The Future of Smartwatches – a Case on the Current Status and Expected Category Evolution on the Portuguese Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Predictive Fingerstroke-Level Model for Smartwatch Interaction

Multimodal Technologies and Interaction Article A Predictive Fingerstroke-Level Model for Smartwatch Interaction Shiroq Al-Megren ID Information Technology Department, King Saud University, Riyadh 12371, Saudi Arabia; [email protected]; Tel.: +966-11-805-7839 Received: 24 May 2018; Accepted: 25 June 2018; Published: 2 July 2018 Abstract: The keystroke-level model (KLM) is commonly used to predict the time it will take an expert user to accomplish a task without errors when using an interactive system. The KLM was initially intended to predict interactions in conventional set-ups, i.e., mouse and keyboard interactions. However, it has since been adapted to predict interactions with smartphones, in-vehicle information systems, and natural user interfaces. The simplicity of the KLM and its extensions, along with their resource- and time-saving capabilities, has driven their adoption. In recent years, the popularity of smartwatches has grown, introducing new design challenges due to the small touch screens and bimanual interactions involved, which make current extensions to the KLM unsuitable for modelling smartwatches. Therefore, it is necessary to study these interfaces and interactions. This paper reports on three studies performed to modify the original KLM and its extensions for smartwatch interaction. First, an observational study was conducted to characterise smartwatch interactions. Second, the unit times for the observed interactions were derived through another study, in which the times required to perform the relevant physical actions were measured. Finally, a third study was carried out to validate the model for interactions with the Apple Watch and Samsung Gear S3. The results show that the new model can accurately predict the performance of smartwatch users with a percentage error of 12.07%; a value that falls below the acceptable percentage dictated by the original KLM ~21%. -

Samsung Products (Wholesale and Retail)

PRICE LIST FOR SAMSUNG PRODUCTS (WHOLESALE AND RETAIL) Samsung S-Series Wholesale Retail Price Samsung Galaxy Note 20 Ultra 256GB 8GB $700 $1,100 Samsung Galaxy Note 20 256GB 8GB $600 $950 Samsung Galaxy S20 Ultra 128GB 12GB $600 $950 Samsung Galaxy S20+ 28GB 8GB $550 $850 Samsung Galaxy S20 128GB 8GB $500 $800 Samsung Galaxy Note10+ 5G 256GB $600 $950 Samsung Galaxy Note10+ 256GB $550 $850 Samsung Galaxy Note10 5G 256GB $500 $800 Samsung Galaxy Note10 256GB $450 $750 Samsung Galaxy S10 5G 128GB $500 $850 Samsung Galaxy S10+ 128GB $350 $600 Samsung Galaxy S10 128GB $260 $440 Samsung Galaxy Note 9 128GB $300 $500 Samsung Galaxy Note 8 64GB $280 $450 Samsung Galaxy S9 64GB $250 $420 Samsung Galaxy S8+ 64GB $220 $400 Samsung Galaxy S8 64GB $200 $350 Samsung Galaxy Note 7 64GB $180 $300 Samsung Galaxy S7 Edge 64GB $180 $300 Samsung Galaxy S7 64GB $150 $280 Samsung Galaxy S6 Edge + 64GB $120 $250 Samsung Galaxy S6 Edge Unlocked 64GB $110 $230 Samsung Galaxy S6 Unlocked 64GB $100 $200 Samsung A-Series Wholesale Retail Price Samsung Galaxy A70s 128GB $350 $550 Samsung Galaxy A20s 64GB $90 $150 Samsung Galaxy A30s 128GB $220 $400 Samsung Galaxy A50s 128GB $230 $430 Samsung Galaxy A90 5G 128GB $230 $430 Samsung Galaxy A90 128GB $250 $450 Samsung Galaxy A10s 64GB $100 $200 Samsung Galaxy A80 64GB $150 $250 Samsung Galaxy A70 64GB $120 $170 Samsung Galaxy A60 64GB $90 $150 Samsung Galaxy A50 128GB $120 $170 Samsung Galaxy A40 64GB $210 $380 Samsung Galaxy A30 64GB $70 $120 Samsung Galaxy A20e 64GB $170 $270 Samsung Galaxy A20 64GB $60 $100 Samsung -

Samsung Comes Full Circle with the Launch of Samsung Gear S2

Samsung Comes Full Circle with the Launch of Samsung Gear S2 Latest Samsung Gear features a versatile circular design for an intuitive, convenient and enjoyable mobile experience From left to right: Samsung Gear S2, Samsung Gear S2 classic Singapore, 15 September 2015 – Samsung Electronics Singapore today announced the Samsung Gear S2 smartwatch, a result of years of progressive innovation in the wearables category. The Samsung Gear S2 comes in a versatile, circular design with an intuitive, custom UX and advanced features that enable users to enhance, personalise and bring more fun to their mobile experience. The Gear S2’s unique rotating bezel, along with the Home and Back buttons, ensure users will have a quicker, more precise method to comfortably access notifications and applications. Specially designed for consumers with distinct preferences, the Gear S2 is available in two different options – the Gear S2 and the Gear S2 classic. The Gear S2 classic is made for users who prefer a more timeless watch design, offering an elegant Black finish with a matching genuine leather band. The Gear S2 is ideal for those who are on-the-go and have an admiration for minimal and modern design. “For several years, Samsung has advanced the wearables category, bringing brave new concepts to the smart wearables market,” said Eugene Goh, Vice President, IT & Mobile, Samsung Electronics Singapore. “The Samsung Gear S2 reflects our most progressive innovation, and serves as a strong testament to our relentless pursuit to push the boundaries in this category. We’ve designed the Gear S2 to complement the wearer’s style for any occasion – be it for day or night, from work to a night out – while making it smarter and ultimately more personal and fun.” A mere 11.4mm thin, the Samsung Gear S2 brings a light and compact design to your wrist. -

Did You Take a Break Today Detecting Playing Foosball Using

The Second IEEE International Workshop on Sensing Systems and Applications Using Wrist Worn Smart Devices, 2016 Did You Take a Break Today?: Detecting Playing Foosball Using Your Smartwatch Sougata Sen‡, Kiran K. Rachuri†, Abhishek Mukherji†, Archan Misra‡ ‡Singapore Management University and †Samsung Research America ‡{sougata.sen.2012,archanm}@smu.edu.sg, †{k.rachuri,a.mukherji}@samsung.com Abstract—Prolonged working hours are a primary cause of stress, work related injuries (e.g, RSIs), and work-life imbalance in employees at a workplace. As reported by some studies, taking timely breaks from continuous work not only reduces stress and exhaustion but also improves productivity, employee bonding, and camaraderie. Our goal is to build a system that automatically detects breaks thereby assisting in maintaining healthy work- break balance. In this paper, we focus on detecting foosball breaks of employees at a workplace using a smartwatch. We selected foosball as it is one of the most commonly played games at many workplaces in the United States. Since playing foosball involves wrist and hand movement, a wrist-worn device (e.g., a smartwatch), due to its position, has a clear advantage over a smartphone for detecting foosball activity. Our evaluation using data collected from real workplace shows that we can identify with more than 95% accuracy whether a person is playing foosball or not. We also show that we can determine how long a Fig. 1: Standard Foosball Table foosball session lasted with an error of less than 3% in the best case. cluded in smartwatches (e.g., Apple Watch, Samsung Gear S2). I. -

Samsung Gear S and S2 Heuristic Evaluation

Stephanie Wong Samsung Gear February 28, 2016 User Design Evaluation Report Samsung Gear S SECTION 1: INTRODUCTION This report is an evaluation of the smartwatch ‘Samsung Gear S’. It is designed and marketed by Samsung Electronics on August 28, 2014 and is the successor for Samsung Gear 2. Compared to the previous model, Samsung Gear S has a curved screen with a 360x480 resolution, a 300ppi Super AMOLED capacitive touch-screen that displays colors more vibrantly and bright. In this report, the smartwatch is analyzed for its usability and its compatibility with the Smartphone. Its interface is tested to see which tasks are supported successfully and to identify those tasks that have a need for improvement. These are listed with their severity level in our final results, along with recommendations on how to improve the user interface for future design solutions. My own opinion: SECTION 2: THE METHODOLOGY As ‘Heuristic Evaluation’ is considered to be used by single experts and is feasible – we used this as our design evaluation. The report is divided into two sections. The first half has the overall user experience- which is a higher categorization and review. The second half covers tasks users could perform or interact with the watch on a daily basis. The severity levels provided in each are indicators for the team to prioritize the tasks that should be addressed first. With each task, we have also provided corresponding recommendations. SECTION 3: RESULTS & INTERPRETATION Samsung Gear S has two main core features, one is to provide notifications and the other is to provide user access to their mobile phones. -

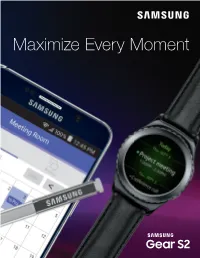

Maximize Every Moment the Future of Enterprise Productivity Is All in the Wrist

Maximize Every Moment The future of enterprise productivity is all in the wrist. Connect in an instant for better productivity. Empower your staff with the tools they need right at their wrists. The circular interface and unique rotating bezel of the Samsung Gear S2 enables an unobstructed view and faster access to relevant information. Navigating through apps and widgets quickly, employees can instantly share instructions and locations with each other; and with calendar reminders and intelligent notifications, they can efficiently manage their workday. Plus, activity tracking allows your employees to monitor their health and daily activities.* Increase efficiency around the clock. Give your team the power to keep going without interruption. The Samsung Gear S2 has an impressive battery life – with built-in wireless charging and the included wireless charging dock, it’s easy to keep powered up throughout the workday.† Once paired with a compatible Android™ phone, 3G or 4G2 standalone capability3 lets you make calls directly from your wrist – even when your phone isn’t close at hand4 – thanks to a built-in speaker and microphone. And with an IP68** rating, the Samsung Gear S2 has the durability to stand up to dust, dirt, water and sweat. Experience the freedom of versatility. The Samsung Gear S2 is more adaptable than ever with compatibility to many Android™ devices.*** After the initial setup, the Samsung Gear S2 can work on its own even if your phone isn’t nearby.4 And with on-board sensors, including an Accelerometer, Gyroscope, Barometer, Heart Rate Monitor and Ambient Light, your team can develop custom applications or select from the rapidly expanding Samsung Gear S2 third-party application ecosystem. -

Downloads/NASA TLX for Ios User Guide Final.Pdf

Long Short-Term Network Based Unobtrusive Perceived Workload Monitoring with Consumer Grade Smartwatches in the Wild a < a a Deniz Ekiz , , Yekta Said Can and Cem Ersoy aDepartment of Computer Engineering, Boğaziçi University, Istanbul, Turkey ARTICLEINFO ABSTRACT Keywords: Continuous high perceived workload has a negative impact on the individual’s well- smartwatch being. Prior works focused on detecting the workload with medical-grade wearable perceived workload detection systems in the restricted settings, and the effect of applying deep learning techniques physiological signal processing for perceived workload detection in the wild settings is not investigated. We present deep learning applications an unobtrusive, comfortable, pervasive and affordable Long Short-Term Memory Net- long short-term memory networks work based continuous workload monitoring system based on a smartwatch applica- tion that monitors the perceived workload of individuals in the wild. We make use of modern consumer-grade smartwatches. We have recorded physiological data from daily life with perceived workload questionnaires from subjects in their real-life en- vironments over a month. The model was trained and evaluated with the daily-life physiological data coming from different days which makes it robust to daily changes in the heart rate variability, that we use with accelerometer features to asses low and high workload. Our system has the capability of removing motion-related artifacts and detecting perceived workload by using traditional and deep classifiers. We dis- cussed the problems related to in the wild applications with the consumer-grade smart- watches. We showed that Long Short-Term Memory Network outperforms traditional classifiers on discrimination of low and high workload with smartwatches in the wild. -

SKU Bezeichnung Condition Country Price K3 Pack Samsung Gear S2 Sport Montre Connecte Blanc + Bracelet Bleu Marine Retourware FR

SKU Bezeichnung Condition Country Price K3 Pack Samsung Gear S2 Sport Montre Connecte Blanc + Bracelet Bleu Marine Retourware FR 111.51 € K3 Samsung Galaxy A3 (2016) Smartphone (4,7 Zoll (12,04 cm) Touch-Display, 16 GB Speicher, Android Retourware DE 84.61 € K3 Samsung Galaxy J3 2017 Or Retourware IT 50.89 € K3 Samsung Galaxy J510Smartphone, 16GB [Italien] Retourware IT 61.13 € K3 Samsung Galaxy Note 3 Smartphone (14,5 cm (5,7 Zoll) AMOLED-Touchscreen, 2,3GHz, Quad-Core, Retourware DE 113.44 € K3 Samsung Galaxy Note 4 Smartphone (5,7 Zoll (14,5 cm) Touch-Display, 32 GB Speicher, Android 4.4) Retourware DE 144.04 € K3 Samsung Galaxy Note 4 Smartphone (Wi-Fi, Bluetooth, USB, Android 4.4 KitKat), 32 GB schwarz Retourware FR 144.04 € K3 Samsung Galaxy S3 mini (GT-I8200) Smartphone (4 Zoll (10,2 cm) Touch-Display, 8 GB Speicher, Retourware DE 46.80 € K3 Samsung Galaxy S3Neo (-smartphone freies Android Display 4,7Zoll Kamera 8Megapixel 16GB Quad- Retourware IT 59.31 € K3 Samsung Galaxy S4 mini Smartphone (4,3 Zoll (10,9 cm) Touch-Display, 8 GB Speicher, Android 4.2) tief- Retourware DE 68.75 € K3 Samsung Galaxy S4 Smartphone (5 Zoll (12,7 cm) Touch-Display, 16 GB Speicher, Android 5.0) schwarz Retourware DE 82.16 € K3 Samsung Galaxy S8+, blau, 64 GB Retourware ES 226.55 € K3 Samsung Galaxy S8+, blau, 64 GB Retourware ES 226.55 € K3 Samsung Gear Fit 2 SM-R360 Smartwatch mit Pulssensor und Benachrichtigungen - Dunkelgrau (L) Retourware UK 61.20 € K3 Samsung Gear Fit 2 Smartwatch mit Pulssensor und Benachrichtigungen - Dunkelgrau (S) -

Investigating Current Techniques for Opposite-Hand Smartwatch Interaction

Investigating Current Techniques for Opposite-Hand Smartwatch Interaction Frederic Kerber1 Tobias Kiefer2 Markus Lochtefeld¨ 3 Antonio Kruger¨ 1 1German Research Center for Artificial Intelligence (DFKI) and 2Saarland University Saarland Informatics Campus, Saarbrucken,¨ Germany 3Department of Architecture, Design and Media Technology, Aalborg University, Aalborg, Denmark [email protected], [email protected], [email protected], [email protected] ABSTRACT The small display size of smartwatches creates a challenge for touch input, which is still the interaction technique of choice. Researchers and producers have started to investigate alterna- tive interaction techniques. Apple and Samsung, for example, introduced digital versions of classic watch components such as the digital crown and the rotatable bezel. However, it re- mains an open question how well these components behave in terms of user interaction. Based on a self-built smartwatch prototype, we compare current interaction paradigms (touch input, rotatable bezel and digital crown) for one-dimensional tasks, i.e. scrolling in a list, two-dimensional tasks, i.e. naviga- tion on a digital map, and a complex navigation/zoom task. To check for ecological validity of our results, we conducted an additional study focusing on interaction with currently avail- Figure 1. Smartwatch prototype consisting of our 3D-printed housing able off-the-shelf devices using our considered interaction including the mechanical components for the digital crown and the paradigms. Following our results, we present guidelines on rotatable bezel, a Moto 360 and the attached Raspberry Pi B+. which interaction techniques to use for the respective tasks. ACM Classification Keywords H.5.2 Information interfaces and presentation (e.g., HCI): User wrist and the forearm are most the desirable areas for wearable Interfaces devices [31]. -

Samsung Wearables, Smartthings and Reemo Help Older Adults Live Independently and Safely

Case Study: The Ohio Masonic Home Samsung Wearables, SmartThings and Reemo Help Older Adults Live Independently and Safely Overview Customer Need Samsung Solution Results To help older adults age respectfully, As part of a five-month pilot, 60 To determine the success of the pilot, the Ohio Masonic Home invests in residents at Ohio Masonic’s Springfield Ohio Masonic tracked three primary cutting-edge technology that improves campus tested a new technology from metrics: frequency of use, health medical care and quality of life for Reemo that combines the Samsung outcomes and resident satisfaction. residents. The organization has tried Gear S2 smartwatch and Samsung’s The solution is helping Ohio Masonic many remote monitoring solutions in SmartThings connected home reduce falls, proactively intervene the past, including pendants that alert technology. This solution enables when residents’ health declines staff when patients fall and in-home older adults to operate lights, locks, and boost patient satisfaction. Pilot cameras and sensors. But residents thermostats, televisions and other participants enjoyed using the solution often failed to adopt this technology, appliances with a flick of the wrist. and appreciate the opportunity to which can seem stigmatizing and Meanwhile, the Ohio Masonic staff provide feedback on cutting-edge intrusive. When evaluating new can remotely track biometric and technology. Ohio Masonic is already solutions, Ohio Masonic not only behavioral data in real time and spot layering this solution into two new wanted remote monitoring capabilities, potential health declines. developments that will be built in the but also products that help older next several years. adults maintain their sense of independence, as well. -

Device Functions Setting up Your Gear S2 Activating the Gear S2

Device Functions Setting Up Your Gear S2 Step 2. Turning Your Gear S2 Step 3. Pairing your Gear S2 to 4. Smartphone: Select the Gear S2 Activating the Gear S2 Home Screen Using the Bezel On and Off a smartphone model name. Once you have connected the Gear S2 to ¬ Press the Power/Home button at Rotate the Gear To turn ON the Gear S2, press and To connect your Gear S2 to your 5. Smartphone: When the Bluetooth Step 1. Charging the Gear S2 ¬ your smartphone, tap Activate on your anytime to return to the home screen. S2 bezel to the left QUICK REFERENCE MANUAL hold the Power/Home button. smartphone, install the Samsung Gear pairing request window is shown, ¬ Carefully place the Gear S2 on the Gear S2 and follow the instructions to set it to view messages app on your phone. tap OK. wireless charging dock and connect ¬ To turn OFF the Gear S2, press and up for standalone use. Moments Bar and notifications, or the dock to a power supply. hold the Power/Home button and For non-Samsung smartphones: From the home screen, swipe the to the right to see tap Power off. Download the Samsung Gear app from the screen down to view the notification panel. Settings and Apps. ™ Back Google Play store or the App Store. From here you can quickly forward calls, Button Compatible with Android 4.4 and later with 1.5GB adjust volume, display brightness and turn Bezel RAM. Some features may not be available. For best on the Do not disturb feature. -

Verso Modelli Predittivi Del Successo Dei Nuovi Prodotti: Un Approccio Sperimentale Sui Social Network

DIPARTIMENTO DI INGEGNERIA DELL’ENERGIA DEI SISTEMI, DEL TERRITORIO E DELLE COSTRUZIONI RELAZIONE PER IL CONSEGUIMENTO DELLA LAUREA MAGISTRALE IN INGEGNERIA GESTIONALE Verso Modelli Predittivi del Successo dei nuovi Prodotti: un approccio sperimentale sui Social Network RELATORI IL CANDIDATO Prof. Andrea Bonaccorsi Marco Del Pivo Dipartimento di Ingegneria dell' Energia dei Sistemi, [email protected] del Territorio e delle Costruzioni. Ing. Filippo Chiarello Dipartimento di Ingegneria Civile e Industriale. Sessione di Laurea del 22/02/2017 Anno Accademico 2016/2017 Consultazione consentita 1 2 Ringraziamenti Un ringraziamento particolare va a tutta la mia famiglia che mi ha sostenuto per tutto il percorso di studi e a tutte le persone che mi sono state vicine. Ringrazio inoltre il Dott. Andrea Cimino e l'Ing. Filippo Chiarello per il supporto nell'estrazione dei dati e nello svolgimento del lavoro di tesi. 3 Sommario La crescente competitività e rapidità di cambiamento del mercato sta portando le aziende a chiedere a progettisti e ingegneri di prodotto di creare idee che incontrino al meglio i bisogni del consumatore rendendo sempre più importante il processo di comprensione di ciò che gli utenti vogliono e desiderano. E' ben noto che una parte significativa dei nuovi prodotti introdotti sul mercato si rivela un fallimento commerciale. L'analisi di Big Data estratti da Social Network è ormai una pratica molto comune con un notevole impatto strategico, che permette di valutare le immediate reazioni del mercato per poter regolare azioni di marketing e di supporto. Le metodologie di analisi implementate fino ad adesso si basano su Sentiment Analysis, una tecnica che mostra le reazioni degli utenti al prodotto, ma non può dire con precisione se il prodotto stia rispondendo o meno ai bisogni dell'utente.