Platinum Japan Fund

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Anellotech Plas-Tcat Funding from R Plus Japan Press Release June 30

Anellotech Secures Funds to Develop Innovative Plas-TCatTM Plastics Recycling Technology from R Plus Japan, a New Joint Venture Company launched by 12 Cross-Industry Partners within the Japanese Plastic Supply Chain Pearl River, NY, USA, (June 30, 2020) —Sustainable technology company Anellotech has announced that R Plus Japan Ltd., a new joint venture company, will invest in the development of Anellotech’s cutting-edge Plas-TCatTM technology for recycling used plastics. R Plus Japan was established by 12 cross-industry partners within the Japanese plastics supply chain. Member partners include Suntory MONOZUKURI Expert Ltd. (SME, a subsidiary of Suntory Holdings Ltd.), TOYOBO Co. Ltd., Rengo Co. Ltd., Toyo Seikan Group Holdings Ltd., J&T Recycling Corporation, Asahi Group Holdings Ltd., Iwatani Corporation, Dai Nippon Printing Co. Ltd., Toppan Printing Co. Ltd., Fuji Seal International Inc., Hokkaican Co. Ltd., Yoshino Kogyosho Co. Ltd.. Many plastic packaging materials are unable to be recycled and are instead thrown away after a single use, often landfilled, incinerated, or littered, polluting land and oceans. Unlike the existing multi-step processes which first liquefy plastic waste back into low value “synthetic oil” intermediate products, Anellotech’s Plas- TCat chemical recycling technology uses a one-step thermal-catalytic process to convert single-use plastics directly into basic chemicals such as benzene, toluene, xylenes (BTX), ethylene, and propylene, which can then be used to make new plastics. The technology’s process efficiency has the potential to significantly reduce CO2 emissions and energy consumption. Once utilized across the industry, this technology will be able to more efficiently recycle single-use plastic, one of the world’s most urgent challenges. -

Minebea Co., Ltd. ANNUAL REPORT 2006 Year Ended March 31, 2006 for Minebea, Competitiveness

Minebea Co., Ltd. ANNUAL REPORT 2006 Year Ended March 31, 2006 For Minebea, competitiveness Minebea Co., Ltd., was established in 1951 as Japan’s first specialized manufacturer means ensuring both ultraprecision of miniature ball bearings. Today, the Company is the world’s leading comprehensive manufacturer of miniature ball bearings and high-precision components, supplying customers worldwide in the information and telecommunications equipment, aerospace, automotive and household electrical appliance industries. machining and mass As of March 31, 2006, the Minebea Group encompassed 44 subsidiaries and affiliates in 13 countries. The Group maintains 28 plants and 43 sales offices and employs a total of 47,526 people. production technologies. Contents 2 At a Glance 3 Consolidated Financial Highlights 4 A Message to Our Shareholders 7 Special Feature: Capitalizing on Core Technologies to Develop Diverse New Businesses 17 Protecting the Environment 17 Contributing to Society 18 Corporate Governance 20 A History of Achievements Disclaimer Regarding Future Projections In this annual report, all statements that are not historical facts are future projections made based on certain assumptions and our 22 Directors, Auditors and Executive Officers management’s judgement drawn from currently available information. Accordingly, when evaluating our performance or value as a 23 Organization going concern, these projections should not be relied on entirely. Please note that actual performance may vary significantly from any particular projection, owing to various factors, including: (i) changes in economic indicators surrounding us, or in demand trends; 24 Contact Information (ii) fluctuation of foreign exchange rates or interest rates; and (iii) our ability to continue R&D, manufacturing and marketing in a timely manner in the electronics business sector, where technological innovations are rapid and new products are launched 25 Financial Section continuously. -

Integrated Report (Year Ended March 2019)

Introduction/ Chapter I Chapter II Chapter III Chapter IV President’s message Value Creation Story of MinebeaMitsumi Financial Strategy and Capital Policy Initiatives for Value Creation Initiatives to Support Value Creation 1986 2010 Hamamatsu Plant is established Suzhou Plant is established to expand Development in the electronic devices production of LED backlights Chapter I Value Creation Story of MinebeaMitsumi and components area is expanded History of MinebeaMitsumi Backlights Suzhou Plant (China) FDDs and MODs 2018 Global development ahead of other Hamamatsu Plant (Japan) Kosice Plant in Slovakia commences 2010 1988 production Our plant is established in Cambodia, and Lop Buri Plant is established in Thailand Supply to Europe market is commences production the next year Production in expanded companies For risk diversification, expansion of the electronic production and reduction of costs devices and components Cambodia Plant Speedy diversification through M&As area is expanded 1980 1963 Lop Buri Plant (Thailand) Ayutthaya Plant is AGA (Active Grill Plant is relocated from Kawaguchi, Saitama, and operations 1994 established 1984 Kosice Plant (Slovakia) Shutter) Actuators begin at the Karuizawa Plant, to become the mother The Company Bang Pa-in Plant is Minebea Electronics & plant of all the MinebeaMitsumi Group’s plants advances for the first established as the second Hi-Tech Components , in Miyota-machi, Nagano worldwide time into Thailand, the (Shanghai) Ltd. (our facility in Thailand Resonant devices Group’s largest first plant -

Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone?

IRLE IRLE WORKING PAPER #188-09 September 2009 Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone? James R. Lincoln, Masahiro Shimotani Cite as: James R. Lincoln, Masahiro Shimotani. (2009). “Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone?” IRLE Working Paper No. 188-09. http://irle.berkeley.edu/workingpapers/188-09.pdf irle.berkeley.edu/workingpapers Institute for Research on Labor and Employment Institute for Research on Labor and Employment Working Paper Series (University of California, Berkeley) Year Paper iirwps-- Whither the Keiretsu, Japan’s Business Networks? How Were They Structured? What Did They Do? Why Are They Gone? James R. Lincoln Masahiro Shimotani University of California, Berkeley Fukui Prefectural University This paper is posted at the eScholarship Repository, University of California. http://repositories.cdlib.org/iir/iirwps/iirwps-188-09 Copyright c 2009 by the authors. WHITHER THE KEIRETSU, JAPAN’S BUSINESS NETWORKS? How were they structured? What did they do? Why are they gone? James R. Lincoln Walter A. Haas School of Business University of California, Berkeley Berkeley, CA 94720 USA ([email protected]) Masahiro Shimotani Faculty of Economics Fukui Prefectural University Fukui City, Japan ([email protected]) 1 INTRODUCTION The title of this volume and the papers that fill it concern business “groups,” a term suggesting an identifiable collection of actors (here, firms) within a clear-cut boundary. The Japanese keiretsu have been described in similar terms, yet compared to business groups in other countries the postwar keiretsu warrant the “group” label least. -

Minebeamitsumi, Iwasaki Electric Began an Iot Street Lighting Joint Demonstration Experiment in Suginami Ward - LED Streetlights with Unique Wireless Connectivity

To whom it may concern February 18, 2020 MINEBEA MITSUMI Inc. IWASAKI ELECTRIC CO., LTD. MinebeaMitsumi, Iwasaki Electric Began an IoT Street Lighting Joint Demonstration Experiment in Suginami Ward - LED Streetlights with Unique Wireless Connectivity - MINEBEA MITSUMI Inc. (MinebeaMitsumi) and IWASAKI ELECTRIC CO., LTD. (Iwasaki Electric) recently were provided the Suginami Ward demonstration field, and launched the “IoT Streetlight Demonstration Experiment”, which pioneered the smart city project. The test site will be equipped with 11 smart streetlights and one environmental sensor near the north exit of Nishi-Ogikubo Station. A unique feature of this set up is that the streetlights equipped with our own wireless connectivity form a network so streetlights and sensors can be centrally managed. The smart LED road/streetlights jointly being developed by MinebeaMitsumi and Iwasaki Electric can freely control the amount of light via wireless communication, enabling monitoring of lighting status and power consumption, while streamlining operation management and reducing power costs at the same time. Furthermore, combining environmental sensors makes it possible to acquire various data, such as temperature, humidity, atmospheric pressure, wind speed, etc., and provide information services to residents. Through this project, we will contribute to energy and labor saving in Suginami Ward management, improvement of convenience for residents, and realization of safe and secure town development. [Installation Site] [Streetlight Information Monitoring Screen] Smart Streetlight Installation situation Environmental Sensor 1 [MinebeaMitsumi Smart City Solution] MinebeaMitsumi has developed a high efficiency LED streetlight with wireless functionality together with Iwasaki Electric with whom we have a business alliance, and been promoting the “Smart City” project since 2015. -

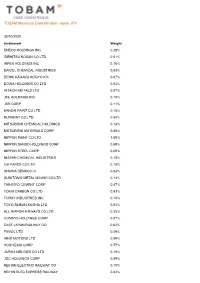

TOBAM Maximum Diversification Japan JPY

TOBAM Maximum Diversification Japan JPY 30/10/2020 Instrument Weight ENEOS HOLDINGS INC 0.28% IDEMITSU KOSAN CO LTD 0.51% INPEX HOLDINGS INC 0.16% DAICEL CHEMICAL INDUSTRIES 0.03% DENKI KAGAKU KOGYO K K 0.07% DOWA HOLDINGS CO LTD 0.04% HITACHI METALS LTD 0.07% JFE HOLDINGS INC 0.10% JSR CORP 0.11% KANSAI PAINT CO LTD 0.15% KURARAY CO LTD 0.04% MITSUBISHI CHEMICAL HOLDINGS 0.13% MITSUBISHI MATERIALS CORP 0.06% NIPPON PAINT CO LTD 1.09% NIPPON SANSO HOLDINGS CORP 0.59% NIPPON STEEL CORP 0.09% NISSAN CHEMICAL INDUSTRIES 0.18% OJI PAPER CO LTD 0.10% SHOWA DENKO K K 0.03% SUMITOMO METAL MINING CO LTD 0.13% TAIHEIYO CEMENT CORP 0.07% TOKAI CARBON CO LTD 0.83% TORAY INDUSTRIES INC 0.10% TOYO SEIKAN KAISHA LTD 0.04% ALL NIPPON AIRWAYS CO LTD 0.25% COMSYS HOLDINGS CORP 0.07% EAST JAPAN RAILWAY CO 0.02% FANUC LTD 0.49% HINO MOTORS LTD 0.05% HOSHIZAKI CORP 0.77% JAPAN AIRLINES CO LTD 0.16% JGC HOLDINGS CORP 0.09% KEIHAN ELECTRIC RAILWAY CO 0.10% KEIHIN ELEC EXPRESS RAILWAY 0.04% TOBAM Maximum Diversification Japan JPY 30/10/2020 Instrument Weight KEIO CORP 0.17% KINDEN CORP 0.05% KINTETSU CORP 0.20% KOMATSU LTD 0.06% KURITA WATER INDUSTRIES LTD 0.09% KYOWA EXEO CORP 0.06% KYUSHU RAILWAY COMPANY 0.08% LIXIL CORP 0.47% MABUCHI MOTOR CO LTD 0.05% MAKITA CORP 0.02% MITSUBISHI CORP 0.38% MITSUBISHI HEAVY INDUSTRIES 0.15% MIURA CO LTD 0.12% MONOTARO CO LTD 0.55% NAGOYA RAILROAD CO LTD 0.14% NIHON M&A CENTER INC 0.23% ODAKYU ELECTRIC RAILWAY CO 0.21% PARK24 CO LTD 0.48% SEIBU HOLDINGS INC 0.06% SEINO HOLDINGS CO LTD 0.05% SG HOLDINGS CO LTD 1.34% SHIMIZU -

![[IFRS] (Consolidated) (Year Ended March 31, 2021)](https://docslib.b-cdn.net/cover/2000/ifrs-consolidated-year-ended-march-31-2021-842000.webp)

[IFRS] (Consolidated) (Year Ended March 31, 2021)

BRIEF REPORT OF FINANCIAL RESULTS〔IFRS〕(Consolidated) (Year ended March 31, 2021) May 7, 2021 Registered Company Name: MINEBEA MITSUMI Inc. Common Stock Listings: Tokyo and Nagoya Code No: 6479 URL https://www.minebeamitsumi.com/ Representative: Yoshihisa Kainuma Representative Director, CEO & COO Contact: Mitsunobu Yamamoto General Manager of Accounting Department Date planned to hold ordinary general meeting of shareholders: June 29, 2021 Expected date of payment for dividends: June 30, 2021 Date planned to file report of securities: June 29, 2021 Phone: (03) 6758-6711 Preparation of supplementary explanation material for financial results : Yes Holding of presentation meeting for financial results : Yes(For Analyst) (Amounts less than one million yen have been rounded.) 1. Business Performance (April 1, 2020 through March 31, 2021) (1) Consolidated Results of Operations (%: Changes from previous fiscal year) Profit before Net sales % Operating income % % income taxes (millions of yen) Change (millions of yen) Change Change (millions of yen) Year ended March 31, 2021 988,424 1.0 51,166 (12.8) 49,527 (14.7) Year ended March 31, 2020 978,445 10.6 58,647 (18.6) 58,089 (18.6) Profit for the year Comprehensive Profit for % attributable to % income % the year Change owners of the parent Change for the year Change (millions of yen) (millions of yen) (millions of yen) Year ended March 31, 2021 38,787 (17.3) 38,759 (15.7) 68,308 177.8 Year ended March 31, 2020 46,923 (22.7) 45,975 (23.6) 24,593 (60.8) Profit to equity Profit before Earnings -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS Variable Portfolio – Partners International Value Fund, September 30, 2020 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 97.9% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Australia 4.2% UCB SA 3,232 367,070 AMP Ltd. 247,119 232,705 Total 13,350,657 Aurizon Holdings Ltd. 64,744 199,177 China 0.6% Australia & New Zealand Banking Group Ltd. 340,950 4,253,691 Baidu, Inc., ADR(a) 15,000 1,898,850 Bendigo & Adelaide Bank Ltd. 30,812 134,198 China Mobile Ltd. 658,000 4,223,890 BlueScope Steel Ltd. 132,090 1,217,053 Total 6,122,740 Boral Ltd. 177,752 587,387 Denmark 1.9% Challenger Ltd. 802,400 2,232,907 AP Moller - Maersk A/S, Class A 160 234,206 Cleanaway Waste Management Ltd. 273,032 412,273 AP Moller - Maersk A/S, Class B 3,945 6,236,577 Crown Resorts Ltd. 31,489 200,032 Carlsberg A/S, Class B 12,199 1,643,476 Fortescue Metals Group Ltd. 194,057 2,279,787 Danske Bank A/S(a) 35,892 485,479 Harvey Norman Holdings Ltd. 144,797 471,278 Demant A/S(a) 8,210 257,475 Incitec Pivot Ltd. 377,247 552,746 Drilling Co. of 1972 A/S (The)(a) 40,700 879,052 LendLease Group 485,961 3,882,083 DSV PANALPINA A/S 15,851 2,571,083 Macquarie Group Ltd. 65,800 5,703,825 Genmab A/S(a) 1,071 388,672 National Australia Bank Ltd. -

Fuji Seal Group Environment Report Vol.7 / New Approach to the Future

Fuji Seal International, INC. ENVIRONMENTAL REPORT Vol. 7 Fuji Seal Group New Approach to the Future in environmental sustainability.both customers and Oursociety’s packages initiatives contribute to R Plus Japan Ltd. - A new joint venture company that will invest in the development of cutting-edge recycling technology for used plastics Fuji Seal Group is proud to announce the establishment of R Plus Japan Ltd., a new joint venture company that will invest in the development of cut- ting-edge recycling technology for used plastics. R Plus Japan (CEO: Mr. Tsunehiko Yokoi, Location: Tokyo, Japan) was established in partnership with Fuji Seal, Inc. and 11 other cross-industry partners within the plastics supply chain in June, 2020. This collaboration aims to find effective solutions to ad- dress plastics waste issues to create a more sustainable society. Member partners include Suntory MONOZUKURI Expert Ltd., TOYOBO Co. Ltd., Rengo Co. Ltd., Toyo Seikan Group Holdings Ltd., J&T Recycling Corporation, Asahi Group Holdings Ltd., Iwatani Corporation, Dai Nippon Printing Co. Ltd., Toppan Printing Co. Ltd., Hokkaiseican Co. Ltd., and Yoshino Kogyosho Co. Ltd.. Our mission statement is “Each day, with renewed commitment, we create new value through packaging.” We are strengthening our ESG initiatives to form a better society and to make the company more sustainable. In par- ticular, we recognize that the environmental problem is an important issue for humanity, and our creativity and efforts should be made to manufac- ture products with environmental aspects in mind. We aim to contribute positively to the environment and society through our products such as like to introduce some of our efforts. -

Japan: Updates on Climate Change Policy Measures

Partnership for Market Readiness 17th Meeting of the Partnership Assembly (PA17) October 24-26, 2017, Hilton Hotel Tokyo, Tokyo, Japan Updates on Climate Change Policy Measures Dr. Akio Takemoto Director for International Strategy on Climate Change, Global Environmental Bureau, Ministry of the Environment 24 Oct. 2017 GHG Emissions Trends (1990-2015) Emissions by sector in FY 2015 (excluding LULUCF) Iindustrial Agriculture Waste Processes 1.6% and 2.5% 1,325 Product Use (IPPU) 7.1% -3.8% or more from FY2005 -26% from FY2013 Energy 88.7% (Source) National Greenhouse Gas Inventory Report of Japan (April, 2017), Note: The values of GHG emissions are based on the 2017 GHG inventory Global Warming Countermeasures Plan submission, which were revised from the values reported in the BR2. In the right pie chart, total is not equal 100% due to rounding. 2 (Source) General Energy Statistics of Japan (April, 2017) Trends of Energy Consumption and GHG Intensity Consumption of Energy Trends Final energy consumption energy Final 17,000 130 16,000 120 15,000the BR2. inventory submission, which revised were from the values reported in Note: 2017),Annual Report on Accounts National (Source) National Greenhouse Gas Inventory Report of Japan (April, 110 14,000 The values of GHG emissions are based on the 2017 GHG 100 13,000 GDP 90 12,000 GHG emissions GHG intensity of GDP of intensity GHG GDP of intensity GHG Index (FY1990=100)Index GHG intensity of GDP 80 Final energy consumption (PJ) consumption energy Final 11,000 10,000 70 1998 2005 2008 2015 1990 1991 -

Toyo Seikan Group CSR Report 2019

Toyo Seikan Group CSR Report 2019 CSR Ofce, Toyo Seikan Group Holdings, Ltd. Osaki Forest Bldg., 2-18-1 Higashi-Gotanda, Shinagawa-ku, Tokyo, 141-8627 Japan Tel. +81-3-4514-2303 Published in October 2019 Table of Contents Editorial Policy .............................................................................................................................................................. 2 Basic Report/Table of Contents .................................................................................................. 3 Company Profile............................................................... ......................................................................................... 4 Top Message ................................................................................................................................................................. 6 We will seriously look at the current situations regarding our eight material issues and commit ourselves to a continuous reform. CSR Management of Toyo Seikan Group ................................................................ 8 Environment Our Commitment to Global Environment ........................................................... 10 Open Up and Social Quality Assurance System ............................................................................................................... 16 Human Rights .............................................................................................................................................................. 18 Together -

Transparency Report 2019

Transparency Report 2019 2018 9 ______年 月 www.kpmg.com jp / / © 2019 KPMG AZSA LLC, a limited liability audit corporation incorporated under the Japanese Certified Public Accountants Law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Transparency Report 2019 1 1. Message from the local Senior Partner As a member of the KPMG network, KPMG AZSA LLC shares a common purpose - to Inspire Confidence, Empower Change – with member firms around the globe. Based on this purpose, we aim to establish the reliability of information through auditing and accounting services and support the change of companies and society towards sustainable growth. AZSA Quality 2019 introduces efforts at KPMG AZSA LLC to improve audit quality, the foundation of which is KPMG’s globally consistent audit quality. In this transparency report, we will additionally introduce KPMG’s system for ensuring audit quality. 2. Who we are 2.1 Our business 2.2 Our strategy KPMG AZSA LLC, a member firm of KPMG International, comprises Our firm’s mission is to ensure the reliability of information by approximately 6,000 people in major cities in Japan, providing audit, providing quality audit and accounting services as well as to attestation, and advisory services such as accounting advisory contribute to the realization of a fair society and healthy services, financial advisory services, IT advisory service and other development of our economy by empowering change. In order to advisory services for initial public offerings and the public sector. execute our firm’s mission, we have following vision: We also offer highly specialized professional services that address To be ‘The Clear Choice’ for our clients, people and society.