Presentation Title

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Finding Aid for the Collection on Frank Johnson, 1904-1957, Accession

Finding Aid for COLLECTION ON FRANK JOHNSON, 1904-1957 Accession 570 Finding Aid Published: January 2011 20900 Oakwood Boulevard ∙ Dearborn, MI 48124-5029 USA [email protected] ∙ www.thehenryford.org Updated: 1/10/2011 Collection on Frank Johnson Accession 570 SUMMARY INFORMATION COLLECTOR: Johnson, Russell F. TITLE: Collection on Frank Johnson INCLUSIVE DATES: 1904-1957 BULK DATES: 1904-1942 QUANTITY: 0.8 cubic ft. ABSTRACT: Collected diaries and oral interview transcripts relating to Frank Johnson’s automotive career with Leland and Faulconer, Cadillac Motor Company, Lincoln Motor Company, and Ford Motor Company. ADMINISTRATIVE INFORMATION ACCESS RESTRICTIONS: The papers are open for research ACQUISITION: Donation, 1956 PREFERRED CITATION: Item, folder, box, Accession 570, Collection on Frank Johnson, Benson Ford Research Center, The Henry Ford PROCESSING INFORMATION: Finding aid prepared by Pete Kalinski, April, 2005 2 Collection on Frank Johnson Accession 570 BIOGRAPHICAL NOTE Russell F. Johnson’s father, Frank Johnson, was born in Paris, Michigan in 1871 and attended local public schools and Michigan State College (now Michigan State University). After earning a degree in mechanical engineering in 1895, Frank Johnson worked as a tool designer and engineer with the Leland and Faulconer Company. Leland and Faulconer Company was a noted machine and tool shop started by Henry M. Leland in 1890 that supplied engines, transmission, and steering gear to the Henry Ford Company and later the Cadillac Motor Company. Leland and his son Wilfred C. Leland assumed control of Cadillac in 1902 and merged the companies. Johnson was instrumental in the key phases of early engine design at Cadillac. -

GM End of Lease Guide

END-OF-LEASE GUIDE GOOD THINGS SHOULD NEVER COME TO AN END. As the end of your current lease with GM Financial draws near, we’d like to thank you for your business, and we hope that you’ve had an excellent driving experience in your General Motors vehicle. To help guide you through the end-of-lease process, we’ve created this step-by- step guide. Or, visit gmfinancial.com/EndofLease. What should you do with your current TABLE OF CONTENTS leased GM vehicle? You have several options from which to choose: Your Lease-End Options 1 • Purchase or lease a new GM vehicle Trade in Your Vehicle 2 • Purchase your current leased vehicle Turn in Your Vehicle 2 • Turn in your leased vehicle Want to continue enjoying the GM driving experience? Select Your Next GM Vehicle 3 GM has many new and exciting models available. Check your mail in the coming weeks because you may become Schedule Your Inspection 4 eligible to receive incentives towards the purchase or lease of a new GM vehicle. Review Your Vehicle’s Condition 6 Frequently Asked Questions 11 What will you be driving this time next year? Contact Us 12 GM is consistently developing new and exciting models for our customers. Visit GM.com to check out Wear-and-Tear Card 13 new vehicles and determine which one fits your needs. YOUR LEASE-END OPTIONS Buick Envision Chevrolet Cruze Cadillac XT5 OPTION 1: OPTION 2: OPTION 3: TURN IN YOUR GM VEHICLE PURCHASE YOUR TURN IN YOUR GM VEHICLE AND PURCHASE OR LEASE LEASED GM VEHICLE Return the vehicle to the GM A NEW GM VEHICLE You can purchase your leased vehicle dealership where it was leased.* Are you ready for your next at any time during your lease period, Remember to bring your GM vehicle? Visit your nearest or you may do so near the end of your owner’s manual, extra set of GM dealer to test drive the lease. -

Preferred Employer Program Companies*

Preferred Employer Program Companies* • 3M Company • AutoZone • Cintas • 7-Eleven • Avera Health • Cisco Systems • AAA - (Employees Only) • Avon Products • Citigroup • Abbott Laboratories • Bacardi USA • Citizens Financial Group • AbbVie Corp. • Bank of America Corp. • Cleveland Clinic Foundation • Accenture Ltd. • Baptist Health South Florida • Coca-Cola Bottling Co. • adidas America • Barclays Capital/Stifel Financial • Coldwell Banker Richard Ellis • Advanced Micro Devices • Bausch & Lomb • Compass Group USA • Aflac - (Employees Only) • Bayer Corp. • ConocoPhillips • Alcon Laboratories • Becton, Dickinson and Company • Continental General Tire • ALDI • Berkshire Hathaway • Corning • Allegheny Health Network • BI Worldwide • Costco • Allergan • Biogen Idec • Cowan Systems • Alliance Data • BioReference Labs • Cox Enterprises • Allianz Global Investors of America • Bloomin’ Brands • Credit Suisse Asset Mgmt. • Allstate Insurance Co. - (Employees Only) • Blue Cross Blue Shield - (Employees Only) • CSRA International • Altice • Blue Iron • Cumberland Farms • Amazon • Boehringer Ingelheim Pharmaceuticals • Curtiss-Wright Corp. • American Airlines Credit Union • Boeing Corp. • CVS • American Association of Physicians • Boston Scientific Corp. • Daimler Trucks North America of Indian Origin • BP • Dassault Systèmes • American Express Co. - (Employees Only) • Braintree Laboratories • DealerTrack Holdings • AMETEK • Bristol Myers Squibb • Del Monte Foods • Amgen • Broadcom • Dell • Analog Devices • Brown-Forman • Deloitte & Touche LLP • Anthem -

2018 Annual Report

2018 ANNUAL REPORT 2018 ANNUAL REPORT AND FORM 20-F 2 2018 | ANNUAL REPORT 2018 | ANNUAL REPORT 3 Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes No Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes No Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and emerging growth company” in Rule 12b-2 of the Exchange Act. Large accelerated filer Accelerated filer Non-accelerated filer Emerging growth company If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing: U.S. -

Can Company 013230

PLEASE CONFIRM CSIP ELIGIBILITY ON THE DEALER SITE WITH THE "CSIP ELIGIBILITY COMPANIES" CAN COMPANY 013230 . Muller Inc 022147 110 Sand Campany 014916 1994 Steel Factory Corporation 005004 3 M Company 022447 3d Company Inc. 020170 4 Fun Limousine 021504 412 Motoring Llc 021417 4l Equipment Leasing Llc 022310 5 Star Auto Contruction Inc/Certified Collision Center 019764 5 Star Refrigeration & Ac, Inc. 021821 79411 Usa Inc. 022480 7-Eleven Inc. 024086 7g Distributing Llc 019408 908 Equipment (Dtf) 024335 A & B Business Equipment 022190 A & E Mechanical Inc. 010468 A & E Stores, Inc 018519 A & R Food Service 018553 A & Z Pharmaceutical Llc 005010 A A A - Corp. Only 022494 A A Electric Inc. 022751 A Action Plumbing Inc. 009218 A B C Contracting Co Inc 015111 A B C Parts Intl Inc. 018881 A Blair Enterprises Inc 019044 A Calarusso & Son Inc 020079 A Confidential Transportation, Inc. 022525 A D S Environmental Inc. 005049 A E P Industries 022983 A Folino Contruction Inc. 005054 A G F A Corporation 013841 A J Perri Inc 010814 A La Mode Inc 024394 A Life Style Services Inc. 023059 A Limousine Service Inc. 020129 A M Castle & Company 007372 A O N Corporation 007741 A O Smith Water Products 019513 A One Exterminators Inc 015788 A P S Security Inc 005207 A T & T Corp 022926 A Taste Of Excellence 015051 A Tech Concrete Co. 021962 A Total Plumbing Llc 012763 A V R Realty Company 023788 A Wainer Llc 016424 A&A Company/Shore Point 017173 A&A Limousines Inc 020687 A&A Maintenance Enterprise Inc 023422 A&H Nyc Limo / A&H American Limo 018432 A&M Supernova Pc 019403 A&M Transport ( Dtf) 016689 A. -

Ally Financial Inc., Resolution Plan, 2017

Ally Financial Inc. Resolution Plan Public Section December 31, 2017 1 Table of Contents Public Section I. Introduction ...................................................................................................................... 3 II. Overview of Ally............................................................................................................... 5 II.A. Names of Material Entities ....................................................................................... 8 II.B. Description of Core Business Lines ......................................................................... 9 II.C. Summary of Financial Information ........................................................................... 13 II.D. Description of Derivative and Hedging Activities...................................................... 21 II.E. Memberships in Material Payment, Clearing and Settlement Systems ................... 26 II.F. Description of Non-U.S. Operations ......................................................................... 27 II.G. Material Supervisory Authorities .............................................................................. 28 II.H. Principal Officers...................................................................................................... 29 II.I. Resolution Planning Corporate Governance Structure ............................................. 37 II.J. Description of Material Management Information Systems ...................................... 39 II.K. High-Level Description of Resolution Strategy........................................................ -

2021 UAW Union-Built Vehicle Guide

2021 UAW Union-Built Vehicle Guide UAW CARS UAW SUVS/CUVS UAW VANS Cadillac CT4 Buick Enclave Chevrolet Express Cadillac CT5 Cadillac Escalade Chevrolet Express (cut-away) Chevrolet Bolt (electric) Cadillac Escalade ESV Ford E-Series (cut-away) Chevrolet Camaro Cadillac Escalade Hybrid Ford Transit Chevrolet Corvette Cadillac XT4 GMC Savana Chevrolet Malibu Cadillac XT5 GMC Savana (cut-away) Chevrolet Sonic Cadillac XT6 Ford Mustang Chevrolet Suburban UNIFOR CARS Lincoln Continental Chevrolet Tahoe Chevrolet Tahoe (police) Chrysler 300 UAW TRUCKS Chevrolet Tahoe (special service) Dodge Challenger Chevrolet Traverse Dodge Charger Chevrolet Colorado Dodge Durango Chevrolet Medium-Duty Silverado Ford Escape UNIFOR SUVS/CUVS Navistar (regular and crew cab) Ford Expedition Chevrolet Equinox* Chevrolet Silverado Light Duty Ford Explorer Ford Edge (crew** and double cab only) GMC Acadia Lincoln Nautilus Chevrolet Silverado Heavy Duty GMC Yukon Ford F Series GMC Yukon Hybrid UNIFOR VANS Ford F-650/750 GMC Yukon XL Ford Ranger Jeep Cherokee Chrysler Pacifica Ford Super Duty Chassis Cab Jeep Grand Cherokee Dodge Grand Caravan GMC Canyon Jeep Wrangler GMC Sierra Light Duty Lincoln Aviator (crew** and double cab only) Lincoln Corsair GMC Sierra Heavy Duty Lincoln Navigator Jeep Gladiator Ram 1500 (classic model — DS)* Ram 1500 (new model — DT)* These vehicles are made in the United States or Canada by members of the UAW and Canada’s Unifor union, for- merly the Canadian Auto Workers (CAW). Because of the integration of vehicle production in both countries, all of the vehicles listed as made in Canada include significant UAW-made content and support the jobs of UAW members. -

Cadillac Ct6 Plug in Hybrid Certified Dealers

CADILLAC CT6 PLUG IN HYBRID CERTIFIED DEALERS Postal Facility Name Address City State Code Telephone CLASSIC BUICK GMC CADILLAC 833 EASTERN BOULEVARD MONTGOMERY AL 36117 (334) 277-3480 COULTER CADILLAC, INC. 1188 E CAMELBACK RD PHOENIX AZ 85014 (602) 264-1188 ROYAL BUICK-GMC-CADILLAC 815 W AUTO MALL DR TUCSON AZ 85705 (520) 624-0481 ARROWHEAD CADILLAC 8310 W BELL RD GLENDALE AZ 85308 (602) 942-4000 EARNHARDT CADILLAC 7901 EAST FRANK LLOYD WRIGHT BLVD SCOTTSDALE AZ 85260 (480) 483-4000 EARNHARDT CHANDLER CADILLAC 1450 S GILBERT RD CHANDLER AZ 85286 (480) 945-1200 VICTORY AUTO PLAZA, INC. 1360 AUTO CENTER DR PETALUMA CA 94952 (707) 762-2300 SMITH CHEVROLET CADILLAC, INC. 1601 AUTO MALL DR TURLOCK CA 95380 (209) 632-3946 STEWART CHEVROLET CADILLAC 780 SERRAMONTE BLVD COLMA CA 94014 (650) 994-2400 MARK CHRISTOPHER AUTO CENTER 2131 CONVENTION CENTER WAY SUITE A ONTARIO CA 91764 (909) 390-2900 RALLY BUICK GMC CADILLAC 39012 CARRIAGE WAY PALMDALE CA 93551 (661) 947-6000 PARADISE CADILLAC 27360 YNEZ RD TEMECULA CA 92591 (951) 699-2699 RELIABLE CADILLAC 400 AUTO MALL DR ROSEVILLE CA 95661 (916) 783-5233 ALLEN CADILLAC GMC 28332 CAMINO CAPISTRANO LAGUNA NIGUEL CA 92677 (949) 485-3700 JESSUP AUTO PLAZA 68111 EAST PALM CANYON DRIVE CATHEDRAL CITY CA 92234 (760) 328-9999 DUTTON MOTOR COMPANY 8201 AUTO DR RIVERSIDE CA 92504 (951) 687-2020 RANCHO MOTOR CO. 15425 DOS PALMAS RD VICTORVILLE CA 92392 (760) 955-8200 PARKWAY BUICK GMC CADILLAC 24055 CREEKSIDE ROAD VALENCIA CA 91355 (661) 253-4441 MARTIN AUTOMOTIVE GROUP 12101 W OLYMPIC BLVD LOS ANGELES CA 90064 (310) 820-3611 SYMES CADILLAC, INC. -

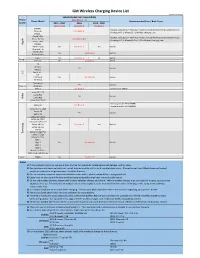

GM Wireless Charging Device List

GM Wireless Charging Device List Revision: Aug 30, 2019 Vehicle Model Year Compatibility Phone ( See Notes 1 - 7) Phone Model Recommended Case / Back Cover Brand 2015 - 2017 2018 2019 - 2020 (See Note 8) (See Note 8) (See Note 9) iPhone 6 ŸBEZALEL Latitude [Qi + PMA] Dual-Mode Universal Wireless Charging Receiver Case iPhone 6s See Note: A ŸAircharge MFi Qi iPhone 6S / 6 Wireless Charging Case iPhone 7 iPhone 6 Plus ŸBEZALEL Latitude [Qi + PMA] Dual-Mode Universal Wireless Charging Receiver Case e iPhone 6s Plus See Note: A & B l ŸAircharge MFi Qi iPhone 6S Plus / 6 Plus Wireless Charging Case p iPhone 7 Plus p A iPhone 8 iPhone X (10) No See Note: C Yes Built-in iPhone Xs / Xr iPhone 8 Plus No See Note: B Built-in iPhone Xs Max Pixel 3 No See Note: C Yes Built-in Google Pixel 3XL No See Note: B Built-in G6 Nexus 4 Yes Built-in Nexus 5 G Spectrum 2 L V30 V40 ThinQ No See Note: B Built-in G7 ThinQ Droid Maxx Yes Built-in Motorola Droid Mini Moto X See Note: A Incipio model: MT231 Lumia 830 / 930 a i Lumia 920 k Yes Built-in o Lumia 928 N Lumia 950 / 950 XL ŸSamsung model: EP-VG900BBU Galaxy S5 See Note: A ŸSamsung model: EP-CG900IBA Galaxy S6 / S6 Edge Galaxy S8 Yes Built-in Galaxy S9 Galaxy S10 / S10e Galaxy S6 Active Galaxy S7 / S7 Active g Galaxy S8 Plus No See Note: C Yes Built-in n u Galaxy S9 Plus s m S10 5G a Galaxy S6 Edge Plus S Galaxy S7 Edge Galaxy S10 Plus Note 5 Note 7 No See Note: B Built-in Note 8 Note 9 Note 10 / 10 Plus Note 10 5G / 10 Plus 5G Xiami MIX2S No See Note: B Built-in Notes: 1) If phone does not charge: remove it from charger for 3 seconds, rotate phone 180 degrees, and try again. -

The Ohio Motor Vehicle Industry

Research Office A State Affiliate of the U.S. Census Bureau The Ohio Motor Vehicle Report February 2019 Intentionally blank THE OHIO MOTOR VEHICLE INDUSTRY FEBRUARY 2019 B1002: Don Larrick, Principal Analyst Office of Research, Ohio Development Services Agency PO Box 1001, Columbus, Oh. 43216-1001 Production Support: Steven Kelley, Editor; Jim Kell, Contributor Robert Schmidley, GIS Specialist TABLE OF CONTENTS Page Executive Summary 1 Description of Ohio’s Motor Vehicle Industry 4 The Motor Vehicle Industry’s Impact on Ohio’s Economy 5 Ohio’s Strategic Position in Motor Vehicle Assembly 7 Notable Motor Vehicle Industry Manufacturers in Ohio 10 Recent Expansion and Attraction Announcements 16 The Concentration of the Industry in Ohio: Gross Domestic Product and Value-Added 18 Company Summaries of Light Vehicle Production in Ohio 20 Parts Suppliers 24 The Composition of Ohio’s Motor Vehicle Industry – Employment at the Plants 28 Industry Wages 30 The Distribution of Industry Establishments Across Ohio 32 The Distribution of Industry Employment Across Ohio 34 Foreign Investment in Ohio 35 Trends 40 Employment 42 i Gross Domestic Product 44 Value-Added by Ohio’s Motor Vehicle Industry 46 Light Vehicle Production in Ohio and the U.S. 48 Capital Expenditures for Ohio’s Motor Vehicle Industry 50 Establishments 52 Output, Employment and Productivity 54 U.S. Industry Analysis and Outlook 56 Market Share Trends 58 Trade Balances 62 Industry Operations and Recent Trends 65 Technologies for Production Processes and Vehicles 69 The Transportation Research Center 75 The Near- and Longer-Term Outlooks 78 About the Bodies-and-Trailers Group 82 Assembler Profiles 84 Fiat Chrysler Automobiles NV 86 Ford Motor Co. -

Car Wars 2020-2023 the Rise (And Fall) of the Crossover?

The US Automotive Product Pipeline Car Wars 2020-2023 The Rise (and Fall) of the Crossover? Equity | 10 May 2019 Car Wars thesis and investment relevance Car Wars is an annual proprietary study that assesses the relative strength of each automaker’s product pipeline in the US. The purpose is to quantify industry product trends, and then relate our findings to investment decisions. Our thesis is fairly straightforward: we believe replacement rate drives showroom age, which drives market United States Autos/Car Manufacturers share, which drives profits and stock prices. OEMs with the highest replacement rate and youngest showroom age have generally gained share from model years 2004-19. John Murphy, CFA Research Analyst Ten key findings of our study MLPF&S +1 646 855 2025 1. Product activity remains reasonably robust across the industry, but the ramp into a [email protected] softening market will likely drive overcrowding and profit pressure. Aileen Smith Research Analyst 2. New vehicle introductions are 70% CUVs and Light Trucks, and just 24% Small and MLPF&S Mid/Large Cars. The material CUV overweight (45%) will likely pressure the +1 646 743 2007 [email protected] segment’s profitability to the low of passenger cars, and/or will leave dealers with a Yarden Amsalem dearth of entry level product to offer, further increasing an emphasis on used cars. Research Analyst MLPF&S 3. Product cadence overall continues to converge, making the market increasingly [email protected] competitive, which should drive incremental profit pressure across the value chain. Gwen Yucong Shi 4. -

General Motors Is Formed William Durant Combined Buick, Olds

Charles H. Wright Museum of African American History 1908 General Motors is formed William Durant combined Buick, Olds, Cadillac, Elmore and Oakland to create what is now General Motors Incorporated. Durant offered different brands in order to target a broad market of incomes and preferences. In 1904, he invested in the Buick brand and used the 1 profits to buy out future automobile companies. Durant purchased Olds Motor Works, the first automobile company in Michigan and then Cadillac from Henry Leland, who previously reorganized the Henry Ford Company when Henry Ford resigned. Cadillac produced automobiles similar to Henry Ford’s Model A using methods of mass production Ford left behind. By 1910, Durant was forced to step down as management of General Motors. In 1914, he was able to buy back a 2 controlling interest in General Motors due to profits generated from the Chevrolet brand. 3 1 William Durant founded General Motors. Walter P. Reuther Library, Wayne State University, ID 20017 2 Chevrolet Automobile Courtesy of the National Automotive History Collection, Detroit Public Library 3 General Motors vehicles outside of liquor store Walter P. Reuther Library, Wayne State University, 19309_1_vmc The copyright law of the United States (Title 17, United States Code) restricts photocopying or reproduction of copyrighted material for anything other than “fair use.” “Fair use” includes private study, scholarship, research and non-profit educational purposes. If you wish to use an image from this website for a purpose other than “fair use” it is your responsibility to obtain permission from the copyright holder. While many images on this website are in the public domain, some are not.