Hansl: a DSL for Econometrics

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Econometrics Oxford University, 2017 1 / 34 Introduction

Do attractive people get paid more? Felix Pretis (Oxford) Econometrics Oxford University, 2017 1 / 34 Introduction Econometrics: Computer Modelling Felix Pretis Programme for Economic Modelling Oxford Martin School, University of Oxford Lecture 1: Introduction to Econometric Software & Cross-Section Analysis Felix Pretis (Oxford) Econometrics Oxford University, 2017 2 / 34 Aim of this Course Aim: Introduce econometric modelling in practice Introduce OxMetrics/PcGive Software By the end of the course: Able to build econometric models Evaluate output and test theories Use OxMetrics/PcGive to load, graph, model, data Felix Pretis (Oxford) Econometrics Oxford University, 2017 3 / 34 Administration Textbooks: no single text book. Useful: Doornik, J.A. and Hendry, D.F. (2013). Empirical Econometric Modelling Using PcGive 14: Volume I, London: Timberlake Consultants Press. Included in OxMetrics installation – “Help” Hendry, D. F. (2015) Introductory Macro-econometrics: A New Approach. Freely available online: http: //www.timberlake.co.uk/macroeconometrics.html Lecture Notes & Lab Material online: http://www.felixpretis.org Problem Set: to be covered in tutorial Exam: Questions possible (Q4 and Q8 from past papers 2016 and 2017) Felix Pretis (Oxford) Econometrics Oxford University, 2017 4 / 34 Structure 1: Intro to Econometric Software & Cross-Section Regression 2: Micro-Econometrics: Limited Indep. Variable 3: Macro-Econometrics: Time Series Felix Pretis (Oxford) Econometrics Oxford University, 2017 5 / 34 Motivation Economies high dimensional, interdependent, heterogeneous, and evolving: comprehensive specification of all events is impossible. Economic Theory likely wrong and incomplete meaningless without empirical support Econometrics to discover new relationships from data Econometrics can provide empirical support. or refutation. Require econometric software unless you really like doing matrix manipulation by hand. -

Econometric Theory

Econometric Theory John Stachurski January 10, 2014 Contents Preface v I Background Material1 1 Probability2 1.1 Probability Models.............................2 1.2 Distributions................................. 16 1.3 Dependence................................. 25 1.4 Asymptotics................................. 30 1.5 Exercises................................... 39 2 Linear Algebra 49 2.1 Vectors and Matrices............................ 49 2.2 Span, Dimension and Independence................... 59 2.3 Matrices and Equations........................... 66 2.4 Random Vectors and Matrices....................... 71 2.5 Convergence of Random Matrices.................... 74 2.6 Exercises................................... 79 i CONTENTS ii 3 Projections 84 3.1 Orthogonality and Projection....................... 84 3.2 Overdetermined Systems of Equations.................. 90 3.3 Conditioning................................. 93 3.4 Exercises................................... 103 II Foundations of Statistics 107 4 Statistical Learning 108 4.1 Inductive Learning............................. 108 4.2 Statistics................................... 112 4.3 Maximum Likelihood............................ 120 4.4 Parametric vs Nonparametric Estimation................ 125 4.5 Empirical Distributions........................... 134 4.6 Empirical Risk Minimization....................... 137 4.7 Exercises................................... 149 5 Methods of Inference 153 5.1 Making Inference about Theory...................... 153 5.2 Confidence Sets.............................. -

Department of Geography

Department of Geography UNIVERSITY OF FLORIDA, SPRING 2019 GEO 4167c section #09A6 / GEO 6161 section # 09A9 (3.0 credit hours) Course# 15235/15271 Intermediate Quantitative Methods Instructor: Timothy J. Fik, Ph.D. (Associate Professor) Prerequisite: GEO 3162 / GEO 6160 or equivalent Lecture Time/Location: Tuesdays, Periods 3-5: 9:35AM-12:35PM / Turlington 3012 Instructor’s Office: 3137 Turlington Hall Instructor’s e-mail address: [email protected] Formal Office Hours Tuesdays -- 1:00PM – 4:30PM Thursdays -- 1:30PM – 3:00PM; and 4:00PM – 4:30PM Course Materials (Power-point presentations in pdf format) will be uploaded to the on-line course Lecture folder on Canvas. Course Overview GEO 4167x/GEO 6161 surveys various statistical modeling techniques that are widely used in the social, behavioral, and environmental sciences. Lectures will focus on several important topics… including common indices of spatial association and dependence, linear and non-linear model development, model diagnostics, and remedial measures. The lectures will largely be devoted to the topic of Regression Analysis/Econometrics (and the General Linear Model). Applications will involve regression models using cross-sectional, quantitative, qualitative, categorical, time-series, and/or spatial data. Selected topics include, yet are not limited to, the following: Classic Least Squares Regression plus Extensions of the General Linear Model (GLM) Matrix Algebra approach to Regression and the GLM Join-Count Statistics (Dacey’s Contiguity Tests) Spatial Autocorrelation / Regression -

The Evolution of Econometric Software Design: a Developer's View

Journal of Economic and Social Measurement 29 (2004) 205–259 205 IOS Press The evolution of econometric software design: A developer’s view Houston H. Stokes Department of Economics, College of Business Administration, University of Illinois at Chicago, 601 South Morgan Street, Room 2103, Chicago, IL 60607-7121, USA E-mail: [email protected] In the last 30 years, changes in operating systems, computer hardware, compiler technology and the needs of research in applied econometrics have all influenced econometric software development and the environment of statistical computing. The evolution of various representative software systems, including B34S developed by the author, are used to illustrate differences in software design and the interrelation of a number of factors that influenced these choices. A list of desired econometric software features, software design goals and econometric programming language characteristics are suggested. It is stressed that there is no one “ideal” software system that will work effectively in all situations. System integration of statistical software provides a means by which capability can be leveraged. 1. Introduction 1.1. Overview The development of modern econometric software has been influenced by the changing needs of applied econometric research, the expanding capability of com- puter hardware (CPU speed, disk storage and memory), changes in the design and capability of compilers, and the availability of high-quality subroutine libraries. Soft- ware design in turn has itself impacted applied econometric research, which has seen its horizons expand rapidly in the last 30 years as new techniques of analysis became computationally possible. How some of these interrelationships have evolved over time is illustrated by a discussion of the evolution of the design and capability of the B34S Software system [55] which is contrasted to a selection of other software systems. -

International Journal of Forecasting Guidelines for IJF Software Reviewers

International Journal of Forecasting Guidelines for IJF Software Reviewers It is desirable that there be some small degree of uniformity amongst the software reviews in this journal, so that regular readers of the journal can have some idea of what to expect when they read a software review. In particular, I wish to standardize the second section (after the introduction) of the review, and the penultimate section (before the conclusions). As stand-alone sections, they will not materially affect the reviewers abillity to craft the review as he/she sees fit, while still providing consistency between reviews. This applies mostly to single-product reviews, but some of the ideas presented herein can be successfully adapted to a multi-product review. The second section, Overview, is an overview of the package, and should include several things. · Contact information for the developer, including website address. · Platforms on which the package runs, and corresponding prices, if available. · Ancillary programs included with the package, if any. · The final part of this section should address Berk's (1987) list of criteria for evaluating statistical software. Relevant items from this list should be mentioned, as in my review of RATS (McCullough, 1997, pp.182- 183). · My use of Berk was extremely terse, and should be considered a lower bound. Feel free to amplify considerably, if the review warrants it. In fact, Berk's criteria, if considered in sufficient detail, could be the outline for a review itself. The penultimate section, Numerical Details, directly addresses numerical accuracy and reliality, if these topics are not addressed elsewhere in the review. -

Regression Models by Gretl and R Statistical Packages for Data Analysis in Marine Geology Polina Lemenkova

Regression Models by Gretl and R Statistical Packages for Data Analysis in Marine Geology Polina Lemenkova To cite this version: Polina Lemenkova. Regression Models by Gretl and R Statistical Packages for Data Analysis in Marine Geology. International Journal of Environmental Trends (IJENT), 2019, 3 (1), pp.39 - 59. hal-02163671 HAL Id: hal-02163671 https://hal.archives-ouvertes.fr/hal-02163671 Submitted on 3 Jul 2019 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Distributed under a Creative Commons Attribution| 4.0 International License International Journal of Environmental Trends (IJENT) 2019: 3 (1),39-59 ISSN: 2602-4160 Research Article REGRESSION MODELS BY GRETL AND R STATISTICAL PACKAGES FOR DATA ANALYSIS IN MARINE GEOLOGY Polina Lemenkova 1* 1 ORCID ID number: 0000-0002-5759-1089. Ocean University of China, College of Marine Geo-sciences. 238 Songling Rd., 266100, Qingdao, Shandong, P. R. C. Tel.: +86-1768-554-1605. Abstract Received 3 May 2018 Gretl and R statistical libraries enables to perform data analysis using various algorithms, modules and functions. The case study of this research consists in geospatial analysis of Accepted the Mariana Trench, a hadal trench located in the Pacific Ocean. -

Estimating Regression Models for Categorical Dependent Variables Using SAS, Stata, LIMDEP, and SPSS*

© 2003-2008, The Trustees of Indiana University Regression Models for Categorical Dependent Variables: 1 Estimating Regression Models for Categorical Dependent Variables Using SAS, Stata, LIMDEP, and SPSS* Hun Myoung Park (kucc625) This document summarizes regression models for categorical dependent variables and illustrates how to estimate individual models using SAS 9.1, Stata 10.0, LIMDEP 9.0, and SPSS 16.0. 1. Introduction 2. The Binary Logit Model 3. The Binary Probit Model 4. Bivariate Logit/Probit Models 5. Ordered Logit/Probit Models 6. The Multinomial Logit Model 7. The Conditional Logit Model 8. The Nested Logit Model 9. Conclusion 1. Introduction A categorical variable here refers to a variable that is binary, ordinal, or nominal. Event count data are discrete (categorical) but often treated as continuous variables. When a dependent variable is categorical, the ordinary least squares (OLS) method can no longer produce the best linear unbiased estimator (BLUE); that is, OLS is biased and inefficient. Consequently, researchers have developed various regression models for categorical dependent variables. The nonlinearity of categorical dependent variable models (CDVMs) makes it difficult to fit the models and interpret their results. 1.1 Regression Models for Categorical Dependent Variables In CDVMs, the left-hand side (LHS) variable or dependent variable is neither interval nor ratio, but rather categorical. The level of measurement and data generation process (DGP) of a dependent variable determines the proper type of CDVM. Binary responses (0 or 1) are modeled with binary logit and probit regressions, ordinal responses (1st, 2nd, 3rd, …) are formulated into (generalized) ordered logit/probit regressions, and nominal responses are analyzed by multinomial logit, conditional logit, or nested logit models depending on specific circumstances. -

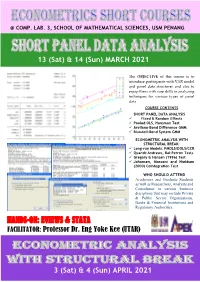

Hands-On & Exercise: Stata Hands-On: Eviews & Stata

@ COMP. LAB. 3, SCHOOL OF MATHEMATICAL SCIENCES, USM PENANG 13 (Sat) & 14 (Sun) MARCH 2021 The OBJECTIVE of this course is to introduce participants with VAR model and panel data structures and also to equip them with core skills in analyzing techniques for various types of panel data HANDS-ON & EXERCISE: STATA COURSE CONTENTS SHORT PANEL DATA ANALYSIS FACILITATORS: ✓ Fixed & Random Effects ✓ Pooled OLS, Hausman Test Dr Zainudin Arsad (USM) & ✓ Arellano-Bond Difference GMM ✓ Blundell-Bond System GMM Ass. Prof. Dr LAW S. HOOK (UPM) ECONOMETRIC ANALYSIS WITH STRUCTURAL BREAK: ✓ Long-run Models: FMOLS/DOLS/CCR ✓ Quandt-Andrews, Bai-Perron Tests ✓ Gregory & Hansen (1996) Test ✓ Johansen, Mosconi and Nieldsen (2000) Cointegration Test WHO SHOULD ATTEND Academics and Graduate Students as well as Researchers, Analysts and Consultants in various business disciplines that may include Private & Public Sector Organizations, Banks & Financial Institutions and Regulatory Authorities. HANDS-ON: EVIEWS & STATA FACILITATOR: Professor Dr. Eng Yoke Kee (UTAR) 3 (Sat) & 4 (Sun) APRIL 2021 SHORT PANEL DATA ANALYSIS DAY 1 : SATURDAY, 13 MARCH 2021 8:15 AM REGISTRATION 8:45 AM SESSION 1 – THE NATURE OF PANEL DATA ▪ Nature and Benefits od Panel Data; Examining & Arranging Your Dataset 10:30 AM TEA BREAK 10:45 AM SESSION 2 – STATIC LINEAR PANEL MODELS ▪ Panel Data Basics: Pooled OLS, Fixed and Random Effects 12:45 PM LUNCH 2:00 PM SESSION 3 – SELECTING PANEL DATA MODELS ▪ Poolability F-test, Breusch-Pagan LM Test, Hausman Test 3.45 PM TEA BREAK 4.00 PM SESSION 4 – ISSUES ON PANEL DATA MODELS: ROBUST ESTIMATES ▪ Diagnostic Tests and Robust Standard Errors 5:45 PM Q & A (SESSIONS 1 - 4) DAY 2 : SUNDAY, 14 MARCH 2021 8:30 AM SESSION 5 – DYNAMIC PANEL DATA APPROACH ▪ Why Dynamic Panel? 10:15 AM TEA BREAK 10:30 AM SESSION 6 – MULTIVARIATE DYNAMIC MODELS WITH PERSISTENT SERIES ▪ Arellano-Bond Difference Estimator, 1-step vs. -

Rtadf: Testing for Bubbles with Eviews

JSS Journal of Statistical Software November 2017, Volume 81, Code Snippet 1. doi: 10.18637/jss.v081.c01 Rtadf: Testing for Bubbles with EViews Itamar Caspi Bank of Israel Abstract This paper presents Rtadf (right-tail augmented Dickey-Fuller), an EViews add-in that facilitates the performance of time series based tests that help detect and date-stamp asset price bubbles. The detection strategy is based on a right-tail variation of the standard augmented Dickey-Fuller (ADF) test where the alternative hypothesis is of a mildly explo- sive process. Rejection of the null in each of these tests may serve as empirical evidence for an asset price bubble. The add-in implements four types of tests: standard ADF, rolling window ADF, supremum ADF (SADF; Phillips, Wu, and Yu 2011) and general- ized SADF (GSADF; Phillips, Shi, and Yu 2015). It calculates the test statistics for each of the above four tests, simulates the corresponding exact finite sample critical values and p values via Monte Carlo methods, under the assumption of Gaussian innovations, and produces a graphical display of the date stamping procedure. Keywords: rational bubble, ADF test, sup ADF test, generalized sup ADF test, mildly explo- sive process, EViews. 1. Introduction Empirical identification of asset price bubbles in real time, and even in retrospect, is surely not an easy task, and it has been the source of academic and professional debate for several decades.1 One strand of the empirical literature suggests using time series estimation tech- niques while exploiting predictions made by finance theory in order to test for the existence of bubbles in the data. -

Investigating Data Management Practices in Australian Universities

Investigating Data Management Practices in Australian Universities Margaret Henty, The Australian National University Belinda Weaver, The University of Queensland Stephanie Bradbury, Queensland University of Technology Simon Porter, The University of Melbourne http://www.apsr.edu.au/investigating_data_management July, 2008 ii Table of Contents Introduction ...................................................................................... 1 About the survey ................................................................................ 1 About this report ................................................................................ 1 The respondents................................................................................. 2 The survey results............................................................................... 2 Tables and Comments .......................................................................... 3 Digital data .................................................................................... 3 Non-digital data forms....................................................................... 3 Types of digital data ......................................................................... 4 Size of data collection ....................................................................... 5 Software used for analysis or manipulation .............................................. 6 Software storage and retention ............................................................ 7 Research Data Management Plans......................................................... -

Introduction to Eviews 2.0

Introduction to EViews 2.0 Overview of product EViews provides regression and forecasting tools on Windows computers. With EViews you can develop a statistical relation from your data and then use the relation to forecast future values of the data. Areas where EViews can be useful include: · Sales forecasting · Cost analysis and forecasting · Financial analysis · Macroeconomic forecasting · Simulation · Scientific data analysis and evaluation EViews is a new version of a set of tools for manipulating time series data originally developed in the Time Series Processor software for large computers. The immediate predecessor of EViews was MicroTSP, first released in 1981. Though EViews was developed by economists and most of its uses are in economics, there is nothing in its design that limits its usefulness to economic time series. Even quite large cross-section projects can be handled in EViews. The basic data object within EViews is the time series. Each series has a name, and you can request operations on all the observations just by mentioning the name of the series. EViews provides convenient visual ways to enter time series from the keyboard or from disk files, to create new series from existing ones, to display and print series, and to carry out statistical analysis of the relations among series. EViews uses the visual features of modern Windows software. You can use your mouse to guide the operation with standard Windows menus and dialogs. Results appear in windows and can be manipulated with standard Windows techniques. Alternatively, you may use EViews' powerful command language. You can enter and edit commands in the command window. -

Gretl User's Guide

Gretl User’s Guide Gnu Regression, Econometrics and Time-series Allin Cottrell Department of Economics Wake Forest university Riccardo “Jack” Lucchetti Dipartimento di Economia Università Politecnica delle Marche December, 2008 Permission is granted to copy, distribute and/or modify this document under the terms of the GNU Free Documentation License, Version 1.1 or any later version published by the Free Software Foundation (see http://www.gnu.org/licenses/fdl.html). Contents 1 Introduction 1 1.1 Features at a glance ......................................... 1 1.2 Acknowledgements ......................................... 1 1.3 Installing the programs ....................................... 2 I Running the program 4 2 Getting started 5 2.1 Let’s run a regression ........................................ 5 2.2 Estimation output .......................................... 7 2.3 The main window menus ...................................... 8 2.4 Keyboard shortcuts ......................................... 11 2.5 The gretl toolbar ........................................... 11 3 Modes of working 13 3.1 Command scripts ........................................... 13 3.2 Saving script objects ......................................... 15 3.3 The gretl console ........................................... 15 3.4 The Session concept ......................................... 16 4 Data files 19 4.1 Native format ............................................. 19 4.2 Other data file formats ....................................... 19 4.3 Binary databases ..........................................