Peterhead / Buchan Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2006 No. 416 LOCAL GOVERNMENT The

SCOTTISH STATUTORY INSTRUMENTS 2006 No. 416 LOCAL GOVERNMENT The Aberdeenshire (Electoral Arrangements) Order 2006 Made - - - - 31st July 2006 Coming into force - - 11th August 2006 The Scottish Ministers, in exercise of the powers conferred by section 17(2) of the Local Government (Scotland) Act 1973(a) and giving effect to proposals submitted to them on 10th May 2006 by the Boundary Commission under section 17(1) of that Act regarding electoral arrangements for the area of Aberdeenshire Council, hereby make the following Order: Citation, commencement and application 1.—(1) This Order may be cited as the Aberdeenshire (Electoral Arrangements) Order 2006 and shall come into force on 11th August 2006. (2) This Order shall apply only for the purposes of elections to be held after the date on which section 1 of the Local Governance (Scotland) Act 2004(b) comes into force. Interpretation 2. In this Order– (a) a reference to an electoral ward is a reference to that electoral ward as constituted in this Order; and (b) “the deposited data” means the data recorded on the DVD-ROM– (i) entitled “Aberdeenshire (Electoral Arrangements) 2006”; and (ii) deposited with the Scottish Ministers at their offices at Victoria Quay, Leith, Edinburgh EH6 6QQ. Electoral arrangements 3.—(1) The area of Aberdeenshire Council shall be divided into 19 electoral wards. (2) The number and name of an electoral ward is as specified in columns 1 and 2 respectively of the Schedule to this Order. (3) The number of councillors to be returned for an electoral ward is as specified in the entry in column 3 of the Schedule to this Order corresponding to that electoral ward. -

Early Years Admission Handbook

1 From mountain to sea ApplyingRep for Early Learning and Childcare for Your Child Early Learning and Childcare Application Booklet for children born between st th 1 March 2016 – 28 Feb 2019 Session 2020–2021 2 | Applying for Early Learning and Childcare for Your Child Contents Glossary 3 What Can I Expect? 4 When is the application period for 2020/21? 4 How Can I Apply? 4 When Can My Child Start? 5 Local Authority 5 Funded Provider 6 What are Aberdeenshire Early Learning and Childcare settings offering? 6 What if my child has additional support needs? 6 What if my child is currently in an Early Learning and Childcare setting? 7 What happens next? 7 Local Authority Provision 7 Funded Providers 7 How are Early Learning and Childcare places allocated? 8 Transferring and Split Placements between Early Learning and Childcare settings 9 Purchasing additional sessions/wraparound care. 9 Deferred entry to Primary one 9 Aboyne Cluster 11 Alford Cluster 12 Banchory Cluster 13 Banff Cluster 14 Ellon Cluster 15 Fraserburgh Cluster 17 Huntly Cluster 18 Inverurie Cluster 19 Kemnay Cluster 20 Applying for Early Learning and Childcare for Your Child | 3 Laurencekirk Cluster 22 Meldrum Cluster 23 Mintlaw Cluster 25 Peterhead Cluster 27 Portlethen Cluster 29 Stonehaven Cluster 31 Turriff Cluster 33 Westhill Cluster 34 Aberdeenshire Council Early Years Enquiries 35 Family Information Service 35 Glossary Family Information Service The Family Information Service is a free, impartial service. It provides detailed information and advice on childcare, as well as a range of services for children aged 0- 19 and their families across Aberdeenshire https://families.scot/[email protected] Telephone: 0800 298 3330 Eligible Child 3 and 4 year old (for Early Learning and Childcare) Eligible Child means all children aged between 3 (the term after their third birthday) and up to school entry. -

Housing Land Audit 2014

Housing Land Audit 2014 Aberdeen City Council Aberdeenshire Council Housing Land Audit 2014 A joint publication by Aberdeen City Council and Aberdeenshire Council 1. Introduction 1.1 Purpose of Audit 1 1.2 Preparation of Audit 1 1.3 Housing Market Areas 3 1.4 Land Supply Denitions 4 2. Background to Housing Land Audit 2014 2.1 2014 Draft Housing Land Audit Consultation 5 2.2 Inclusion of Local Development Plan Sites 5 3. Established Housing Land Supply 3.1 Established Housing Land Supply 6 3.2 Greeneld / Browneld Land 7 4. Constrained Housing Land Supply 4.1 Constrained Housing Land Supply 8 4.2 Analysis of Constraints 9 4.3 Constrained Sites and Completions 10 5. Effective Housing Land Supply 5.1 Five Year Effective Supply 12 5.2 Post Five Year Effective Supply 13 5.3 Small Sites 14 5.4 Trends in the Effective Supply 15 6. Housing Requirement and Effective Supply 6.1 Housing Requirement and Effective Supply 17 7. Agreement on Effective Supply 7.1 Agreement on Effective Supply 18 8. Cairngorms National Park Sites 8.1 Cairngorms National Park Sites 19 Appendix 1 Glossary of Terms Denitions used in Housing Land Audit Tables Appendix 2 Detailed Statement of Established, Constrained and Effective Land Supply 2014 for Aberdeen City and Aberdeenshire Tables: - Aberdeen City - Aberdeenshire part of Aberdeen Housing Market Area - Aberdeenshire Rural Housing Market Area Appendix 3 Actual and Anticipated Housing Completions: - Housing Market Areas - Strategic Growth Areas - Aberdeenshire Settlements Appendix 4 Constrained Sites Appendix 5 Long Term Constrained Sites Published August 2014 Aberdeen City Council Aberdeenshire Council Enterprise, Planning & Infrastructure Infrastructure Services Business Hub 4 Woodhill House Ground Floor North Westburn Road Marischal College Aberdeen Broad Street AB16 5GB Aberdeen AB10 1AB 1. -

View Schedule

5 HILLVIEW, NEW PITSLIGO AB43 6JS 2 Bedroom Mid Terrace Property Recently Refurbished New Kitchen & Shower Room Lounge / Dining Room on Open Plan Partial E Rad Infrared Heating Open Countryside Views Offers Over £90,000 Home Report Valuation £90,000 www.stewartwatson.co.uk ACCOMMODATION Entrance Hall Lounge/Dining 18’5 x 10’10 (5.63m x 3.31m) Kitchen 13’0 x 7'3 (3.98m x 2.22m) Shower Room 7'7 x 5’3 (2.33m x 1.61m) Landing Bedroom 1 14’3 x 8’10 (4.36m x 2.71m) Bedroom 2 14’3 x 8’6 (4.36m x 2.59m) Please Note: All sizes taken at widest point TYPE OF PROPERTY Accessed by shared steps and path this property lies in a quiet cul-de-sac in an elevated position with excellent views over New Pitsligo and the surrounding countryside. The property has recently been refurbished to a high standard and has a new fitted kitchen and shower room. The property would be ideal for first time buyers and offers good accommodation for the price sought. There are UPVC windows and E Rad infrared Heating on the ground floor with electric panel heating in the bedrooms. The twin aspect lounge has countryside views to the front and a dining area to the rear. The newly fitted kitchen is fitted out with a mix of hi-gloss white & grey units with matching worktops and white metro tiled splash backs incorporating stainless steel extra bowl sink, ceramic hob with oven below and extractor above, integrated fridge, freezer and dishwasher and space and plumbing for a washing machine. -

THE PINNING STONES Culture and Community in Aberdeenshire

THE PINNING STONES Culture and community in Aberdeenshire When traditional rubble stone masonry walls were originally constructed it was common practice to use a variety of small stones, called pinnings, to make the larger stones secure in the wall. This gave rubble walls distinctively varied appearances across the country depend- ing upon what local practices and materials were used. Historic Scotland, Repointing Rubble First published in 2014 by Aberdeenshire Council Woodhill House, Westburn Road, Aberdeen AB16 5GB Text ©2014 François Matarasso Images ©2014 Anne Murray and Ray Smith The moral rights of the creators have been asserted. ISBN 978-0-9929334-0-1 This work is licensed under the Creative Commons Attribution-Non-Commercial-No Derivative Works 4.0 UK: England & Wales. You are free to copy, distribute, or display the digital version on condition that: you attribute the work to the author; the work is not used for commercial purposes; and you do not alter, transform, or add to it. Designed by Niamh Mooney, Aberdeenshire Council Printed by McKenzie Print THE PINNING STONES Culture and community in Aberdeenshire An essay by François Matarasso With additional research by Fiona Jack woodblock prints by Anne Murray and photographs by Ray Smith Commissioned by Aberdeenshire Council With support from Creative Scotland 2014 Foreword 10 PART ONE 1 Hidden in plain view 15 2 Place and People 25 3 A cultural mosaic 49 A physical heritage 52 A living heritage 62 A renewed culture 72 A distinctive voice in contemporary culture 89 4 Culture and -

ABERDEENSHIRE 04.Indd

Local Government Boundary Commission for Scotland Fourth Statutory Review of Electoral Arrangements Aberdeenshire Council Area Report E06002 Report to Scottish Ministers May 2006 Local Government Boundary Commission for Scotland Fourth Statutory Review of Electoral Arrangements Aberdeenshire Council Area Constitution of the Commission Chairman: Mr John L Marjoribanks Deputy Chairman: Mr Brian Wilson OBE Commissioners: Professor Hugh M Begg Dr A Glen Mr K McDonald Mr R Millham Report Number E06002 May 2006 Aberdeenshire Council Area 1 Local Government Boundary Commission for Scotland 2 Aberdeenshire Council Area Fourth Statutory Review of Electoral Arrangements Contents Page Summary Page 7 Part 1 Background Pages 9 – 14 Paragraphs Origin of the Review 1 The Local Governance (Scotland) Act 2004 2 – 4 Commencement of the 2004 Act 5 Directions from Scottish Ministers 6 – 9 Announcement of our Review 10 – 16 General Issues 17 – 18 Defi nition of Electoral Ward Boundaries 19 – 24 Electorate Data used in the Review 25 – 26 Part 2 The Review in Aberdeenshire Council Area Pages 15 – 24 Paragraphs Meeting with the Aberdeenshire Council 1 – 3 Concluded View of the Council 4 Aggregation of Existing Wards 5 – 7 Initial Proposals 8 – 14 Informing the Council of our Initial Proposals 15 – 16 The Aberdeenshire Council Response 17 – 18 Consideration of the Council Response to the Initial Proposals 19 – 21 Provisional Proposals 22 – 26 Representations 27 Consideration of Representations 28 – 38 Part 3 Final Recommendation Pages 25 – 26 Appendices Pages 27 -

Introduction to New Pitsligo & St. John's School

1 From mountain to sea New Pitsligo & St. John’s School Handbook 2018/19 2 |New Pitsligo & St. John’s School Contents Introduction to Ashire School Error! Bookmark not defined. Our Vision, Values and School Ethos Error! Bookmark not defined. Curriculum Error! Bookmark not defined. 1 1+2 Approach to Language Learning in AberdeenshireError! Bookmark not defined. 2 Further Information Error! Bookmark not defined. Assessment and Reporting Error! Bookmark not defined. Transitions (Moving On) Error! Bookmark not defined. 3 Admissions Error! Bookmark not defined. 4 Placing requests & School Zones Error! Bookmark not defined. 5 (S) Skills Development Scotland 14 6 Developing Young Workforce 14 Support for Children and Young People Error! Bookmark not defined. 7 Getting it Right for Every Child Error! Bookmark not defined. 8 The Named Person Error! Bookmark not defined. 9 Educational Psychology Error! Bookmark not defined. 10 Enhanced Provision & Community Resource HubsError! Bookmark not defined. 11 Support for Learning Error! Bookmark not defined. 12 The Child’s Plan Error! Bookmark not defined. 13 Child Protection Error! Bookmark not defined. 14 Further Information on Support for Children and Young PeopleError! Bookmark not defined. Parent & Carer Involvement and Engagement Error! Bookmark not defined. 15 Parental Involvement 20 16 Parental Engagement 20 17 Communication Error! Bookmark not defined. 18 Learning at Home 20 19 Parent Forum and Parent Council 21 20 Parents and School Improvement 21 21 Volunteering in school 21 22 Collaborating with the Community 21 School Policies and Useful Information Error! Bookmark not defined. 23 Attendance Error! Bookmark not defined. 24 Holidays during term time. Error! Bookmark not defined. -

A Stunning Six Bedroom Former Manse

A stunning six bedroom former manse Avaig, Crimond, Fraserburgh, Aberdeenshire, AB43 8QN Freehold A stunning six bedroom former manse with two traditional stone built outbuildings, situated within tranquil garden grounds of approximately 2.1 acres on the outskirts of the thriving village of Crimond. Ground floor: entrance vestibule • reception hall drawing room • sitting room • dining room • study Mezzanine floor: bedroom one • bathroom • wet room First floor: bedrooms two • three • four • five and six Lower ground floor: rear vestibule • WC cloakroom family room • dining kitchen • utility room • boot room • store gym with wine cellar off • boiler room EPC rating: Band E SUMMARY from where a partially glazed Situated within tranquil door leads into the welcoming grounds extending to reception hall. An impressive approximately 2.1 acres, Avaig curved staircase with ornate is a handsome six bedroom wrought iron balustrades and former manse. Category C timber handrail leads up to the Listed, the original early mezzanine and first floor Georgian part of the building is landings. Two stained glass understood to be around 200 windows provide plentiful years old, while the front natural light, while a door section of the property was beneath the main staircase constructed by James reveals a further staircase Henderson in 1845. The current which leads down to the lower owner has undertaken ground floor and basement. a significant programme of Within the spacious drawing renovation to restore this room a square bay window characterful property to its looks out onto the front garden former glory. Providing to the fields beyond. With spacious and versatile arched alcoves to either side of accommodation, a host of the striking open fireplace, this original features remain, is a warm and inviting public including deep skirtings and room. -

Term 1 Newsletter

MINTLAW ACADEMY Station Road, Mintlaw, Peterhead, AB42 5FN Tel: 01771 622994 Fax: 01771 624228 Absence Line: 01771 620000 Office Opening Hours 8.30am – 4pm E-mail: [email protected] Website: www.mintlawacademy.aberdeenshire.sch.uk NEWSLETTER: Term 1 2017/18 Introduction School Health Therapeutic Garden Online Payments House Challenge Alerts System Construction Visit Cashless Catering Charities New Alerts System Higher Geography Trip Absence Procedure Higher Modern Studies Trip Follow us on Twitter GCSE Geology Trip Groupcall messenger Sponsored Walk PTA Mega Draw Winners School Reunion Dates for your Diary 2017/18 Work Experience An Introduction from Mrs Duthie . It’s hard to believe we are at the end of Term 1 already. As ever this has been a very busy term at Mintlaw Academy. Our 17-18 Executive team of Rebecca Kindness, (Head Girl) Alastair Strachan, (Head Boy) Emily Findlay (Depute Head Girl) and Luke Michie (Depute Head Boy) head up a large team of House Captains, Sports Captains and their deputies. In conjunction with our prefect group, who are made up of a small number of S4 students as well as their S5-6 peers, our seniors have been working hard to support school events. Back in August, pupils celebrated another set of very strong results with eight S4 students gaining six Grade A National 5 Awards and three S5 students delighted to achieve straight A results across five Higher courses. Well done to them and to last year’s S4-S6 as a whole who worked hard and should be very proud of their results. Both our S4 and S6 results were the strongest for the past 6 years. -

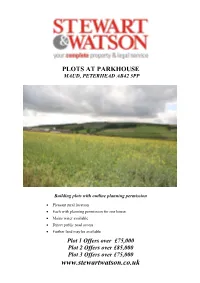

Plots at Parkhouse Maud, Peterhead Ab42 5Pp

PLOTS AT PARKHOUSE MAUD, PETERHEAD AB42 5PP Building plots with outline planning permission Pleasant rural location Each with planning permission for one house Mains water available Direct public road access Further land may be available Plot 1 Offers over £75,000 Plot 2 Offers over £85,000 Plot 3 Offers over £75,000 www.stewartwatson.co.uk PLOTS AT PARKHOUSE, MAUD, PETERHEAD ABERDEENSHIRE AB42 5PP GENERAL These three plots each have planning permission in principle for one house and garage. Further details of the planning permission can be viewed on line on Aberdeenshire Council's website www.Aberdeenshire.gov.uk/planning under reference numbers 2015/0926 (Plot 1) and 2015/0927 (Plot 2) and 2015/2585 (Plot 3). There is a mains water supply available close to the sites. Sewerage will be to septic tanks to be installed by the purchasers. All plots have direct public road access. LOCATION Parkhouse is located in pleasant rolling countryside off the road leading between the villages of Old Deer and Maud. The houses to be built will benefit from attractive countryside views. From Old Deer head towards Maud and turn off left at the signpost for Stone Circle. Alternatively, from Stuartfield head out Windhill Street and up past Scroghill and on to Parkhouse. Both Maud and Stuartfield offer village facilities with further more extensive amenities available at the popular Buchan village of Mintlaw. Entry By arrangement Offers All offers should be submitted in writing to Viewing our Mintlaw office Contact our Mintlaw office – 01771 622338 Reference Email HAB Email: [email protected] Plot 1 Plot 2 Plot 3 FREE VALUATION – We are pleased to offer a free and without obligation, valuation of your property. -

Genealogical Material on Microfilm

Genealogical material on microfilm Microfilmed genealogical material is held at the following locations: Area Library where microfilm located Aberdour Old Parish Registers HQ, Fraserburgh, 1841 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie, Macduff 1851 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie 1861 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie, Peterhead, Strichen 1871 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie 1881 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie 1891 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie 1901 Census HQ, Fraserburgh, Strichen Aberlour 1841 Census HQ, Fraserburgh, Macduff 1851 Census HQ, Fraserburgh, Macduff 1861 Census HQ, Fraserburgh, Macduff 1871 Census HQ, Fraserburgh, Macduff 1881 Census HQ, Fraserburgh, Macduff 1891 Census HQ, Fraserburgh, Macduff 1901 Census HQ, Macduff Aboyne and Glentanar Old Parish Registers HQ, Banchory, Stonehaven 1841 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie, Macduff 1851 Census HQ, Ellon, Huntly, Inverurie, 1861 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie, Peterhead, Strichen 1871 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie 1881 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie 1891 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie 1901 Census HQ, Fraserburgh, Strichen Alford Old Parish Registers HQ, 1841 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie, Macduff 1851 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie 1861 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie, Peterhead, Strichen 1871 Census HQ, Ellon, Fraserburgh, Huntly, Inverurie -

29 John Forman (1819-1906)

1 John Forman(1819-1906)=Margaret Bruce(1820-1906) JOHN FORMAN and MARGARET BRUCE (Written by Thomas Summers West 1927-2010) Name John Forman Margaret Bruce Born Wed. 4 Aug. 1819 Tues. 21 Nov. 1820 Place Buchanhaven, Peterhead. Peterhead. Married Sat. 9 May 1840, Buchanhaven, Peterhead, Aberdeenshire. Died Thurs. 25 Jan. 1906 Sat. 3 Feb. 1906 Place 6 Harbour St., Buchanhaven 6 Harbour St., Buchanhaven Buried Constitution St. Cemetery, Peterhead, both in Lair C108 Occupation Fisherman Parents:- Father John Forman Robert Bruce Mother Margaret Bruce Elizabeth Buchan _____________________________________________________________________ Children: John Forman May 1841 d July 1841 Elizabeth Forman 8 Sept 1842 d1927 William Forman 14 Jan.1847 d1922 Robert Forman 17 Jun.1849 Margaret Forman 14 Aug.1851 Jean Birnie Forman 10 Jan. 1854 d1935 James Forman 5 Mar 1856 d1918 Christian Ann Forman 24 Jan 1858 d1899 Alexander Jamieson Forman 24 Jan 1858 Joseph Forman 10 May 1860 d1931 ________________________________________________________________ 29 JOHN FORMAN (1819-1906) My great-grandfather John Forman was born/baptised on 4 August 1819, apparently the only child of his father John Forman and mother Margaret Bruce in the fishing village of Buchanhaven which was not then a part of Peterhead. The Peterhead OPR record of the event [1] reads:- ‘4th August 1819. John Forman, fisherman in Buchanhaven and Margaret Bruce his wife had a son baptised and named John’. When I started researching this part of my ancestry, I found it confusing that there were two John Forman’s one the son of the other who both married Margaret Bruce’s. To avoid confusion when both are being discussed together, I will call the father John Sr.