Footwear Cluster in Kolkata: a Case of Self-Exploitative Fragmentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CIN/BCIN Company/Bank Name Date of AGM(DD-MON-YYYY)

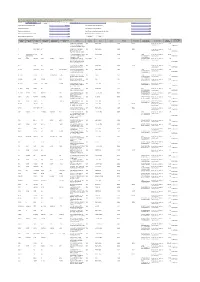

Note: This sheet is applicable for uploading the particulars related to the unclaimed and unpaid amount pending with company. Make sure that the details are in accordance with the information already provided in e-form IEPF-2 CIN/BCIN L17299WB1985PLC038517 Prefill Company/Bank Name RUPA & COMPANY LTD Date Of AGM(DD-MON-YYYY) 31-AUG-2017 Sum of unpaid and unclaimed dividend 177070.50 Sum of interest on matured debentures 0.00 Sum of matured deposit 0.00 Sum of interest on matured deposit 0.00 Sum of matured debentures 0.00 Sum of interest on application money due for refund 0.00 Sum of application money due for refund 0.00 Redemption amount of preference shares 0.00 Sales proceed for fractional shares 0.00 Validate Clear Proposed Date of Investor First Investor Middle Investor Last Father/Husband Father/Husband Father/Husband Last DP Id-Client Id- Amount Address Country State District Pin Code Folio Number Investment Type transfer to IEPF Name Name Name First Name Middle Name Name Account Number transferred (DD-MON-YYYY) A BANERJEE NA C/O SHYAMAL CHAKRABORTY, INDIA WEST BENGAL 712148 A00115 Amount for unclaimed and 15.00 VILL MERIA BHADRAKALITALA, unpaid dividend 05-NOV-2019 P.O.AKNA DIST HOOGHLY, 712148 A CHAKRABORTTY NA C/O SHYAMAL CHAKRABORTY, INDIA WEST BENGAL 712148 A00127 Amount for unclaimed and 15.00 MERIA BHADRAKALI TALA, unpaid dividend 05-NOV-2019 P.O.AKNA DT HOOGHLY, 712148 A RWEALTHADVIS LIMITED NA THE MALL CROSS ROAD, SHOP NO INDIA UTTAR PRADESH 273001 33300- Amount for unclaimed and 150.00 ORYSERVICESPR 8 AND 9 2ND FLOOR, -

List of Contact Person As Well As Hospitals of KPGM Policy '2017-18'

List of Contact Person as well as Hospitals of KPGM Policy ’2017-18’ Insurance Company : National Insurance Company Limited, Division – XXII, CRO – II, Kolkata-700 001. TPA : MDIndia Health Insurance TPA Pvt. Ltd. Office : 18, Lalbazar Street, Kolkata – 700 001. Phone Number : 033 – 2214 – 1936 / 1937 : Dr. Pijush Kanti Ghosh - 93320-80207 For Cashless : Mr. Soumen Jena - 99321-79757 : Dr. Sukanta Hens - 76992-23715 Reimbursement Claim : Mr. T. N. Das - 87980-85986 : 10:00 a.m. to 5:30 p.m. (Monday – Friday) Office Hours : 10:00 a.m. to 2:00 p.m. (Saturday) Claim Co-Coordinator : Mr. T. N. Das - 87980-85986 Nodal Officer, KPGM : Rabi Bhusan Paul - 94326 – 12632 KPGM Stuff : ASI - Kanchan Kr. Chowbey - 98366 - 32468 KPGM Office, Lalbazar : 033 – 2250 – 5156 List of empanelled Hospitals / Nursing Homes in Kolkata, Vellore and Districts for cashless facility for the members of Kolkata Police Group Mediclaim Policy’2017-18. K.P.G.M HOSPITAL LIST- 2017-2018 (KOLKATA) Sl. Contact Hospital Name Location Address Contact No No Person P-4&5, Gariahat Road Block-A, 033-66260000/ 1 AMRI -Dhakuria Kolkata Scheme-L11, Dhakuria, Kolkata Suvendu Pal 99030-11694 700029 230 Barakhola Lane, Purba Jadavpur, Behind Metro Cash n 033-66061041/ 2 AMRI -Mukundapur Kolkata Carry, Mukundapur, Kolkata - Dr Sukhendu 98310-65329 700099 JC - 16 & 17 Saltlake City, KB 033-66147700/ 3 AMRI -Saltlake Kolkata Block, Sector III, Kolkata - 700098 Victar Nandi 98310-13578 All Asia Medical 8B, Garcha First Lane, Beside 033-40012200/ 4 Institute (Harsh Kolkata Gariahat Pantaloons, Ballygunge, Ranjit Ukil 98305-92300 Medical) Kolkata - 700019 033-24567890/ B M Birla Heart 1, National Library Ave, Sector 1, 5 Kolkata S. -

Date Wise Details of Covid Vaccination Session Plan

Date wise details of Covid Vaccination session plan Name of the District: Darjeeling Dr Sanyukta Liu Name & Mobile no of the District Nodal Officer: Contact No of District Control Room: 8250237835 7001866136 Sl. Mobile No of CVC Adress of CVC site(name of hospital/ Type of vaccine to be used( Name of CVC Site Name of CVC Manager Remarks No Manager health centre, block/ ward/ village etc) Covishield/ Covaxine) 1 Darjeeling DH 1 Dr. Kumar Sariswal 9851937730 Darjeeling DH COVAXIN 2 Darjeeling DH 2 Dr. Kumar Sariswal 9851937730 Darjeeling DH COVISHIELD 3 Darjeeling UPCH Ghoom Dr. Kumar Sariswal 9851937730 Darjeeling UPCH Ghoom COVISHIELD 4 Kurseong SDH 1 Bijay Sinchury 7063071718 Kurseong SDH COVAXIN 5 Kurseong SDH 2 Bijay Sinchury 7063071718 Kurseong SDH COVISHIELD 6 Siliguri DH1 Koushik Roy 9851235672 Siliguri DH COVAXIN 7 SiliguriDH 2 Koushik Roy 9851235672 SiliguriDH COVISHIELD 8 NBMCH 1 (PSM) Goutam Das 9679230501 NBMCH COVAXIN 9 NBCMCH 2 Goutam Das 9679230501 NBCMCH COVISHIELD 10 Matigara BPHC 1 DR. Sohom Sen 9435389025 Matigara BPHC COVAXIN 11 Matigara BPHC 2 DR. Sohom Sen 9435389025 Matigara BPHC COVISHIELD 12 Kharibari RH 1 Dr. Alam 9804370580 Kharibari RH COVAXIN 13 Kharibari RH 2 Dr. Alam 9804370580 Kharibari RH COVISHIELD 14 Naxalbari RH 1 Dr.Kuntal Ghosh 9832159414 Naxalbari RH COVAXIN 15 Naxalbari RH 2 Dr.Kuntal Ghosh 9832159414 Naxalbari RH COVISHIELD 16 Phansidewa RH 1 Dr. Arunabha Das 7908844346 Phansidewa RH COVAXIN 17 Phansidewa RH 2 Dr. Arunabha Das 7908844346 Phansidewa RH COVISHIELD 18 Matri Sadan Dr. Sanjib Majumder 9434328017 Matri Sadan COVISHIELD 19 SMC UPHC7 1 Dr. Sanjib Majumder 9434328017 SMC UPHC7 COVAXIN 20 SMC UPHC7 2 Dr. -

167 – Maniktala Assembly Constituency Sl

167 – Maniktala Assembly Constituency Sl. Name & Address of the Polling Premises P.S. Attached Ward No Borough Police Station THE PARK INSTITUTION, 12, Mohanlal Street, P.S. 1 1, 2, 3, 4, 5, 6, 7, 8 12 II Ultadanga Ultadanga, Kolkata-4 K.M.C.P.SCHOOL, 44, Canal West Road, P.S. 2 9, 10 12 II Ultadanga Ultadanga, Kolkata-4 J.B. ROY STATE AYURVEDIC MEDICAL 11, 12, 13, 14, 15, 3 COLLEGE & HOSPITAL, 170-172, Raja Dinendra 12 II Ultadanga 16, 17 Street, Kol-4 ULTADANGA UNITED HIGHER SECONDARY 18, 19, 20, 21, 22, 4 12 II Ultadanga SCHOOL, 49, Ultadanga Road, Kolkata -4 23, 24, 25 DASPARA ABAITANIK PRATHAMIK 5 VIDYALAYA, 10/2, Kritibas Mukherjee Road, Kolkata 26, 27 13 III Ultadanga - 67 CHAYANIKA VIDYAMANDIR, 7/1, Gorapada Sarkar 6 28, 29, 37, 38, 52 13 III Ultadanga Lane, Ultadanga, Kolkata - 67 SARADA PROSAD INSTITUTION FOR GIRLS, 1/1 30, 31, 32, 33, 34, 7 13 III Ultadanga CIT Sch VIII M Dhar Bagan, (PS-Ultadanga) Kolkata - 9 60 SUDHIR PAL PRATHAMIK VIDYALAYA, 27, B. 8 35, 36 13 III Ultadanga Adhar Chandra Das Lane, Kolkata - 67 NEW ST THOMAS PUBLIC SCHOOL, 7/H, Gorapada 9 39, 40, 41, 42, 43 13 III Ultadanga Sarkar Lane, Ultadanga, Kolkata - 67 MUNICIPALITY WARD OFFICE, WARD NO. -13, 10 45, 46 13 III Maniktala 17, Bidhan Nagar Road, Kolkata-700067 SITALA SANGHA PRATHAMIK VIDYALAYA, 11 44, 51 13 III Ultadanga 20/H/7/2, Kirtibas Mukerjee Rd., Kolkata - 67. NATIONAL ACADEMY OF CUSTOM EXC & NAR 12 EST REGN. P-27 CIT Scheme VIIIM, Bidhan Nagar 47, 48, 57, 58, 59 13 III Maniktala Rd., Kolkata - 67. -

BUS ROUTE-18-19 Updated Time.Xls LIST of DROP ROUTES & STOPPAGES TIMINGS LIST of DROP ROUTES & STOPPAGES TIMINGS

LIST OF DROP ROUTES & STOPPAGES TIMINGS LIST OF DROP ROUTES & STOPPAGES TIMINGS FOR THE SESSION 2018-19 FOR THE SESSION 2018-19 ESTIMATED TIMING MAY CHANGE SUBJECT ESTIMATED TIMING MAY CHANGE SUBJECT TO TO CONDITION OF THE ROAD CONDITION OF THE ROAD ROUTE NO - 1 ROUTE NO - 2 SL NO. LIST OF DROP STOPPAGES TIMINGS SL NO. LIST OF DROP STOPPAGES TIMINGS 1 DUMDUM CENTRAL JAIL 13.00 1 IDEAL RESIDENCY 13.05 2 CLIVE HOUSE, MALL ROAD 13.03 2 KANKURGACHI MORE 13.07 3 KAJI PARA 13.05 3 MANICKTALA RAIL BRIDGE 13.08 4 MOTI JEEL 13.07 4 BAGMARI BAZAR 13.10 5 PRIVATE ROAD 13.09 5 MANICKTALA P.S. 13.12 6 CHATAKAL DUMDUM ROAD 13.11 6 MANICKTALA DINENDRA STREET XING 13.14 7 HANUMAN MANDIR 13.13 7 MANICKTALA BLOOD BANK 13.15 8 DUMDUM PHARI 01:15 8 GIRISH PARK METRO STATION 13.20 9 DUMDUM STATION 01:17 9 SOVABAZAR METRO STATION 13.23 10 7 TANK, DUMDUM RD 01:20 10 B.K.PAUL AVENUE 13.25 11 AHIRITALA SITALA MANDIR 13.27 12 JORABAGAN PARK 13.28 13 MALAPARA 13.30 14 GANESH TALKIES 13.32 15 RAM MANDIR 13.34 16 MAHAJATI SADAN 13.37 17 CENTRAL AVENUE RABINDRA BHARATI 13.38 18 M.G.ROAD - C.R.AVENUE XING 13.40 19 MOHD.ALI PARK 13.42 20 MEDICAL COLLEGE 13.44 21 BOWBAZAR XING 13.46 22 INDIAN AIRLINES 13.48 23 HIND CINEMA XING 13.50 24 LEE MEMORIAL SCHOOL - LENIN SR. 13.51 ROUTE NO - 3 ROUTE NO - 04 SL NO. -

BK Centers in Kolkata, India

BK Centers in Kolkata, India Source: “Centers Finder” service by www.bkgsu.com/centres Centre Name Centre Address Contact Info. Kolkata Behala H.no: 28/1a 033-23976685 Pani Tanki Street, Rishi Bankim 9836912303 Chandra Road [email protected] Royde Park, Behala Kolkata Kolkata-700034 West Bengal Kolkata Ashutosh 1-a, Ashutosh Mukherjee Road 033-24753521 Mukherjee Road Near Sambhunath Pandit Hospital 9831142250 L.r.sarani [email protected] Kolkata Kolkata-700020 West Bengal Kolkata Bangur Rajyoga Bhawan 033-25747863 Avenue 81/1, Bangur Avenue 9874123356 Block C, V.i.p. Road Side [email protected] Kolkata North 24 Parganas-700055 West Bengal Kolkata Baranagar Saptarshi Aparment, Flat No:1, 2nd 9143605992, 9433305040 Floor [email protected] 17, Gopal Lal Thakur Road Baranagar Kolkata Kolkata-700036 West Bengal Kolkata Roy Bagan H.no: 23/4c 033- 25557073 Roy Bagan Street 8450837215, 9748482916 Kolkata [email protected] Kolkata-700006 West Bengal Kolkata Howrah B-1, Ground Floor, Ganges Garden 033-26386594 106, Kiran Chandra Sinha Road 9874922884 Opp. Aloka Cinema, Shibpur [email protected] Howrah Howrah-711102 West Bengal Kolkata 30b, 2nd Floor 033-23558683 Kankurgachi Maniktala Mainroad 9674069994 Kankurgachi [email protected] Kolkata Kolkata-700054 West Bengal Kolkata Gyan Sarovar, First Floor 033- 23592591 Phoolbagan 2b, Motilal Basak Lane 9748482916, 8450837215 Kankurgachi, Phoolbagan [email protected] Kolkata Kolkata-700054 West Bengal Kolkata Dum Dum 83/46, Chatterjee Lodge 033-25134096 Dum Dum Road -

Pick up Fee with Chart.Xlsx

Pick‐Up Routes with time (NURSERY ‐ CLASS‐X) for The Academic Session 2018‐19 Route # 1 (8585059795) Time KM Fee(INR) Route # 9 (8585014347) Time KM Fee(INR) Route # 15 (8585059823) Time KM Fee(INR) Route # 23 (7603089214) Time KM Fee(INR) Route # 31 (7595064661) Time KM Fee(INR) Lake Town VIP 07:00 AM Above 15 Km 3900 Sealdah ESIC Hospital 06.40 Am Above 15 Km 3900 Newtown Metro Plaza 07.15 Am 0 ‐ 10 Km 3400 Kestopur Subway 07:05 AM 11 Km ‐ 15 Km 3650 Hind Cinema 06:55 AM Above 15 Km 3900 Lake Town Host 07:02 AM Above 15 Km 3900 Rajabazar Sci. College Bus Stop 06.45 Am Above 15 Km 3900 Rajarhat Check Post 07.20 Am 0 ‐ 10 Km 3400 Baguiati College 07:08 AM 11 Km ‐ 15 Km 3650 Chandni Chowk Metro 06:58 AM Above 15 Km 3900 Lake Town Nursing Home 07:04 AM Above 15 Km 3900 Karbala 06.47 Am Above 15 Km 3900 Route # 16 (8585059796) Time KM Fee(INR) Baguiati Bus Stop 07:12 AM 11 Km ‐ 15 Km 3650 C.R Avenue Metro 07:00 AM Above 15 Km 3900 Lake Town Mansa Bari 07:05 AM Above 15 Km 3900 Sahitya Parishad Crossing 06.50 Am Above 15 Km 3900 Park Circus 7 Point 06:40 AM Above 15 Km 3900 Baguiati Big Bazar(opp) 07:15 AM 11 Km ‐ 15 Km 3650 Md. Ali Park 07:05 AM Above 15 Km 3900 Route # 2 (8585059790) Time KM Fee(INR) Pareshnath Mandir Crossing 06.53 Am Above 15 Km 3900 Quest Mall 06:42 AM Above 15 Km 3900 Raghunathpur Bus Stop 07:18 AM 11 Km ‐ 15 Km 3650 Ram Mandir 07:10 AM 11 Km ‐ 15 Km 3650 Bangur Swimming Pool 07:00 AM Above 15 Km 3900 Deshbandhu Park 06.58 Am Above 15 Km 3900 Ballygunge Phari 06:45 AM Above 15 Km 3900 Route # 24 (7603089215) Time KM -

16‐06‐20 13 5 Seals Garden Lane Cossipore 700002 1 1

Affected Zone DAYS SINCE Date of reporting of REPORTING Sl No. Address Ward Borough Local area the case 13 5 SEALS GARDEN LANE The premises itself 1 1 1 Cossipore 16‐06‐20 COSSIPORE 700002 14 The affected flat/the 59 Kalicharan Ghosh Rd standalone house 2 kolkata ‐ 700050 West 2 1 Sinthi Bengal India 16‐06‐20 14 The premises itself 21/123 RAJA MANINDRA 3 31 Paikpara ROAD BELGACHIA 700037 16‐06‐20 14 14A BIRPARA LANE The premises itself 4 kolkata ‐ 700030 West 31 Belgachia 16‐06 ‐20 BBlIdiengal India 14 The flat itself A4 6 R D B RD Kolkata ‐ 5 41 Paikpara 700002 West Bengal India 16‐06‐20 14 110/1A COSSIPORE Road The premises itself 6 Kolkata ‐ 700002 West 6 1 Chitpur 16‐06‐20 Bengal India 14 Adjacent common passage of affected hut 14 3 GALIFF STREET 7 7 1 Bagbazar including toilet and BAGHBAZAR 700003 water source of the 16‐06‐20 slum 14 Adjacent common passage of affected hut 14 3 GALIFF STREET 8 7 1 Bagbazar including toilet and BAGHBAZAR 700003 water source of the 16‐06‐20 slum 14 Affected Zone DAYS SINCE Date of reporting of REPORTING Sl No. Address Ward Borough Local area the case 1 RAMKRISHNA LANE The premises itself 9 Kolkata ‐ 700003 West 7 1 Girish Mancha 16‐06‐20 Bengal India 14 The premises itself 4/2/1B KRISHNA RAM BOSE 10 STREET SHYAMPUKUR 10 2 Shyampukur KOLKATA 700004 16‐06‐20 14 T/1D Guru Charan Lane The premises itself 11 Kolkata ‐ 700004 West 10 2 Hatibagan 16‐06‐20 Bengal India 14 Adjacent common 47 1 SHYAMBAZAR STREET passage of affected hut 12 Kolk at a ‐ 700004 W est 10 2 Shyampu kur iilditiltdncluding toilet and -

Summary Report 2020-09-17 05:00

SUMMARY REPORT 2020-09-17 05:00 Average Max Geofence Geofence Ignition Ignition Device Distance Spent Engine Start End Sr Speed Speed Start Address End Address In Out On Off Name (Kms) Fuel hours Time Time (Km/h) (Km/h) (times) (times) (times) (times) Indian Oil Petrol Pump/Prafulla Service Indian Oil Petrol Pump/Prafulla Service 2020- 2020- WB 25K 0 h 16 1 2.04 3.6 57.0 0 Station,Durgapur Expressway Borai, West Bengal- Station,Durgapur Expressway Borai, West 09-16 09-16 0 0 5 5 2604 m 712306 India Bengal-712306 India 00:04:19 23:21:57 2020- 2020- WB 67B 2 h 48 Murari Pukur Road, Phoolbagan, Maniktala, Kolkata, Phoolbagan, Narkeldanga, Kolkata, West 2 44.17 18.3 60.0 0 09-16 09-16 0 0 24 23 1249 m West Bengal, 700037, India Bengal, 700004, India 10:25:05 23:59:47 2020- 2020- WB 33D Daspur-I, Paschim Medinipur, West Bengal, 721250, Sun Enterprises,SH 4 Kuspata, Ghatal, 3 22.17 18.8 69.0 0 1 h 5 m 09-16 09-16 0 0 18 19 4790 India West Bengal-721212 India 00:00:01 23:07:38 2020- 2020- WB 25F 12 h 2 New Barrakpore, Khardaha, Barrackpur - II, North 24 Bally, Bally Jagachha, Howrah, West 4 260.49 23.0 65.0 0 09-16 09-16 0 0 87 88 3526 m Parganas, West Bengal, 700131, India Bengal, 711227, India 00:00:01 22:19:47 2020- 2020- WB 25J 6 h 45 JRK Electric,Ghola Road Belgharia, Kolkata, West NH12, Krishnanagar, Krishnagar-I, Nadia, 5 170.62 33.7 104.0 0 09-16 09-16 0 0 5 5 0480 m Bengal-700083 India West Bengal, 741101, India 16:36:59 23:58:31 Old Nimta Road, Belgharia, Khardaha, 2020- 2020- WB 25J Kachari Maidan, NH112, Barasat, Barasat - I, North -

East-West Metro to Run Full Course by 2021: MD of KMRC - Times of India

3/15/2018 East-West Metro to run full course by 2021: MD of KMRC - Times of India Printed from East-West Metro to run full course by 2021: MD of KMRC TNN | Mar 14, 2018, 06.22 AM IST KOLKATA: The East-West Metro will connect with the first underground station Phoolbagan in early 2019 and Sealdah in 2020 before running the full course by 2021. The day after Union minister Babul Supriyo announced the probable date for the inauguration of the first phase of the service from Sector V to Salt Lake Stadium on October 2 this year, the managing director of the Kolkata Metro Rail Corporation (KMRC) Parashuram Singh said that KMRC would open first phase of the alignment by stages before making the entire alignment operational in 2021. https://timesofindia.indiatimes.com/city/kolkata/east-west-metro-to-run-full-course-by-2021-md-of-kmrc/articleshowprint/63293230.cms 1/3 3/15/2018 East-West Metro to run full course by 2021: MD of KMRC - Times of India Speaking to TOI on the sideline of the Assocham seminar, Mass Rapid Transport System For Urban Areas: Opportunities And Challenges, he said, “We are receiving two complete rakes from BEML most probably next month. The rest of the rakes will come well ahead of the inauguration of the first phase.” According to the original plan, the stretch from Sector V to Sealdah was to be inaugurated in the first phase but the change of alignment hit the entire plan. “Sealdah station can’t be ready till the tunnel boring machine (TBM), which starts construction from Esplanade to Sealdah in May, is retrieved at Sealdah station shaft,” said KMRC spokesperson A K Nandy. -

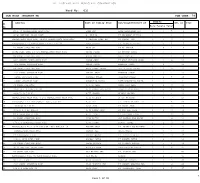

SR NO First Name Middle Name Last Name Address

SR NO First Name Middle Name Last Name Address Pincode Folio Amount 1 AK AGRAWAL 110 D M C D COLONY AZADPUR DELHI 110033 0000000000CEA0018033 240.00 2 A K PARBHAKAR 8 SCHOOL BLOCK SHAKARPUR DELHI 110092 0000000000CEA0018043 750.00 3 A GROVER 2-A GOKHLE MARG LUCKNOW 226001 0000000000CEA0018025 645.00 4 A D KODILKAR 58/1861 NEHRUNAGAR KURLA EAST MUMBAI 400024 0000000000CEA0018011 1,125.00 5 A D KODILKAR BLDG NO 58 R NO 1861 NEHRU NAGAR KURLA EAST MUMBAI 400024 0000000000CEA0018012 180.00 6 A M RAJAPURKAR 11 CHANCHAL APPT SANGHVI NAGAR AUNDH PUNE 411007 0000000000CEA0018056 225.00 7 A M RAJAPURKAR 11 CHANCHAL APTS SANGHVI NAGAR AVNDH PUNE 411007 0000000000CEA0018057 240.00 8 A M RAJAPURKAR 11 CHANCHAL APTS SANGHVI NAGAR AUNDH PUNE 411007 0000000000CEA0018058 240.00 9 A GIRIDHAR 125 ANNAM GARDEN KAVADIGUDA HYDERABAD 500003 0000000000CEA0018021 255.00 10 A KARISHMA 125 ANNAM GARDENS KAVADIGUDA HYDERABAD 500003 0000000000CEA0018050 510.00 11 A MEGHNA 125 ANNAM GARDON KAVADIGUDA HYDERABAD 500003 0000000000CEA0018066 255.00 12 A VIKYAT 125 ANNAM GARDENS KAVADIGUDA HYDERABAD 500003 0000000000CEA0018106 255.00 13 A VINDHYA 125 ANNAM GARDENS KAVADIGUDA HYDERABAD 500003 0000000000CEA0018109 510.00 14 A SARADA FLAT NO 202 PREMIER COURT APPTS GOLKONDA X ROADS MUSHIRABAD HYDERABAD 500020 0000000000CEA0018089 750.00 15 A SRINIVASA RAO FLAT NO 202 KRISHNA ENCLAVE PLOT NO F-64 MADHURANAGAR HYDERABAD 500038 0000000000CEA0018092 240.00 16 A GAYATHRI C/O M MADHVESACHAR PLOT NO 41, MIG PHASE-I H NO 6-4-9, VANASTHALIPURAM HYDERABAD ANDHRA PRADESH 500070 0000000000CEA0018019 -

Ward No: 031 ULB Name :KOLKATA MC ULB CODE: 79

BPL LIST-KOLKATA MUNICIPAL CORPORATION Ward No: 031 ULB Name :KOLKATA MC ULB CODE: 79 Member Sl Address Name of Family Head Son/Daughter/Wife of BPL ID Year No Male Female Total 1 98/H/36 NARKELDANGA MAIN ROAD PAMA DAS LATE PANCHANAN DAS 2 3 5 1 2 40/41 MATILAL BASAK LANE A KHULLA LT MAHAMMAD KHULLA 1 1 2 3 3 NARKELDANGA MAIN ROAD 89/B14 NARKELDANGA MAIN ROAD A TEWAWRI RABI DAS LT PANCHU DAS 3 1 4 4 4 KANKURGACHI 14 KANKUR GACHI ROAD, KOL-54 ABHA BISWAS LT. PRABHAS BISWAS 2 3 5 5 5 89 KANAL CIRCULAR ROAD ABIR SA LT MD IMRISA 2 4 6 6 6 GHORE BIBI LANE 2/H/14 NARKELDANGA MAIN ROAD ABODH SINGH LT PROVAN SINGH 4 3 7 7 7 89 CANAL CIRCULAR ROAD ABUNA MONDAL RAJIB MONDAL 1 1 2 8 8 94/7 NARKEL DANGA MAIN ROAD ADESH SHAW LT HARI KRISHAN SHAW 2 2 4 10 9 71/1 KANAL CIRCULAR ROAD ADHIR SINGH RAMRAJA SINGH 5 2 7 11 10 89 CANAL CIRCULAR ROAD AGIN KUMAR YADAV SRI SHIBLAL YADAV 1 3 4 12 11 71/1 KANAL CIRCULAR ROAD AHALYA DEVI HARIBAN SINGH 2 3 5 13 12 CANAL CIRCULAR ROAD AHATALI MOLLA SALESMAN MOLLA 3 2 5 14 13 CANAL CIRCULAR ROAD AHMADULLA MOLLA LATE ALAWINDIN MOLLA 3 2 5 17 14 89 CANAL CIR ROAD AJIJUL SEKH SAMSUDDIN SEKH 2 2 4 18 15 40/41 M L B LANE KOL-54 AJIT KUMAR PRAJAPATI BABULAL PRAJAPATI 2 3 5 20 16 98/H/15 N D M RD AJIT NASKAR MURARI NASKAR 3 3 6 23 17 NARKELDANGA MAIN ROAD 6 102 NARKELDANGA MAIN ROAD AJIT RAJBHAR SUJIT RAJBHAR 3 0 3 24 18 KANKURGACHI 14 KANKURGACHI ROAD, KOL-54 AJOY DEY LT.