Usaid/Pakistan Non- Agricultural Value Chain Assessment

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rank-List-ET2020-Bed.Pdf

MAULANA AZAD NATIONAL URDU UNIVERSITY A Central University Accredited “A” Grade by NAAC Entrance Test 20 20 – Rank List (B.Ed.) General Hall Ticket Application No. Name Gender Category Sub Category PWD Type Rank 2023071098 M200011162 REBEKA SULTANA F 1 OBC 2023071067 M200007100 RIZWANA NAZ F 2 OBC 2018071061 M200004218 WAJIHA FIRDAUS F 3 General 2018071137 M200007779 SHAISTA PERWEEN F 4 OBC 2023071046 M200004137 MD USMAN GANI M 5 OBC 2025071033 M200005610 AISHA TUFAIL F 6 General 2023071070 M200007411 MUSAWWIR REZA M 7 OBC 2018071068 M200004542 SAUBIA TASNEEM AAFAQEE F 8 General EWS 2011071009 M200004583 DARAKHSHAN IQUBAL F 9 OBC 2023071105 M200012109 TARIQUE HASAN M 10 General 2023071103 M200011551 SAHIBA NASREEN F 11 OBC 2025071023 M200004206 MD FAIZ AZAM M 12 OBC 2018071154 M200008867 SYED SALEEMULLAH M 13 General 2018071078 M200005012 MD EHTESHAMUDDIN M 14 OBC 2018071077 M200004908 FATIMA ZOHRA F 15 OBC 2018071006 M200000730 AAISHA BAKHTEYAR F 16 General 2011071007 M200004189 MAHJABEEN F 17 General 2023071091 M200009893 HAZIQUE SHADAN M 18 General Page 1 of 159 MAULANA AZAD NATIONAL URDU UNIVERSITY A Central University Accredited “A” Grade by NAAC Entrance Test 20 20 – Rank List (B.Ed.) General Hall Ticket Application No. Name Gender Category Sub Category PWD Type Rank 2026071007 M200011969 AZRA ISLAM F 19 OBC 2018071027 M200002690 DARAKHSHAN NASEER F 20 OBC 2025071046 M200007540 SHAISTA SABA F 21 OBC 2018071049 M200003703 NIKHAT PARWEEN F 22 OBC 2025071040 M200006517 SANA FATMA F 23 OBC 2023071048 M200004171 MD RAUNAQUE HAYAT M 24 -

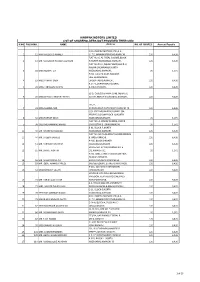

Hinopak Motors Limited List of Shareholders Not Provided Their Cnic S.No Folio No

HINOPAK MOTORS LIMITED LIST OF SHAREHOLDERS NOT PROVIDED THEIR CNIC S.NO FOLIO NO. NAME Address NO. OF SHARES Amount Payable C/O HINOPAK MOTORS LTD.,D-2, 1 12 MIR MAQSOOD AHMED S.I.T.E.,MANGHOPIR ROAD,KARACHI., 120 6,426 FLAT NO. 6, AL-FAZAL SQUARE,BLOCK- 2 13 MR. MANZOOR HUSSAIN QURESHI H,NORTH NAZIMABAD,KARACHI., 120 6,426 FLAT NO.19-O, IQBAL PLAZA,BLOCK-O, NAGAN CHOWRANGI,NORTH 3 18 MISS NUSRAT ZIA NAZIMABAD,KARACHI., 20 1,071 H.NO. E-13/40,NEAR RAILWAY LINE,GHARIBABAD, 4 19 MISS FARHAT SABA LIAQUATABAD,KARACHI., 120 6,426 R.177-1,SHARIFABADFEDERAL 5 24 MISS TABASSUM NISHAT B.AREA,KARACHI., 120 6,426 52-D, Q-BLOCK,PAHAR GANJ, NEAR LAL 6 28 MISS SHAKILA ANWAR FATIMA KOTTHI,NORTH NAZIMABAD,KARACHI., 120 6,426 171/2, 7 31 MISS SAMINA NAZ AURANGABAD,NAZIMABAD,KARACHI-18. 120 6,426 C/O. SYED MUJAHID HUSSAINP-394, PEOPLES COLONYBLOCK-N, NORTH 8 32 MISS FARHAT ABIDI NAZIMABADKARACHI, 20 1,071 FLAT NO. A-3FARAZ AVENUE, BLOCK- 9 38 SYED MOHAMMAD HAMID 20GULISTAN-E-JOHARKARACHI, 20 1,071 B-91, BLOCK-P,NORTH 10 40 MR. KHURSHID MAJEED NAZIMABAD,KARACHI. 120 6,426 FLAT NO. M-45,AL-AZAM SQUARE,FEDRAL 11 44 MR. SALEEM JAWEED B. AREA,KARACHI., 120 6,426 A-485, BLOCK-DNORTH 12 51 MR. FARRUKH GHAFFAR NAZIMABADKARACHI. 120 6,426 HOUSE NO. D/401,KORANGI NO. 5 13 55 MR. SHAKIL AKHTAR 1/2,KARACHI-31. 20 1,071 H.NO. 3281, STREET NO.10,NEW FIDA HUSSAIN SHAIKHA 14 56 MR. -

Federal Urdu University of Arts, Sciences & Technology

Degree Year Of Student Selection Campus Department Title Study Full Name Father Name CNIC Degree Title CGPA Status Merit Status Islamabad Applied Physics Bachelors 1 Khizra Khalil Khalil Ahmed Bajwa 6110152362736 BS (Hons) 3.2 Selected Student Eligible Islamabad Applied Physics Bachelors 1 ANAM ZHARA SYED AKHTER HUSSAIN SHAH 3740319867784 BS (Hons) 3.3 Selected Student Eligible Islamabad Applied Physics Bachelors 1 masood ur rehman Rehan shah 2140792271819 BS (Hons) 3.16 Selected Student Eligible Islamabad Applied Physics Bachelors 1 Muhammad Irfan Allah Dewaya 3220336130281 BS (Hons) 3.6 Selected Student Eligible Islamabad Applied Physics Bachelors 1 Ahsan Iftikhar Iftikhar Ahmad 3720114487337 BS (Hons) 3.58 Selected Student Eligible Islamabad Applied Physics Bachelors 1 Qurat Ul Ain Aziz Ullah Khan 3830101789040 BS (Hons) 3.18 Selected Student Eligible Islamabad Applied Physics Bachelors 1 Muhammad Majid Muhammad Faridoon 3740589951603 BS (Hons) 3.51 Selected Student Eligible Islamabad Applied Physics Bachelors 1 Abdul Manan Muhammad Saleem 3740341694235 BS (Hons) 3.88 Selected Student Eligible Islamabad Applied Physics Bachelors 1 Muhammad Awais Muhammad Saeed 3710293250617 BS (Hons) 3.55 Selected Student Eligible Islamabad Applied Physics Bachelors 1 MAYA SYED SYED TAFAZUL HASSAN 6110194455878 BS (Hons) 3.7 Selected Student Eligible Islamabad Applied Physics Bachelors 1 Mehreen Bibi Faqar Din 8220209594876 BS (Hons) 3.2 Selected Student Eligible Islamabad Applied Physics Bachelors 1 AMBREEN SAFDAR MALIK SAFDAR HUSSAIN 6110192701214 -

64 Pakistani Artists, 30 and Under

FRESH! 64 Pakistani Artists, 30 and Under Amin Gulgee Gallery Karachi March 2014 Curated by Raania Azam Khan Durrani Saba Iqbal Amin Gulgee Amin Gulgee Gallery Amin Gulgee launched the Amin Gulgee Gallery in the spring of 2002, was titled Uraan and in 2000 with an exhibition of his own sculpture, was co-curated by art historian and founding Open Studio III. The artist continues to display editor of NuktaArt Niilofur Farrukh and gallerist his work in the Gallery, but he also sees the Saira Irshad. A thoughtful, catalogued survey need to provide a space for large-scale and of current trends in Pakistani art, this was an thematic exhibitions of both Pakistani and exhibition of 100 paintings, sculptures and foreign artists. The Amin Gulgee Gallery is a ceramic pieces by 33 national artists. space open to new ideas and different points of view. Later that year, Amin Gulgee himself took up the curatorial baton with Dish Dhamaka, The Gallery’s second show took place in an exhibition of works by 22 Karachi-based January 2001. It represented the work created artists focusing on that ubiquitous symbol by 12 artists from Pakistan and 10 artists of globalization: the satellite dish. This show from abroad during a two-week workshop in highlighted the complexities, hopes, intrusions Baluchistan. The local artists came from all and sheer vexing power inherent in the over Pakistan; the foreign artists came from production and use of new technologies. countries as diverse as Nigeria, Holland, the US, China and Egypt. This was the inaugural In 2003, Amin Gulgee presented another major show of Vasl, an artist-led initiative that is part exhibition of his sculpture at the Gallery, titled of a network of workshops under the umbrella Charbagh: Open Studio IV. -

![Pagina 1 Van 2 Business Recorder [Pakistan's First Financial Daily] 27](https://docslib.b-cdn.net/cover/5586/pagina-1-van-2-business-recorder-pakistans-first-financial-daily-27-1405586.webp)

Pagina 1 Van 2 Business Recorder [Pakistan's First Financial Daily] 27

Business Recorder [Pakistan's First Financial Daily] pagina 1 van 2 Friday March 27, 2009 Back Issues [From 2004-01-01] 2009-03-27 Get LATEST : Bomb at Khyber Agency mosque, at least 45 de- Top Stories . Business & Economy - Stocks & Bonds Monsanto may be allowed to introduce hybrid, Bt Jobs in pakistan General News cottonseed varieties Middle East Job Editorials ASMA RAZAQ Opportunities. Upload ISLAMABAD (March 19 2009): The Economic Co-ordination Articles & Letters your Resume now: Free! Committee (ECC) of the Cabinet may approve plan to allow www.Bayt.com Cotton & Textiles Monsanto introduce both hybrid and Bt cottonseed varieties in Pakistan. Reliable sources told Business Recorder here on Agriculture & Allied Wednesday that the Ministry of Food and Agriculture (Minfa) had Fuel & Energy decided to move a summary to ECC meeting on Thursday (March Karachi Hotels Money & Banking 19) for giving permission to Monsanto to introduce hybrid and the Bt cotton seed varieties in Pakistan. One-stop source to Telecommunication compare hotel room rates IT & Computers According to the sources, after the ECCs approval, an agreement from across the web. would be signed between the government and Monsanto. The www.OneTime.com Taxation government had signed a LoI with Monsanto a year ago to Company News collaborate in biotechnology. Monsanto cotton traits are currently approved in 13 countries of the world. Stock & Funds Rates & Schedules Research Sports Sources said that Monsanto had demanded 16 dollars per acre as Get Insights with Weather royalty, which, according to Pakistan, was a huge amount. The Morningstar. 4000 government was not ready to pay even a single penny to Monsanto Reports with Free 14 Day that is why even after signing the LoI, Pakistan has not finalised the The Rupee agreement with Monsanto. -

Dalda Foundation Scholarships List of 400 Selected Candidates of DFT Category 2017-2018 S.No

Dalda Foundation Scholarships List of 400 selected candidates of DFT category 2017-2018 S.No. Name Father’s Name Marks Test Name of Beneficiary Contact # in Score Matric PESHAWAR 1 Abdul Muqtadar Abdul Khaliq 1044 47 Mohammad 923108687030 Afrasiyab 2 Muhammad Junaid Tahir Sartaj 1039 47 Tahir Sartaj 923409377135 3 Sajjad Anwar Muhammad Sher 1035 47 Muhammad Sher 923499127196 4 Mishkat Ullah Inam Ullah 1035 47 Inam Ullah 923489516785 5 Mehak Saeed Rehman Saeed 1049 46 Dr Rehman Saeed 923139913901 6 Mohammad Afrasiyab Muhammad Iqbal 1044 45 Mohammad 923161189935 Afrasiyab 7 Muhammad Khuzaifa Inayat ullah 1035 45 Muhammad Shafiq 923471979242 8 Ismail Khan Musammar Khan 1022 44 Raham Dil 923425096707 9 Ameer Hamza Hamid Ali 1021 44 Zohaib Hassan 923135308980 10 Muhammad Farooq Ikram ullah 1035 44 Ikram ullah 923449669345 11 Haseeb Ullah Lateef Ullah 1034 44 Lateef Ullah 923415692946 12 Aizaz Ahmad Fazali Dayan 1019 44 Fazali Dayan 923178118355 13 Muhammad Imran Shah Daraz 1018 44 Bashir Ahmad 923155031266 14 Taimoor Islam Noor Ul Islam 1018 44 Noor Ul Islam 923115580791 15 Javid Iqbal Zar Khan 1015 44 Shakeela Begum 923454534638 16 Mohammad Shareef Ullah 1021 43 Shareef Ullah Khan 923048953091 Qinwanullah Khan 17 Ahmad Istiraj Istiraj Khan 1021 43 Kalsoom Rani 923158233799 18 Ziyad Ali Liaqat Ali 1043 43 Salma Begum 923139625728 19 Hafiz Shayan Ahmad Jaanis Khan 1041 43 Zeeshan Ahmad 923318131819 20 Bashir Ahmad Muhammad Uzair 1036 43 Izhar Ullah 923499282132 21 Mansoor Iqbal Iqbal Akbar 1036 43 Iqbal Akbar 923498927178 KOHAT 22 Wajid ullah -

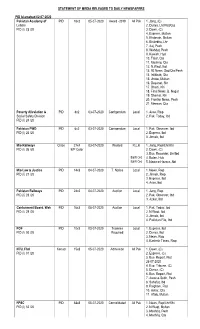

Statement of Media Released to Daily Newspapers Pid

STATEMENT OF MEDIA RELEASED TO DAILY NEWSPAPERS PID Islamabad 02-07-2020 Pakistan Academy of PID 18x2 05-07-2020 Award -2019 All Pak 1. Jang, (C) Letters 2. Dunya, Lhr/Fbd/Guj PID (I) 23 /20 3. Dawn, (C) 4. Express, Multan 5. Khabrain, Multan 6. Bhulekha, Lhr 7. Aaj, Pesh 8. Wahdat, Pesh 9. Kawish, Hyd 10. Talar, Qta 11. Mashriq, Qta 12. N.Waqt, Ibd 13. 92 News, Sgd/Qta/Pesh 14. Intikhab, Qta 15. Jhoke, Multan 16. Deyanat, Skr 17. Dharti, Khi 18. Final News, B. Nagar 19. Shamal, Khi 20. Frontier News, Pesh 21. Meezan, Qta Poverty Alleviation & PID 8x2 03-07-2020 Corrigendum Local 1. Asas, Rwp Social Safety Division 2. Pak. Today, Ibd PID (I) 24 /20 Pakistan PWD PID 6x2 03-07-2020 Corrigendum Local 1. Pak. Observer, Ibd PID (I) 25 /20 2. Express, Ibd 3. Jinnah, Ibd M/o Railways Circle 27x4 03-07-2020 Wanted R.L.K 1. Jang, Rwp/Lhr/Khi PID (I) 26 /20 B/P Color 2. Dawn, (C) 3. Bus. Recorder, Lhr/Ibd B&W Ord 4. Bolan, Hub B&W Ord 5. Nawa-e-Hazara, Abt M/o Law & Justice PID 14x3 04-07-2020 T. Notice Local 1. News, Rwp PID (I) 27 /20 2. Jinnah, Rwp 3. Express, Ibd 4. Asas, Ibd Pakistan Railways PID 24x2 04-07-2020 Auction Local 1. Jang, Rwp PID (I) 28 /20 2. Pak. Observer, Ibd 3. Azkar, Ibd Cantonment Board, Wah PID 16x3 08-07-2020 Auction Local 1. Pak. Today, Ibd PID (I) 29 /20 2. -

Pakistan Culture CLASSES XI-XII

Higher Secondary School Certificate Examination Pakistan Culture CLASSES XI-XII (based on National Curriculum 2002) Published by Aga Khan University Examination Board Bungalow # 233 / E.I.Lines, Daudpota Road, Karachi, Pakistan. First reviewed 2010 Latest Revision June 2012 All rights reserved This syllabus is developed by Aga Khan University Examination Board for distribution to all its affilia ted schools. Higher Secondary School Certificate Examination Syllabus Pakistan Culture CLASSES XI-XII This subject is examined in both May and September Examination sessions Sr. No. Table of Contents Page No. Preface 5 1. Aims/Objectives of the National Curriculum (2002) 7 2. Rationale of the AKU-EB Examination Syllabuses 8 3. Topics and Student Learning Outcomes of the Examination Syllabus 10 4. Scheme of Assessment 33 5. Teaching-Learning Approaches and Classroom Activities 36 6. Recommended Texts and Reference Materials 37 7. Definition of Cognitive Levels and Command Words in the Student 38 Learning Outcomes in Examination Papers Annex : HSSC Scheme of Studies 41 For queries and feedback Address: The Aga Khan University Examination Board Bungalow No. 233/ E.I.Lines, Daudpota Road, Karachi-Pakistan. Phone: (92-21) 35224702-10 Fax: (92-21) 35224711 E-mail: [email protected] Website: http://examinationboard.aku.edu http://learningsupport.akueb.edu.pk Facebook: www.facebook.com/akueb Latest Revision June 2012 Page 4 PREFACE In pursuance of National Education Policy (1998-2010), the Curriculum Wing of the Federal Ministry of Education has begun a process of curriculum reform to improve the quality of education through curriculum revision and textbook development (Preface, National Curriculum documents 2000 and 2002). -

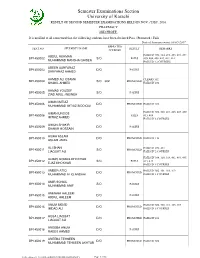

Semester Examinations Section University of Karachi RESULT of SECOND SEMESTER EXAMINATIONS HELD in NOV

Semester Examinations Section University of Karachi RESULT OF SECOND SEMESTER EXAMINATIONS HELD IN NOV. / DEC. 2016 PHARMACY 2ND PROFF. It is notified to all concerned that the following students have been declared Pass / Promoted / Fails Date of Announcement: 08-05-2017 REPEATED SEAT NO STUDENT'S NAME RESULT REMARKS COURSES FAILS IN 302, 314, 401, 403, 405, 407, ABDUL REHMAN BP1450002 S/O FAILS 405, 404, 408, 410, 412, 414 MUHAMMAD MANSHA QAISER FAILS IN 12 COURSES ABEER SARFARAZ BP1450003 D/O PASSES SARFARAZ AHMED AHMED ALI OSAMA CLEARS 302 BP1450004 S/O 302 PROMOTED SHAKIL AHMED FAILS IN 403 AHMAD YOUSEF BP1450005 S/O PASSES ZIAD ABUL JNEINEH AIMAN IMTIAZ BP1450006 D/O PROMOTED FAILS IN 401 MUHAMMAD IMTIAZ SIDDIQUI FAILS IN 306, 308, 401, 403, 405, 409, AIMAN UROOS BP1450008 D/O FAILS 413, 408 IMTIAZ AHMED FAILS IN 8 COURSES AIMUN SHAKIR BP1450009 D/O PASSES SHAKIR HOSSAIN AISHA ASLAM BP1450010 D/O PROMOTED FAILS IN 413 ASLAM JAMIL ALI SHAN FAILS IN 403, 413 BP1450011 S/O PROMOTED LIAQUAT ALI FAILS IN 2 COURSES FAILS IN 308, 310, 314, 401, 403, 405, ALMAS ROMAIL KHOKHAR BP1450012 S/O FAILS 413, 410 EJAZ KHOKHAR FAILS IN 8 COURSES AMBER ATIQ FAILS IN 302, 401, 403, 413 BP1450013 D/O PROMOTED MUHAMMAD ATIQ ANSARI FAILS IN 4 COURSES AMIR SOHAIL BP1450014 S/O PASSES MUHAMMAD ARIF AMMARA HALEEM BP1450015 D/O PASSES ABDUL HALEEM ANUM IMDAD FAILS IN 302, 308, 401, 403, 405 BP1450016 D/O PROMOTED IMDAD ALI FAILS IN 5 COURSES AQSA LIAQUAT BP1450017 D/O PROMOTED FAILS IN 403 LIAQUAT ALI AREEBA ANUM BP1450018 D/O PASSES RAEES AHMED AREEBA TEHSEEN BP1450019 D/O PROMOTED FAILS IN 306 MUHAMMAD TEHSEEN AKHTAR E:\E\(F) Drive Data on 31-12-13\All Result\RESULT 2ND SEM.2016\PHARMACY Page 1 of 12 Semester Examinations Section University of Karachi RESULT OF SECOND SEMESTER EXAMINATIONS HELD IN NOV. -

Cultural Scenario of Pakistan in Democratic and Military Eras (1947-2013)

South Asian Studies A Research Journal of South Asian Studies Vol. 32, No. 1, January – June 2017, pp.67 – 80 Cultural Scenario of Pakistan in Democratic and Military Eras (1947-2013) Saira Siddiqui Government College University, Faisalabad, Pakistan. Syeda Khizra Aslam Government College University, Faisalabad, Pakistan. Muhammad Rashid Khan University of the Punjab, Lahore, Pakistan. ABSTRACT This study investigates a politico-cultural mapping of leisure and life in Pakistan, a country in South Asia, with a political developmental period in historical perspective from its independence in 1947. A classification of ruling eras is done, and accordingly the paper carries its discussion. A few tables are presented to give the percentage of leisure-time spent, and leisure-activities pursued by Pakistani men and women. The data is from nationally represented samples of 2690 respondents in 2009, and 1294 respondents interviewed in 2012 by Gilani Research Foundation, Pakistan. The findings also include statistics from a research by the authors own empirical study of 2013, from a sample of 222 women respondents in Faisalabad City, Punjab, Pakistan. Key Words: Democratic and military eras, Pakistan, leisure and life, recreational facilities Introduction South Asia is one of the most heavily populated places in the world. The countries within its area are Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan, and Sri Lanka (Cultural Geography of South Asia, 2002). Pakistan and Bangladesh in South Asia have Muslim influence, politico-cultural histories of political conflicts, and different civilizations. Pakistan has seen military rule and instability from time to time. The cultural histories of Nepal, Bhutan, Maldives, and Sri Lanka are different. -

The Role of Media in Pakistan Dr

Journal of South Asian and Middle Eastern Studies, 35 :4, Summer 2012. The Role of Media in Pakistan Dr. Nazir Hussain The explosion of information revolution and the proliferation of electronic media have virtually converted the world into a globalized village. Now, information, news and events have no barriers and control to reach anywhere around the world. These happenings reach to every living room instantaneously even before the governments can react and control it. The enhanced role of media has impacted the social, economic and political life. What one thinks, believes and perceives are based on the images shown on the media. It has penetrated the routine life of all individuals; commoners, elites, decision-makers and statesmen. States have often been inclined to use the media as a propaganda tool for political and military purposes. The decades of 1980s and 1990s have for instance witnessed the use of US media for politico-military ends. The projection of Soviet Union as an ‘Evil Empire’, the Saddam saga and the ‘Weapons of Mass Destruction’ and the Osama Bin Laden from ‘Freedom Fighter to a Terrorist’ are some of the examples. However, now the media has come out of the domain of the state controls, it is the financiers, the media houses and the media anchors that make heroes and villains, leaders and terrorists. Therefore, the role of media is growing from an observer to an active player in political decision making. The political leaders and government officials have become dependent to convey and defend their policies through the use of media. The media where ‘more anti-government will earn more business’ is considered a basic key to success. -

Following Clarification/Rebuttal Was Issued to Business Recorder in Response to an Editorial Published on February 6, 2020 Entitled: ‘IMF Programme Needs Tweaking’

Following Clarification/Rebuttal was issued to Business Recorder in response to an Editorial published on February 6, 2020 entitled: ‘IMF programme needs tweaking’ This is with reference to your editorial titled ‘IMF programme needs tweaking’ published on 6th February, 2020. We would like to draw your attention to the three points raised in your editorial that are either factually or conceptually incorrect. These points are: 1. “…however, what was ignored at the time and continues to be ignored to this day is data uploaded on State Bank of Pakistan's (SBP's) website which notes that the rupee had been undervalued since December 2018 and that in March 2019 it was undervalued to the tune of just under 3 percent.” 2. “…a decision that would reduce SBP profits thereby putting pressure on the fiscal deficit given that during the first quarter, an unprecedented rise in SBP profits went half way in lowering the budget deficit.” 3. Additionally, the high discount rate has attracted foreign portfolio investment in government securities which are even worse than the then finance minister Ishaq Dar's policy to incur debt equity (sukuk/eurobonds) as the return is more than 6 percent higher while the amortization period is a lot less than the five- and 10-year maturity set by Dar.” SBPs views on these points are as follows 1. The first statement appears to be referring to data on the nominal / real effective exchange rate (NEER/REER) indices of the Pakistani Rupee available on SBP’s website. However, it is factually incorrect and an inaccurate reading of what the data represent.