Econometric Theory

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Brendan K. Beare

Brendan K. Beare Department of Economics University of California – San Diego 9500 Gilman Drive #0508 La Jolla, California 92093, U.S.A. Email: [email protected] : http://econweb.ucsd.edu/ bbeare/ ∼ Born: January 23, 1980 Citizenship: Australia & United States Current position 2015– Associate Professor, University of California – San Diego Prior appointments held 2008–2015 Assistant Professor, University of California – San Diego 2007–2008 Research Fellow, Nuffield College and University of Oxford Education 2007 PD in Economics, Yale University 2006 MA in Statistics, Yale University 2005 MP in Economics, Yale University 2004 MA in Economics, Yale University 2002 BE(H) in Econometrics, University of New South Wales Honors & awards 2011–2016 Sir Clive W. J. Granger Chair, University of California – San Diego 2008 George Trimis Prize for Distinguished Dissertation in Economics, Yale University 2007 MA by Resolution, University of Oxford 2007 Dissertation Fellowship, Yale University 2006 Carl Arvid Anderson Prize, Cowles Foundation for Research in Economics 2006 Cowles Summer Prize, Cowles Foundation for Research in Economics 2002–2006 Cowles Prize, Cowles Foundation for Research in Economics 2002–2006 University Fellowship, Yale University 2002 Economic Society of Australia Honours Prize 1 Publications 2019 Beare, Brendan K. and Shi, Xiaoxia. An improved bootstrap test of density ratio ordering. Econometrics and Statistics, 10: 9-26. 2019 Seo, Won-Ki and Beare, Brendan K. Cointegrated linear processes in Bayes Hilbert space. Statistics and Probability Letters, 147: 90-95. 2018 Beare, Brendan K. Unit root testing with unstable volatility. Journal of Time Series Analysis, 39(6): 816-835. 2018 Beare, Brendan K. and Dossani, Asad. Option augmented density forecasts of market returns with monotone pricing kernel. -

Econometrics Oxford University, 2017 1 / 34 Introduction

Do attractive people get paid more? Felix Pretis (Oxford) Econometrics Oxford University, 2017 1 / 34 Introduction Econometrics: Computer Modelling Felix Pretis Programme for Economic Modelling Oxford Martin School, University of Oxford Lecture 1: Introduction to Econometric Software & Cross-Section Analysis Felix Pretis (Oxford) Econometrics Oxford University, 2017 2 / 34 Aim of this Course Aim: Introduce econometric modelling in practice Introduce OxMetrics/PcGive Software By the end of the course: Able to build econometric models Evaluate output and test theories Use OxMetrics/PcGive to load, graph, model, data Felix Pretis (Oxford) Econometrics Oxford University, 2017 3 / 34 Administration Textbooks: no single text book. Useful: Doornik, J.A. and Hendry, D.F. (2013). Empirical Econometric Modelling Using PcGive 14: Volume I, London: Timberlake Consultants Press. Included in OxMetrics installation – “Help” Hendry, D. F. (2015) Introductory Macro-econometrics: A New Approach. Freely available online: http: //www.timberlake.co.uk/macroeconometrics.html Lecture Notes & Lab Material online: http://www.felixpretis.org Problem Set: to be covered in tutorial Exam: Questions possible (Q4 and Q8 from past papers 2016 and 2017) Felix Pretis (Oxford) Econometrics Oxford University, 2017 4 / 34 Structure 1: Intro to Econometric Software & Cross-Section Regression 2: Micro-Econometrics: Limited Indep. Variable 3: Macro-Econometrics: Time Series Felix Pretis (Oxford) Econometrics Oxford University, 2017 5 / 34 Motivation Economies high dimensional, interdependent, heterogeneous, and evolving: comprehensive specification of all events is impossible. Economic Theory likely wrong and incomplete meaningless without empirical support Econometrics to discover new relationships from data Econometrics can provide empirical support. or refutation. Require econometric software unless you really like doing matrix manipulation by hand. -

International Journal of Forecasting Guidelines for IJF Software Reviewers

International Journal of Forecasting Guidelines for IJF Software Reviewers It is desirable that there be some small degree of uniformity amongst the software reviews in this journal, so that regular readers of the journal can have some idea of what to expect when they read a software review. In particular, I wish to standardize the second section (after the introduction) of the review, and the penultimate section (before the conclusions). As stand-alone sections, they will not materially affect the reviewers abillity to craft the review as he/she sees fit, while still providing consistency between reviews. This applies mostly to single-product reviews, but some of the ideas presented herein can be successfully adapted to a multi-product review. The second section, Overview, is an overview of the package, and should include several things. · Contact information for the developer, including website address. · Platforms on which the package runs, and corresponding prices, if available. · Ancillary programs included with the package, if any. · The final part of this section should address Berk's (1987) list of criteria for evaluating statistical software. Relevant items from this list should be mentioned, as in my review of RATS (McCullough, 1997, pp.182- 183). · My use of Berk was extremely terse, and should be considered a lower bound. Feel free to amplify considerably, if the review warrants it. In fact, Berk's criteria, if considered in sufficient detail, could be the outline for a review itself. The penultimate section, Numerical Details, directly addresses numerical accuracy and reliality, if these topics are not addressed elsewhere in the review. -

Hands-On & Exercise: Stata Hands-On: Eviews & Stata

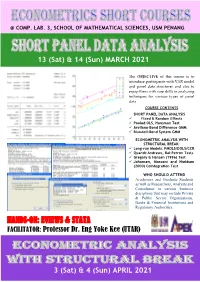

@ COMP. LAB. 3, SCHOOL OF MATHEMATICAL SCIENCES, USM PENANG 13 (Sat) & 14 (Sun) MARCH 2021 The OBJECTIVE of this course is to introduce participants with VAR model and panel data structures and also to equip them with core skills in analyzing techniques for various types of panel data HANDS-ON & EXERCISE: STATA COURSE CONTENTS SHORT PANEL DATA ANALYSIS FACILITATORS: ✓ Fixed & Random Effects ✓ Pooled OLS, Hausman Test Dr Zainudin Arsad (USM) & ✓ Arellano-Bond Difference GMM ✓ Blundell-Bond System GMM Ass. Prof. Dr LAW S. HOOK (UPM) ECONOMETRIC ANALYSIS WITH STRUCTURAL BREAK: ✓ Long-run Models: FMOLS/DOLS/CCR ✓ Quandt-Andrews, Bai-Perron Tests ✓ Gregory & Hansen (1996) Test ✓ Johansen, Mosconi and Nieldsen (2000) Cointegration Test WHO SHOULD ATTEND Academics and Graduate Students as well as Researchers, Analysts and Consultants in various business disciplines that may include Private & Public Sector Organizations, Banks & Financial Institutions and Regulatory Authorities. HANDS-ON: EVIEWS & STATA FACILITATOR: Professor Dr. Eng Yoke Kee (UTAR) 3 (Sat) & 4 (Sun) APRIL 2021 SHORT PANEL DATA ANALYSIS DAY 1 : SATURDAY, 13 MARCH 2021 8:15 AM REGISTRATION 8:45 AM SESSION 1 – THE NATURE OF PANEL DATA ▪ Nature and Benefits od Panel Data; Examining & Arranging Your Dataset 10:30 AM TEA BREAK 10:45 AM SESSION 2 – STATIC LINEAR PANEL MODELS ▪ Panel Data Basics: Pooled OLS, Fixed and Random Effects 12:45 PM LUNCH 2:00 PM SESSION 3 – SELECTING PANEL DATA MODELS ▪ Poolability F-test, Breusch-Pagan LM Test, Hausman Test 3.45 PM TEA BREAK 4.00 PM SESSION 4 – ISSUES ON PANEL DATA MODELS: ROBUST ESTIMATES ▪ Diagnostic Tests and Robust Standard Errors 5:45 PM Q & A (SESSIONS 1 - 4) DAY 2 : SUNDAY, 14 MARCH 2021 8:30 AM SESSION 5 – DYNAMIC PANEL DATA APPROACH ▪ Why Dynamic Panel? 10:15 AM TEA BREAK 10:30 AM SESSION 6 – MULTIVARIATE DYNAMIC MODELS WITH PERSISTENT SERIES ▪ Arellano-Bond Difference Estimator, 1-step vs. -

Rtadf: Testing for Bubbles with Eviews

JSS Journal of Statistical Software November 2017, Volume 81, Code Snippet 1. doi: 10.18637/jss.v081.c01 Rtadf: Testing for Bubbles with EViews Itamar Caspi Bank of Israel Abstract This paper presents Rtadf (right-tail augmented Dickey-Fuller), an EViews add-in that facilitates the performance of time series based tests that help detect and date-stamp asset price bubbles. The detection strategy is based on a right-tail variation of the standard augmented Dickey-Fuller (ADF) test where the alternative hypothesis is of a mildly explo- sive process. Rejection of the null in each of these tests may serve as empirical evidence for an asset price bubble. The add-in implements four types of tests: standard ADF, rolling window ADF, supremum ADF (SADF; Phillips, Wu, and Yu 2011) and general- ized SADF (GSADF; Phillips, Shi, and Yu 2015). It calculates the test statistics for each of the above four tests, simulates the corresponding exact finite sample critical values and p values via Monte Carlo methods, under the assumption of Gaussian innovations, and produces a graphical display of the date stamping procedure. Keywords: rational bubble, ADF test, sup ADF test, generalized sup ADF test, mildly explo- sive process, EViews. 1. Introduction Empirical identification of asset price bubbles in real time, and even in retrospect, is surely not an easy task, and it has been the source of academic and professional debate for several decades.1 One strand of the empirical literature suggests using time series estimation tech- niques while exploiting predictions made by finance theory in order to test for the existence of bubbles in the data. -

What Is in a Word Or Two?

What Is in a Word or Two? Dale J. Poirier Department of Economics University of California, Irvine April 15, 2004 Abstract To measure the impact of Bayesian reasoning, this paper investigates the occurrence of two words, “Bayes” and “Bayesian,” over 1970-2003 in journal articles in a variety of disciplines, with a focus on economics and statistics. The growth in statistics is documented, but the growth in economics is largely confined to economic theory/mathematical economics rather than econometrics. Poirier (1989, 1992) described the penetration of Bayesian articles in econometrics and statistics journals. Data were collected by examination of individual articles and classifying each as “Bayesian” or “non-Bayesian.” Here the time period is expanded to 1970-2003 (when possible), and the number of journals is expanded to include journals in JSTOR (see Appendix) plus some from Elsevier [Journal of Econometrics (JE) and Economics Letters (EL)], the American Statistical Association [Journal of Business & Economic Statistics (JBES)], and Cambridge University Press [Econometric Theory (ET)]. Attention focuses (but not exclusively) on economics and statistics. The data collection exercise is “objectified” by using search engines to compute the annual proportion of journal “articles” containing in their text either the words “Bayes” or “Bayesian.” While not all such articles are “Bayesian,” their numbers provide an upper bound on the number of Bayesian articles, and they capture the impact of Bayesian thinking on authors. Two qualifiers should be kept in mind. First, what constitutes an “article” differs across journals. Some journals [e.g., Journal of the American Statistical Association (JASA)] count comments and replies separately, whereas other journals [e.g., Journal of the Royal Statistical Society, Series B (JRSSB)] count them as part of the original text. -

Introduction to Eviews 2.0

Introduction to EViews 2.0 Overview of product EViews provides regression and forecasting tools on Windows computers. With EViews you can develop a statistical relation from your data and then use the relation to forecast future values of the data. Areas where EViews can be useful include: · Sales forecasting · Cost analysis and forecasting · Financial analysis · Macroeconomic forecasting · Simulation · Scientific data analysis and evaluation EViews is a new version of a set of tools for manipulating time series data originally developed in the Time Series Processor software for large computers. The immediate predecessor of EViews was MicroTSP, first released in 1981. Though EViews was developed by economists and most of its uses are in economics, there is nothing in its design that limits its usefulness to economic time series. Even quite large cross-section projects can be handled in EViews. The basic data object within EViews is the time series. Each series has a name, and you can request operations on all the observations just by mentioning the name of the series. EViews provides convenient visual ways to enter time series from the keyboard or from disk files, to create new series from existing ones, to display and print series, and to carry out statistical analysis of the relations among series. EViews uses the visual features of modern Windows software. You can use your mouse to guide the operation with standard Windows menus and dialogs. Results appear in windows and can be manipulated with standard Windows techniques. Alternatively, you may use EViews' powerful command language. You can enter and edit commands in the command window. -

Gretl User's Guide

Gretl User’s Guide Gnu Regression, Econometrics and Time-series Allin Cottrell Department of Economics Wake Forest university Riccardo “Jack” Lucchetti Dipartimento di Economia Università Politecnica delle Marche December, 2008 Permission is granted to copy, distribute and/or modify this document under the terms of the GNU Free Documentation License, Version 1.1 or any later version published by the Free Software Foundation (see http://www.gnu.org/licenses/fdl.html). Contents 1 Introduction 1 1.1 Features at a glance ......................................... 1 1.2 Acknowledgements ......................................... 1 1.3 Installing the programs ....................................... 2 I Running the program 4 2 Getting started 5 2.1 Let’s run a regression ........................................ 5 2.2 Estimation output .......................................... 7 2.3 The main window menus ...................................... 8 2.4 Keyboard shortcuts ......................................... 11 2.5 The gretl toolbar ........................................... 11 3 Modes of working 13 3.1 Command scripts ........................................... 13 3.2 Saving script objects ......................................... 15 3.3 The gretl console ........................................... 15 3.4 The Session concept ......................................... 16 4 Data files 19 4.1 Native format ............................................. 19 4.2 Other data file formats ....................................... 19 4.3 Binary databases .......................................... -

Eviews 10 Getting Started Eviews 10 Getting Started Copyright © 1994–2017 IHS Global Inc

EViews 10 Getting Started EViews 10 Getting Started Copyright © 1994–2017 IHS Global Inc. All Rights Reserved ISBN: 978-1-880411-36-0 This software product, including program code and manual, is copyrighted, and all rights are reserved by IHS Global Inc. The distribution and sale of this product are intended for the use of the original purchaser only. Except as permitted under the United States Copyright Act of 1976, no part of this product may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written permission of IHS Global Inc. Disclaimer The authors and IHS Global Inc.assume no responsibility for any errors that may appear in this manual or the EViews program. The user assumes all responsibility for the selection of the pro- gram to achieve intended results, and for the installation, use, and results obtained from the pro- gram. Trademarks EViews® is a registered trademark of IHS Global Inc. Windows, Excel, PowerPoint, and Access are registered trademarks of Microsoft Corporation. PostScript is a trademark of Adobe Corpora- tion. X11.2 and X12-ARIMA Version 0.2.7, and X-13ARIMA-SEATS are seasonal adjustment pro- grams developed by the U. S. Census Bureau. Tramo/Seats is copyright by Agustin Maravall and Victor Gomez. Info-ZIP is provided by the persons listed in the infozip_license.txt file. Please refer to this file in the EViews directory for more information on Info-ZIP. Zlib was written by Jean-loup Gailly and Mark Adler. More information on zlib can be found in the zlib_license.txt file in the EViews directory. -

Journal of Econometrics, 133, 97-126 (With R. Paap). • Testing, 2005, Forthcoming in the New Palgrave Dictionary of Economics

Curriculum Vitae Personal data: Name Frank Roland Kleibergen Professional Experience: • September 2003-present: professor of Economics, Brown University • January 2002-December 2007: associate professor University of Amsterdam sponsored by a NWO Vernieuwingsimpuls research grant • April 99-December 2001: Postdoc in Econometrics at the University of Amsterdam • April 96-April 99: NWO-PPS Postdoc Erasmus University Rotterdam • August 95-April 96: Assistant professor, Econometrics Department, Tilburg University • September 94-August 95: Assistant professor, Finance Department, Erasmus University Rotterdam Grants and Prizes: • Fellow of the Journal of Econometrics, 2007 • 2003 Joint winner of the Tinbergen Prize for the most scientifically successful alumnus of the Tinbergen Institute • Acquired a DFL 1.5 million (680670 € = 680000 USD) NWO (Dutch NSF) Vernieuwingsimpuls research grant entitled “Empirical Comparison of Economic models” for the period 2002-2007 • Acquired a DFL 200.000 (90.756 € = 80000 USD) NWO PPS subsidy for 1995-1997 Editorships: Associate editor of Economics Letters Referee of the journals/conferences: Journal of Econometrics, Journal of Applied Econometrics, Journal of Empirical Finance, Econometric Theory, Econometrica, Journal of the American Statistical Association, International Journal of Forecasting, Journal of Business and Economic Statistics, Review of Economics and Statistics, Econometrics Journal, Economics Letters, Program committee member ESEM 2002 and Econometric Society World Meeting 2005. Scientific publications: • Weak Instrument Robust Tests in GMM and the New Keynesian Phillips Curve, 2009, Journal of Business and Economic Statistics, (Invited Paper), 27, 293-311 (with S. Mavroeidis). • Rejoinder, 2009, Journal of Business and Economic Statistics, 27, 331-339. (with S. Mavroedis) • Tests of Risk Premia in Linear Factor Models , 2009, Journal of Econometrics, 149, 149- 173. -

Houtan BASTANI Philadelphia, PA 19143 Nationalities: USA, France, Iran [email protected]

Houtan BASTANI Philadelphia, PA 19143 Nationalities: USA, France, Iran [email protected] EDUCATION MSc Economics, London School of Economics 2008-09 Graduated with Merit B.S. Economics and Computer Science, College of William & Mary 2000-03 Graduated Summa Cum Laude, Phi Beta Kappa College education financed through scholarships, grants, loans and work Candidate for B.S.E. Computer Science Engineering, University of Pennsylvania 1998-00 Transferred FELLOWSHIPS, HONORS AND AWARDS US Fulbright Research Fellow, Italy 2003-04 Elected member of Phi Beta Kappa honor society 2002 Frances L. and Edwin K. Cummings Scholar 2002 NSF REU Program 2001, 2002 Dean’s List 1999-03 WORK EXPERIENCE Research Software Engineer, Dynare, CEPREMAP, École Normale Supérieure since 2009 Focused on development of Dynare, primarily in C++ and MATLAB Programmed o OLS, FGLS, Gibbs Sampling for SUR models, VAR forecasts, … o Interpreter for Dynare’s macro processing language o Dynare's Reporting functionality o Dynare's test suite, run nightly upon commit o Integrated Sims, Waggoner and Zha MS-SBVAR code o JSON and Julia output of preprocessor o among others... Responsible for distribution on macOS: create installation packages and snapshots; created and maintain installation scripts on Homebrew Webmaster http://www.dynare.org Consultant, Organisation for Economic Co-operation and Development (OECD) 2018 Added Gandhi, Navarro and Rivers (2017) module to MultiProd codebase Fixed bug in Stata Gtools Gave class on Git Consultant, Copywrighte Design 2018 Created interactive in-store display using Python and Raspberry Pi Consultant, CQER, Federal Reserve Bank of Atlanta 2011 Worked for Dan Waggoner and Tao Zha, creating an interface for use with their Regime-Switching DSGE models. -

G023) 1 Autumn Term 2007/2008: Weeks 2 - 8 J´Erˆomeadda

M.Sc. in Economics Department of Economics, University College London Econometric Theory and Methods (G023) 1 Autumn term 2007/2008: weeks 2 - 8 J¶er^omeAdda for an appointment, e-mail [email protected] Introduction This course provides students with a foundation in econometric theory and methods. Courses in Microeconometrics and Time Series Econometrics in the Spring Term provide further instruction on speci¯c econometric topics. Many of the other M.Sc. course in economics provide material essential in developing econometric models and a strong motivation for the use of econometric methods. Some of these courses will make frequent reference to the results of econo- metric analysis. Econometric methods are used by academic researchers to develop and test models of economic behaviour and interaction, by govern- ment in the design and evaluation of economic and social policy and by commercial users to understand aspects of the markets in which they oper- ate. Most practicing professional economists, and many academic economists, have to conduct, evaluate, or use the results of econometric analysis on a day to day basis. There has been recent rapid growth in the availability of information on economic phenomena, in the computing power necessary to access and analyse this information, and in the scope and power of econo- metric techniques. As a result there is rapidly increasing demand for people with good econometric skills. 1I am grateful to Andrew Chesher, the previous lecturer of this course to make the teaching material available. 1 Econometrics Econometrics is the collection of tools and methods used to understand and predict economic phenomena.