -Notification - Orders – Issued. AGRICULTURE & CO-OPERATION (Agri.II.) DEPARTMENT G.O.Rt.No. 1182 Dated: 01-11-2017 Read the following: 1. From the Joint Secretary to Govt. of India, Ministry of Agriculture, DAC, New Delhi Lr.No. 13015/03/2016-Credit-II, Dated.23.02.2016. 2. From the Commissioner of Agriculture, Telangana, Hyderabad Lr.No.Crop.Ins.(2)/175/2017,Dated:12-10-2017. -oOo- O R D E R: The following Notification shall be published in the Telangana State Gazette: N O T I F I C A T I O N The Government of Telangana hereby notify the Crops and Areas (District wise) to implement the “Village as Insurance Unit Scheme” with one predominant crop of each District and other crops under Mandal Insurance Unit scheme under Pradhan Mantri Fasal Bhima Yojana (PMFBY) during Rabi 2017 -18 season vide Annexure I to VIII and Annexure I and II and Statements 1-30 and Proforma A&B of 30 Districts for Village as Insurance Unit Statements 1 to 30 for Mandal Insurance Unit and Appended to this order. 2. Further, settlement of the claims “As per the Pradhan Mantri Fasal Bhima Yojana (PMFBY) Guidelines and administrative approval of Government of India for Kharif 2016 season issued vide letter 13015/03/2016-Credit-II, Dated.23.02.2016 the condition that, the indemnity claims will be settled on the basis of yield data furnished by the State Government based on requisite number of Crop Cutting Experiments (CCEs) under General Crop Estimation Survey (GCES) conducted and not any other basis like Annavari / Paisawari Certificate / Declaration of drought / flood, Gazette Notification etc., by any other Department / Authority. -

CSP Details for Basix Sub K I Transacations

Sr. CSP Location Name of BC-CSP Agent Adddress Contact Number Villages covered No. 1 Puppalapalle Chatla Sanjeev H no 2-10, Puppalapalle, Jakranpally, Nizamabad, AP -503003 94922 54471 Puppalapalle 2 Gaggupalle Miripala Mallaiah H no 1-49, Gaggupalli, Armoor, Nizamabad, Andhra Pradesh - 503224 88974 24849 Gaggupalle 3 Wandrikal Govindhu Arlappa H no 1-61, Wandrikal village, Gandhari Mandal, Nizamabad, Andhra Pradesh- 94927 29813 Wandrikal 503120 4 Brahmanapalle Elupula Bhaskar H no 1-12/1, Bhramanpalli village, Gandhari Mandal, Nizamabad , Andhra 77020 47793 Brahmanapalle Pradesh-503114 5 Gujjul Chitike Raju H no 1-98, Gujjal Village, Gandhari Mandal, Nizamabad, Andhra Pradesh- 94915 34542 Gujjul 503114 6 Durgam Gone Vishnu H no 1-17, Durgam Village, Gandhrari Mandal, Nizamabad Andhra Pradesh - 94936 62642 Durgam , Somaram 503114 7 Tipparam Yerram Bharati H no 1-81/1, Tipparam Village,Gandhari Mandal, Nizamabad District, Andhra 94905 08158 Tipparam Pradesh-503114 8 Tekrial Nangunuri Venkatesham H no 1-23, Tekiryal Village, Kamareddy Mandal, Nizamabad, Andhra Pradesh- 96184 91758 Tekrial 503111 9 Ravutla Sithap Naresh Kumar H no 5-61/1, Harijanawada, Ravutla village, Sirkonda Mandal, Nizamabad Dist, 99669 07301 Ravutla, Salampur AP-503165 10 Sikindrapur Barla Sanjeev H no 1-15/13, Jakranpally, Sikindrapur, Nizamabad, Telangana-503175 81438 12174 Sikindrapur, Madhapur 11 Kelojiwadi Allipuram Ranjith Kumar H no 2-74/A, Kalojiwadi village, Tadwai Mandal, Nizamabad District, 94942 61530 Kelojiwadi Telangana-503145 12 Manoharabad Chintakindi -

District Census Handbook, Karimnagar, Part XII-A & B, Series-2

CENSUS OF INDIA 1991 SERIES 2 ANDHRA PRADESH DISTRICT CENSUS HANDBOOK KARIMNAGAR PART XII - A &. B VILLAGE &. TOWN DIRECTORY VILLAGE &. TOWNWISE PRIMARY CENSUS ABSTRACT R.P.SINGH OF THE INDIAN ADMINISTRATIVE SERVICE DIRECTOR OF CENSUS OPERATIONS ANDHRA PRADESH PUlLISHED BY THE: G:)VERNMt:NT OF ANDHRA PRADESH 1995 FOREWORD Publication of the District Census Handbooks (DCHs) was initiated after the 1951 Census and is continuing since then with some innovations/modifications after each decennial Census. This is the most valuable district level publication brought out by the Census Organisation on behalf of each State Govt./ Uni~n Territory a?ministratio~. It Inte.r alia Provides data/information on some of the basIc demographic and socia-economic characteristics and on the availability of certain important civic amenities/facilities in each village and town of the respective districts. This publication has thus proved to be of immense utility to the planners., ~dministrators, academicians and researchers. The scope of the DCH was initially confined to qertain important census tables on population, economic and socio-cultural aspects as also the Primary Census Abstract (PCA) of each village and town (ward wise) of the district. The DCHs published after the 1961 Census contained a descriptive account of the district, administrative statistics, census tables and Village and Town Directories including PCA. After the 1971 Census, two parts of the District Census Handbooks (Part-A comprising Village and Town Directories and Part-B comprising Village and Town PCA) were released in all the States and Union Territories. The third Part (C) of the District Census Handbooks comprising administrative statistics and district census tables, which was also to be brought out, could not be published in many StatesjUTs due to considerable delay in compilation of relevant materia1. -

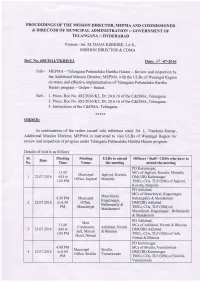

Roc No.608/2014/TKHH/E1 Datez O2l -07-2016

PROCEEDINGS OF THE MISSION DIRECTO& MEPMA AND COMMTSSIONER & DIRECTOR OF MUNICIPAL ADMINISTRATION :: GOVERNMENT oF TELANGANA:: HYDERABAD Present:- Sri. M. DANA KISHORE, I.A.S., MISSION DIRECTOR & CDMA RoC No.608/2014/TKHH/E1 Datez o2l -07-2016 Sub:- MEPMA - Telangana Pattanalaku Haritha Haram - Review and inspection by the Additional Mission Director, MEPMA with the ULBs of Warangal Region on status and effective implementation of Telangana Pattanalaku Haritha Haram program - Orders - Issued. Ref:- 1. Procs. Roc No. 682l20l6ll3,Dt:24.6.16 of the C&DMA, Telangana. 2. Procs. Roc No. 682120161K3, Dt: 28.6.16 of the C&DMA, Telangana. 3. Instructions of the C&DMA, Telangana *** {< {< ORDER: In continuation of the orders issued vide reference cited, Sri. L. Vandana Kumar, Additional Mission Director, MEPMA is instructed to visit ULBs of Warangal Region for review and inspection of progress under Telangana Pattanalaku Haritha Haram program. Details of visit is as follows sl. Meeting Meeting ULBs to attend Officers / Staff / CBOs who have to Date No. Time Venue the meeting attend the meeting PD Karimnagar, 11.00 MCs of Jagityal, Korutla, Metpally Municipal Jagityal, Korutla, I 22.07.2016 AM to DMC(IB) Karimnagar Office, Jagityal Metpally 1.00 PM TMCs, COs, TLF (OBs) of Jagityal, Korutla, Metpally PD Adilabad, MCs of Manchiryal, Kagaznagar, Manchiryal, 4.30 PM Municipal Bellampally & Mandamarri Kagaznagar, 2 22.07.2016 to 6.30 Office, DMC(IB) Adilabad Bellampally & PM Manchiryal TMCs, COs, TLF (OBs) of Mandamarri Manchiryal, Kagaznagar, Bellampally -

Annexure 1B 18416

Annexure 1 B List of taxpayers allotted to State having turnover of more than or equal to 1.5 Crore Sl.No Taxpayers Name GSTIN 1 BROTHERS OF ST.GABRIEL EDUCATION SOCIETY 36AAAAB0175C1ZE 2 BALAJI BEEDI PRODUCERS PRODUCTIVE INDUSTRIAL COOPERATIVE SOCIETY LIMITED 36AAAAB7475M1ZC 3 CENTRAL POWER RESEARCH INSTITUTE 36AAAAC0268P1ZK 4 CO OPERATIVE ELECTRIC SUPPLY SOCIETY LTD 36AAAAC0346G1Z8 5 CENTRE FOR MATERIALS FOR ELECTRONIC TECHNOLOGY 36AAAAC0801E1ZK 6 CYBER SPAZIO OWNERS WELFARE ASSOCIATION 36AAAAC5706G1Z2 7 DHANALAXMI DHANYA VITHANA RAITHU PARASPARA SAHAKARA PARIMITHA SANGHAM 36AAAAD2220N1ZZ 8 DSRB ASSOCIATES 36AAAAD7272Q1Z7 9 D S R EDUCATIONAL SOCIETY 36AAAAD7497D1ZN 10 DIRECTOR SAINIK WELFARE 36AAAAD9115E1Z2 11 GIRIJAN PRIMARY COOPE MARKETING SOCIETY LIMITED ADILABAD 36AAAAG4299E1ZO 12 GIRIJAN PRIMARY CO OP MARKETING SOCIETY LTD UTNOOR 36AAAAG4426D1Z5 13 GIRIJANA PRIMARY CO-OPERATIVE MARKETING SOCIETY LIMITED VENKATAPURAM 36AAAAG5461E1ZY 14 GANGA HITECH CITY 2 SOCIETY 36AAAAG6290R1Z2 15 GSK - VISHWA (JV) 36AAAAG8669E1ZI 16 HASSAN CO OPERATIVE MILK PRODUCERS SOCIETIES UNION LTD 36AAAAH0229B1ZF 17 HCC SEW MEIL JOINT VENTURE 36AAAAH3286Q1Z5 18 INDIAN FARMERS FERTILISER COOPERATIVE LIMITED 36AAAAI0050M1ZW 19 INDU FORTUNE FIELDS GARDENIA APARTMENT OWNERS ASSOCIATION 36AAAAI4338L1ZJ 20 INDUR INTIDEEPAM MUTUAL AIDED CO-OP THRIFT/CREDIT SOC FEDERATION LIMITED 36AAAAI5080P1ZA 21 INSURANCE INFORMATION BUREAU OF INDIA 36AAAAI6771M1Z8 22 INSTITUTE OF DEFENCE SCIENTISTS AND TECHNOLOGISTS 36AAAAI7233A1Z6 23 KARNATAKA CO-OPERATIVE MILK PRODUCER\S FEDERATION -

Pincode Officename Districtname Statename

pincode officename districtname statename 500001 Hyderabad G.P.O. Hyderabad TELANGANA 500001 State Bank Of Hyderabad S.O Hyderabad TELANGANA 500001 Seetharampet S.O Hyderabad TELANGANA 500001 Gandhi Bhawan S.O (Hyderabad) Hyderabad TELANGANA 500001 Moazzampura S.O Hyderabad TELANGANA 500002 Hyderabad Jubilee H.O Hyderabad TELANGANA 500002 Moghalpura S.O Hyderabad TELANGANA 500003 Secunderabad H.O Hyderabad TELANGANA 500003 Kingsway S.O Hyderabad TELANGANA 500004 Khairatabad H.O Hyderabad TELANGANA 500004 Vidhan Sabha S.O (Hyderabad) Hyderabad TELANGANA 500004 A.Gs Office S.O Hyderabad TELANGANA 500004 Anandnagar S.O (Hyderabad) Hyderabad TELANGANA 500004 Bazarghat S.O (Hyderabad) Hyderabad TELANGANA 500004 Parishram Bhawan S.O Hyderabad TELANGANA 500005 Balapur B.O K.V.Rangareddy TELANGANA 500005 Jalapally B.O Hyderabad TELANGANA 500005 Pahadishareef B.O K.V.Rangareddy TELANGANA 500005 Crp Camp S.O (Hyderabad) Hyderabad TELANGANA 500005 Keshogiri S.O Hyderabad TELANGANA 500006 Karwan Sahu S.O Hyderabad TELANGANA 500006 Kulsumpura S.O Hyderabad TELANGANA 500006 Mangalhat S.O Hyderabad TELANGANA 500007 IICT S.O Hyderabad TELANGANA 500007 Ngri S.O Hyderabad TELANGANA 500007 Tarnaka S.O Hyderabad TELANGANA 500007 Jama I Osmania S.O Hyderabad TELANGANA 500008 Nanakramguda B.O Hyderabad TELANGANA 500008 Toli Chowki S.O Hyderabad TELANGANA 500008 Sakkubai Nagar S.O Hyderabad TELANGANA 500008 Kakatiya Nagar S.O Hyderabad TELANGANA 500008 Lunger House S.O Hyderabad TELANGANA 500008 Golconda S.O Hyderabad TELANGANA 500009 Manovikasnagar S.O Hyderabad -

Meos & MIS Co-Ordinators

List of MEOs, MIS Co-orfinators of MRC Centers in AP Sl no District Mandal Name Designation Mobile No Email ID Remarks 1 2 3 4 5 6 7 8 1 Adilabad Adilabad Jayasheela MEO 7382621422 [email protected] 2 Adilabad Adilabad D.Manjula MIS Co-Ordinator 9492609240 [email protected] 3 Adilabad ASIFABAD V.Laxmaiah MEO 9440992903 [email protected] 4 Adilabad ASIFABAD G.Santosh Kumar MIS Co-Ordinator 9866400525 [email protected] [email protected] 5 Adilabad Bazarhathnoor M.Prahlad MEO(FAC) 9440010906 n 6 Adilabad Bazarhathnoor C.Sharath MISCo-Ord 9640283334 7 Adilabad BEJJUR D.SOMIAH MEO FAC 9440036215 [email protected] MIS CO- 8 Adilabad BEJJUR CH.SUMALATHA 9440718097 [email protected] ORDINATOR 9 Adilabad Bellampally D.Sridhar Swamy M.E.O 7386461279 [email protected] 10 Adilabad Bellampally L.Srinivas MIS CO Ordinator 9441426311 [email protected] 11 Adilabad Bhainsa J.Dayanand MEO 7382621360 [email protected] 12 Adilabad Bhainsa Hari Prasad.Agolam MIS Co-ordinator 9703648880 [email protected] 13 Adilabad Bheemini K.Ganga Singh M.E.O 9440038948 [email protected] 14 Adilabad Bheemini P.Sridar M.I.S 9949294049 [email protected] 15 Adilabad Boath A.Bhumareedy M.E.O 9493340234 [email protected] 16 Adilabad Boath M.Prasad MIS CO Ordinator 7382305575 17 Adilabad CHENNUR C.MALLA REDDY MEO 7382621363 [email protected] MIS- 18 Adilabad CHENNUR CH.LAVANYA 9652666194 [email protected] COORDINATOR 19 Adilabad Dahegoan Venkata Swamy MEO 7382621364 [email protected] 20 -

Notification for the Posts of Gramin Dak Sevaks Cycle – Iii/2020-2021 Telangana Circle

NOTIFICATION FOR THE POSTS OF GRAMIN DAK SEVAKS CYCLE – III/2020-2021 TELANGANA CIRCLE RE/GDS ONLINE/CYCLE-3/2021 Applications are invited by the respective engaging authorities as shown in the annexure ‘I’against each post, from eligible candidates for the selection and engagement to the following posts of Gramin Dak Sevaks. I. Job Profile:- (i) BRANCH POSTMASTER (BPM) The Job Profile of Branch Post Master will include managing affairs of Branch Post Office, India Posts Payments Bank ( IPPB) and ensuring uninterrupted counter operation during the prescribed working hours using the handheld device/Smartphone/laptop supplied by the Department. The overall management of postal facilities, maintenance of records, upkeep of handheld device/laptop/equipment ensuring online transactions, and marketing of Postal, India Post Payments Bank services and procurement of business in the villages or Gram Panchayats within the jurisdiction of the Branch Post Office should rest on the shoulders of Branch Postmasters. However, the work performed for IPPB will not be included in calculation of TRCA, since the same is being done on incentive basis.Branch Postmaster will be the team leader of the Branch Post Office and overall responsibility of smooth and timely functioning of Post Office including mail conveyance and mail delivery. He/she might be assisted by Assistant Branch Post Master of the same Branch Post Office. BPM will be required to do combined duties of ABPMs as and when ordered. He will also be required to do marketing, organizing melas, business procurement and any other work assigned by IPO/ASPO/SPOs/SSPOs/SRM/SSRM and other Supervising authorities. -

Lions Clubs International Club Membership Register

LIONS CLUBS INTERNATIONAL CLUB MEMBERSHIP REGISTER SUMMARY THE CLUBS AND MEMBERSHIP FIGURES REFLECT CHANGES AS OF JUNE 2018 MEMBERSHI P CHANGES CLUB CLUB LAST MMR FCL YR TOTAL IDENT CLUB NAME DIST NBR COUNTRY STATUS RPT DATE OB NEW RENST TRANS DROPS NETCG MEMBERS 4207 026520 BELLAMPALLI INDIA 320 G 4 06-2018 93 44 0 0 -30 14 107 4207 026539 KARIMNAGAR INDIA 320 G 4 06-2018 107 3 0 0 -24 -21 86 4207 026564 RAMAGUNDAM INDIA 320 G 4 04-2018 81 3 0 0 -1 2 83 4207 026570 SIRSILLA INDIA 320 G 4 06-2018 108 8 0 0 -6 2 110 4207 029870 MANCHERIAL INDIA 320 G 4 06-2018 103 7 0 0 -3 4 107 4207 038384 MANTHANI INDIA 320 G 4 06-2018 22 0 0 0 0 0 22 4207 061552 PEDDAPALLY INDIA 320 G 4 06-2018 51 17 0 0 -3 14 65 4207 065069 SULTANABAD INDIA 320 G 4 06-2018 27 7 0 2 -9 0 27 4207 076040 ASIFABAD INDIA 320 G 4 06-2018 28 6 0 0 -7 -1 27 4207 078404 KARIMNAGAR SATHAVAHANA INDIA 320 G 4 06-2018 73 8 0 0 0 8 81 4207 097521 KARIMNAGAR MANAIR INDIA 320 G 4 06-2018 96 40 1 0 -36 5 101 4207 098674 MANCHERIAL GARIMILLA INDIA 320 G 4 06-2018 44 11 1 0 -19 -7 37 4207 101093 KARIMNAGAR KALESHWARI INDIA 320 G 4 06-2018 28 5 0 0 -11 -6 22 4207 101628 BEJJANKI INDIA 320 G 4 06-2018 60 7 0 0 -5 2 62 4207 102433 KORATLA INDIA 320 G 4 06-2018 77 15 1 0 -4 12 89 4207 103920 CHOPPADANDI INDIA 320 G 4 06-2018 39 4 0 0 -1 3 42 4207 104257 KARIMNAGAR KAMAN INDIA 320 G 4 06-2018 21 0 0 0 -7 -7 14 4207 104749 KARIMNAGAR SAHAYA INDIA 320 G 4 06-2018 36 6 0 0 -4 2 38 4207 104901 BELLAMPALLI SINGARENI INDIA 320 G 4 06-2018 13 7 0 0 0 7 20 4207 106382 VEMULAWADA INDIA 320 G 4 06-2018 -

Planned Outages

/nt h NoRTHERN powpR DISTRIBUTIoN coMpANy oF TELANGANA LTD \rY coRPoRATE oFFrcE:: wARANGAL Ctrcular Memo No.CGM/C/DE/C/ADE/C/AE/C1&C2IF.EoDB/D.No. 1O98. Dt:31-12-18 Sub: CGM/Commercial/TSNPDCL/WGL Ease of Dolng Buslness Uploadtng the Planned-outages one month ln advance ln TSNPDCL web-portal to notlfy the customers Instnrctlons issued - Regardlng. Ref: 1. Business Reforms Action PIan (BRAPI - 2}lrg received from Spl. Chief Secretary, Energy Department, GorA. of T.S., dated 13-11-18 2. Memo No. CGM/ C I DE I C IADEIC/AE I C1eC2 I F.EoDB/ D.No. 1O85, Dt:28-12-2O18 &&&&& In the reference lst cited above, the DIPP has mandated in the Business Reform Action Plan (BRAP) - 2OL9 that the DISCOMs have to notify the customers of planned-outages (Maintenance and load shedding) for next one month, in advance. Accordingly, provisions are made in the TSNPDCL Web-portal to notify the planned-outages for the next one month in advance. The Schedules of 33/ 11 KV SS malntenance is given in the reference 2nd cited above. Apart from this, any planned power outages are to be notilied in advance. The DEs/Opn are directed to instruct the AEs/?ech of Operation Divlslon offlcei to enter the schedules of planned outages (Maintenance and load shedding) proposed pertaining to thelr Dlvision in the application explained above, one month in advance (Ptanned outages ln January, 2OL9 are entered ln the month of December,2O18 ttself and so onf. The SEs/Opn are instructed to direct the AEs/Tech of Operation Circle Offlces to monitor the lssue pertainlng to their circle. -

Jagtial District

JAGTIAL DISTRICT We acknowledge the content from http://jagitial.telangana.gov.in/district-profile Jagtial district is one of the 31 districts in the state of Telangana. Jagtial was carved out of Karimnagar district and was made as a district on October 11, 2016. Jagtial district is spread across an area of 3,043 square kilometers and has a population of 9,83,414 as per 2011 Census data. Jagtial town is the headquarters with a population of 1,03,962. Korutla is the second largest town with a population of 1,08,297. Jagtial and Metpally are the revenue divisions in this district. These are further divided into 18 mandals. Jagtial, Korutla, Dharmapuri, Choppadondi and Vemulawada Assembly constituencies are under Jagtial district. Jagtial town got its name from Jaggadeva. Godavari River flows through this district. There is Acharya N. G. Ranga Agricultural University's Agricultural College in Polasa. Kotilingala located on the bank of Godavari River was an important town in ancient town during the period of the Assaka mahajanapada and the Satavahanas. Lakshminarasimha Swamy Temple at Dharmapuri and Anjaneya Swamy Temple at Kondagattu are famous temples. There is sugar factory located at Muthyampeta. PHYSICAL FEATURES OF JAGTIAL DISTRICT: HISTORICAL PLACES: The historical Qila at Jagtial. TEMPLES: The holy temple of Sri Laxminarsimha Swamy on the banks of the Godavari River at Dharmapuri Mandal head-quarters The holy temple of Sri Koteshwara Swamy on the banks of the Godavari River at Kotilingala village in Velgatur Mandal The holy temple of Sri Anjaneya Swamy located at Kondagattu of Muthyampet village in Mallial Mandal. -

List of Industries Issued with Closure Directions for Operating Without

LIST OF INDUSTRIES ISSUED WITH CLOSURE ORDERS WHICH ARE OPERATING WITHOUT CFO OF THE BOARD S.No. Name of the Industry 1. M/s. Sri Vijaya Ganapathi Chemicals, Sy.No.117, Chilkamarry (V), P.A.Pally (M), Yadadri Bhuvanagiri District. 2. M/s. Delta Materials, Dharmaram (V), Turkapally (M), Yadadri Bhuvanagiri District. 3. M/s. Swamini Industries, Sy.No.374 & 375, Thimmapuram (V), Bommalaramaram (M), Yadadri Bhuvanagiri District. 4. M/s. Anjana Explosivies Ltd., Unit-I, Peddakaparthy (V), Chityal (M), Nalgonda District. 5. M/s. Anjana Explosivies Ltd., Unit-II, Peddakaparthy (V), Chityal (M), Nalgonda District. 6. M/s. South Indian Alluminium rolling Industries, Durajpally (V), Chivemla (M), Suryapet District. 7. M/s. SHV Energy (P) Ltd., Ltd., S.Lingotam (V), Choutuppal (M), Yadadri Bhuvanagiri District. 8. M/s. K. Vijay Bhupal Reddy, (6.67 Ha. Black Granite Mine), Sy.No.263, Kalimera (V), Kattangur (M), Nalgonda District. 9. M/s. Sri Ch. Satyanarayana, Sy.No. 297, Tavaklapuram (V), Gundlapally (M), Nalgonda District. 10. M/s. Black Granite Mine of Priya Granites, Kampalapally (V), Thripuraram (M), Nalgonda District. 11. M/s. Black Granite Mine of Sri Guntheti Praveen, Indurthi (V), Marriguda (M), Nalgonda District. 12. M/s. Sunshine Minerals & Trading, Sy.No.122 & 138 (P), Chimiryal (V), Kodad (M), Suryapet District. 13. M/s. Chava Venu Gopala Krishna Mines, Mining of Black Granite, Nagaram (V), Valigonda (M), Yadadri Bhuvanagiri District. 14. M/s. Sridevi Mines & Granites Impex (P) Ltd., Chillapur (V), S. Narayanapur (M), Yadadri Bhuvanagiri District. 15. M/s. Sridevi Mines & Granites Impex (P) Ltd., Pagidipally (V), Bhongir (M), Yadadri Bhuvanagiri District.