Embassy Property Developments Private Limited: Ratings Reaffirmed; Outlook Revised to Negative

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Embassy Office Parks REIT TRACK RECORD

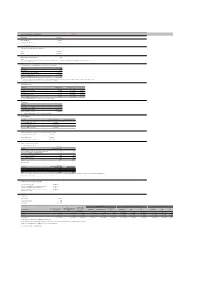

Embassy Office Parks REIT TRACK RECORD Name of the issue Embassy Office Parks REIT 1 Type of issue (IPO/ FPO/InvIT/REIT) Embassy Office Parks REIT 2 Issue size (Rs crore) 4,750.00 Source: Final Offer Document 27-Mar-19 3 Grade of issue alongwith name of the rating agency NA 4 Subscription level (number of times) 2.58x 2.58 is excluding anchor and stratgicand before removing multiple/duplicate bids and technical rejections. Amount of subscription includes all bids received within the price band of INR 299 to INR 300 per Unit Source: Basis of allotment 5 QIB holding (as a % of total outstanding capital) as disclosed to stock exchanges (i) allotment in the issue 79.6%* (ii) at the end of the 1st Quarter immediately after the listing of the issue (Jun 30, 2019) 17.00% (iii) at the end of 1st FY (31 March 2020) 17.00% (iv) at the end of 2nd FY (31 March 2021) 33.42% (v) at the end of 3rd FY (31 March 2022) NA** * Source: Basis of allotment (including strategic, anchor and institutional investor) ** The above data is not disclosed as reporting for the relevant fiscal years has not been completed 6 Financials of the issuer (Rs. in crores) Parameters FY2020 (1) FY2021 (1) FY2022 (2) Income from operations 2,145 2,360 - Net Profit for the period 766 698 - Paid-up equity share capital 22,912 28,826 - Reserves excluding revaluation reserves (594) (1,733) - Note: (1) Financials correspond to condensed consolidated financial statements of the REIT; Reserves are retained earnings only Note: (2) Financials are not disclosed as reporting for the relevant fiscal years has not been completed. -

Annual Deal List

Annual Deal List 16th annual edition Contents Section Page Mergers & Acquisitions 04 1. Domestic 05 2. Inbound 15 3. Merger & Internal Restructuring 18 4. Outbound 19 Private Equity 23 QIP 67 IPO 69 Disclaimer This document captures the list of deals announced based on the information available in the public domain. Grant Thornton Bharat LLP does not take any responsibility for the information, any errors or any decision by the reader based on this information. This document should not be relied upon as a substitute for detailed advice and hence, we do not accept responsibility for any loss as a result of relying on the material contained herein. Further, our analysis of the deal values is based on publicly available information and appropriate assumptions (wherever necessary). Hence, if different assumptions were to be applied, the outcomes and results would be different. This document contains the deals announced and/or closed as of 23 December 2020. Please note that the criteria used to define Indian start-ups include a) the company should have been incorporated for five years or less than five years as at the end of that particular year and b) the company is working towards innovation, development, deployment and commercialisation of new products, processes or services driven by technology or intellectual property. Deals have been classified by sectors and by funding stages based on certain assumptions, wherever necessary. Dealtracker editorial team Pankaj Chopda and Monica Kothari Our methodology for the classification of deal type is as follows: Minority stake - 1%-25% | Strategic stake - 26%-50% | Controlling stake - 51%-75% | Majority stake - 76%-99% Maps are for graphical purposes only. -

Morning Note Market Snapshot

Morning Note Market Snapshot February 26, 2021 Market Snapshot (Updated at 8AM) Key Contents Indian Indices Close Net Chng. Chng. (%) Market Outlook/Recommendation Sensex 51039.31 257.62 0.51 Today’s Highlights Nifty 15097.35 115.35 0.77 Global News, Views and Updates Global Indices Close Net Chng. Chng. (%) Links to important News highlight DOW JONES 31402.01 559.85 1.75 Top News for Today NASDAQ COM. 13119.43 478.54 3.52 FTSE 100 6651.96 7.01 0.11 HCL Technologies: HCL America Inc., a wholly-owned step-down subsidiary of the company has approved the proposal for issuance of U.S. Dollar denominated CAC 40 5783.89 14.09 0.24 unsecured notes aggregating to an amount not exceeding $500 million. The DAX 13879.33 96.67 0.69 Notes are backed by a corporate guarantee of the company. The guarantee is NIKKEI 225 29408.38 762.98 2.53 subject to the aggregate liability of the company not exceeding $525 million, (105 % of the principal amount of the notes). SHANGHAI 3511.69 64.50 1.80 Infosys: Has announced its commitment to add 300 American workers in HANG SENG 29228.64 823.18 2.74 Pennsylvania in continuation of its overall hiring plan in the U.S. The company will recruit for a range of opportunities across technology and digital services, Currency Close Net Chng. Chng. (%) client administration, and operations as it expands its new Retirement Services Center of Excellence. USD / INR 72.43 0.08 0.12 Bank of Baroda: The Board of Directors has approved raising of funds not USD / EUR 1.22 0.00 0.40 exceeding Rs 4,500 crore through issue of equity shares through qualified USD / GBP 1.40 0.01 0.48 institutional placement subject to the approval of the regulatory and statutory USD / JPY 106.16 0.16 0.15 authorities. -

Embassy Office Parks Reit

For private circulation only Book Built Issue Sr. No.: ____________ Addressed to: __________ Date: September 4, 2020 EMBASSY OFFICE PARKS REIT Registered in the Republic of India as an irrevocable trust under the Indian Trusts Act, 1882 and as a real estate investment trust under the Securities and Exchange Board of India (Real Estate Investment Trusts) Regulations, 2014, on August 3, 2017 at Bengaluru having registration number IN/REIT/17- 18/0001 Principal Place of Business: Royal Oaks, Embassy Golflinks Business Park, Off Intermediate Ring Road, Bengaluru 560 071, Karnataka, India Telephone No.: +91 80 3322 0000/ 2222; Fax No.: +91 80 4903 0046; E-mail: [email protected] Website: www.embassyofficeparks.com The Embassy Office Parks REIT (the “Issuer” or “Embassy REIT”) proposes to issue up to 15,000 (Fifteen Thousand) listed, rated, secured, redeemable, transferable, rupee denominated non-convertible debentures of face value of ₹1,000,000 (Indian Rupees One Million only) each, aggregating up to ₹1,500 crores (Indian Rupee One Thousand Five Hundred only ) (the “Debentures”) on a private placement basis, in one or more tranches, to be listed on the wholesale debt market (“WDM”) segment of the BSE Limited (“Stock Exchange” or “BSE”) (the “Issue”). The Issuer has obtained an ‘in-principle’ approval from the Stock Exchange for listing of the Debentures vide letter dated September 3, 2020. This disclosure document (the “Information Memorandum”) containing disclosures in accordance with Schedule I of the Securities and Exchange Board of India (Issue and Listing of Debt Securities) Regulations, 2008, as amended, is in relation to the issue of the first tranche of up to 7,500 (Seven Thousand Five Hundred) Debentures, aggregating up to ₹750 crores (Indian Rupee Seven Hundred Fifty crore only) on a private placement basis (“Tranche A Issue”) by the Embassy REIT. -

November 13, 2020 To, the Corporate Relations Department

November 13, 2020 To, The Corporate Relations Department The Corporate Relations Department The National Stock Exchange of India Ltd. Department of Corporate Services Exchange Plaza, 5th Floor, BSE Limited Plot No. C/1, G-Block, 25th Floor, Phiroze Jeejeebhoy Towers, Bandra-Kurla Complex, Dalal Street, Mumbai – 400001 Bandra (E), Mumbai - 400051 Re: Scrip Code 960165, 958770, 959074 and 959990; Scrip Code 542602 and Scrip Symbol “EMBASSY” Dear Sir/Madam, Subject: Submission of Half-Yearly Report Pursuant to Regulation 23(3) of the Securities and Exchange Board of India (Real Estate Investment Trusts) Regulations, 2014, we have enclosed the Half-Yearly Report with respect to the activities of Embassy Office Parks REIT for the period ended September 30, 2020. The Half-Yearly report referred above is also uploaded on our website at www.ir.embassyofficeparks.com. Kindly take the same on your record. Thank you Yours sincerely, For and on behalf of Embassy Office Parks REIT acting through its Manager, Embassy Office Parks Management Services Private Limited Deepika Srivastava Company Secretary and Compliance Officer A23654 Encl: As above Embassy Office Parks Management Services Pvt. Ltd. Embassy GolfLinks Business Park, Pebble Beach, Off Intermediate Ring Road, Bangalore – 560 071, India. T: +91 80 4903 0000 F: +91 80 4903 0046. www.embassyofficeparks.com I CIN: U70100KA2014PTC073362 Registered Office: Embassy Point, 1st Floor, 150, Infantry Road, Bangalore – 560 001. India T: +91 80 4179 9999 I F: +91 80 2228 6912 WHERE THE WORLD COMES TO -

Deal Watcher

DEAL WATCHER INDIA MARKET UPDATE FOR THE QUARTER ENDED JUNE 30, 2021 FOREWORD Dear Clients and Associates, After battling the second wave of the COVID pandemic, the Indian economy is starting to gain some semblance of normalcy by the end of H1 2021. The pandemic saw the focus of businesses shifting from growth to sustainability. Despite of all the deleterious effects of the pandemic, start-ups are seeing million-dollar fundraises at billion-dollar valuations. 2021 is turning out to be a landmark year for investments by private equity and venture capital funds. In six months, India has witnessed the creation of 16 unicorns, compared to just three in H1 2020. A major chunk of the total private equity investments was in technology enabled sectors, benefiting from increased digital adoption during the pandemic. The recent Zomato IPO indicates the heightened interest amongst retail investors and the same is mirrored by companies like Paytm who have rushed to file for going public. A gradual decrease in the infection rate and an aggressive vaccination push have brightened the near-term prospects for the economy but the rising inflation and fuel prices continue to remain a concern for the masses. In the quarter ended June, there were 476 private equity investments & venture capital investments with reported values of over US$ 15.52 bn. Byju’s, Swiggy and Mphasis walked away with a significant share (22% approximately) of the cumulative deal value. Key deals include: • EdTech giant Byju’s surpassed Paytm to become India’s most valued startup after a series F fundraise of US$ 1.48 bn during the quarter • Blackstone rolled over its stake in Mphasis Ltd to a separate fund triggering an open offer to acquire an additional 26% in the company. -

Exploring the New Investment World of REIT for Private Circulation Only March 2019 Exploring the New Investment World of REIT

Exploring the new investment world of REIT For private circulation only March 2019 Exploring the new investment world of REIT ii Exploring the new investment world of REIT Contents Introduction 2 REIT - Regulatory Landscape 7 REIT - Tax Landscape 11 Comparative Analysis 13 Competitive Benchmarking 15 Abbreviations 16 01 Exploring the new investment world of REIT Introduction What is REIT? REITs allow anyone to invest in portfolios These companies have to meet a number Overview of real estate assets the same way they of requirements to qualify as REITs. Real Estate Investment Trusts (REITs) invest in other industries – through the REITs are registered with the Securities are companies that own or finance purchase of individual company stock or and Exchange Board of India (SEBI) income-producing real estate in a range a mutual fund or exchange traded fund under SEBI (REITs) Regulations, 2014 of property sectors. They provide all (ETF). The stockholders of a REIT earn a (the Regulation) as amended from time investors the chance to own valuable real share of the income produced through to time. It is mandatory for units of all estate, present the opportunity to access real estate investment – without actually REITs to be listed on a recognised stock dividend-based income and total returns, having to go out and buy, manage or exchange having nationwide trading and help communities grow, thrive and finance property. terminals, whether publicly issued or revitalise. privately placed. Background Table: General Introduction Year Citation REIT Type REIT Market 26 September 2014 Securities and Exchange Board Trust As of this date, there are no registered Real Estate of India (Real Estate Investment Investment Trusts (‘REIT’) in India. -

Morning Insight

Morning Insight JUNE 25, 2020 % Chg News Highlights 24-Jun 1 Day 1 Mth 3 Mths International Monetary Fund (IMF) projects sharp contraction of Indian Indices 4.5% in Indian economy in 2020; a historic low citing the SENSEX Index 34,869 (1.6) 13.7 22.2 unprecedented coronavirus pandemic that has nearly stalled all NIFTY Index 10,305 (1.6) 14.0 23.9 NSEBANK Index 21,427 (3.8) 24.0 25.3 economic activities, but said the country is expected to bounce back NIFTY 500 Index 8,496 (1.5) 14.6 33.5 in 2021 with a robust 6% growth rate. The COVID-19 pandemic has CNXMcap Index 14,810 (1.4) 20.8 38.5 had a more negative impact on activity in the first half of 2020 than BSESMCAP Index 13,140 (1.1) 16.6 33.2 anticipated, and the recovery is projected to be more gradual than World Indices previously forecast. In 2021, global growth is projected at 5.4 per Dow Jones 25,446 (2.7) 4.0 20.0 cent, as per the report. (ET) Nasdaq 9,909 (2.2) 6.3 34.2 FTSE 6,124 (3.1) 2.2 7.7 Checks on Chinese imports throw domestic industry into tizzy: The NIKKEI 22,379 (0.7) 7.9 14.5 sudden move of the customs authorities to carry out 100% checks Hangseng 24,782 (0.5) 8.0 5.3 of import consignments coming from China at the ports has thrown Shanghai 2,980 - 6.0 7.0 the domestic industry into a tizzy at a time when it’s still far from full Value traded (Rs cr) 24-Jun % Chg Da recovery from the impact of lockdown. -

Accelerated Deployment of Renewable Energy Sector

Accelerated Deployment of Renewable Energy Sector Financial Instruments for catalyzing private sector investment for Indian RE sector Draft Report for Discussion Disclaimer This Report has been prepared on the basis set out in our contract for ‘Service Provider for Supporting Structural Reforms in the Indian Power Sector’ with the Secretary of State for International Development at the Department for International Development (“the Client”) dated 4 November 2016 (the “Services Contract”), and should be read in conjunction with the Services Contract. Nothing in this report constitutes a valuation or legal advice. We have not veried the reliability or accuracy of any information obtained in the course of our work, other than in the limited circumstances set out in the Services Contract. This Report is for the benet of the Client only. This Report has not been designed to be of benet to anyone except the Client. In preparing this Report we have not taken into account the interests, needs or circumstances of anyone apart from the Client, even though we may have been aware that others might read this Report. We have prepared this report for the benet of the Client alone. This Report is not suitable to be relied on by any party wishing to acquire rights against KPMG in India (other than the Client) for any purpose or in any context. Any party other than the Client that obtains access to this Report or a copy (under the Freedom of Information Act 2000, the Freedom of Information (Scotland) Act 2002, through the Client’s Publication Scheme or otherwise) and chooses to rely on this Report (or any part of it) does so at its own risk. -

Plots & Storeys

14 August 2020 FLASH UPDATE INDIA REAL ESTATE Plots & storeys India's weekly real estate news & numbers HIGHLIGHTS Blackstone set to acquire Prestige Group's assets Mall owners in Pune demand property tax waiver for US$ 1.7billion HSBC puts commercial building in South Embassy Group in talks with Indospace, ESR to Mumbai's Horniman Circle on the block monetise warehousing business ICICI Bank takes possession of Mantri SC reserves verdict on plea challenging NGT Developers' corporate office in Bengaluru order quashing EC for Godrej Reflections Have millions of homebuyers vanished? The Top realtors see spurt in take-over proposals for success of digital home sales says otherwise stressed office projects Japanese firm Amperex Technology Limited Sumitomo, Krishna group JV to invest INR 6.5bn acquires 180-acre at INR 5.5bn in Haryana in Gurugram township Delhi court pulls up Miniso Life Style for non- payment of rent CLICK HERE FOR Manish Agrawal [email protected] | Tel: (91 22) 6630 3068 LAST REPORT JM Financial Research is also available on: Bloomberg - JMFR <GO>, Thomson Publisher & Reuters S&P Capital IQ, FactSet and Visible Alpha. Please see Appendix I at the end of this report for Important Disclosures and Disclaimers and Research Analyst Certification. You can also access our portal www.jmflresearch.com JM FINANCIAL INSTITUTIONAL SECURITIES LIMITED India Real Estate 14 August 2020 We highlight this week’s top real estate news: Blackstone set to acquire Prestige Group's assets for US$ 1.7billion: Blackstone Group is set to acquire Prestige Group’s rental income assets for more than US$ 1.7billion in the largest real estate portfolio buyout in India, said three persons with direct knowledge of the matter. -

Real Estate Newsletter

AUGUST 2010 Real Estate Newsletter Editorial Contents Dear Reader, Industry News .......................................................2 The happy days are back. The Sensex has breached the Private Equity News .............................................5 psychological 20,000-barrier and is hovering near it. The rally is fuelled by high liquidity and huge inflows from Regulatory Buzz ...................................................6 overseas fund houses. Public Markets ......................................................7 Land Deals ...........................................................8 The bull-run in the Sensex has rubbed off to the realty market as well. According to a report by JLLM, the total Technology Parks/SEZs .......................................9 market value of real estate under construction in India has Hospitality .......................................................... 10 crossed the US$ 100 Bn mark for the first time in 2010. Of Commercial Properties ...................................... 12 this, Mumbai, where property prices are among the highest in the world, has nearly a 40% chunk. The residential Townships ......................................................... 13 component contributes 66% of this U$100 Bn, while the rest About Avendus Capital ...................................... 14 is contributed to by commercial office and retail space Contact Details .................................................. 14 combined. This growth is backed by a robust inflow of FDI, which has jumped a whopping 80 times between 2005 and 2010 from a mere US$ 40 Mn in 2005 to US$ 3,000 Mn in 2009-10. While the supply-side is steaming ahead, one needs to have a careful watch on the absorption rates. The threat of a supply overhang leaving a glut of inventory, especially in the high-end segment, is very real. Happy Reading! Avendus Real Estate Team Disclaimer: The news contained herein has been taken from published sources as indicated under each item. Avendus will not be held liable for any erroneous data as published in the source indicated. -

Embassy Office Parks REIT 17 July 2020 1 Type of Issue

Name of the Issue: Embassy Office Parks REIT 17 July 2020 1 Type of Issue IPO of REITs 2 Issue Size (Rs. Cr) 4,749.996 - Fresh Issue Size (Rs. Cr) 4,749.996 - Offer for Sale Component (Rs. Cr) - Source: Final Post Issue Report 3 Grade of issue along with name of the rating agency Name Not Applicable Grade Not Applicable 4 Subscription Level (Number of times) 1.6952 Notes: 1) The above figure is post elimination of bids for which the amounts were not blocked/ returned but before technical rejections. Excluding strategic and anchor investors Source: Final Post Issue Report 5 QIB Holding (as a %age of Outstanding Units) as disclosed to Stock Exchanges Particulars %age (i) On Allotment (1) 16.34% (ii) at the end of 1st FY (March 31, 2020) (2) Not available (iii) at the end of 2nd FY (March 31, 2021) (2) Not available (iv) at the end of 3rd FY (March 31, 2022) (2) Not available Note: (1) This is from the Basis of allotment (including strategic, anchor and institutional investor) where units were under the Issue. This does not include unitholding of the Sponsor entities. (2) QIB holding not disclosed as reporting for the fiscal year/ period has not been completed 6 Financials of the issuer Parameters 1st FY (FY 2020) 2nd FY (FY 2021) (1) 3rd FY (FY 2022) (1) Net Sales/ Income from operations 21,449.22 Not available Not available Net Profit 7,655.34 Not available Not available Paid up Equity Share Capital 2,29,120.96 Not available Not available Reserves excluding revaluation reserves (5,943.12) Not available Not available (1) Financials not